All posts by Alex Lvoff

March is a time when the idea of luck is in the air, with St. Patrick’s Day celebrations and hopeful thoughts of pots of gold at the end of the rainbow. But while the "Luck of the Irish" may be a fun idea, scammers take advantage of this sentiment to exploit people through fraudulent lottery scams and prize schemes. Take, for example, the so-called "Luck of the Irish" scams that flood inboxes and phone lines every March. You might receive a message claiming you have won the "Irish National Lottery" or another grand prize, but there is a catch—you need to pay fees or provide sensitive personal information to claim it. Before you know it, the scammers have vanished with your money or used your data for further fraud. Red flags of lottery scams Financial institutions can help protect clients by educating them on the warning signs of fraudulent lottery schemes. According to the FTC website, here are three clear indicators that a prize is too good to be true: You must pay to claim your winnings – Legitimate lotteries do not require winners to pay taxes, fees, or handling charges upfront. If you are asked to send money to claim a prize, it is a scam. You never entered the lottery – If you did not buy a ticket or enter a sweepstake, you cannot win. Any message saying otherwise is a red flag. They ask for personal or financial information – No legitimate lottery will ask for your Social Security number, bank details, or credit card information to process winnings. How scammers operate Lottery scammers use a variety of tactics to trick victims, including: Impersonating well-known brands or government agencies to appear credible. Sending fake checks that later bounce after victims have sent money. Using high-pressure tactics, such as claiming the offer is time sensitive. Requesting payment through difficult-to-trace methods like gift cards, wire transfers, or cryptocurrency. How financial institutions can help clients stay safe Banks and financial institutions play a critical role in protecting their clients from falling victim to lottery scams. Here is how they can help: Educate clients: Provide fraud awareness materials explaining common scams, red flags, and safe financial practices. Implement transaction monitoring: Monitor for suspicious transactions, especially those involving large wire transfers or unusual payments to unknown entities. Encourage multi-factor authentication: Strengthening account security can prevent unauthorized transactions if scammers obtain a victim’s personal information. Offer a safe reporting channel: Encourage clients to report suspected scams so the institution can take preventive action and share warnings with others. Final thoughts Winning the lottery may be a dream for many, but no real jackpot comes with a catch. Financial institutions can be the first line of defense by helping clients recognize scams before they lose money. The best approach? Remind clients that the only "pot of gold" worth chasing is the one they have earned and safeguarded through smart financial habits. And finally, check out this educational tune with a catchy rhythm, designed to raise awareness about scams. Learn more

As Valentine’s Day approaches, hearts will melt, but some will inevitably be broken by romance scams. This season of love creates an opportune moment for scammers to prey on individuals feeling lonely or seeking connection. Financial institutions should take this time to warn customers about the heightened risks and encourage vigilance against fraud. In a tale as heart-wrenching as it is cautionary, a French woman named Anne was conned out of nearly $855,000 in a romance scam that lasted over a year. Believing she was communicating with Hollywood star Brad Pitt; Anne was manipulated by scammers who leveraged AI technology to impersonate the actor convincingly. Personalized messages, fabricated photos, and elaborate lies about financial needs made the scam seem credible. Anne’s story, though extreme, highlights the alarming prevalence and sophistication of romance scams in today’s digital age. According to the Federal Trade Commission (FTC), nearly 70,000 Americans reported romance scams in 2022, with losses totaling $1.3 billion—an average of $4,400 per victim. These scams, which play on victims’ emotions, are becoming increasingly common and devastating, targeting individuals of all ages and backgrounds. Financial institutions have a crucial role in protecting their customers from these schemes. The lifecycle of a romance scam Romance scams follow a consistent pattern: Feigned connection: Scammers create fake profiles on social media or dating platforms using attractive photos and minimal personal details. Building trust: Through lavish compliments, romantic conversations, and fabricated sob stories, scammers forge emotional bonds with their targets. Initial financial request: Once trust is established, the scammer asks for small financial favors, often citing emergencies. Escalation: Requests grow larger, with claims of dire situations such as medical emergencies or legal troubles. Disappearance: After draining the victim’s funds, the scammer vanishes, leaving emotional and financial devastation in their wake. Lloyds Banking Group reports that men made up 52% of romance scam victims in 2023, though women lost more on average (£9,083 vs. £5,145). Individuals aged 55-64 were the most susceptible, while those aged 65-74 faced the largest losses, averaging £13,123 per person. Techniques scammers use Romance scammers are experts in manipulation. Common tactics include: Fabricated sob stories: Claims of illness, injury, or imprisonment. Investment opportunities: Offers to “teach” victims about investing. Military or overseas scenarios: Excuses for avoiding in-person meetings. Gift and delivery scams: Requests for money to cover fake customs fees. How financial institutions can help Banks and financial institutions are on the frontlines of combating romance scams. By leveraging technology and adopting proactive measures, they can intercept fraud before it causes irreparable harm. 1. Customer education and awareness Conduct awareness campaigns to educate clients about common scam tactics. Provide tips on recognizing fake profiles and unsolicited requests. Share real-life stories, like Anne’s, to highlight the risks. 2. Advanced data capture solutions Implement systems that gather and analyze real-time customer data, such as IP addresses, browsing history, and device usage patterns. Use behavioral analytics to detect anomalies in customer actions, such as hesitation or rushed transactions, which may indicate stress or coercion. 3. AI and machine learning Utilize AI-driven tools to analyze vast datasets and identify suspicious patterns. Deploy daily adaptive models to keep up with emerging fraud trends. 4. Real-time fraud interception Establish rules and alerts to flag unusual transactions. Intervene with personalized messages before transfers occur, asking “Do you know and trust this person?” Block transactions if fraud is suspected, ensuring customers’ funds are secure. Collaborating for greater impact Financial institutions cannot combat romance scams alone. Partnerships with social media platforms, AI companies, and law enforcement are essential. Social media companies must shut down fake profiles proactively, while regulatory frameworks should enable banks to share information about at-risk customers. Conclusion Romance scams exploit the most vulnerable aspects of human nature: the desire for love and connection. Stories like Anne’s underscore the emotional and financial toll these scams take on victims. However, with robust technological solutions and proactive measures, financial institutions can play a pivotal role in protecting their customers. By staying ahead of fraud trends and educating clients, banks can ensure that the pursuit of love remains a source of joy, not heartbreak. Learn more

