All posts by Guest Contributor

Over the last year and a half, strong trends emerged in how businesses and consumers interact online - specifically when validating identities and preventing fraud. We initially explored these trends at a global level, and now we've explored U.S.-specific insights into online security, the customer experience, and digital activities and operations. Download the North America findings report to learn more about business and consumer fraud and identity trends impacting the way we live, work, and interact. Review your fraud strategy

For credit unions, having the right income and employment verification tools in place helps to create an application process that is easy and low friction for both new and existing members. Digital first is member first The digital evolution created an expectation for online experiences that are simple, fast, and convenient. Attracting and building trusted, loyal relationships and paving the way for new revenue-generating opportunities now hinges on a lender's ability to provide experiences that meet those expectations. At the same time, market volatility and economic uncertainty are driving catalysts behind the need for credit unions to gain a more holistic view of a member’s financial stability. To gain a competitive advantage in today’s lending environment, credit unions need income and employment verification solutions that balance two often polarizing business drivers: member experience and risk management. While verified income and employment data is key to understanding stability, it’s equally important to streamline the verification process and make it as frictionless as possible for borrowers. With these things in mind, here are three considerations to help credit unions ensure their income and employment verification process creates a favorable member experience. The more payroll records, the better Eliminate friction for members by tapping into a network of millions of unique employer payroll records. Gaining instant access into a database of this scale helps enable decisions in real-time, eliminates the cost and complexity of many existing verification processes, and allows members to skip cumbersome steps like producing paystubs. Create a process with high configuration and flexibility Verification is not a one-size-fits-all process. In some cases, it might be advantageous to tailor a verification process. Make sure your program is flexible, scalable and highly configurable to meet your evolving business needs. It should also have seamless integration options to plug and play into your current operations with ease. The details are in the data When it comes to income and employment verification, make sure that you are leveraging the most comprehensive source of consumer information. It’s important that your program is powered by quality data from a wealth of datasets that extend beyond traditional commercial businesses to ensure you are getting the most comprehensive view. Additionally, look to leverage a network of exclusive employer payroll records. With both assets, make sure you understand how frequently the data is refreshed to be certain your decisioning process is using the freshest and highest-quality data possible. Implementing the right solution By including a real-time income and employment verification solution in your credit union’s application process, you can improve the member experience, minimize cost and risk, and make better and faster decisions. To learn more about Experian’s income and employment verification solutions, or for a complimentary demo, feel free to contact an expert today. Learn more Contact us

Earlier this year, we shared our predictions for five fraud threats facing businesses in 2021. Now that we’ve reached the midpoint of the year and economic recovery is underway, we’re taking another look at how these threats can impact businesses and consumers. Putting a Face to Frankenstein IDs: Synthetic identity fraudsters will attempt to bypass fraud detection methods by using AI to combine facial characteristics from different people to form a new identity. Overexposure: As many as 80% of SSNs may have been exposed on the dark web, creating opportunities for account application fraud. The Heist: Surges in data breaches, advances in automation, expanded online banking services and vulnerabilities exposed from social engineering mistakes have lead to rises in account takeover fraud. Overstimulated: Opportunistic fraudsters may take advantage of ongoing relief payments by using stolen data from consumers. Behind the Times: Businesses with lackluster fraud prevention tools and insufficient online security technology will likely experience more attacks and suffer larger losses. To learn more about upcoming fraud threats and how to protect your business, download our new infographic and check out Experian’s fraud prevention solutions. Download infographic Request a call

As stimulus-generated fraud wanes, we anticipate a return of more traditional forms of fraud, including account opening fraud. As businesses embrace the digital evolution and look ahead to responsible growth, it’s important to balance the customer experience with the risks associated with account opening fraud. Preventing account opening fraud requires a layered fraud and identity management strategy that allows you to approve good customers while keeping criminals out. With the right tools in place, you can optimize the customer experience while still keeping risk low. Download infographic Review your fraud strategy

Experian’s Q1 2021 Automotive Market Trends Review revealed that some of the once-consistent new registration generational trends have reversed.

