All posts by Business Information Services

For decades, lenders and others have relied on core credit data focused on financial borrowing and repayment behavior. Many factors go into the decision-making process, including the length of credit history, the number of open accounts, and on-time bill payments. What happens when a consumer or small business owner relies on cash for financial transactions or has never held a mortgage or a business loan? A significant portion of the U.S. adult population faces this problem. According to a 2020 report by the Federal Reserve, as many as 21 percent of U.S. consumers survive without a credit card. As a result, the traditional credit-scoring model doesn't tell the full story of their financial health, and they could be labeled “credit invisible" or “unscored" due to limited access to credit. It's both a personal and business problem. For consumers, that might mean not being able to secure a mortgage, insurance, or even be considered for a job. Start-ups and small businesses, meanwhile, may not be able to access credit to fuel their future growth and success. The recent explosion of new business filings brings the challenge of credit access to a head. Because small and emerging businesses can lack sufficient credit histories to qualify for credit on their own, they may rely on the owner's personal credit profile for lending decisions. Yet, some small businesses continue to struggle to get financing. It's especially pronounced in communities of color. For example, Black-owned businesses get turned down for bank financing at twice the rate that white-owned businesses do, according to the Federal Reserve. Technological innovations such as Experian's Experian Boost are shaking up the conventional scoring system by bringing in alternative credit factors to fill out the credit picture. For lenders, the emergence of alternative data, otherwise known as non-traditional data, helps them make informed business credit decisions among a wider number of customers and prospects. What is non-traditional data? Traditionally, lending and other credit decisions have been based on factors such as credit history and on-time payments. That can allow people and businesses that do not have a lot of cash but can demonstrate good repayment behavior to borrow. However, it's quite another story when the situation is flipped. Some consumers and businesses don't utilize financial products, though they might have healthy cash flow. As a result, they lack the necessary data to generate a credit score, making them appear to be unattractive credit risks. Non-traditional data is an important way to give consumers access to better rates and open up borrowing to more consumers and businesses. This data can include things like rent and cell phone payments, giving lenders a broader range of information to consider. According to FinRegLab, 96 percent of U.S. households have a bank account or a prepaid card and 91 percent of U.S. adults have at least one utility account in their names. Overall, including other credit data, in addition to core credit data, would bring more people into the credit system. Including non-traditional forms of data can create financial inclusion for consumers and businesses. Where does non-traditional data come from? Non-traditional data is generated by aggregators that scour utility accounts, public records and property information to understand the financial activities of consumers. It considers a wider range of financial behaviors than what just appears on a credit report. These can include: Rent payments Utility payments Employment verification Bank account information, including recurring payroll deposits, average account balances and withdrawal activity. Property records Non-traditional credit data goes one step further and supplements this data with information on consumers' use of alternative lending arrangements such as payday loans, small-dollar credit lenders, auto financiers, rent-to-own, retail financing, and others. Commercial lenders can also take advantage of technological innovations to gather non-traditional data for lending decisions, which can drive more approvals and greater profits. For businesses, non-traditional credit data can include: Social media: How many user check-ins and reviews is a business getting on social media? That can say a lot about its business. Experian Social Media Insight™ provides a social media view to help lenders better score business borrowers with thin credit profiles. Online financial activity: An uptick in PayPal or Venmo transactions can suggest healthy cash flow. Bank details: Borrowers can permit lenders to view their business banking account, which shows how much cash on hand they have. Accounting software: With direct access to QuickBooks or FreshBooks, lenders can make determinations about a potential customer's financial health in real-time. Shipping information: For businesses moving products, analyzing shipping data allows lenders to make assumptions on cash flow. How is non-traditional data currently used? Financial institutions have become receptive to other credit data sources to provide additional insights. That can improve the accuracy of credit scoring and allow lenders to find more creditworthy consumers. According to Experian's 2020 State of Alternative Credit Data report, 96 percent of lenders believe that during times of economic stress, non-traditional credit data allows them to more closely evaluate consumers' creditworthiness and reduce their credit risk exposure. By deeming more consumers creditworthy, financial institutions can increase financial inclusion, while uncovering new lending opportunities for themselves. Modern tools make that possible. For example, Experian's Clarity Services provides insights on more than 62 million U.S. consumers, helping lenders better assess and manage risk. Lenders can see consumers' utilization of alternative finance and payment behaviors for a more holistic view of their creditworthiness. How can non-traditional data be used to calculate credit risk? Non-traditional credit data can help lenders gain deeper insights into their borrowers to better assess risk. For starters, it allows them to spot creditworthiness trends in real-time, rather than a snapshot in time that traditional credit data typically provides. A deteriorating financial position among prime customers and signs of improvement among marginal customers can be spotted faster with a combination of traditional and non-traditional data. Also, some consumers may appear to be “risky" through the lens of core credit data but may prove less so when non-traditional data points are included. For example, according to FinRegLab research, cash flow data can be predictive of credit risk, not just credit utilization and history. Owner-permissioned data lets consumers decide what lenders can see when making their credit determinations. For instance, lenders who use only traditional data might see an account that has been turned over to collections. With owner-permissioned data, on the