As we step into 2025, the convergence of credit and fraud risk has become more pronounced than ever. With fraudsters leveraging emerging technologies and adapting rapidly to new defenses, risk managers need to adopt forward-thinking strategies to protect their organizations and customers. Here are the top fraud trends and actionable resolutions to help you stay ahead of the curve this year. 1. Combat synthetic identity fraud with advanced AI models The trend: Synthetic identity fraud is surging, fueled by data breaches and advanced AI tooling. Fraudsters are combining genuine credentials with fabricated details, creating identities that evade traditional detection methods. Resolution: Invest in sophisticated identity validation tools that leverage advanced AI models. These tools can differentiate between legitimate and fraudulent identities, ensuring faster and more accurate creditworthiness assessments. Focus on integrating these solutions seamlessly into your customer onboarding process to enhance both security and user experience. 2. Strengthen authentication against deepfakes The trend: Deepfake technology is putting immense pressure on existing authentication systems, particularly in high-value transactions and account takeovers. Resolution: Adopt a multilayered authentication strategy that combines voice and facial biometrics with ongoing transaction monitoring. Dynamic authentication methods that evolve based on user behavior and fraud patterns can effectively counter these advanced threats. Invest in solutions that ensure digital interactions remain secure without compromising convenience. 3. Enhance detection of payment scams and APP fraud The trend: Authorized Push Payment (APP) fraud and scams are increasingly difficult to detect because they exploit legitimate customer behaviors. Resolution: Collaborate with industry peers and explore centralized consortia to share insights and develop robust detection strategies. Focus on monitoring both inbound and outbound transactions to identify anomalies, particularly payments to mule accounts. 4. Optimize Your Fraud Stack for Efficiency and Effectiveness The trend: Outdated device and network solutions are no match for GenAI-enhanced fraud tactics. Resolution: Deploy a layered fraud stack with persistent device ID technology, behavioral analytics, and GenAI-driven anomaly detection. Begin with frictionless first-tier tools to filter out low-hanging fraud vectors, reserving more advanced and costly tools for sophisticated threats. Regularly review and refine your stack to ensure it adapts to evolving fraud patterns. 5. Build collaborative relationships with fraud solution vendors The trend: Vendors offer unparalleled industry insights and long-tail data to help organizations prepare for emerging fraud trends. Resolution: Engage in reciprocal knowledge-sharing with your vendors. Leverage advisory boards and industry insights to stay informed about the latest attack vectors. Choose vendors who provide transparency and are invested in your fraud mitigation goals, turning product relationships into strategic partnerships. Turning resolutions into reality Fraudsters are becoming more ingenious, leveraging GenAI and other technologies to exploit vulnerabilities. To stay ahead of fraud in 2025, let us make fraud prevention not just a resolution but a commitment to safeguarding trust and security in a rapidly evolving landscape. Learn more

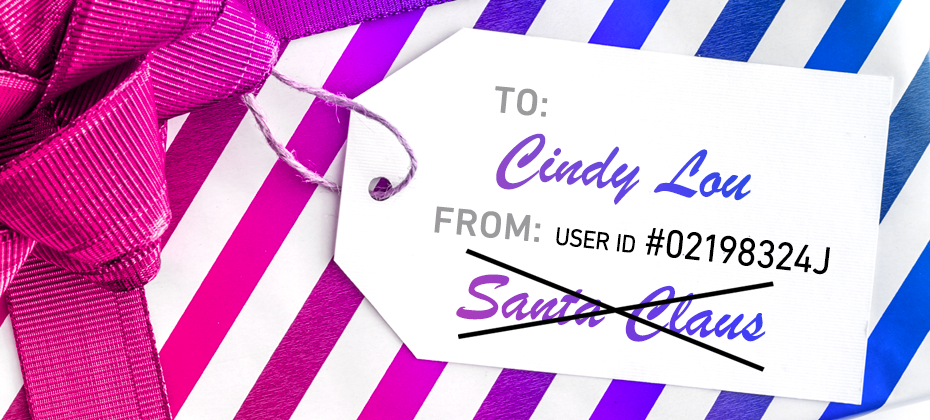

A tale of synthetic ID fraud Synthetic ID fraud is an increasing issue and affects everyone, including high-profile individuals. A notable case from Ohio involved Warren Hayes, who managed to get an official ID card in the name of “Santa Claus” from the Ohio Bureau of Motor Vehicles. He also registered a vehicle, opened a bank account, and secured an AAA membership under this name, listing his address as 1 Noel Drive, North Pole, USA. This elaborate ruse unraveled after Hayes, disguised as Santa, got into a minor car accident. When the police requested identification, Hayes presented his Santa Claus ID. He was subsequently charged under an Ohio law prohibiting the use of fictitious names. However, the court—presided over by Judge Thomas Gysegem—dismissed the charge, arguing that because Hayes had used the ID for over 20 years, "Santa Claus" was effectively a "real person" in the eyes of the law. The judge’s ruling raised eyebrows and left one glaring question unanswered: how could official documents in such a blatantly fictitious name go undetected for two decades? From Santa Claus to synthetic IDs: the modern-day threat The Hayes case might sound like a holiday comedy, but it highlights a significant issue that organizations face today: synthetic identity fraud. Unlike traditional identity theft, synthetic ID fraud does not rely on stealing an existing identity. Instead, fraudsters combine real and fictitious details to create a new “person.” Think of it as an elaborate game of make-believe, where the stakes are millions of dollars. These synthetic identities can remain under the radar for years, building credit profiles, obtaining loans, and committing large-scale fraud before detection. Just as Hayes tricked the Bureau of Motor Vehicles, fraudsters exploit weak verification processes to pass as legitimate individuals. According to KPMG, synthetic identity fraud bears a staggering $6 billion cost to banks.To perpetrate the crime, malicious actors leverage a combination of real and fake information to fabricate a synthetic identity, also known as a “Frankenstein ID.” The financial industry classifies various types of synthetic identity fraud. Manipulated Synthetics – A real person’s data is modified to create variations of that identity. Frankenstein Synthetics – The data represents a combination of multiple real people. Manufactured Synthetics – The identity is completely synthetic. How organizations can combat synthetic ID fraud A multifaceted approach to detecting synthetic identities that integrates advanced technologies can form the foundation of a sound fraud prevention strategy: Advanced identity verification tools: Use AI-powered tools that cross-check identity attributes across multiple data points to flag inconsistencies. Behavioral analytics: Monitor user behaviors to detect anomalies that may indicate synthetic identities. For instance, a newly created account applying for a large loan with perfect credit is a red flag. Digital identity verification: Implement digital onboarding processes that include online identity verification with real-time document verification. Users can upload government-issued IDs and take selfies to confirm their identity. Collaboration and data sharing: Organizations can share insights about suspected synthetic identities to prevent fraudsters from exploiting gaps between industries. Ongoing employee training: Ensure frontline staff can identify suspicious applications and escalate potential fraud cases. Regulatory support: Governments and regulators can help by standardizing ID issuance processes and requiring more stringent checks. Closing thoughts The tale of Santa Claus’ stolen identity may be entertaining, but it underscores the need for vigilance against synthetic ID fraud. As we move into an increasingly digital age, organizations must stay ahead of fraudsters by leveraging technology, training, and collaboration. Because while the idea of Spiderman or Catwoman walking into your branch may seem amusing, the financial and reputational cost of synthetic ID fraud is no laughing matter. Learn more

