All posts by Theresa Nguyen

Since 1996, The Internal Revenue Service (IRS) has issued more than 27 million individual taxpayer identification numbers (ITINs) – a 9-digit number used by individuals who are required to file or report taxes in the United States but are not eligible to obtain a Social Security number (SSN). Across the country, ITIN holders are actively contributing to their communities and the U.S. financial system. They pay bills, build businesses, contribute billions in taxes and manage their finances responsibly. Yet despite their clear engagement, many remain underrepresented within traditional lending models. Lenders have a meaningful opportunity to bridge the gap between intention and impact. By rethinking how ITIN consumers are evaluated and supported, financial institutions can: Reduce barriers that have historically held capable borrowers back Build products that reflect real borrower needs Foster trust and strengthen community relationships Drive sustainable, responsible growth Our latest white paper takes a more holistic look at ITIN consumers, highlighting their credit behaviors, performance patterns and long-term growth potential. The findings reveal a population that is not only financially engaged, but also demonstrating signs of ongoing stability and mobility. A few takeaways include: ITIN holders maintain a lower debt-to-income ratio than SSN consumers. ITIN holders exhibit fewer derogatory accounts (180–400 days past due). After 12 months, 76.9% of ITIN holders remained current on trades, a rate 15% higher than SSN consumers. With deeper insight into this segment, lenders can make more informed, inclusive decisions. Read the full white paper to uncover the trends and opportunities shaping the future of ITIN lending. Download white paper

Growth, risk and the rise of "hidden" business accounts As inflation remains elevated and early signs of labor market cooling emerge, the credit card landscape is entering its next phase. Over the past few weeks, policy actions and discussions around potential interest-rate caps have driven increased uncertainty across the credit card industry and broader global markets. Lenders face a careful balancing act: capturing growth opportunities while maintaining disciplined risk oversight. Our second annual State of Credit Cards Report explores the macroeconomic forces influencing the market, key shifts in originations and delinquency trends, and lender mix. New this year, the report also digs into an often‑overlooked segment: business accounts hidden inside consumer credit card portfolios. Additionally, the report offers actionable strategies to help lenders segment risk and drive disciplined growth more effectively. Key insights include: 30+ DPD delinquency rates remained above pre-pandemic levels in 2025, underscoring the need for disciplined asset‑quality monitoring. Fintechs continue to gain ground, posting a 71% YOY increase in account originations. Business accounts masked in the consumer credit card universe represent roughly 14% of balances and are more than 50% larger than the business card universe — a material segment with distinct risk and profitability dynamics that many lenders are not explicitly managing today. The report also outlines practical strategies to: Identify and segment business behavior within consumer portfolios. Align underwriting and account management with actual usage patterns. Capture targeted growth while protecting long‑term portfolio performance. Ready to dive deeper? Download the full 2026 State of Credit Cards Report to uncover insights that can help your organization manage risk more precisely and grow with confidence. Download report

Credit marketing is entering a new era of precision. Data privacy, personalization and digital-first expectations are rewriting the playbook for financial services marketers. The winners in 2026 won’t just optimize; they’ll orchestrate, using connected intelligence — the linking of data, AI models and insights across platforms — to find, know and grow the right customers. Our latest checklist breaks down what it takes to compete in this new environment, including how to: Master the new prospecting formula Use data to drive personalization at scale Create cohesive, compliant messaging across channels Whether your focus is to expand your portfolio, deepen existing relationships or improve marketing efficiency, this checklist can help you drive stronger, smarter growth all year round. And if you're interested in diving deeper, register for our upcoming webinar on January 15, 2026 to hear directly from Experian experts. Access checklist Register for webinar

