Commercial Pulse Report

The bi-weekly Commercial Pulse provides a directional update on small business credit. It delivers a quick read on current market impacts, high level credit trends, score and attribute impacts, and other market related activities.

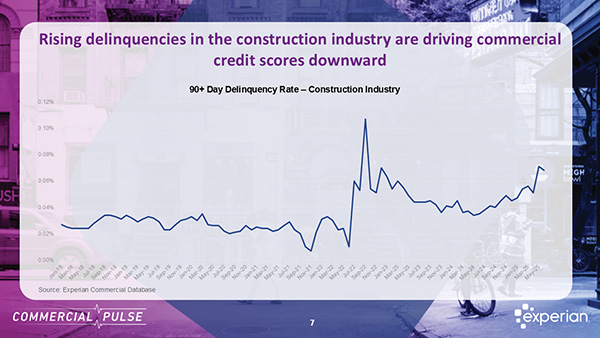

This week Experian focuses on the growing construction industry and early warning risk signals for lenders and risk managers.

Discover how small businesses have transformed since the pandemic, from digital adoption to growth resilience, in Experian’s latest report.

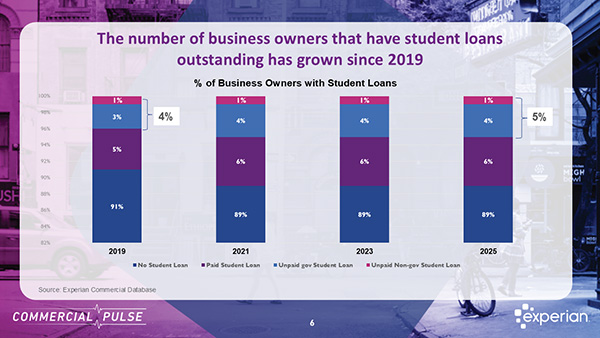

Experian Commercial Pulse Report - Business owners with unpaid student loans carry a higher risk for lenders.

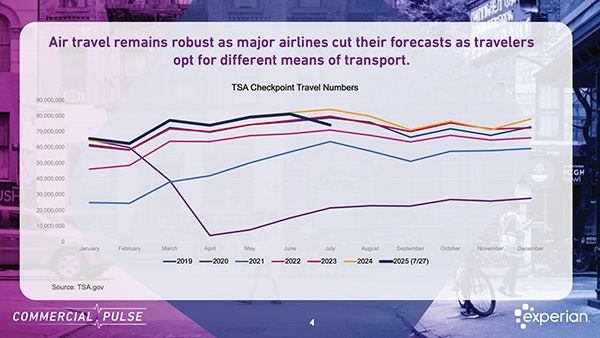

The Experian Commercial Pulse Report reveals key credit trends and risks in the hospitality and travel industry as summer travel surges.

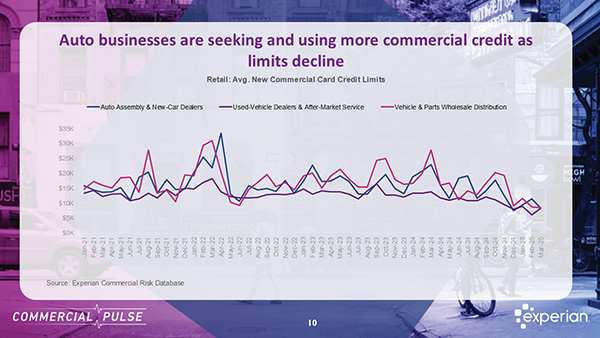

Experian's latest Commercial Pulse Report reveals rising car prices drive demand for used vehicles as commercial credit lines for b2b decline

Experian Commercial Pulse Report reveals decline in total number of ecommerce businesses, strong revenue, and fewer credit inquiries.

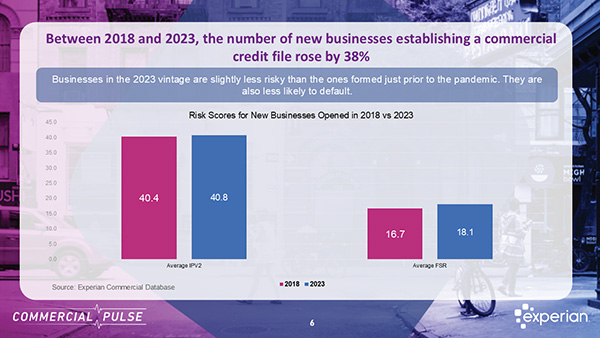

Economic uncertainty is often seen as a deterrent to growth. What's driving this wave of entrepreneurial activity?

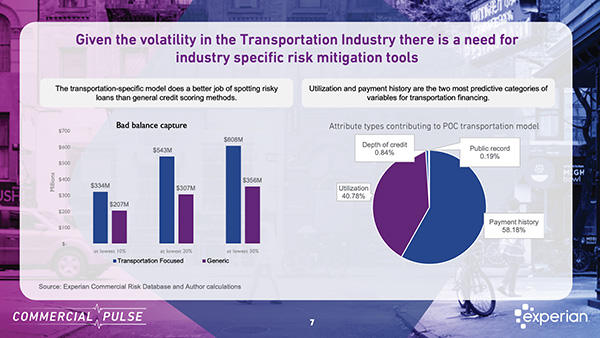

Discover how industry-specific risk models do a better job of assessing transportation financing risk in the latest Commercial Pulse Report.

Discover highlights from Experian’s March 2025 Commercial Pulse Report: GDP dip, small business growth, and rising income inequality.