Business Information Blog

Credit Management

Reports & Scores

Data & Analytics

The latest from our experts

The Experian Small Business Index (SBI) declined two points in December to 40.6, following an uptick in November 2025. Follow for updates.

AI is reshaping work, driving small business growth. Discover how AI, corporate shifts, and Gen Z are fueling an entrepreneurial boom.

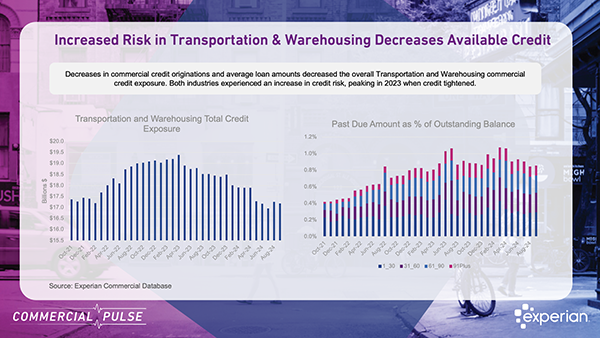

Fresh Insights from the latest Commercial Pulse Report, highlighting growth and credit challenges in U.S. transportation and warehousing.

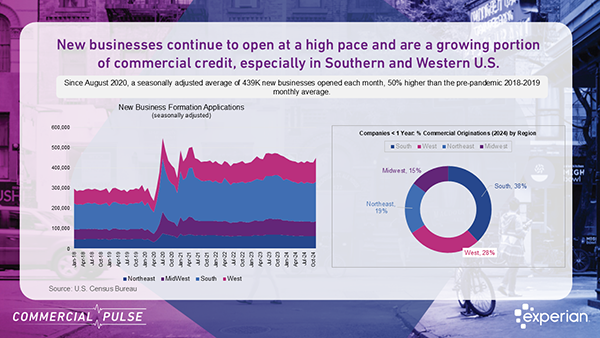

Use credit risk automation to capitalize on new business formation, expand digital relationships, and drive growth in a shifting economy.

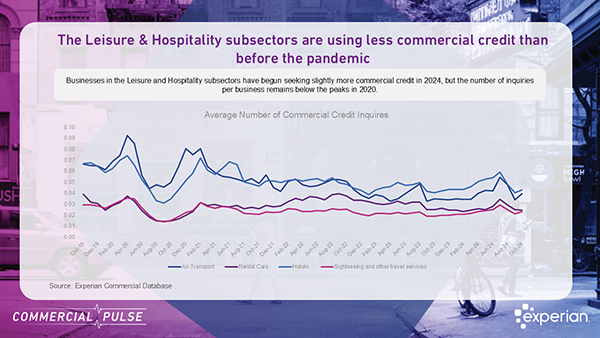

Explore Leisure & Hospitality trends in the commercial pulse report. Insights to help credit managers drive smarter decisions

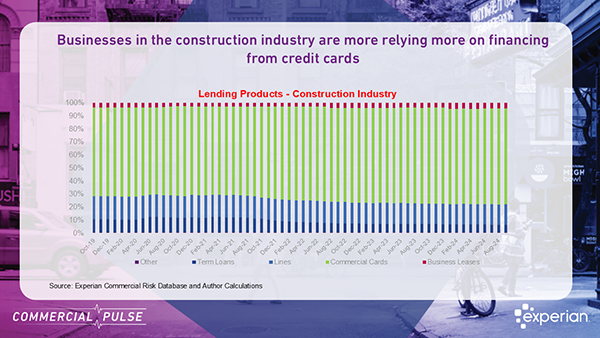

Discover industry-specific risk trends: Construction and Food Services face higher delinquencies, while Retail and Healthcare show stable performance. Learn more!

Small business credit performance resilient in Q3 as tariffs re-enter supply chains complicating an otherwise stable environment.

Experian’s Commercial Pulse report focuses on the dynamics of the housing business and construction companies in our November 26th issue.

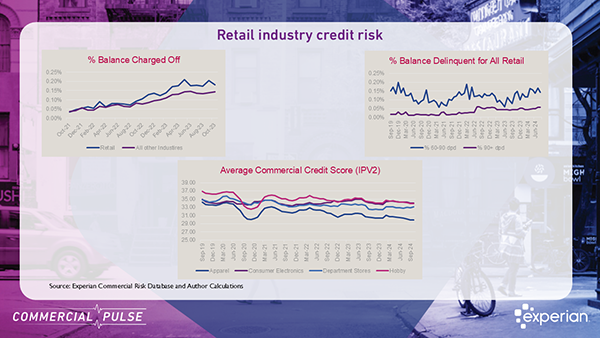

Explore the latest retail insights from Experian’s Commercial Pulse Report: credit demand surges, lending tightens, and retail growth slows.

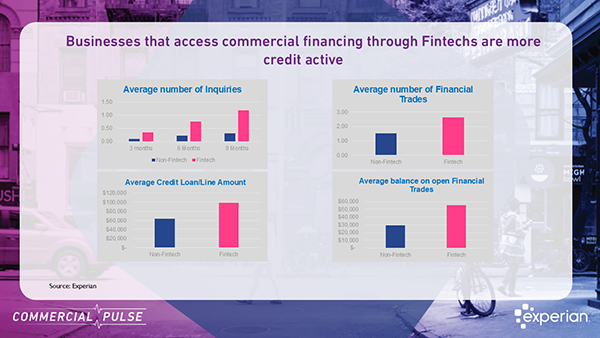

Fintech borrowers have increased credit activity, higher loan balances, but with greater delinquency risks in business financing decisions.

The Fall Beyond The Trends report offers a unique view into the challenges hitting small businesses, and how to navigate a cooling economy.