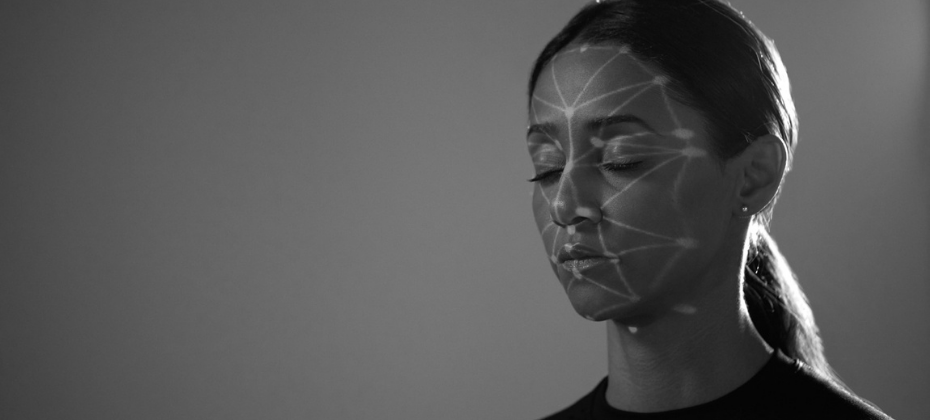

Over the past year and a half, the development of digital identity has shifted the ways businesses interact with consumers. Companies across every industry have incorporated digital services, biometrics, and other verification tools to enhance the consumer experience without increasing risk. Changing consumer expectations A digital identity strategy is no longer a nice-to-have, it’s table stakes. Consumers expect to be recognized across platforms and have a seamless experience every time. 89% of consumers use mobile banking 80% of companies now have a customer recognition strategy in place 55% of banking customers say they plan to visit the bank branch less often moving forward Businesses are responding to these changing expectations while working to grow during the economic recovery – trying to balance consumer experience with risk appetite and bottom-line goals. The present state of digital identity Digital identity strategies require both standardization and interoperability. The first provides the ability to consistently capture data and characteristics that can be used to recognize a specific individual. The second allows businesses to resolve an identity to a specific person – recognizing a phone number, user ID and password, or a device – and use that information to determine if the user of the identity is in fact the identity owner. There are some roadblocks on the road to a seamless digital identity strategy. Issues include a lack of consumer trust and an ambiguous regulatory landscape – creating friction on both ends of the equation. Recipe for success To succeed, businesses need a framework that can reliably use different combinations of physical and digital identity data to determine that the person behind the identity is a known, verified, and unique individual. A one-size-fits-all solution doesn’t exist. However, a layered approach allows businesses to modernize identity, providing the services consumers want and expect while remaining agile in an ever-changing environment. In our newest white paper, developed in partnership with One World Identity, we explore the obstacles hindering digital identity management, and the best way to build a layered solution that is flexible, trustworthy, and inclusive. To learn more, download our “Capturing the Digital Evolution Through a Layered Approach” white paper. Download white paper

In the Q1 2021 Market Trends Review, we explore the average age myth and highlight other ways to inform aftermarket strategy.

The pandemic changed nearly everything – and consumer credit is no exception. Data, analytics, and credit risk decisioning are gaining an even more significant role as we grow closer to the end of the global crisis. Consumers face uneven roads to recovery, and while some are ready to spend again, others are still dealing with pandemic-related financial stress. We surveyed nearly 9,000 consumers and 2,700 businesses worldwide about how consumers are stabilizing their finances and businesses are returning to growth for our new Global Decisioning Report. In this report, we dive into: Key business priorities in 2021 Financial concerns for consumers How to navigate an uneven recovery Business priorities for the year ahead The importance of the online experience As we begin to near the end of the pandemic, businesses need to prioritize technology that enables a responsive, flexible, efficient and confident approach. This can be done by leveraging advanced data and analytics and integrating machine learning tools into model development. By investing in the right credit risk decisioning tools now, you can help ensure your future. Download the report

As quarantine restrictions lift and businesses reopen, there is still uncertainty in the mortgage market. Research shows that more than two million households face foreclosure as moratoriums expire. And with regulators, like the Consumer Financial Protection Bureau (CFPB), urging mortgage servicers to prepare for an expected surge in homeowners needing assistance, lenders need the right resources as well. One of the resources mortgage lenders rely on to help gain greater insight into their borrower’s financial picture is income and employment verification. The challenge, however, is striking the right balance between gaining the insights needed to support lending decisions and creating a streamlined, frictionless mortgage process. There are three main barriers on the path to a seamless and digital verification process. Legacy infrastructure Traditional verification solutions tend to rely on old technology or processes. Whether a lender’s verification strategy is centered around a solution built on older technology or a manual process, the time to complete a borrower verification can vary from taking a day to weeks. Borrowers have grown accustomed to digital experiences that are simple and frictionless and experiencing a drawn out, manual verification process is likely to impact loyalty to the lender’s brand. Stale employment and income data The alternative to a manual process is an instant hit verification solution, with the aim to create a more seamless borrower experience. However, lenders may receive stale borrower income and employment data back as a match. Consumer circumstances can change frequently in today’s economic environment and, depending on the data source the lender is accessing, data may be out of date or simply incorrect. Decisioning based on old information is problematic since it can increase origination risk. Cost and complexity Lenders that use manual processes to verify information are adding to their time to close and ultimately, their bottom line by way of time and resources. Coupled with pricing increases, lenders are paying more to put their borrowers through a cumbersome and sometimes lengthy process to verify employment and income information. How can mortgage lenders avoid these common pitfalls in their verification strategy? By seeking verification solutions focused on innovation, quality of data, and that are customer-centric. The right tool, such as Experian VerifyTM, can help provide a seamless customer experience, reduce risk, and streamline the verification process. Learn more