The advent of artificial intelligence (AI) is significantly transforming the landscape of real estate fraud, enabling criminals to execute complex schemes like deed theft with greater ease. A notable case involves Spelling Manor, a $137.5 million mansion in Los Angeles, where the owner alleges they are entangled in deed fraud. Scammers reportedly filed fraudulent documents that have prevented the owner from selling the estate, thwarting offers from buyers, including former Google CEO Eric Schmidt. Understanding deed/title fraud Deed fraud, also known as title or property fraud, occurs when someone illegally transfers ownership of a property without the owner’s knowledge or consent. Typically, fraudsters create fake documents or forge the owner’s signature on a deed to make it look like the property has been legally transferred to them. Once the title is in their name, they may try to sell or mortgage the property, leaving the original owner unaware until it’s too late. How deed fraud works Identify a target: Fraudsters often look for properties that appear vulnerable, such as vacant land, unoccupied homes, or properties owned by elderly individuals who may not check their records frequently. Forge documentation: Using fake IDs and forged signatures, scammers create documents that appear to show a legitimate transfer of ownership. With modern technology, these documents can look highly convincing. Record the fake deed: Fraudsters then file these documents with the local county clerk or recorder’s office. This officially changes the ownership records, making it seem as if the scammer is the legitimate owner. Exploit the ownership: Once listed as the owner, the fraudster may sell the property to an unsuspecting buyer, take out loans against it, or even rent it out. The impact on victims In the summer of 2024, Elvis Presley’s family got confronted to a forged deed scam. A fake firm, Naussany Investments, falsely claimed Lisa Marie Presley owed millions and used Graceland as collateral. They placed a foreclosure notice and attempted to auction the estate. Riley Keough filed a lawsuit, exposing the firm as fraudulent and halting the foreclosure through a judge’s injunction. Lisa Jeanine Findley, who forged documents and posed as firm employees, was arrested and charged with deed forgery fraud and identity theft. She faces up to 22 years in prison if convicted. The FBI's Internet Crime Complaint Center does not specifically monitor deed fraud. However, in 2023, it processed a total of 9,521 real estate-related complaints defined as the loss of funds from a real estate investment, resulting in more than $145 million in losses. Victims of deed fraud can face severe financial and legal issues. They may discover the fraud only when trying to sell, refinance, or even pay taxes on the property. Reversing deed fraud typically requires a costly and time-consuming legal process, as courts must determine that the transfer was fraudulent and restore the original owner’s rights. Prevention and safeguards There are several preventive measures and fraud prevention solutions that can be established to help mitigate the risks associated with deed/title fraud. These include: For lending institutions: Enhanced ID verification: Implement multi-factor identity checks at the loan approval stage. Regular portfolio audits: Conduct periodic audits to detect unusual property transfers and title changes in their loan portfolios. For title companies: AI-driven document verification tools: Use machine learning algorithms to identify inconsistencies in deed and ownership documents. Real-time fraud monitoring: Employ analytics to track suspicious behavior patterns, such as rapid ownership changes. Seller authentication: Require biometric or multi-step identity verification for anyone claiming ownership or initiating sales. For realtors: Training and awareness: Educate realtors on how to spot warning signs of fraudulent listings and seller impersonations. Pre-transaction verification: Collaborate with title companies to validate ownership early in the listing process. Acting with the right solution Mortgage fraud is a constant threat that demands ongoing vigilance and adaptability. As fraudsters evolve their tactics, the mortgage industry must stay one step ahead to safeguard homeowners and lenders alike. With concerns over deed/title-related fraud rising, it is vital to raise awareness, strengthen preventive measures, and foster collaboration to protect the integrity of the mortgage market. By staying informed and implementing robust safeguards, we can collectively combat and prevent mortgage fraud from disrupting the financial security of individuals and the industry. Experian mortgage powers advanced capabilities across the mortgage lifecycle by gaining market intelligence, enhancing customer experience to remove friction and tapping into industry leading data sources to gain a complete view of borrower behavior. Visit our website to see how these solutions can help your business prevent deed fraud. Learn more

U.S. federal prosecutors have indicted Michael Smith of North Carolina for allegedly orchestrating a $10 million fraud scheme involving AI-generated music. Smith is accused of creating fake bands and using AI tools to produce hundreds of tracks, which were streamed by fake listeners on platforms like Spotify, Apple Music, and Amazon Music. Despite the artificial engagement, the scheme generated real royalty payments, defrauding these streaming services. This case marks the first prosecution of its kind and highlights a growing financial risk: the potential for rapid, large-scale fraud in digital platforms when content and engagement can be easily fabricated. A new report from Imperva Inc. highlights the growing financial burden of unsecure APIs and bot attacks on businesses, costing up to $186 billion annually. Key findings highlight the heavy economic burden on large companies due to their complex and extensive API ecosystems, often unsecured. Last year, enterprises managed about 613 API endpoints on average, a number expected to grow, increasing associated risks. APIs exposure to bot attacks Bot attacks, similar to those seen in streaming fraud, are also plaguing financial institutions. The risks are significant, weakening both security and financial stability. 1. Fraudulent transactions and account takeover Automated fraudulent transactions: Bots can perform high volumes of small, fraudulent transactions across multiple accounts, causing financial loss and overwhelming fraud detection systems. Account takeover: Bots can attempt credential stuffing, using compromised login data to access user accounts. Once inside, attackers could steal funds or sensitive information, leading to significant financial and reputational damage. 2. Synthetic identity fraud Creating fake accounts: Bots can be used to generate large numbers of synthetic identities, which are then used to open fake accounts for money laundering, credit fraud, or other illicit activities. Loan or credit card fraud: Using fake identities, bots can apply for loans or credit cards, withdrawing funds without intent to repay, resulting in significant losses for financial institutions. 3. Exploiting API vulnerabilities API abuse: Just as bots exploit API endpoints in streaming services, they can also target vulnerable APIs in financial platforms to extract sensitive data or initiate unauthorized transactions, leading to significant data breaches. Data exfiltration: Bots can use APIs to extract financial data, customer details, and transaction records, potentially leading to identity theft or data sold on the dark web. Bot attacks targeting financial institutions can result in extensive fraud, data breaches, regulatory fines, and loss of customer trust, causing significant financial and operational consequences. Safeguarding financial integrity To safeguard your business from these attacks, particularly via unsupervised APIs, a multi-layered defense strategy is essential. Here’s how you can protect your business and ensure its financial integrity: 1. Monitor and analyze data patterns Real-time analytics: Implement sophisticated monitoring systems to track user behavior continuously. By analyzing user patterns, you can detect irregular spikes in activity that may indicate bot-driven attacks. These anomalies should trigger alerts for immediate investigation. AI, machine learning, and geo-analysis: Leverage AI and machine learning models to spot unusual behaviors that can signal fraudulent activity. Geo-analysis tools help identify traffic originating from regions known for bot farms, allowing you to take preventive action before damage occurs. 2. Strengthen API access controls Limit access with token-based authentication: Implement token-based authentication to limit API access to verified applications and users. This reduces the chances of unauthorized or bot-driven API abuse. Control third-party integrations: Restrict API access to only trusted and vetted third-party services. Ensure that each external service is thoroughly reviewed to prevent malicious actors from exploiting your platform. 3. Implement robust account creation procedures PII identity verification solutions: Protect personal or sensitive data through authenticating someone`s identity and helping to prevent fraud and identity theft. Email and phone verification: Requiring email or phone verification during account creation can minimize the risk of mass fake account generation, a common tactic used by bots for fraudulent activities. Combating Bots as a Service: Focusing on intent-based deep behavioral analysis (IDBA), even the most sophisticated bots can be spotted, without adding friction. 4. Establish strong anti-fraud alliances Collaborate with industry networks: Join industry alliances or working groups that focus on API security and fraud prevention. Staying informed about emerging threats and sharing best practices with peers will allow you to anticipate new attack strategies. 5. Continuous customer and account monitoring Behavior analysis for repeat offenders: Monitor for repeat fraudulent behavior from the same accounts or users. If certain users or transactions display consistent signs of manipulation, flag them for detailed investigation and potential restrictions. User feedback loops: Encourage users to report any suspicious activity. This crowd-sourced intelligence can be invaluable in identifying bot activity quickly and reducing the scope of damage. 6. Maintain transparency and accountability Audit and report regularly: Offer regular, transparent reports on API usage and your anti-fraud measures. This builds trust with stakeholders and customers, as they see your proactive steps toward securing the platform. Real-time dashboards: Provide users with real-time visibility into their data streams or account activities. Unexplained spikes or dips can be flagged and investigated immediately, providing greater transparency and control. Conclusion Safeguarding your business from bot attacks and API abuse requires a comprehensive, multi-layered approach. By investing in advanced monitoring tools, enforcing strict API access controls, and fostering collaboration with anti-fraud networks, your organization can mitigate the risks posed by bots while maintaining credibility and trust. The right strategy will not only protect your business but also preserve the integrity of your platform. Learn more

