All posts by Stefani Wendel

If you're looking for a competitive edge in 2020, Vision is your ticket into differentiating your organization with the latest insights and innovation.

Exploring some of the top trends for the financial services industry going into the new decade from data and decisioning to fraud and customer experience.

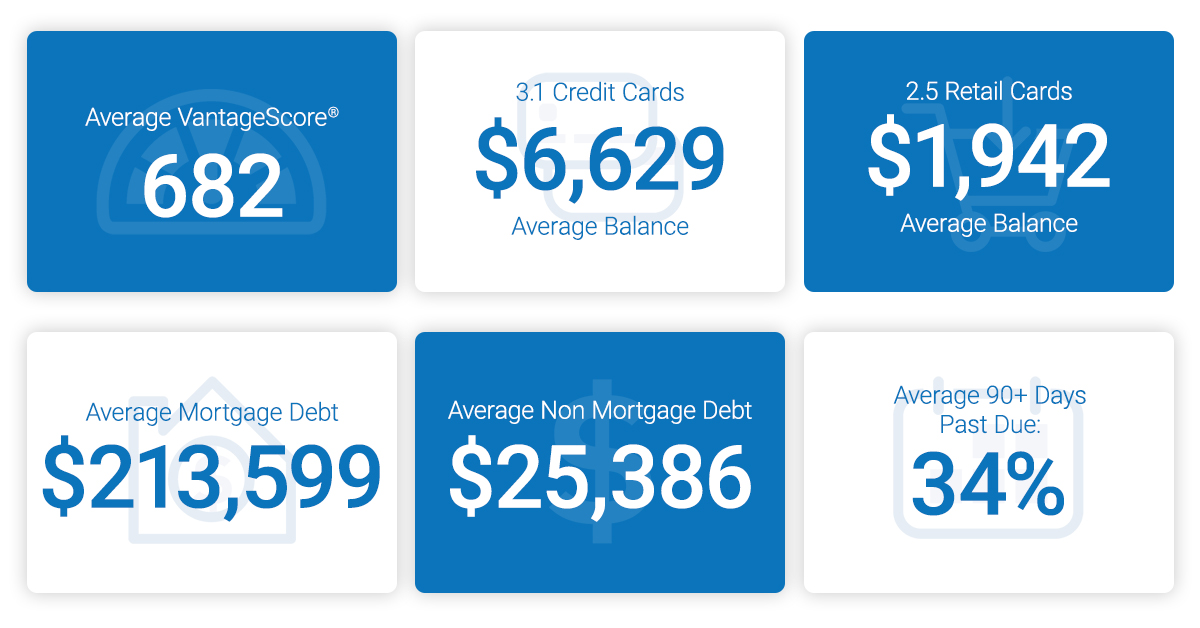

As look forward to the next decade, things are looking up. The 10th annual State of Credit Report highlights consumer credit scores and borrowing behavior.

Experian and Oliver Wyman have joined forces to launch Ascend CECL Forecaster to help financial institutions of all sizes forecast lifetime credit losses.

The next recession is a matter of when, not if. As the economy shifts, so will the priorities for your portfolio, so now is the time to strategize.

The 2019 report reveals new consumer and lending insights, an overview of the regulatory landscape, and what's next for machine learning and alt data.

Experian's annual State of Credit Report includes consumer credit data trends and a 10 year look back to when America started to enter the recession.

Day 2 of the annual conference covered topics ranging from alternative credit data and regulatory compliance to marketing analytics and fraud.

Experian's annual thought leadership conference will be held May 5-8 in San Antonio Texas, and will feature 50+ sessions on the industry's latest trends.

As Gen Z enters the economy, they bring with them an entirely new set of priorities when it comes to their finances. Move over Millennials.

Recent studies show many Americans consider debt a deal-breaker when it comes to their romantic relationships. Who is carrying the debt?

Alternative Credit Data and Trended Data have different strengths, but when used together, they can make a world of difference on your strategy as a whole.

In the head to head match up between alternative credit data and trended data, who will win? Both offer value above and beyond traditional credit data.

Lenders and financial institutions can help their customers get on the right financial foot for 2019 by helping them maximize their tax refund.

Credit access for the masses, machine learning and fraud are among the top 5 trending topics for the financial services industry in 2019.