Business Information Blog

Credit Management

Reports & Scores

Data & Analytics

The latest from our experts

The Experian Small Business Index™ rose by 1.8 points in March, reaching 47.2, marking the third consecutive month of modest gains.

April 2025 Pulse Report reveals trade disruption uncertainty, small business sentiment shifts, and a surge in manufacturing entrepreneurship.

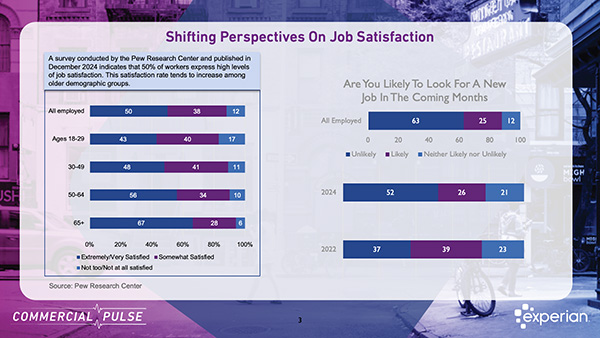

Despite concerns about a slowing job market, job satisfaction among American workers remains high.

This handy guide explains the practice of Credit Portfolio Management, managing, and monitoring all aspects of your company’s credit portfolio.

The Experian Small Business Index™ rose by 3.9 points in February, reaching 45.4, marking the second consecutive month of modest gains.

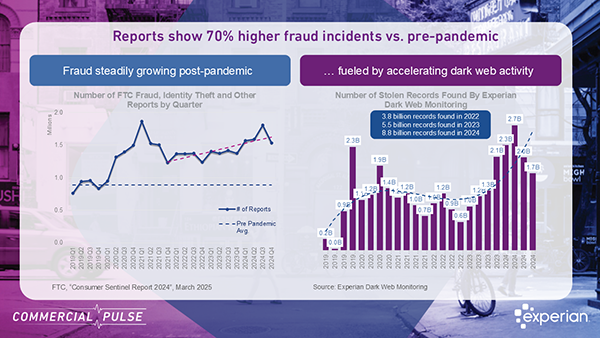

This week we focus on 2025 small business financial fraud, why it has increased, key stats, and strategies to protect your business.

The Experian Small Business Index increased by 1.0 pt in January signaling a modest improvement after December’s decline.

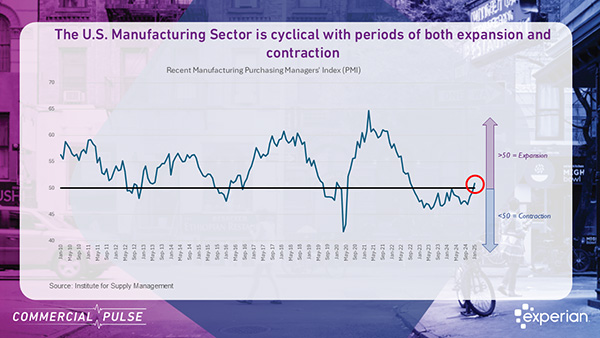

Experian reports the manufacturing sector may be on the verge of a shift after more than two years of contraction | Commercial Pulse Report

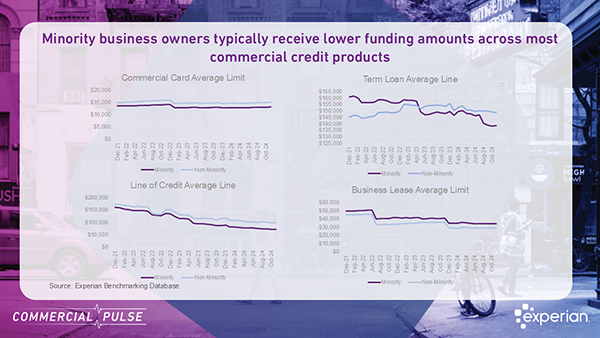

Commercial Pulse Report – minority-owned businesses are booming, yet they face a funding gap. A $2 trillion opportunity for lenders.

Experian Q4 Main Street Report reveals credit trends, lending shifts, and economic forces shaping growth amid policy changes and global uncertainties.

Join the Experian experts for a review on recent small business credit performance Tuesday, March 4th, 10:00 a.m. Pacific

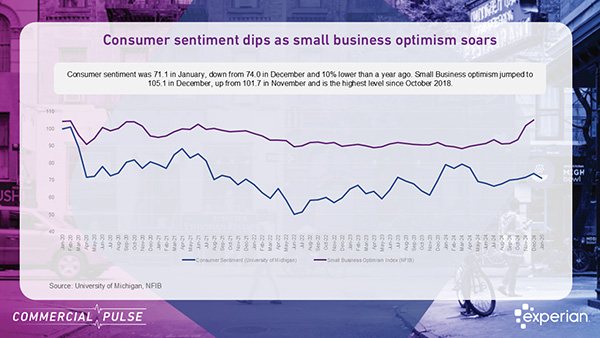

Commercial Pulse Report insights, including small business optimism vs consumer confidence, and the Experian Small Business Index.