Fraud-as-a-Service (FaaS) represents an emerging and increasingly sophisticated business model within cybercrime. In this model, malicious actors commercialize their expertise, tools, and infrastructure, enabling others to perpetrate fraud more easily and efficiently. These FaaS offerings are often accessible via dark web marketplaces or underground forums, streamlining and automating fraud processes, such as large-scale phishing campaigns. This enables the creation of convincing counterfeit websites and the distribution of bulk emails, allowing cybercriminals to harvest credentials and personal information en masse. Organized cybercrime syndicates leverage account creation bots to establish hundreds of fraudulent accounts across various platforms, bypassing standard security protocols and scaling their illicit activities seamlessly. A fraudster no longer requires deep technical skills or detailed knowledge of complex verification techniques, such as liveness detection. Instead, they can acquire turnkey FaaS solutions that, for instance, inject pre-recorded video footage to spoof verification processes, enabling the rapid creation of thousands of fraudulent accounts. The commoditization of fraud has effectively democratized it, lowering the barriers to entry. Previously accessible to a select few, FaaS has developed sophisticated techniques and is now available to a broader and less technically adept audience. Now, even individuals with basic computer skills can access these services and initiate fraudulent schemes with minimal effort. Key tools in the FaaS arsenal Central to the success of fraud-as-a-service is the ability to create fraudulent accounts while evading detection. This process can be alarmingly straightforward, even for companies adhering to industry-recognized best practices. Widely available programs, such as app cloners, enable fraudsters to generate multiple instances of the same application on a single device, modifying its source code to bypass security measures to detect such activities. The generalization of artifical intelligence (AI) and increased access to technology have provided cybercriminals with new tools to launch sophisticated scams, such as Pig Butchering and Authorized Push Payment (APP) scams. Similarly, image injection tools facilitate the insertion of manipulated images to deceive verification systems, while emulators simulate legitimate device activity at scale, making detection more challenging. Techniques such as location spoofing allow fraudsters to alter the perceived geographical location of a device, thereby evading location-based security checks and allowing their scams to remain undetected. Once fraudulent accounts are established, cybercriminals focus on monetizing their efforts. Industries like food delivery and ride-hailing are particularly vulnerable to promotional abuse. Fraudsters exploit promotional offers intended for new customers by using cloned apps, injected images, and emulators to create multiple fake accounts, redeem discounts, and resell them for profit. AI-driven automation and advanced communication technologies lower the barriers for these scams, enabling criminals to operate at a larger scale and with greater efficiency. This has made scams more pervasive and difficult for individuals and institutions to detect. In the ride-hailing industry, these tactics are used to manipulate fare structures and incentives. Fraudsters operate multiple driver or rider accounts on the same device to earn referral bonuses and other promotional rewards. Emulators can simulate rides with fabricated start and end points, while location spoofing tools manipulate GPS data, inflating fares, and earnings. Such fraudulent activities result in significant financial losses for companies and degrade service quality for legitimate users, as resources are diverted from genuine transactions and logistical algorithms are disrupted. The implications of FaaS for businesses The commercialization of fraud poses a substantial threat to businesses, not only by democratizing fraud but also by enabling it to rapidly scale. . Fraudsters can experiment with multiple schemes simultaneously, sharing feedback and accelerating their learning curve. A single tool developed by one individual can be deployed by numerous bad actors to perpetrate fraud on a large scale, with remarkable speed. This ease of execution allows fraudsters to overwhelm companies with a barrage of attacks, maximizing their financial gains while exacerbating the challenges of fraud prevention for targeted organizations. Developing a FaaS-Resilient fraud prevention strategy To effectively combat fraud-as-a-service, businesses must adopt AI fraud strategies that mirror the operational sophistication of fraudsters. These cybercriminals treat their activities as profitable enterprises, continually optimizing their return on investment through scalable and adaptable tactics. By deeply understanding the methodologies employed by fraudsters, companies can develop more effective fraud prevention measures that disrupt fraudulent operations without inconveniencing legitimate users. Proactive fraud prevention strategies are essential in countering FaaS tactics. Effective measures rely on robust data collection and analysis. Regular reviews of key performance indicators (KPIs) and velocity checks, which monitor the rate at which users complete transactions, can help identify irregular behaviors. Passive signals, such as device fingerprinting and location intelligence, are also invaluable in detecting suspicious activities. By scrutinizing data related to app tampering or device emulation, businesses can more accurately determine whether a genuine user is accessing their platform or if a fraudster is attempting to bypass detection. Given the dynamic nature of FaaS, adaptation is crucial. Fraud prevention strategies must evolve continually to keep pace with emerging threats. Advanced technologies offer nuanced insights into user behavior, enabling businesses to identify and thwart fraud attempts with greater precision. Moreover, cutting-edge risk monitoring tools can help avoid false positives, ensuring that legitimate users are not unduly impacted. As fraudsters persist in innovating and refining their tactics, organizations must remain vigilant, stay informed about emerging trends, invest in advanced fraud prevention and detection technologies, and cultivate a culture of security and awareness. While it may be tempting to underestimate fraudsters due to the illicit nature of their activities, it is important to recognize that many approach their work with a level of professionalism comparable to legitimate businesses. Understanding this reality offers valuable insights into how companies can effectively counteract fraud and protect their monetary interests. Learn more This article includes content created by an AI language model and is intended to provide general information.