other hand, a lender can also see a record of paying rent and cell phone bills on time. As a result, lenders can evaluate both types of behaviors in their credit decision, providing them with a fuller picture. Looking at how consumers leverage alternative financial products to manage debt can also reveal responsible credit-management behaviors. Consumers who appear to be low-risk in the eyes of traditional credit data may actually be riskier if they do not manage their alternative finance products well – an activity that doesn't appear on most credit reports. The challenges of non-traditional credit data Non-traditional credit data has the potential to open the world of credit to underserved communities. For lenders, it can unlock opportunities by bringing in a wider range of potential customers. But it's important to recognize that there are challenges too. For starters, lenders are still figuring out how to incorporate it into their lending decisions. While non-traditional credit data has always been available, big data collection now makes it easier to access. As lenders and regulators become more comfortable with its use, they will begin to incorporate it into credit decisions, while also being aware of its limitations. Consumers, meanwhile, may have data security and privacy concerns about how their information will be used and who may have access to it. The Consumer Financial Protection Bureau is working on guidelines that ensure that lenders are using data appropriately and fairly. Related Posts

This weeks guest post is by Katie Keitch, VP of Commercial Services at InsideARM. InsideARM is a media company who specializes in training for credit management professionals. To receive future articles, sign up to the InsideARM newsletter. Katie Keich, V.P. Commercial Services InsideARM It's 2019, we have IVR systems that sound like you are talking to a human. We have AI technology that can analyze and form collections treatment. We can process payment via SMS messaging. Is it silly to think that the "right" letter strategy could possibly outperform a live collector? A letter series is delivered most commonly today using e-mail and/or through the customer's account portal. Let's dig in. In my travels and conversations, a very succinct theme is the question, "Who collected the money? Did my collector's efforts bring in the cash? Or was it something else?" Often businesses can't be 100% sure if it was a collector's efforts that brought the money in or not. Did the customer just pay the bill on their own because they suddenly could afford to? How much of the money was recovered by no one making a call? Could a letter strategy replace a collector, or should it enhance the collector's efforts? These questions are normal things to consider. As a credit and collections leader, I think it's always important to give your collectors the ability to utilize as many resources and tools to enhance their efforts. Step One: Is your current letter strategy set up to aid the collector's efforts or compete with the collector? Are you using the letter strategy in tandem with a collector's dials or instead of their dials? You must decide if a letter series is going to replace the collector's efforts or if it is going to be assisting there collection efforts. Quick Exercise: If you'd like to put your collectors' efforts to the test, discontinue the use of customer touches via letter strategy. Create an escalated letter series that runs without a collector making a phone call. I would measure it for 60, 90, and 120 days and measure the collector's recovery rate. Is the collector performing at lower, higher or the same rate of recovery? How did the customers that never got phone calls and only got the letter series perform? How much cash came in without a collector calling? Step Two: Is your current letter strategy saying the same thing each time or does it have escalated intent in the verbiage? If you want to make the most of your letter series, they should look and sound different. Letter 1- Should be sent about a week before the invoice is due and include a copy of the invoice. This way, if they lost or didn't receive, the invoice for the first time, you are automatically re-sending. Letter 2- Should be sent a week after the invoice is due, notifying the customer you haven't received payment. If they want to avoid late fees, maximize discounts with you, etc. they should process payment immediately online. If you are sending this via email or pop-up message on their portal, the link should be included to process payment. Automatically offer the customer the discounted rate if they process payment before end of business day. If you don't have a payment portal, honor the discounted pricing with payment process via phone that day. Letter 3- Should be sent approximately 10 business days after letter 2 if payment still hasn't been received. You should be mentioning possible service interruption, loss of discounts and/or late fees if unresolved. You want it to be clear that the account is in jeopardy of service interruption if not resolved within 5 business days. Step Three: Does your letter strategy have dates and accountability? You want to ensure that urgency can be read in the tone and verbiage chosen. It shouldn't be open ended, and it should always offer the customer the ability to resolve the delinquency. If they haven't filed an invoice dispute with you by now, that's a problem. If you don't receive the payment be prepared to temporarily disrupt service. Letter 4- Should be sent approximately 5 business days after letter 3 if payment hasn't been received. You should include a date for service interruption, loss of discounts and/or late fees, and mention reporting the delinquency to the credit bureaus. Quick tip: If you want the customer to make you a priority than you should be reporting your delinquent customers monthly. You can set up to automatically send an aging report to the credit report providers. This is a great tool to help the customer in making you a priority for payment. Step Four: Does your letter series clearly communicate the penalties if payment is delinquent after service interruption? Does the customer understand if you have to send them to a third-party collection agency that they will incur additional costs? Letter 5- Should be sent 5 business days after letter 4. It should include an incentive to pay you immediately. However, it should clearly state if payment isn't received the incurred actions taken and fees associated. This should be your final demand for payment. My recommendation is for the letter strategy to be used in addition to collector calls. If you want to maximize the efforts of your collectors than you should use a dual strategy. Many organizations use a dual strategy today but don't sleep on the fact that you could have a very effective letter series, if developed and executed properly. Business Chat | LIVE Watch the interview we did with Katie Keich of InsideARM on best practices in planning your first collections call with your delinquent customer.

