All posts by Gary.Stockton@experian.com

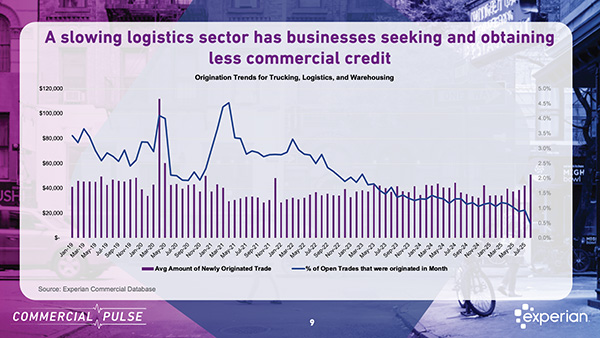

Logistics credit risk is rising according to Experian's latest Commercial Pulse report, signaling financial strain.

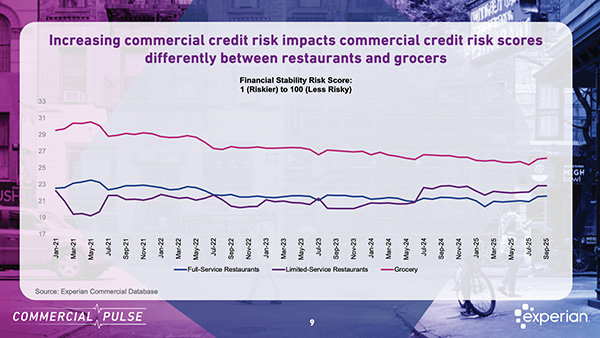

Experian Commercial Pulse Report shows food prices are having a big impact on where and how consumers choose to eat, but also on credit risk.

Experian Small Business Index suggests the US economy is set to expand in the third quarter, spurred on by recent rate cuts.

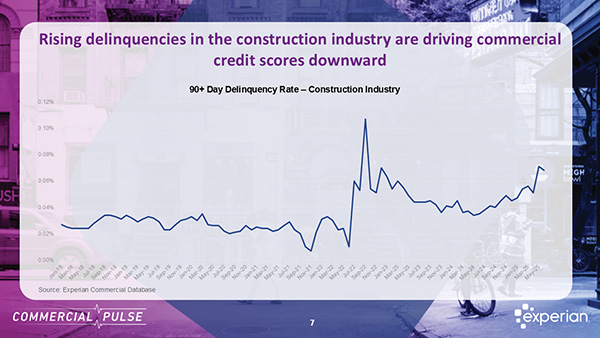

This week Experian focuses on the growing construction industry and early warning risk signals for lenders and risk managers.

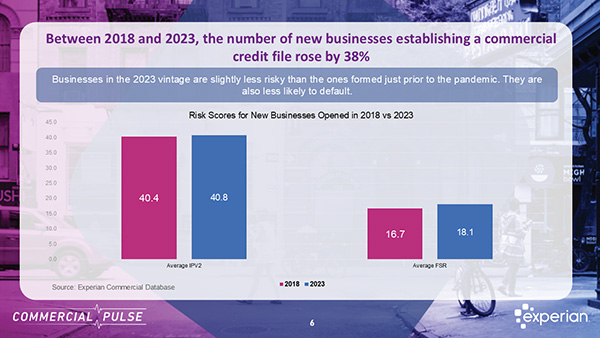

Discover how small businesses have transformed since the pandemic, from digital adoption to growth resilience, in Experian’s latest report.

The Experian Small Business Index™ declined in July to 32.8, down 11.9 points. The index tracks the health of small business owners nationwide

Find out what's really happening on Main Street during the Quarterly Business Credit Review webinar, August 19th, 10am Pacific.

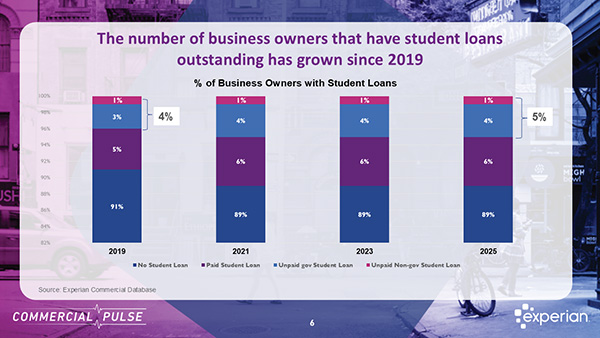

Experian Commercial Pulse Report - Business owners with unpaid student loans carry a higher risk for lenders.

Main Street Report - small businesses are navigating an environment marked by persistent inflation, elevated interest rates, and volatility.