Lenders are looking for ways to accurately score more consumers and grow their applicant pool without increasing risk. And it looks like more and more are turning to the VantageScore® credit score to help achieve their goals. So, who’s using the VantageScore® credit score? ![]()

- 9 of the top 10 financial institutions.

- 18 of the top 25 credit card issuers.

- 21 of the top 25 credit unions.

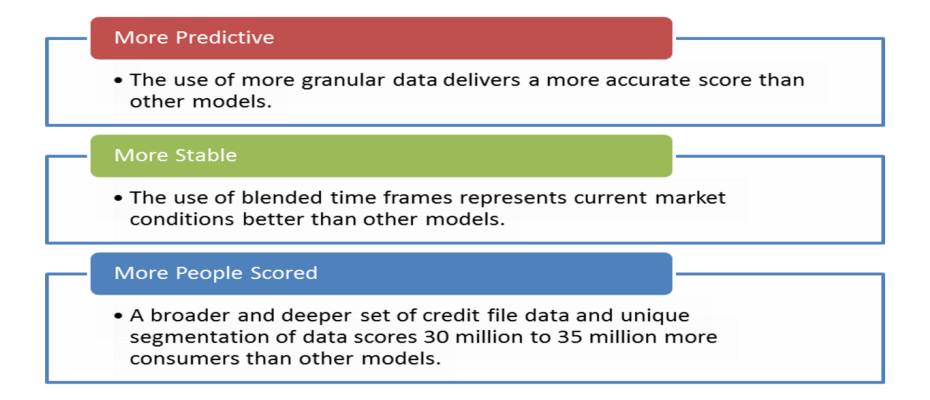

VantageScore leverages the collective experience of the industry’s leading experts on credit data, modeling and analytics to provide a more consistent and highly predictive credit score.