This weeks guest post is by Katie Keitch, VP of Commercial Services at InsideARM. InsideARM is a media company that specializes in training for credit management professionals. To receive future articles sign up to the InsideARM newsletter. Oftentimes organizations miss out on higher bad debt recoveries. The number one reason this happens is that they hold on to the debt for too long. It’s important in the onboarding process to start with the end in mind: setting yourself up for success by having mutually agreed payment terms, billing cycle, right party contact information, etc. However, even if you have done that all correctly from the start, some customers, unfortunately, aren’t able to pay for one reason or another. Here’s how to know when to cut bait and enlist the help of a 3rd party collections agency. Don’t ignore the warning signs Your customer isn’t paying within the agreed payment terms. Or maybe they were paying on time, but lately they have been pushing farther and farther out. Your customer is showing past due more often and/or farther past due than historically Your customer hasn’t paid you in the last 45+ days Your customer is 60+ day’s past due to their mutually agreed payment terms Your customer made broken promises to pay Your customer stopped taking your phone calls Your customer’s emails are suddenly not going through or the physical mailing address is returning mail to sender Be proactive in your communication Don’t be afraid to ask how things are going, especially if you noticed they are outside their normal payment cycle. Immediately offer alternative options instead of having to pay you the full past-due amount today. Set the expectation that it’s vitally important that they keep the communication lines open. If they have something come up, they need to call you. And always answer your calls. You have to be blunt and purposeful in your approach here so that they understand the commitment to you. Offer some alternative options While it’s so important that your customer takes your calls, it’s equally important to give them attainable goals. If they feel that they have options, they are more likely to keep the lines of communication open. Alternative options might include things like offering the ability to make a small weekly payment towards the balance. Offer your customer the ability to continue doing business with you while making payments. The best way to accomplish this is to set the expectation they must remain current on the new invoices. Make the weekly payments smaller so they are able to keep to the commitment. Your customer can always call you and make additional payments. However, it's important that they stick to their original commitment. Ask your customer what is the dollar amount they can afford to pay weekly (hopefully automatically)? If the dollar amount is less than their normal spend, this is a sign that they can’t stay active as a customer. Give them the option to use alternative vendors until they can cover their average invoices plus the delinquent amount. Your stakeholders in Sales may not be immediately supportive. but they will thank you in the long run. Especially if they have chargebacks or are commissioned on collected revenue. Last, in my experience, customers appreciate that you recognize and don’t want to see them get to a place of debt they can't repay. The snowball effect of continuing to let a customer who can’t pay continue billing can be detrimental. No one wins, if your customer files for bankruptcy or worse, go out of business. Recommended exercise, review customers that haven’t made a payment to you in the last 45 days. These should be a top priority for collections. Make your goal to be first in line not last Don’t miss out on collecting because you waited too long to send an account. If you are working with a 3rd party collections agency, do you have an easy process for your collector to recognize it’s time to cut bait? Are the collectors being trained to recognize the warning signs and make quicker decisions? Don’t let your customers get into the 90 and 120-day buckets. They should already be with your third-party agency at that point. That is if you want an opportunity to recover the debt and fast. If you are using the steps outlined above, you should be seeing higher recoveries.