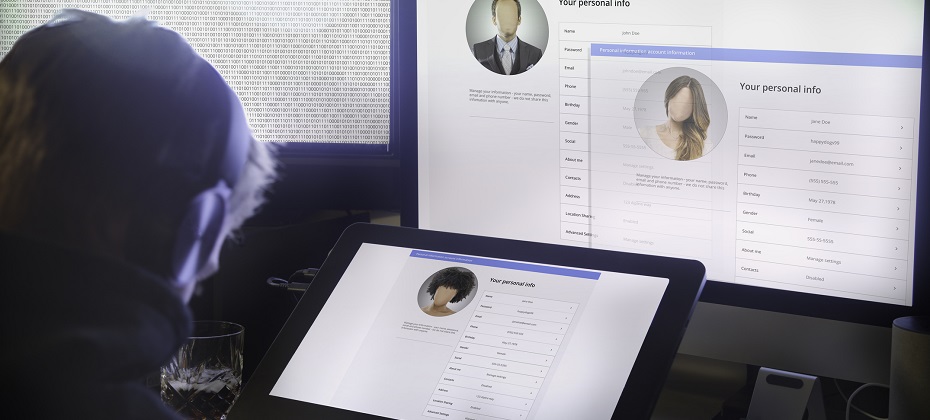

Gen Z, or "Zoomers," born from 1997 to 2012, are molded by modern transformations. They have witnessed events from post-9/11 impacts to the rise of the internet and the COVID-19 crisis. As early adopters of technology, their lives are intertwined with smartphones, online shopping, social platforms, cloud services, emerging fintech, and artificial intelligence. They are called “digital natives” as they are the first generation to grow up with internet as part of their daily life. Research generally indicates that this post-millennial generation values practicality, favoring financial stability over entrepreneurial pursuits. They appreciate communication tailored to them and often employ social media to cultivate their personal brands. As a generation growing up immersed in technology, they tend to choose digital interactions, seeking to forge robust, secure, genuine, and unconstrained digital experiences. The challenge of identity verification Identity verification presents a considerable challenge for Generation Z. According to a Fortune survey, close to 50% of this demographic regrets not opening financial accounts earlier, citing a lack of readiness to join the financial ecosystem by the age of 18. Consequently, this has given rise to "digital ghosts"—people with minimal or nonexistent financial histories who face challenges when trying to utilize financial services. The 2009 Credit Card Accountability Responsibility and Disclosure Act mandates that individuals under 21 need a cosigner or show income proof to get a credit card, hindering their early financial involvement. Moreover, conventional identity checks are becoming less reliable due to the surge in identity theft. Innovative solutions for verifying Gen Z Verifying identities and preventing fraud among Gen Z presents unique challenges due to their digital-native status and limited credit histories. Here are some effective strategies and approaches that financial institutions can adopt to address these challenges: Leveraging alternative data sources Academic records leverage information from higher learning institutions such as universities, colleges, and vocational schools. This data can be vital for authenticating the identities of younger individuals who may lack a substantial credit history. Employment verification retrieve data confirming the identity and employment status, especially focusing on Gen Z who are new to the job market. Utility and telecom records leverage payment histories for utilities, phone bills, and other recurring services, which can provide additional layers of identity verification. Alternative financial data includes online small dollar lenders, online installment lenders, single payment, line of credit, storefront small dollar lenders, auto title and rent-to-own. Phone-Centric ID Phone-Centric Identity refers to technology that leverages and analyzes mobile, telecom, and other signals for the purposes of identity verification, identity authentication, and fraud prevention. Phone-Centric Identity relies on billions of signals from authoritative sources pulled in real time, making it a powerful proxy for digital identity and trust. Advance authentication technologies Behavioral biometrics analyze user behaviors such as typing patterns, navigation habits, and device usage. These subtle behaviors can help create a unique profile for each user, making it difficult for fraudsters to impersonate them. Adaptive risk-based authentication that adjusts the level of security based on the user's behavior, location, device, and other factors. For example, a higher level of verification might be required for transactions that are deemed unusual or high-risk. Real-time fraud detection AI and machine learning: Deploy AI and machine learning algorithms to analyze transaction patterns and detect anomalies in real-time. These technologies can identify suspicious activities and flag potential fraud. Fraud analytics: Use predictive analytics to assess the likelihood of fraud based on historical data and current behavior. This approach helps in proactively identifying and mitigating fraudulent activities. Secure digital onboarding Digital identity verification: Implement digital onboarding processes that include online identity verification with real-time document verification. Users can upload government-issued IDs and take selfies to confirm their identity. Video KYC (Know Your Customer): Use video calls to conduct KYC processes, allowing bank representatives to verify identities and documents remotely via automated identity verification. This method is secure and convenient for tech-savvy Gen Z customers. Make identity verification easy To authenticate identities and combat fraud within the Gen Z population, financial organizations need to implement a comprehensive strategy utilizing innovative technologies, non-traditional data, and strong protective protocols. Such actions will enable the creation of a trustworthy and frictionless banking environment that appeals to a generation adept in digital interactions, thereby establishing trust and encouraging enduring connections. To learn more about Experian’s automated identity verification solutions, visit our website. Learn more

In this article...What is a TOAD attack?How TOAD attacks happenEffective countermeasures Keeping TOADS at bay with Experian Imagine receiving a phone call informing you that your antivirus software license is about to expire. You decide to renew it over the phone, and before you know it, you have been “TOAD-ed”! What is a TOAD attack? Telephone-Oriented Attack Deliveries (TOADs) are an increasingly common threat to businesses worldwide. According to Proofpoint's 2024 State of the Phish Report, 10 million TOAD attacks are made every month, and 67% of businesses globally were affected by a TOAD attack in 2023. In the UK alone, businesses have lost over £500 million to these scams, while in the United States the reported monetary loss averaged $43,000 per incident, with some losses exceeding $1 million.TOADs involve cybercriminals using real phone numbers to impersonate legitimate callers, tricking victims into divulging sensitive information or making fraudulent transactions. This type of attack can result in substantial financial losses and reputational damage for businesses. How TOAD attacks happen TOAD attacks often involve callback phishing, where victims are tricked into calling fake call centers. Before they strike, scammers will gather a victim's credentials from various sources, such as past data breaches, social media profiles, and information bought on the dark web. They will then contact the individual through applications like WhatsApp or call their phone directly. Here is a common TOAD attack example: Initial contact: The victim receives an email from what appears to be a reputable company, like Amazon or PayPal. Fake invoice: The email contains a fake invoice for a large purchase, prompting the recipient to call a customer service number. Deception: A scammer, posing as a customer service agent, convinces the victim to download malware disguised as a support tool, granting the scammer access to the victim's computer and personal information. These techniques keep improving. One of the cleverer tricks of TOADs is to spoof a number or email so they contact you as someone you know. Vishing is a type of phishing that uses phone calls, fake numbers, voice changers, texts, and social engineering to obtain sensitive information from users. It mainly relies on voice to fool users. (Smishing is another type of phishing that uses texts to fool users, and it can be combined with phone calls depending on how the attacker works.) According to Rogers Communication website, an employee in Toronto, Canada got an email asking them to call Apple to change a password. They followed the instructions, and a “specialist” helped them do it. After receiving their password, the cyber criminals used the employee's account to send emails and deceive colleagues into approving a fake payment of $5,000. Artificial intelligence (AI) is also making it easier for TOAD phishing attacks to happen. A few months ago, a Hong Kong executive was fooled into sending HK$200m of his company's funds to cyber criminals who impersonated senior officials in a deepfake video meeting. Effective countermeasures To combat TOAD attacks, businesses must implement robust solutions. Employee training and awareness: Regular training sessions and vishing simulations help employees recognize and respond to TOAD attacks. Authentication and verification protocols: Implementing multi-factor authentication (MFA) and call-back verification procedures enhances security for sensitive transactions. Technology solutions: Bots and spoofing detection and voice biometric authentication technologies help verify the identity of callers and block fraudulent numbers. Monitoring and analytics: Advanced fraud detection and behavioral analytics identify anomalies and unusual activities indicative of TOAD attacks. Secure communication channels: Ensure consumers have access to verified customer service numbers and promote secure messaging apps. A strong strategy should also involve using advanced email security solutions with AI fraud detection and machine learning (ML) to effectively defend against TOAD threats. These can help identify and stop phishing emails. Regular security audits and updates are necessary to find and fix vulnerabilities, and an incident response plan should be prepared to deal with and reduce any breaches. By integrating technology, processes, and people into their strategy, organizations can develop a strong defense against TOAD attacks. Keeping TOADS at bay with Experian® By working and exchanging information with other businesses and industry groups, you can gain useful knowledge about new or emerging threats and defense strategies. Governments and organizations like the Federal Communications Commission (FCC) have a shared duty to defend the private sector and public consumers from TOAD attacks, while many of the current rules and laws seem to lag behind what criminals are doing. By combining the best data with our automated ID verification processes, Experian® helps you protect your business and reputation. Our best-in-class solutions employ device recognition, behavioral biometrics, machine learning, and global fraud databases to spot and block suspicious activity before it becomes a problem. Learn more *This article includes content created by an AI language model and is intended to provide general information.