Experian recently announced its expansion into Employer Services and the release of a new suite of real-time income and employment verification products, Experian Verify™. The COVID-19 pandemic amplified lenders' need for deeper insights into a consumer's financial situation. At the same time, employers were flooded with record-breaking unemployment claims, while managing stay-at-home orders, income and employment verification fulfillment requests, and more. "We're committed to helping employers, businesses, lenders, and consumers on the road to recovery from the pandemic and beyond," said Alex Lintner, Group President Experian Consumer Information Services. "To support this, we're building two businesses: Experian Employer Services and Verification Solutions. These businesses will create meaningful change and provide our clients with competitive options to achieve their verification needs while helping improve access to credit for consumers." With Experian Verify, lenders can quickly and easily create a more complete picture of a consumer's financial situation by verifying an applicant's income and employment status. Powered by our growing network of payroll and proprietary employer data, Experian Verify offers lenders flexible and secure access to income and employment records. With a consumer's consent, lenders can request the information from Experian and an income and employment report can be delivered to lenders through an API, online Experian dashboard, or paired with an Experian credit report. "As we begin to recover from the COVID-19 pandemic and employers are reopening their doors, we're confident we have assembled the best-of-the-best to help employers overcome their toughest challenges. We're committed to leveraging our combined capabilities and focus on high-touch customer service to deliver secure, scalable and transparent services to employers," said Michele Bodda, President of Experian Mortgage, Employer Services and Verification solutions. Visit us for more information on Experian Verify and Experian's Employer Services. Contact us

Forrester recently named Experian to their Programs of the Year awards, which recognize outstanding achievements in a particular area in sales, marketing and product functions. Forrester gives this award to companies who achieve the successful implementation of Forrester’s research, frameworks and best practices to improve functional performance. At Experian, innovation is at the heart of what we do. We strive for continuous improvement, and look for ways to progress our products and services to better serve businesses and consumers. Over the last year, Experian’s Decision Analytics Portfolio Marketing team engaged with Forrester’s SiriusDecisions group to refine the programs they employ to assess and respond to market needs while meeting their stated growth and performance goals. Experian’s Keir Breitenfeld, Vice President, Portfolio Marketing, Experian Decision Analytics, who presented the team’s results at the recent Forrester B2B summit said, “I’m proud of the Decision Analytics Portfolio Marketing team for what they accomplished while working alongside Forrester SiriusDecisions. We were able to reframe how we assess market opportunities for increased impact as we highlight Experian’s areas of expertise to better serve businesses and the consumers that rely on them.” To learn more about the Programs of the Year award and how Experian innovation helps businesses achieve their goals, visit us or request a call. Contact us

The surge in digital demand over the past year reinforced the deep connection between recognition, fraud prevention and the online customer experience. As businesses transformed their operations to accommodate the rapidly growing volume of digital transactions, consumer expectations for easy, secure interactions increased at an even faster pace. That meant less tolerance for the interruptions caused by security and risk controls. We surveyed more than 9,000 consumers and 2,700 businesses worldwide about this connection for our 2021 Global Identity and Fraud Report. This year’s report dives into: Business priorities for the year ahead Why the digital customer experience remains siloed Consumer preferences that impact the digital customer journey Pandemic-era digital activities that have changed consumer expectations As we move forward into the rest of 2021 it’s crucial that businesses continue to focus on fraud prevention. In order to implement an effective fraud strategy that also makes it easier for customers to engage, businesses need to move away from a one-size-fits-all approach and focus on applying the right level of protection to each and every transaction. Download the report Review your fraud strategy