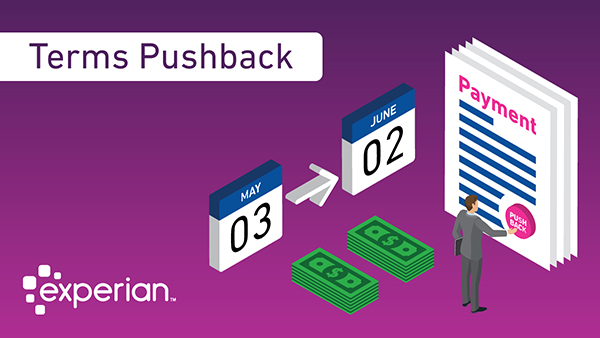

In this week's guest post, Scott Blakeley shares perspectives on a growing trend in business - Terms Pushback (TPB). Scott is the founder of Blakeley, LLP, a noted expert in the field of creditors’ rights, commercial law, e-commerce and bankruptcy law. Scott regularly speaks to industry groups around the country and via monthly webcasts on the topics of creditors rights and bankruptcy. After a slow sales quarter, a large retail clothing store needs to improve their working capital and cash flow. Before the 2008 recession, the retailer likely would have turned to traditional business credit options. However, after the downturn, lenders changed their qualifications and terms, making traditional credit options a much less desirable option. In some cases, retailers, especially midsize or new businesses, can no longer even qualify for traditional credit sources. Businesses are now increasingly renegotiating their payment terms with suppliers through a program called Terms Pushback (TPB). When a jewelry retailer reviews its payment terms, for example, it sees that the main vendor supplier for jewelry currently requires payment 15 days after delivery. As a deliberate strategy — which is different from a company not having the money to pay its bill — to give the retailer more working capital, they reach out to ask the supplier to change the terms to 30 days. This means they would have access to the money paid to the vendor for 15 days longer; this process is often referred to as trade credit. Credit Today found that the most common extension is for 16 to 30 days, with 45% reporting this range as the most common extension. Impact of Terms Pushback on Suppliers While TPB improves cash flow for customers, it causes issues for suppliers because they must wait longer for their payment. Many consultants are now actively recommending TPB as a best practice. Because international companies more commonly using this strategy, many U.S.-based companies are adopting it due to international influence. Companies operating as middlemen between retailers and manufacturers often face the biggest challenges. Longer terms mean that they have less capital to buy more products and have a higher number of outstanding receivables. Additionally, businesses have lower cash conversion metrics, which can hurt publicly traded companies and cause concern for shareholders. According to Credit Today Bench-marking, 19% of suppliers always or usually say no to requests for extended terms, and 3% usually agree. Interestingly, 4% report that their answer depends on customer size — yes to large customers and no to small customers. However, the majority (63%) of businesses review the requests on their individual merits. However, denying the request often has long-term ramifications. If the business denies the request, the customer must pay or suffer credit damage. Customers often get around this by paying late enough to improve their own cash flow but before credit damage occurs. Even more challenging, suppliers are often hesitant to report customers to credit bureaus because this often permanently damages or even ends the relationship. If a supplier denies the request, the majority of options to get the payment are punitive. For example, the supplier can charge a late fee for payment. However, the customer may still decide that the value of the money for the extra days is worth more than the late fee. Other avenues include implementing a credit hold, having two price lists, terminating credit, firing the customer and reporting the customer to industry groups. However, each of these options permanently damages and probably ends the customer relationship, which may result in loss of a high volume of sales. Effectively Managing Terms Pushback with Supply Chain Finance Programs Supply Chain Finance programs are asset-based lending programs structured to improve a customer’s payment terms, reduce costs and improve cash flow enabling financial institutions to pay suppliers for invoiced services. Suppliers can benefit from SCFP as it receives payment within normal terms or earlier which helps keep the credit team’s credit scoring and risk models consistent. The customers benefits as well as their capital is not tied up in day-to-day operational payments and creates more reinvestment opportunities. When a company receives a TPB request, the first step is evaluating the customer — their credit, the risk, the volume of business and the value of the relationship for the supplier. Often, larger companies have an advantage over smaller companies when negotiating term extensions because their business relationship is worth more to the customer than the monetary value of the shorter term. Here are three best practices to managing TPB requests: Offer incentives for shorter terms. Instead of punitive actions, consider giving customers who pay within shorter terms a discount or an annual volume discount for consistent payment with shorter terms. Actively monitor threshold for customers with extended terms. Suppliers must effectively manage their own cash flow to make payroll and other expenses. By extending