The world of finance can be a dangerous place, where cunning schemes lurk in the shadows, ready to pounce on unsuspecting victims. In the ever-evolving landscape of financial crime, the insidious ‘pig butchering’ scam has emerged as a significant threat, targeting both financial institutions and their clients. What is a ‘pig butchering’ scam? ‘Pig butchering’ scams are named after the practice of farmers fattening up their livestock before “butchering” them. This comparison describes the core of ‘pig butchering’ scams, where criminals entice victims to participate in investment schemes and cryptocurrency fraud. Originating in Southeast Asia and now rampant in the United States, these scams often start with online interactions via social media or dating applications. Scammers build trust with the victim, eventually gaining access to their online accounts. They "fatten the pig" by enticing more cryptocurrency investments and then make off with their ill-gotten gains. The repercussions are staggering, with reported losses exceeding $3.5 billion in 2023 alone according to an AP News article, and around 40,000 victims in the United States, including cases of losses as massive as $4 million. The real-life impact The story of “RB,” a San Francisco man who engaged with a scammer named "Janey Lee," serves as a stark warning. Through social media, Janey orchestrated an elaborate scheme, promising "RB” substantial returns in cryptocurrency investment. Seduced by false promises, “RB” emptied his life savings into the scam, only to be rescued by a Federal Bureau of Investigation (FBI) intervention, narrowly avoiding financial ruin.1 Malicious actors are improving their targeting skills, and often pursue executives and victims with a large sum of money, such as C-level officials from financial institutions. This past February, a $50 million pig slaughtering fraud incident caused the CEO of a local bank in Kansas to lose all his funds and the bank to collapse a few months later. FinCEN's vigilance and updates The Financial Crimes Enforcement Network (FinCEN) remains vigilant, issuing advisories to financial institutions to combat ‘pig butchering’ scams. Their latest advisory highlights evolving scam tactics, including aggressive promotions, using money mules for illegal fund transfers, and leveraging new financial products like decentralized finance (DeFi) platforms to obfuscate transactions. FinCEN also warns about red flags such as large and sudden investments from older customers, quick fund withdrawals after big deposits, and the frequent use of coins or mixers that hide transactions. Financial institutions are encouraged to: Report any suspicious activities by using specific terms like "pig butchering fraud advisory" in their reports to make analysis and response easier. File suspicious activity reports (SARs) using the key term “FIN-2023-PIGBUTCHERING.” Guide potential victims to report to the FBI’s IC3 or the Security and Exchange Commission (SEC’s) reporting system. A call to action for financial institutions The fight against ‘pig butchering’ scams requires proactive measures from financial institutions: Enhance fraud detection and anti-money laundering (AML) programs: Implement robust systems compliant with regulatory guidelines, conduct thorough customer enhanced due diligence, and leverage fraud detection software to spot anomalies and red flags., and leverage fraud detection software to spot anomalies and red flags. Leverage data analytics: Utilize data analytics tools to monitor customer behavior, identify irregular patterns, and swiftly detect potential ‘pig butchering’ activities. Employee training: Educate employees on scam risks, fraud detection techniques, and FinCEN red flags to empower them as the first line of defense., and FinCEN red flags to empower them as the first line of defense. Community education: Educate customers on recognizing and avoiding investment scams, promoting awareness, and safeguarding their assets. Navigating challenges with effective solutions ‘Pig butchering’ scams cause not only money losses but also personal troubles and reputational harm. Awareness, learning, and cooperation are essential in protecting from these complex financial fraudsters, securing the safety and confidence of your institutions and stakeholders. By combining the best data with our automated identification verification processes, you can protect your business and onboard new talents efficiently. Our industry-leading solutions employ device recognition, behavioral biometrics, machine learning, and global fraud databases to spot and block suspicious activity before it becomes a problem. Learn more 1San Francisco Chronical (2023). Crypto Texting Scam *This article includes content created by an AI language model and is intended to provide general information.

In the ever-expanding financial crime landscape, envision the most recent perpetrator targeting your organization. Did you catch them? Could you recover the stolen funds? Now, picture that same individual attempting to replicate their scheme at another establishment, only to be thwarted by an advanced system flagging their activity. The reason? Both companies are part of an anti-fraud data consortium, safeguarding financial institutions (FIs) from recurring fraud. In the relentless battle against fraud and financial crime, FIs find themselves at a significant disadvantage due to stringent regulations governing their operations. Criminals, however, operate without boundaries, collaborating across jurisdictions and international borders. Recognizing the need to level the playing field, FIs are increasingly turning to collaborative solutions, such as participation in fraud consortiums, to enhance their anti-fraud and Anti-Money Laundering (AML) efforts. Understanding consortium data for fraud prevention A fraud consortium is a strategic alliance of financial institutions and service providers united in the common goal of comprehensively understanding and combatting fraud. As online transactions surge, so does the risk of fraudulent activities. However, according to Experian’s 2023 U.S. Identity and Fraud Report, 55% of U.S. consumers reported setting up a new account in the last six months despite concerns around fraud and online security. The highest account openings were reported for streaming services (43%), social media sites and applications (40%), and payment system providers (39%). Organizations grappling with fraud turn to consortium data as a robust defense mechanism against evolving fraud strategies. Consortium data for fraud prevention involves sharing transaction data and information among a coalition of similar businesses. This collaborative approach empowers companies with enhanced data analytics and insights, bolstering their ability to combat fraudulent activities effectively. The logic is simple: the more transaction data available for analysis by artificial-intelligence-powered systems, the more adept they become at detecting and preventing fraud by identifying patterns and anomalies. Advantages of data consortiums for fraud and AML teams Participation in an anti-fraud data consortium provides numerous advantages for a financial institution's risk management team. Key benefits include: Case management resolution: Members can exchange detailed case studies, sharing insights on how they responded to specific suspicious activities and financial crime incidents. This collaborative approach facilitates the development of best practices for incident handling. Perpetrator IDs: Identifying repeat offenders becomes more efficient as consortium members share data on suspicious activities. Recognizing patterns in names, addresses, device fingerprints, and other identifiers enables proactive prevention of financial crimes. Fraud trends: Consortium members can collectively analyze and share data on the frequency of various fraud attempts, allowing for the calibration of anti-fraud systems to effectively combat prevalent types of fraud. Regulatory changes: Staying ahead of evolving financial regulations is critical. Consortiums enable FIs to promptly share updates on regulatory changes, ensuring quick modifications to anti-fraud/AML systems for ongoing compliance. Who should join a fraud consortium? A fraud consortium can benefit any organization that faces fraud risks and challenges, especially in the financial industry. However, some organizations may benefit more, depending on their size, type, and fraud exposure. Some of the organizations that should consider joining a fraud consortium are: Financial institutions: Banks, credit unions, and other financial institutions are prime targets for fraudsters, who use various methods such as identity theft, account takeover, card fraud, wire fraud, and loan fraud to steal money and information from them. Fintech companies: Fintech companies are innovative and disruptive players in the financial industry, who offer new and alternative products and services such as digital payments, peer-to-peer lending, crowdfunding, and robot-advisors. Online merchants: Online merchants are vulnerable to fraudsters, who use various methods such as card-not-present fraud, friendly fraud, and chargeback fraud to exploit their online transactions and payment systems. Why partner with Experian? What companies need is a consortium that allows FIs to collaboratively research anti-fraud and AML information, eliminating the need for redundant individual efforts. This approach promotes tighter standardization of anti-crime procedures, expedited deployment of effective anti-fraud/AML solutions, and a proactive focus on preventing financial crime rather than reacting to its aftermath. Experian Hunter is a sophisticated global application fraud and risk management solution. It leverages detection rules to screen incoming application data for identifying and preventing fraudulent activities. It matches incoming application data against multiple internal and external data sources, shared fraud databases and dedicated watch lists. It uses client-flexible matching rules to crossmatch data sources for highlighting data anomalies and velocity attempts. In addition, it looks for connections to previous suspected and known fraudulent applications. Hunter generates a fraud score to indicate a fraud risk level used to prioritize referrals. Suspicious applications are moved into the case management tool for further investigation. Overall, Hunter prevents application fraud by highlighting suspicious applications, allowing you to investigate and prevent fraud without inconveniencing genuine customers. To learn more about our fraud management solutions, visit us online or request a call. Learn more This article includes content created by an AI language model and is intended to provide general information.

