All posts by Gary.Stockton@experian.com

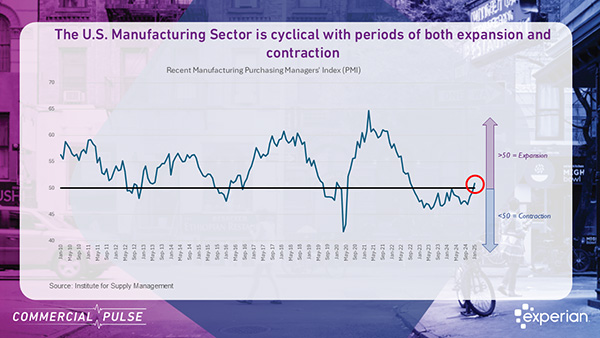

Experian reports the manufacturing sector may be on the verge of a shift after more than two years of contraction | Commercial Pulse Report

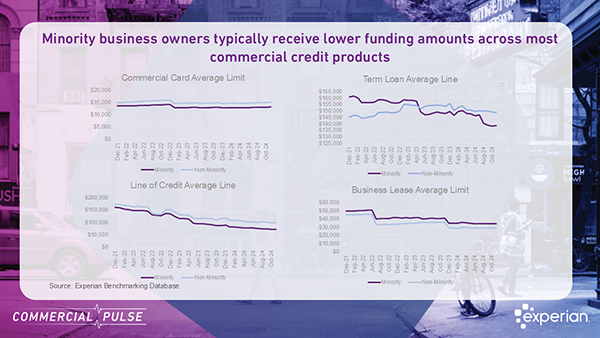

Commercial Pulse Report - minority-owned businesses are booming, yet they face a funding gap. A $2 trillion opportunity for lenders.

Experian Q4 Main Street Report reveals credit trends, lending shifts, and economic forces shaping growth amid policy changes and global uncertainties.

Join the Experian experts for a review on recent small business credit performance Tuesday, March 4th, 10:00 a.m. Pacific

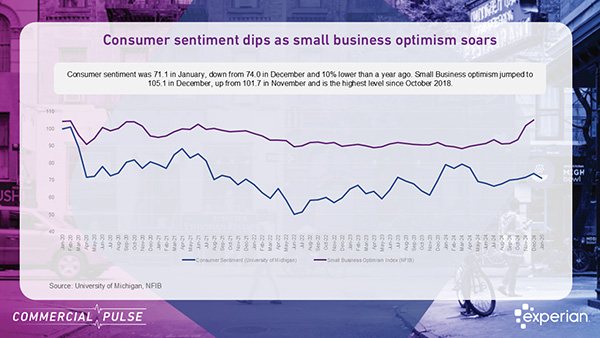

Commercial Pulse Report insights, including small business optimism vs consumer confidence, and the Experian Small Business Index.

The Experian Small Business Index (SBI) declined two points in December to 40.6, following an uptick in November 2025. Follow for updates.

AI is reshaping work, driving small business growth. Discover how AI, corporate shifts, and Gen Z are fueling an entrepreneurial boom.

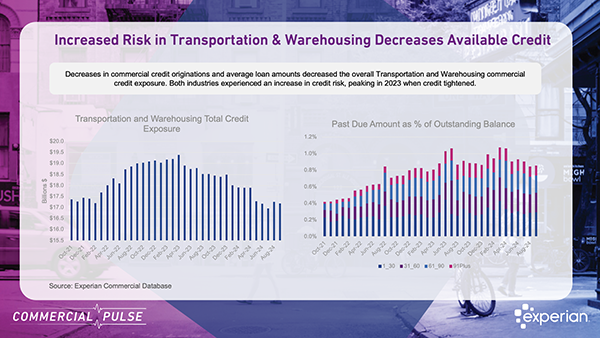

Fresh Insights from the latest Commercial Pulse Report, highlighting growth and credit challenges in U.S. transportation and warehousing.

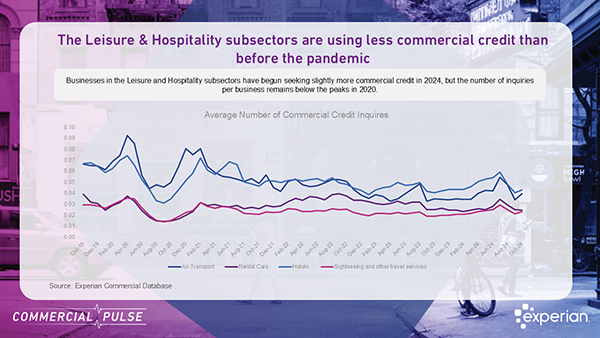

Explore Leisure & Hospitality trends in the commercial pulse report. Insights to help credit managers drive smarter decisions