too many customer terms, suppliers can jeopardize their own financial stability. Create a team to evaluate requests. By establishing a process to handle the requests and a team to formally evaluate requests, suppliers can more effectively evaluate all aspects of the decision, such as the risks of extending to its own financial health and the risk of losing the client relationship. With a team made representing stakeholders from different departments, all perspectives can be represented and considered. As TPB becomes more common as a strategy, suppliers must proactively create a process to manage requests. Often, extending the terms can improve the customer relationship and even increase the amount ultimately paid. By creating a team and strategy, suppliers can make the smartest decision and actively manage pushback requests. Scott Blakeley is a founder of Blakeley LLP, where he advises companies around the United States and Canada regarding creditors’ rights, commercial law, e-commerce and bankruptcy law. He was selected as one of the 50 most influential people in commercial credit by Credit Today. He is contributing editor for NACM’s Credit Manual of Commercial Law, contributing editor for American Bankruptcy Institute’s Manual of Reclamation Laws, and author of A History of Bankruptcy Preference Law, published by ABI. Credit Research Foundation has published his manuals entitled The Credit Professional’s Guide to Bankruptcy, Serving On A Creditors’ Committee and Commencing An Involuntary Bankruptcy Petition. Scott has published dozens of articles and manuals in the area of creditors’ rights, commercial law, e-commerce and bankruptcy in such publications as Business Credit, Managing Credit, Receivables & Collections, Norton’s Bankruptcy Review and the Practicing Law Institute, and speaks frequently to credit industry groups regarding these topics throughout the country. He is a member on the board of editors for the California Bankruptcy Journal, and is co-chair of the sub-committee of unsecured creditors’ Committee of the ABI. Scott holds an B.S. from Pepperdine University, an M.B.A. from Loyola University and a law degree from Southwestern University. He served as law clerk to Bankruptcy Judge John J. Wilson. He is admitted to the Bar of California.

For credit and risk managers, how effectively you manage your book of business can sometimes be the difference between tirelessly chasing after accounts for collections or proactively growing your portfolio. Though there may be many factors that affect your specific credit risk management process, the underlying goal to reduce and manage your exposure to risk does not change. To help you successfully manage your portfolio, we address 4 common mistakes you need to avoid: 1. Not automating your processes By not having an automated, standardized method of assessing your current accounts, overall portfolio exposure to risk increases substantially. The manual review process relies too much on shrinking human capital, requires more time to complete, and can cause inconsistencies across the board. Automating processes where you can will help you focus your resources to the applications and accounts that need attention or manual review. 2. Not setting up triggers that alert you of key events When you know problems are coming, you can take steps to protect yourself and your business. The sooner you know about something, the faster you can act on it. Setting up triggers that notify you of key changes within your customers’ accounts like a rise in late payments, increased number of collection filings, or bankruptcy filings, allows you to keep a close eye on your customers and take immediate action, if necessary. Especially when your portfolio outgrows your resources to manage it, setting up automated triggers can give credit and risk managers the foresight to manage proactively, rather than reactively. 3. Not monitoring for risk (or growth) Managing a large portfolio can be extremely labor-intensive if you don’t apply risk scoring. A traditional risk score, in this case, usually considers the credit, public record and demographic attributes of the account, and applies a value to the results as a means of quantifying risk. This helps you prioritize your time and efforts on the minority of customers with scores that signify increased credit risk, rather than all your customers at the same time. On the flip side, you can target accounts with positive scores for growth opportunities. 4. Not segmenting your portfolio Another common mistake that many portfolio managers make is not segmenting their portfolios to identify insights at a macro level. For instance, leveraging data to segment your customers and accounts by industry, business type, business size, etc., can help you uncover hidden trends not obvious otherwise. This then allows you to apply appropriate treatment strategies to mitigate risk within the accounts. Additionally, you can identify market opportunities for growth using SIC/NAICS codes and other marketing data sources to grow your footprint. Want to talk to an Experian expert regarding your portfolio management strategies? Contact us today.