E-commerce is booming. Global online sales continue to rise with forecasts predicting growth to $7.89 trillion by 2028. Unfortunately, with any lucrative market comes fraudulent activity. As e-commerce grows by leaps and bounds, so do fraud incidents. E-commerce fraud is defined as any illegal or deceptive activity conducted during an online transaction with the intent to steal money, goods or sensitive information. As digital shopping flourishes, the tactics criminals use to exploit vulnerabilities in payment systems, customer accounts and merchant operations is rapidly expanding. According to Experian’s tenth annual Identity & Fraud Report, nearly 60% of U.S. businesses reported higher fraud losses in 2025, driven by more sophisticated attacks and legacy security gaps. The same report highlighted the damage from e-commerce fraud goes beyond the loss of revenue, directly impacting consumer trust. The survey found that only 13% of consumers feel fully secure opening new accounts. Chief amongst their concerns, 68% of consumer worry about identity theft, while 61% are fearful of stolen credit card data. The constant threat of e-commerce fraud has placed tremendous pressure on merchants and retailers to take robust steps in mitigating these attacks. In addition to protecting the bottom line, such measures are essential to earning consumer trust. According to Experian’s merchant-focused edition of our Identity & Fraud Report, consumers consistently perceive physical and behavioral biometrics tools as the most secure authentication methods — yet merchants are slow to adopt them. This gap highlights a key opportunity for businesses to strengthen security practices and build trust without adding friction to the user experience. After all, 74% of consumers say security is the most important factor when deciding to engage with a business.3 E-commerce fraud comes in many shapes and sizes E-commerce fraud is an umbrella term for a variety of attacks that target merchants and retailers. Amongst these is chargeback fraud, which occurs when a customer makes a legitimate purchase and then falsely disputes the charge with their credit card issuer, claiming the item never arrived or the transaction was unauthorized. The merchant loses both the product and the payment. Another is account takeover fraud, which happens when cybercriminals gain access to a customer’s online account, often through stolen login credentials, and use it to make unauthorized purchases, change shipping details or withdraw loyalty points. In card-not-present (CNP) fraud, attackers use stolen credit card information to make purchases online or by phone, where the physical card isn’t required. Because identity verification is limited, merchants bear the financial losses. This type of fraud includes BIN attacks, targeting the Bank Identification Number (BIN) on a credit or debit card that identifies the issuing financial institution. The goal of a BIN attack is to discover valid card numbers that can be used for fraudulent transactions. There are also refund fraud attacks, which involve scammers exploiting return or refund policies — such as claiming an item didn’t arrive or sending back a different or counterfeit product for reimbursement. Together, different forms of e-commerce fraud cost businesses billions annually, demanding strong fraud detection, authentication and monitoring systems to combat them. E-commerce fraud prevention should be a priority for every merchant and retailer. E-commerce fraud prevention: Ways merchants can fight back Merchants report the highest rates of new account fraud, yet it ranks just 15th among their active investments for 2025. While fraudsters continue to find new and innovative ways to attack, merchants and retailers can better prepare by following industry best practices in e-commerce fraud prevention: Chargeback fraud: When it comes to preventing and managing chargeback fraud, merchants should ensure customers are fully aware of return and refund policies. Utilize Address Verification Services (AVS) and Card Verification Value (CVV2) verification for online and over-the-phone transactions to establish the validity of a purchase. Keeping meticulous records of all transactions can serve as compelling evidence to defend the transaction. Leverage advanced fraud detection tools, such as tokenization and machine learning and AI fraud detection solutions that flag potentially fraudulent transactions and detect suspicious spending patterns and anomalies. Account takeover fraud: Merchants can minimize the risk of account takeover fraud using holistic, risk-based identity and device authentication, as well as behavioral analytics or targeted, knowledge-based authentication. End-to-end fraud management solutions can help reduce manual processes and remove the risk of information silos. Card-not-present fraud: Mitigating the risk of CNP fraud can be accomplished by implementing additional security measures at the time of transaction. These can include requiring verification information, such as a CVV code or a billing zip code to further authenticate the card holder’s identity. Advanced e-commerce fraud prevention tools To stay ahead of the fraudsters, merchants and retailers should take a multilayered approach to e-commerce fraud prevention that takes advantage of the latest, most advanced tools. At Experian®, we offer innovative fraud management