All posts by Managing Editor, Experian Software Solutions

Why businesses are using identity graphs as a useful tactic to help detect and prevent fraud as the fraud landscape continues to evolve.

We’ve compiled the top global business headlines that you need to stay in-the-know on the latest hot topics and insights from our experts.

Take a look at this infographic to discover what the key findings from our Global Insights Report, October 2021, mean for your business

eWeek’s James Maguire talks to Donna DePasquale, EVP of Global Decisioning Software, about the use of technology in financial services

Find out how consumer expectations have changed over the course of the pandemic and what that means for businesses when it comes to decisioning

Lenders, do you need a model or a strategy when it comes to credit risk decision management? Here are the three questions to consider.

Read about why businesses need to invest in technology to keep up with consumer expectations online in our latest research

We’ve compiled the top global business headlines that you need to stay in-the-know on the latest hot topics and insights from our experts.

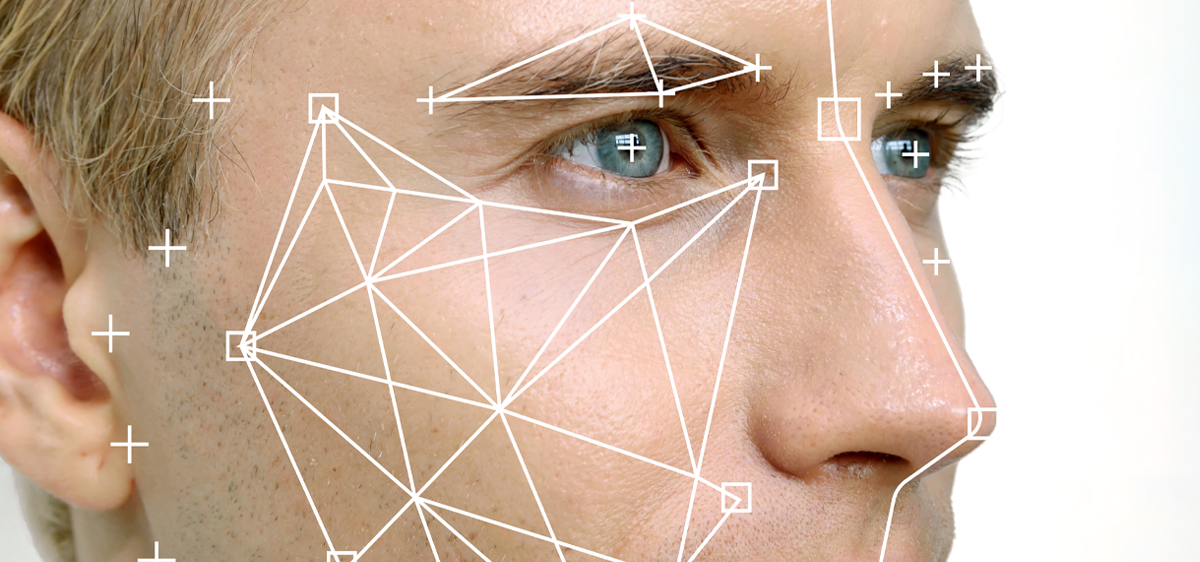

What is deepfake fraud and how do cybercriminals use it? This infographic shows how AI and machine learning play a part in both its production and defence.

We’ve compiled the top global business headlines that you need to stay in-the-know on the latest hot topics and insights from our experts.

Why lenders need to rapidly build new and better models to onboard customers and create a more dynamic customer journey to compete.

Read about why Experian has been recognized for AI, fraud prevention and fraud detection by Juniper Research's Future Digital Awards.