This week, we invited Charles H. Green to offer his perspectives on the online marketplace lending sector. Charles is Managing Director of Small Business Finance Institute, which provides professional training to commercial lenders for banks and nonbanks. He has written extensively about the marketplace lending sector, including the recent Banker’s Guide to New Small Business Finance (John Wiley & Sons, 2014). Earlier in his career, he founded and served as President/CEO of Sunrise Bank of Atlanta. The evolution of commercial lending over the past seven years has certainly had its share of ups and downs. Remember the ominous days leading up to the financial crisis when it seemed like everything was teetering on collapse? In the end, and more than five hundred bank failures later, the economy found a very slow path back to growth. During that uncertain time, commercial lenders took a lot of criticism from several directions. Regulators were skeptical of the risk level that lenders accepted, borrowers argued when their credit score did not qualify them for a loan and seemingly everyone else had an opinion on how long it took to turn lending volumes around. On top of those worries, a new channel emerged, “online marketplace lending.” These new lenders funded loans from technology platforms that turned around loan applications in very short order, seeming to best banks at their own game. Fast forward several years, and traditional lending has had plenty to cheer about, even if not recognized in the broader economy. The bank failures largely have been resolved, making some of the healthy surviving banks much larger and eliminating some competitors in many markets. Additionally, bank profits are back up as balance sheets have been mostly cleared of underperforming credits, with a renewed focus on good underwriting and solid risk management. Banks Have Advantages This new phenomenon known as online marketplace lending has grown dramatically on the strength of loans that traditional banks have had difficulty serving in the past: small, unsecured working capital loans to service and retail businesses. By performing the sorely needed task of scaling smaller business loans, online marketplace lenders have strengthened many small companies that were otherwise unable to secure financing from banks. However, banks never lost their core strength: their customers. While deregulation gave rise to competitors from a long list of bank services and products, few small-business owners left their banks behind entirely. During the crisis, many companies flocked back to the safety of the federally insured deposit system. Online marketplace lenders may augment but never replace those kinds of relationships. Another advantage large banks have is a strong tie with local businesses. While online lenders can respond quickly to application requests with the latest digital efficiency, their capacity to forge direct relationships is often limited to the term of their outstanding loan. Once repaid, they must restart the cycle to convince clients to borrow again. Banks, on the other hand, offer dozens of products and services that can help small business owners manage everything from business finances, household purchases, retirement savings, auto loans, safe deposit boxes, etc. Most online lenders offer a shorter product list, with options intended to serve a specific customer demographic. Perhaps the most significant advantage banks carry is their degree of flexibility. While online marketplace lenders can leverage the many benefits of a digital platform, there is often only one way to apply for a loan. Many online lenders lose business when an applicant falls outside their parameters. Finally, banks offer flexibility to negotiate around certain conditions or requirements that may bear consideration of alteration. There are people at various levels who can waive some rules or make exceptions when warranted. Given their similarities (looking for business among the same customer prospects) and differences (average loan size, structure and underwriting), banks and online marketplace lenders have the perfect opportunity to forge cooperative arrangements to exchange business. Imagine there is a bank president with a 50 percent loan-to-deposit ratio who is starved for a larger book of earning assets. Perhaps he needs assets from some areas that came up weak in his Community Reinvestment Act (CRA) examination? Maybe his loan product mix is too heavily reliant on big Commercial Real Estate (CRE) loans, but he struggles to book small credits profitably due to the boarding cost? What if he could go to a trusted online marketplace dashboard and search for loans to buy based on a transparent credit grading matrix, with adequate returns commensurate with the risk? Maybe he could even target specific ZIP™ codes to invest funds in places he is lacking market presence. Small-business loans, consumer loans, student loans — they’re all there, and more lines are on the way. Online lenders are nonbank entities that finance much in the same way as banks. A considerable portion of their capital must be invested in their proprietary digital capacity, so when lending grows, many are scrambling for funding. Most of them fund this volume with either revolving lines of credit, securitization or by selling off loans/portfolios to investors. The interesting part is that nothing should stop a commercial bank from participating in any of these activities. There are plenty of opportunities for banks to engage with the marketplace for profitable results with manageable risk. Banks can buy portfolios or loans, refer loan applicants, use the online lender’s proprietary technology to underwrite and fund certain loans, or participate with lender finance, which has been a common practice for alternative lenders for decades. Each type of financial institution has its own inherent advantages. However, playing to the strengths of the online marketplace and banks alike enables both types of entities to open new pockets of opportunity — a situation that may lead to a faster path for economic growth. Related articles Just how alternative are today’s online marketplace lenders? How online marketplace lenders are changing the rules of small-business finance Self-Regulatory Program for Nonbank Small Business Lenders Top regulatory priorities for commercial lenders Playing to Your Strength - Opportunities for Regional Banks to Build Better Lending Portfolios Game Changer - How Marketplace Platforms Are Bringing Financial Institutions Back to Small-Business Lending Marketplace Matchmakers - How Loan Aggregators Bring Borrowers and Lenders Together New Frontiers - What's Next For Marketplace Lending?