solutions that provide the right level of security without causing customer friction. Three advanced e-commerce fraud prevention tools that every merchant should have in their arsenal include: Experian LinkTM: This tool enhances credit card authentication by linking the payment instrument with the digital identity presented for payment. Experian Link enables merchants to quickly and accurately identify legitimate customers to reduce friction and increase acceptance rates, reduce operation costs by preventing fraudulent credit card use, make better risk decisions to protect legitimate customers, limit false declines and identify potential fraudsters. Behavioral analytics: With the growth of AI, fraudsters can now replicate static data, but mimicking human behavior remains challenging. Behavioral analytics detects subtle interaction patterns that are extremely difficult for GenAI-driven fraudsters, including fraud rings and next-generation fraud bots, to replicate. Powered by NeuroID, our behavioral analytics capabilities help organizations proactively mitigate fraud, reduce false positives and streamline risk detection, ultimately creating a secure and frictionless experience for trustworthy users — while locking out fraudsters earlier. Precise ID®: This advanced tool enables businesses to pursue growth confidently by providing robust, real-time identity verification, as well as the ability to accurately identify a wide range of fraud risks including identity theft, synthetic identity and first-party fraud, along with tools that facilitate confirmation when risks are detected. The threat of fraud never stops Merchants and retailers are under a constant and unrelenting threat of attacks by fraudsters. Vigilance is required to protect the customer experience and the bottom line. Fortunately, innovative tools are leveling the playing field, offering much needed e-commerce fraud protection. To learn how Experian can help you combat fraud and meet consumers’ demands for trust and privacy, explore our best-in-class fraud management solutions and download our latest report on closing the trust gap in e-commerce. Explore our solutions Download report

In today’s fast-moving financial services landscape, fintechs face a dual challenge: scaling profitably while managing increasingly complex risk. From credit underwriting to fraud prevention, every decision carries both opportunity and exposure. That’s why forward-looking fintech leaders are turning to data-driven credit risk management strategies to sharpen decision-making, enhance compliance and unlock growth. Why data-driven risk management matters in fintech Fintechs are navigating an environment shaped by rapid innovation, shifting regulations and evolving consumer expectations. Within this landscape, three challenges come to the forefront: Evolving fraud threats: Fraudsters are advancing quickly, exploiting digital onboarding and consumer data. Siloed functions: Traditionally, credit, fraud and compliance were separate, but as fraud detection becomes a higher priority, forward-looking companies are now integrating these functions, with84% planning to share more data across the industry to help prevent fraud.1 Operational complexity: Fintechs must balance growth with compliance, often with lean teams, tech-debt that demands a strong return on investment (ROI)and aggressive timelines. These challenges make it clear that static, one-dimensional risk measures are no longer sufficient. By leveraging a unified decisioning platform that incorporates behavioral data and advanced analytics, fintechs can gain a more holistic view of consumer financial behavior. This broader perspective not only improves the accuracy of credit assessments but also strengthens defenses against sophisticated fraud threats. Driving efficiency through automation A data-driven risk management strategy is only as effective as its ability to be executed at scale. This is why automation is no longer a nice-to-have, but a competitive necessity in an industry defined by speed, complexity and rising consumer expectations. By embedding automation into credit and fraud risk management processes, fintechs can create systems that are more efficient, resilient and compliant. Key advantages include: Increased underwriting efficiency: Combined with data-driven insights, automated decisioning platforms allow fintechs to evaluate applications quickly and more accurately, resulting in faster and fairer credit decisions. Portfolio growth: Leveraging expanded data and automation allow enables smarter customer segmentation and more precise risk-based pricing, driving broader market reach and greater profitability. Fraud mitigation: Automated identity verification helps fintechs quickly validate customers, reduce friction in the onboarding process and block fraudulent activity before it impacts portfolios. Regulatory readiness: Unified, automated risk processes enable fintechs to adapt quickly to regulatory shifts, fraud trends and market disruptions, building