It's 2024, and it has never been easier to buy a car in person or online, but automobiles are not quite as affordable as prior to the pandemic. While everyone is looking for the best car deal, some folks are pushing it too far and are falling for auto scams. What is auto lending fraud? Fraud perpetrators are drawn to sectors they perceive as highly lucrative. The accessibility of online vehicle financing and purchasing, coupled with the substantial financial magnitude associated with automotive transactions, renders the auto industry an optimal avenue for cash-out endeavors. Auto lending fraud refers to deceptive or fraudulent activities related to obtaining or processing auto finance. This can involve various schemes aimed at misleading lenders, financial institutions, or individuals involved in the lending process. Criminal networks now operate on social media sites like Facebook and Telegram, offering a unique car buying service using synthetic identities. They create synthetic identities, finance cars with no down payment, and deliver vehicles to addresses chosen by buyers. The process involves selecting a car online, sending a small amount of dollars and a photo against a white background, and receiving a fake driver's license. Those networks claim to exploit car sites' policies successfully. While appealing to those in urgent need of a car, the service poses significant risks as the synthetic identity may be used for other fraudulent activities beyond car purchase. Who is at risk? Everyone involved in the car buying process is at risk of falling victim to auto loan fraud. Car buyers looking to secure financing, as well as lenders, need to be aware of the potential red flags and take necessary precautions to safeguard their interests. Thieves leverage the internet and electronic transactions to perpetrate auto loan fraud. While the growth of online commerce has improved many aspects of trade, it has also made personally identifiable information and financial details vulnerable to data breaches. Unscrupulous individuals can gain unauthorized access to such information, providing the foundation for various identity theft schemes. The internet also facilitates the creation of seemingly legitimate documents that support auto loan fraud. Online services exist to help fraudsters fabricate income statements and fake employment verification from fictitious companies. This trend has made auto loan fraud an increasingly popular method for acquiring vehicles with minimal cash and risk. Another auto loan fraud trend is the increased use of CPN (Credit Privacy Number). Credit Repair firms introduced a novel strategy targeting consumers — the CPN (Credit Privacy Number). Marketed as a nine-digit alternative to a Social Security Number (SSN), CPNs are purportedly usable for obtaining credit. However, it is crucial to note that utilizing a CPN for credit applications constitutes a criminal offense, potentially leading to legal consequences, and car dealerships should not accept them. Detecting auto loan fraud There are several types of auto loan fraud worth noting to better understand the landscape: Income fabrication: Prospective buyers may falsify their income details to qualify for a larger loan or better terms. Lenders should verify income using documents like pay stubs, tax returns, or bank statements and watch out for inconsistencies. Employment misrepresentation: Applicants could lie about their job titles or employment status. Lenders should verify employment details through HR departments or by directly contacting the employer. Trade-in vehicle deception: Some individuals may overstate the value of their trade-in vehicle to secure a higher loan amount. Lenders should perform thorough appraisals or consult trusted sources to ascertain the accurate value of the trade-in. Identity fraud: Fraudsters can assume someone else's identity, commit first party fraud or create a fictitious persona to obtain an auto loan. Lenders must verify the applicant's identity using reliable identification documents and consider using identity verification tools. Forged documentation: Fraudsters may forge or alter documents like income statements, bank statements, or driver's licenses. Lenders should scrutinize documents carefully for discrepancies or signs of tampering. Straw borrower fraud: In this scenario, someone with poor credit convinces a friend or relative with better credit to front the deal, posing as the buyer. A better credit score allows for better terms or a more valuable vehicle. The actual buyer may continue to make payments to the friend, or the loan may become delinquent, negatively affecting the friend's credit score. In extreme cases, the straw buyer is part of a fraud ring, and the vehicle has already been sold in a foreign market. Synthetic identity fraud: Data breaches providing personally identifying information enable identity theft schemes. Perpetrators use illicitly acquired information to create false borrower profiles that appear authentic. These profiles typically have excellent credit, a social security number, an affluent home address, stable employment, and other attributes that make them seem like desirable borrowers. However, a detailed investigation reveals subtle inconsistencies indicative of high risk. How to prevent auto loan fraud To combat auto loan fraud and protect profitability, auto lenders can leverage technological advancements. By applying analytics and machine learning to millions of loan applications and histories, you can identify fraudulent patterns and inconsistencies. Machine learning can determine the type of suspected fraud and provide a confidence factor to guide further investigation and verification. Additionally, you should: Conduct thorough background checks on prospective buyers and verify their personal information and documents. and verify their personal information and documents. Implement a comprehensive loan underwriting process that includes income verification, employment verification, and collateral evaluation. Educate employees about common fraud schemes, warning signs, and best practices to ensure they remain vigilant during loan applications. Foster a culture of cooperation with local law enforcement agencies, sharing information about suspected fraudsters to help prevent future incidents. It is important for individuals and businesses to be vigilant and report any suspicious activity. Car dealerships and financial institutions work to prevent fraud through proper identification verification, credit checks, and adherence to legal and ethical standards. If you suspect fraudulent activity or identity theft, it is crucial to report it to the appropriate authorities immediately. Gearing-up Taking advantage of the latest fintech capabilities, such as cloud-based loan origination that integrates analytics, machine learning, and automated verification services, can significantly reduce the likelihood of fraudulent applications becoming another auto lending fraud statistic. By combining the best data with our automated ID verification checks, Experian helps you safeguard your business and onboard customers efficiently. Our best-in-class solutions employ device recognition, behavioral biometrics, machine learning, and global fraud databases to spot and block suspicious activity before it becomes a problem. Learn more about our automotive fraud prevention solutions *This article includes content created by an AI language model and is intended to provide general information.

It is a New Year and a new start. How about a new job? That is what thousands of employees will consider over the next month. It is also a time for employers to attract new talents, but they must be aware of different types of employment fraud. The rise of remote work has significantly increased the prevalence of remote hiring practices, from the initial job application to the onboarding process and beyond. Unfortunately, this shift has also opened the door to a surge in imposter employees, also known as ‘candidate fraud,’ posing a significant concern for organizations. How does employment identity theft happen? Instances of potential job candidates utilizing real-time deepfake video and deepfake audio, along with personally identifiable information (PII), during remote interviews to secure positions within American companies have been on the rise. The Federal Bureau of Investigation (FBI) reports that fraudulent individuals often acquire PII through fake job opening posts, which enable them to gather candidate information and resumes. Surprisingly, the tools necessary for impersonation on live video calls do not require sophisticated or expensive hardware or software. Employment identity theft can occur in several ways. Here are a few examples: Inaccurate credentials: Employers may inadvertently hire someone with false or stolen credentials if they fail to conduct comprehensive background checks. When the employer discovers the deception, it can be challenging to trace the true identity of the person they unknowingly hired. Limited-term job offers: Some industries offer temporary job opportunities in distant locations. Individuals with criminal backgrounds may steal victims' identities to apply for these jobs, hoping that their crimes will go unnoticed until after the job is complete. Perpetrated by colleagues: In rare instances, jealous colleagues or coworkers can commit employment identity theft. They may steal a coworker's information during a data breach and sell it on the dark web or use the victim's credentials to frame them for fraudulent workplace actions. Preventing employment identity theft In addition to the reported cases of imposter employee fraud, it is crucial to acknowledge the potential for other scams that exploit new technologies and the prevalence of remote work. Malicious cyber attackers could secure employment using stolen credentials, enabling them to gain unauthorized access to sensitive data or company systems. A proficient hacker possessing the necessary IT skills may find it relatively easy to leverage social engineering techniques during the hiring process. Consequently, the reliability of traditional methods for employee verification, such as face-to-face interactions and personal recognition, is diminishing in the face of remote work and the technological advancements that enable individuals to manipulate their appearance, voice, and identity. To mitigate risks associated with hiring imposters, it is imperative to incorporate robust measures into the recruitment process. Here are some key considerations: Establish clear policies and employment contracts: Clearly communicate your organization's policies regarding moonlighting in employment contracts, employee handbooks, or other official documents. Confidentiality and non-compete agreements: Implement confidentiality and non-compete agreements to protect your company's sensitive information and intellectual property. Monitoring: Automate employment and income verification of your employees. Provide training on cybersecurity best practices: Educate employees about cyber-attacks and identity scams, such as phishing scams, through seminars and workplace training sessions. Implement robust security measures: Use firewalls, encrypt sensitive employee information, and limit access to personal data. Minimize the number of employees who have access to this information. Thoroughly screen new employees: Verify the accuracy of Social Security numbers and other information during the hiring process. Conduct comprehensive background checks, including checking bank account information and credit reports and fight against synthetic identities. Offer identity theft protection as a benefit: Consider providing identity theft protection services to your employees as part of their benefits package. These services can detect and alert victims of potential identity theft, facilitating a fast response. The new era of remote work necessitates a fresh perspective on the hiring process. It is crucial to reevaluate HR practices and leverage AI fraud detection technologies to ensure that the individuals you hire, and employ are who they claim to be, guarding against the infiltration of imposters. Navigating employment fraud with effective solutions Employment fraud presents significant risks and challenges for employers, including conflicts of interest, reputation damage, and breaches of confidentiality. By taking the right preventative measures, you can safeguard your organization and employees. Streamlining the hiring process is essential to remain competitive. But how do you balance the need for speed and ease of use with essential ID checks? By combining the best data with our automated ID verification processes, Experian helps you protect your business and onboard new talents efficiently. Our best-in-class solutions employ device recognition, behavioral biometrics, machine learning and global fraud databases to spot and block suspicious activity before it becomes a problem. Learn more about preventing employement fraud *This article includes content created by an AI language model and is intended to provide general information.