This week, we invited Charles H. Green to offer his perspectives on the online marketplace lending sector. The following article is his contribution to our series on marketplace lending. The phrase “man bites dog” is an aphorism in journalism that describes how an unusual, infrequent event (such as a man biting a dog) is more likely to be reported as news than an ordinary occurrence with similar consequences, such as a dog biting a man. In other words, an event is considered more newsworthy if there is something unusual about it. Thus, the headline above likely will draw more attention than the same story with the headline “Hedge fund offers to refinance consumer loans for 7 percent APR.” While both parties might actually own a portion of the same loan portfolio in today’s “sharing economy,” known in financial services as “peer-to-peer lending,” this kind of loan is one of many that have evolved on the Internet under the new financial industry sector labeled “marketplace lending.” Online marketplace lenders, funders, and investors have caused quite a stir over the past couple of years by offering alternative financing products and platforms to serve consumers and businesses that may have trouble securing a loan from traditional financial services, i.e., banks. But what’s so radically different about what they do, other than using a Website rather than a drive-up branch to initiate a financial relationship? After all, don’t both extend money to another party with strings attached — that is, conditions about who gets the money, how much and when they promise to repay it, as well as the consequences if they don’t? It seems like a better “alternative” would be to simply win the lottery! In fact, there is plenty of “alternative” in alternative lending, and in a relatively short period of time, the results have been phenomenal for consumers and businesses alike. What’s so different? For starters, the submission process for loan applications varies greatly. Due to supervisory oversight of the industry and a conservative lending culture, applying for a bank loan often means that a more complete disclosure of personal and business information is required. The aftereffects of the Great Recession and housing bubble meant that many banks curtailed most lending altogether until their balance sheets recovered, On the flip side, online lenders process applications with very little information —generally about 40 data points. This is because these lenders leverage the information and often ask for a borrower’s authorization to gain access to the cloud, where they can acquire more data on a borrower. Furthermore, online lenders have a narrow focus on where they are willing to lend money, so their decision analytics focus more precisely on a smaller set of information that really determines the risk for that particular type of loan. This leads us to how online lenders make credit decisions. Most use proprietary algorithms that weigh various data collected from a borrower’s application and reach a decision based on the numerical score produced at that time. There’s little human intervention to sway the verdict positively or negatively since the decision matrix was developed by testing millions of blind data files with historical loan outcomes to measure and manage their exposure to credit loss. There are plenty more differences in the online lenders’ approach, but probably none more important than the customer experience. Online loan applications can be submitted 24-7, and a borrower will be “conditionally qualified” or declined usually within minutes. Final credit approval often comes within a couple of hours, and funding might be in 48 to 72 hours. How can they do it? The answer lies primarily within four factors: 1) These companies are driven by innovation, with technology used to address many aspects that we don’t like about traditional lending; 2) Online lenders are not banks, and as such, they are relatively free of the regulation that comes with accepting public deposits to fund their operations; and 3) By focusing on a smaller niche of prospective borrowers, online lenders don’t try to be everything to everybody but rather specialize to serve a smaller set of clients better. 4) These companies have developed niche products to satisfy the particular needs of each market. What happens next? Is the end of commercial banks as we know them at hand? No. While the rise of online marketplace lending has been meteoric and the industry climbed to an admirable $9 billion of funding in 2014, it is a very small portion of the trillions of dollars funded by traditional banking today. Still, what they do is attract plenty of attention in the trade. Expect to hear more about strategic partnerships, acquisitions, and other flattering forms of imitation, as the banking industry will adopt and adapt many of the inspiring improvements brought by the online marketplace lending sector. Both sides will win, but the real prize goes to consumers and small-business owners who will have a more robust and competitive environment to get financing capital in the years ahead. About Charles H. Green Charles is Managing Director of Small Business Finance Institute, which provides professional training to commercial lenders for banks and nonbanks. He has written extensively about the marketplace lending sector, including the recent Banker’s Guide to New Small Business Finance (John Wiley & Sons, 2014). Earlier in his career, he founded and served as President/CEO of Sunrise Bank of Atlanta. Related articles Just how alternative are today’s online marketplace lenders? How online marketplace lenders are changing the rules of small-business finance Self-Regulatory Program for Nonbank Small Business Lenders Top regulatory priorities for commercial lenders Playing to Your Strength - Opportunities for Regional Banks to Build Better Lending Portfolios Game Changer - How Marketplace Platforms Are Bringing Financial Institutions Back to Small-Business Lending Marketplace Matchmakers - How Loan Aggregators Bring Borrowers and Lenders Together New Frontiers - What's Next For Marketplace Lending?