At some point a lender may need to issue an RFI or an RFP for a credit decisioning system. In this latest installment of “working with vendors” let’s dive into some best practices for writing RFIs and RFPs that will help you more quickly and efficiently understand the capabilities of a vendor. First, have one person (or at most a very small group) review the document before it goes out to vendors. Too often these kinds of documents seem like they’re just cut and pasted together without any concern if they paint a coherent picture. If it’s worth the time to write an RFI/RFP, then it’s worth the time to get it right so that the vendor responses make sense. If your document paints an inconsistent picture, a vendor may not know what products will best serve your requirements. In turn, precious time will be wasted in discussions around what’s being proposed. Here are some things to make clear in the document: For what part of the credit life cycle does this RFI/RFP apply (prospecting, origination, account management or collections)? If the request covers more than one part of the life cycle, make clear which questions apply to which part of the life cycle. Do you need a system that processes in batch or real-time requests (or both)? For example, a credit card account management solution can process accounts in batch (for proactive line management), in real time (for reactive requests) or possibly even both. Let the vendor know what it is you’re trying to do, as there may be different systems involved in processing these requests. Do you want this system hosted at the vendor, a third party (like AWS, Azure, etc.) or installed on premises? If you have a preference, let the vendor know. If you have no preference, ask the vendor what they can support. In general, consider playing down or skip detailed pricing questions. There’s nothing wrong with asking for a price range. For credit decisioning systems, detailed pricing is difficult for the vendor since there are often high levels of unknown customization to do. A better question might be, “What things will the vendor have to know in order to accurately price the solution? What are the logical next steps to get more accurate pricing? What’s the typical range of pricing in a solution such as this and what drives that range?” Will you be acting as an aggregator? Sometimes systems are created as front ends to several lenders. For example, a client may want to create a website where a borrower can “shop” among several lenders. This is certainly doable but carries with it a whole host of legal, compliance, business and technical questions. In my opinion, I’d skip the RFI/RFP in this situation and have a robust sit down directly with the vendors. This option will likely be far more productive. Ask more open-ended questions. “How does the solution perform task X?” as opposed to, “Do you support Y?” Often, there’s more than one way to accomplish a task. Asking more open-ended questions will yield a more comprehensive answer from the vendor rather than a simple yes or no response. It also gives you the opportunity to learn about the latest decisioning techniques. Be careful that you have not copied old RFP questions that are no longer relevant. I’ve had clients ask if we support Bernoulli Boxes (a mid-80s kind of floppy disk), or whether we support OS/2, etc. I’ve even had questions about supporting a particular printer. These kinds of questions are centered on the support of the operating system and not a particular vendor’s credit decisioning software. Instead of asking yes/no technology questions, ask for a typical sample architecture. Ask what kinds of APIs are supported (REST, SOAP/XML, etc.). Ask about the solution’s capabilities to call third-party systems (both internal and external). Ask fewer, but more in-depth questions. If the solution needs screens, be clear which screens you’re talking about. Do you need screens to make rule adjustments or configuration changes? Do you need screens for manual review or some sort of case management? Do you need consumer-facing screens where borrowers can type in their application data? If you need screens, be clear on the task the screens should perform. If you have particular concerns, ask them in an open-ended way. For example, “The solution will have to exchange file-based data with a mainframe. How can your solution best satisfy this requirement?” In general, state your requirement not the technology to use. A preamble or brief executive summary is useful to get the big picture across before the vendor delves into any questions. A paragraph or two can go a long way to help the vendor better assess your requirements and provide more meaningful answers to you. This works well because it’s easier to give the big picture in a few paragraphs as opposed to sprinkled around in multiple questions. To summarize, be clear on your requirements and provide a more open-ended format for the vendor to respond. This will save both you and the vendor a lot of time. In section three, I’ll cover evaluating vendors.

Experian’s Q4 2020 Market Trends Review takes a closer look at aftermarket trends, including the growing sweet spot.

The sharp uptick in fraud that coincided with the digital evolution made it clear that banks, credit unions, and fintechs need to invest in a strategy that utilizes identity layers to keep their customers and their finances safe. The steady rise in fraud over the last several years spiked—payment fraud rose 70% last year and is expected to increase by 95% in 2021—making it more challenging than ever to address the fraud threat while meeting increasing customer expectations. The rising fraud threat 2020 saw a rapid influx of customers using digital channels and the amount of data flowing into financial systems. There’s been a seismic shift, and we’re not going back. According to a recent study, 80% of consumers now prefer to manage their finances digitally, leaving the door open for fraudsters to take advantage of digital newbies. The increase in online activity corresponded with criminal activity. The rates of synthetic identity, account opening, and account takeover fraud have risen as fraudsters’ tactics have evolved. 80% of fraud losses now come from synthetic identities In 2020 the rate of new account credit card fraud attempts rose 48% Account takeover accounted for 54% of all fraud attacks in 2020 Fraudsters will continue to take advantage of current conditions, moving from stimulus-related fraud back to more traditional forms of financial theft, and financial institutions must adapt in turn with robust identity layers. Resolving the identity threat In our recent white paper, developed in partnership with One World Identity, we explore how businesses can address the fraud threat. It requires a multilayered identity proofing strategy for both onboarding and ongoing authentication. By doing this, financial institutions can gain a holistic view of consumers and their associated risks, decreasing friction while enabling robust fraud protection. To learn more, download our “Improving Fraud by Increasing Identity Layers” white paper. Download white paper