The online gaming industry has experienced tremendous growth in recent years, with millions of players engaging in immersive virtual worlds and competitive gameplay. Unfortunately, this surge in popularity has also sparked an increase in online gaming fraud. Unscrupulous individuals have sought to exploit the industry through fraudulent activities, leading to financial losses and reputational damage for gaming vendors.According to a recent study conducted by Lloyds Bank, children are spending more time playing online games than ever before – over five million children between the ages of three and 15 are now regularly playing games online, up from approximately 4.6 million in 2019.Fraudsters, always ready to take advantage of opportunities presented by new trends, are now increasingly targeting this rising demographic. Gaming vendors have a responsibility to shield minors from fraud in online gaming by implementing robust safety measures, educating young players and their parents, and actively monitoring and addressing fraudulent activities. A vulnerable target That same study from Lloyds revealed that over a third (36%) of parents are concerned about the possibility of their children falling victim to gaming fraud and losing money. In today's tech-savvy world, the ease of payment authorization has only exacerbated these concerns. All it takes for a child to make a payment is to key in their parents' online store username and password. It is a practice fraught with danger. Parents can only do so much to safeguard their children while gaming, and despite their best efforts, there will always remain a lingering possibility of encountering scammers. Gaming vendors should establish robust age verification processes during account creation to ensure that minors are not exposed to age-inappropriate content. Additionally, they should incorporate comprehensive parental controls that allow parents to regulate their children's online activities, including chat limitations, spending controls, and access to certain features.But contrary to common assumptions, the gaming population is not restricted to teenagers or young adults. With an average age of 35, gamers have significant purchasing power and actively participate in the gaming ecosystem. They spend an average of over six hours per week gaming, dedicating nearly an hour each day to their preferred gaming experiences. This engagement is spread across all age groups and financial profiles, making the gaming community a vast market to attract cybercrime. Types of fraud in online gaming In 2022, the revenue from the worldwide gaming market was estimated at almost 347 billion U.S. dollars, with the mobile gaming market generating an estimated 248 billion U.S. dollars of the total. The gaming market is constantly evolving, and technological advancements are opening new possibilities for game developers to create more immersive and engaging experiences.But alarming reports indicate that scammers have honed in on the younger demographic of gamers, leveraging their innocence to exploit their finances and identities. Identity theft (67%) and hacking (61%) rank as the two most prevalent forms of fraud experienced by young gamers, according to the Lloyds Bank study. Here are some different types of online gaming fraud: Account hacking: Hackers employ various techniques like phishing, keylogging, and credential stuffing to gain unauthorized access to players' accounts. Once compromised, accounts could be used for fraudulent activities, including unauthorized in-game transactions or selling virtual assets for real money. Chargeback fraud: This occurs when players make legitimate purchases within a game using real money and then issue chargebacks, falsely claiming that the transaction was unauthorized or fraudulent. This results in financial losses for gaming vendors as they lose the revenue and virtual goods/services provided to the player. Virtual asset fraud: Virtual assets, such as in-game currency, items, or characters, hold economic value. Fraudsters engage in scams involving fake virtual asset transactions or market manipulation, exploiting players' desires to acquire rare or high-value items. Match-fixing and cheating: Competitive gaming is at the heart of many online games. Fraudsters seek to manipulate matches, exploit glitches, or use cheat software to gain an unfair advantage over others. This undermines the integrity of the gaming experience and discourages fair competition. The game changer for online platforms: fraud prevention strategies Given the anticipated growth of these threats in the foreseeable future, it is imperative that online platforms prioritize the protection of young gamers and their parents. In line with the enhanced safeguards and anti-fraud initiatives observed in banks and financial institutions, it is high time for game companies to elevate their security and consumer protection measures by adopting the following guidelines: Implement strong account security measures: Encourage players to create unique, complex passwords, and consider implementing multifactor authentication solutions. Regularly educate players about common hacking techniques and promote safe browsing habits to prevent phishing attempts. Utilize fraud detection systems: Invest in advanced fraud detection tools that employ machine learning algorithms and biometrics templates to identify suspicious activities and patterns. These systems can flag potentially fraudulent transactions, allowing you to take appropriate measures promptly. Monitor and analyze user behavior: Keep an eye on players' activities and digital identity, such as unusual login patterns, high-value transactions, or frequent chargebacks. Analyze gameplay data, interactions, and purchasing behavior to identify patterns indicative of fraud or cheating. Secure payment processing systems: Choose reputable payment gateways that prioritize security measures. Employ tokenization and encryption technologies to safeguard players' payment information during transactions. Regularly test and update your payment system's security infrastructure. Raise player awareness: Educate your player community about common fraud techniques and the importance of securing their accounts with identity authentication. Share security tips through newsletters, blog posts, and in-game messaging. Foster a culture of vigilance and encourage players to report any suspicious activities. Foster fair gameplay and zero tolerance policy: Implement robust anti-cheat measures and regularly update your game to address vulnerabilities and exploits. Promote fair competition and enforce a zero-tolerance policy against cheating, match-fixing, and other forms of unfair gameplay. Leveling-up Ultimately, the ability to protect players online could be the ultimate gamechanger for gaming platforms. By embracing identity verification mechanisms that rely on secure and privacy-centric facial recognition, online fraud and identity theft can be significantly curtailed. Moreover, the verification and onboarding processes can be streamlined, simplifying the user experience further. Just as bringing top-tier games on board is crucial, game platforms must ensure their customers engage in a secure gaming environment. Streamlining the onboarding and sign-in process is essential to remain competitive. But how do you balance the need for speed and ease of use with essential ID checks? By combining the best data with our automated ID verification checks, Experian helps you safeguard your business and onboard customers efficiently. Using passive, invisible checks when customers sign into their accounts helps to keep fraudsters at bay and protects legitimate players without the need for irritating security challenges. Experian’s best-in-class solutions employ device recognition, behavioral biometrics, machine learning and global fraud databases to spot and block suspicious activity before it becomes a problem. Learn more *This article leverages/includes content created by an AI language model and is intended to provide general information.