Building financial capability and improving access to credit is essential for economic growth in our country. This is especially true for entrepreneurs, many of whom rely on their personal consumer credit standing when applying for a loan for keeping their small businesses strong or for a capital injection to expand their operations. While commercial lending has made a steady increase since the height of the recent economic recession, a recent report from Experian finds that women business owners continue to trail their male counterparts when it comes to commercial and consumer credit scores. Gender gap in access to both commercial and consumer credit The findings make clear that a gender gap exists in both commercial and consumer credit files: The average commercial credit score for a woman-owned business is 34, while the average score for a male-owned business is 35; The average consumer credit score for women business owners is 689, compared to 699 for male business owners; More than 22 percent of male-owned businesses have at least one open commercial trade line, while the same can be said for only 18.5 percent of women-owned businesses; In the last 24 months, female business owners had an average of 1.3 personal accounts become 90-plus days past due, while male business owners had an average of .9 go delinquent. This has a direct and quantifiable impact on the bottom lines for women-owned businesses. For example, Experian’s analysis found that more than 24 percent of male-owned businesses have sales that exceeded $500,000, while only 14.5 percent of women-owned businesses see sales of that size. In addition, 21.2 percent of male business owners have a personal income of $125,000 or greater, compared to just 17.4 percent of women business owners. Policymakers recognize the need to improve credit access for women-owned businesses Developing sound public policy to improve access to credit — especially for women and minority-owned business owners — is a top priority for policymakers in Washington, DC. In July 2014, then-Senate Small Business Committee Chair Maria Cantwell (D-Wash.) released a report, entitled “21st Century Barriers to Women’s Entrepreneurship.” The report took a wide-ranging look at some of the challenges that women face in starting a business. In particular, it found that “$1 of every $23 in conventional small business loans goes to a woman-owned business.” Look for legislative proposals to aide small business owners Look for Congress to continue to discuss policy proposals aimed at increasing access to fair and affordable credit for consumers and small business owners alike. One such proposal that has garnered bipartisan support would make it easier for utilities and telecommunication providers to report positive, on-time credit data to the nation’s credit bureaus. While they have long made pricing decisions based upon the full-file credit data furnished by traditional creditors, like lenders and retailers, telecommunication and utility companies have historically only furnished derogatory data, such as when an account is in collection. Including both positive and negative data from these sources will enable tens of millions of thin-file consumers — and small business owners — with a proven record of meeting monthly financial obligations to access fair and affordable credit. Experian welcomes the opportunity to work with policymakers to help improve access to fair and affordable credit for consumers and small business owners alike. Resources for business owners Understanding and monitoring their company’s business credit profile to ensure it is in good standing is essential for small-business owners to gain access to necessary capital. With the insights that business credit reports provide, small-business owners can take the appropriate actions necessary that will positively impact their business. Experian provides some helpful resources to help small-business owners gauge the health of their business, including: BusinessCreditFacts.com — An authoritative source for understanding and learning about the benefits of managing business credit. Visit http://www.businesscreditfacts.com. Experian Business Credit — A site that enables small-business owners to access a copy of their business credit report as well as understand the impact that maintaining a positive credit profile can have on a small business. Visit https://www.experian.com/businesscreditreport. Business Score Planner™ — An education tool for business owners to understand how financial plans and changes to commercial credit information can impact a business credit score. Visit http://sbcr.experian.com/scoreplanner.

Hello, I’m Hiq Lee, president of Experian’s Business Information Services, and I’d like to talk to you about how we are using data for good to help companies, large and small, succeed in the marketplace. At Experian, our group plays a crucial role in the big data ecosystem as an enabler of commerce and insights for the business community at large. We deliver unbiased information on more than 25 million active U.S. businesses, plus our international data capabilities, enable our customers to make more confident decisions on companies overseas. In 2012, along with Moody’s Analytics, we developed the Small Business Credit Index, which provides a unique perspective on the health of small businesses in the United States. The report contains important trends on bankruptcy rates, delinquencies, and overall payment behavior, as well as macro-economic information. This deeper look at the business landscape helps financial institutions and businesses every day to make sound lending decisions, gain key insights on business credit health and prospect for the right customer. At Experian, we are committed to delivering quality data and are strategically focused on the innovation of new and advanced products and services that enable businesses to thrive. Whether it’s analyzing millions of business credit transactions to generate industry-leading commercial credit scores and business credit reports, or safeguarding and securing millions of records to protect businesses and their customers from fraud, Experian is at the forefront of big data, driving value for our customers the world over. For Experian’s Business Information Services, using our data for good means constantly innovating and looking for ways to benefit businesses, as well as consumers and the overall economy. Related Data Is Good - Analytics Make It Great - Craig Boundy, CEO