long-term sustainability. Comparing legacy and modern credit risk approaches in fintech Data and automation have become essential for executing risk strategies at scale, highlighting just how far credit risk management has evolved. Below are key differences between traditional and modern approaches to credit risk. FeatureLegacy approachData-driven approachRisk detectionPoint-in-time scoresTrajectory-based modelingFraud preventionManual reviewAutomated, behavioral analyticsComplianceSiloed functionsUnified decisioning platformCustomer experienceSlow, manualFast, fair, automated Why fintechs choose Experian® As fintechs navigate an environment of increasing regulation, fraud sophistication and consumer expectations, the winners will be those who embrace a data-driven, automated and converged approach to credit and fraud risk management. Experian offers fintechs a partner with unmatched data accuracy, robust alternative data capabilities and end-to-end decisioning solutions designed for today’s converged risk landscape, including: Trended 3DTMattributes capture 24 months of key consumer credit activity, enabling fintechs to better manage portfolio risk and determine next best actions. Cashflow Score leverages consumer-permissioned banking transaction data to predict the likelihood of a borrower going 60+ days past due in the next 12 months, providing deeper visibility into financial health and repayment capacity. Experian Decisioning is a unified, automated decision engine that incorporates data, strategy design, decision automation and detailed monitoring and reporting to help fintechs streamline credit decisions with speed and consistency. Our behavioral analytics capabilities, powered by NeuroID, provide a seamless, invisible gauge of user risk, allowing fintechs to proactively mitigate fraud while creating a secure, low-friction customer experience. Frequently asked questions What is data-driven risk management in fintech? It’s the application of advanced analytics, behavioral data and automation to help fintechs improve credit risk assessment, fraud prevention and compliance in digital-first environments. How does automation help fintechs manage credit risk? Automation enables fintechs to scale efficiently by streamlining underwriting, minimizing manual errors and ensuring consistent decision-making. What are the benefits of unified decisioning platforms? Unified platforms integrate credit, fraud and compliance decisions into a single workflow, helping fintechs onboard customers faster, respond quickly to fraud threats and maintain compliance without slowing down innovation. Discover how our fintech solutions can help your fintech strengthen credit risk management, reduce fraud and accelerate growth. Learn more 1Experian Vision

In today’s digital payments landscape, fraudsters are constantly developing new tactics to exploit vulnerabilities. One of the most common credit card schemes financial institutions and merchants face are BIN attacks. But what exactly is a BIN attack, and how does BIN attack fraud work? What is a BIN attack? BIN attacks, a type of card not present fraud, target the Bank Identification Number (BIN) — the first six to eight digits of a credit or debit card number that identify the issuing financial institution. Fraudsters use these digits to systematically generate and test potential card number combinations. The goal of a BIN attack is to discover valid card numbers that can be used for fraudulent transactions. Because BINs are publicly available and consistent across card issuers, they provide a predictable framework for attackers. How does it differ from other types of payment fraud? Payment fraud takes many forms, but BIN attacks stand apart because of their scale and automation. Card testing fraud vs. BIN attacks: Both involve criminals running authorization attempts to identify valid card details. However, card testing typically uses data from a single stolen card, while BIN attacks systematically generate thousands of possible card numbers from a known BIN range. Account takeover fraud vs. BIN attacks: In an account takeover, fraudsters gain access to a customer’s existing account, often through phishing or stolen login credentials. BIN attacks don’t require account access — instead, they exploit card number patterns to guess valid accounts. What are the consequences of a BIN attack? BIN attacks don’t just result in stolen card numbers — they create wide-ranging business risks that can impact operations, revenue and customer trust. For financial institutions and merchants, the ripple effects can be significant: High transaction volumes: BIN attacks are carried out using automated scripts or bots that fire off thousands of transaction attempts per minute. This traffic can overwhelm payment systems, slow down processing and disrupt the checkout experience for legitimate customers. Increased chargebacks: Once fraudsters identify valid cards, they make unauthorized purchases that often result in chargebacks. Both merchants and issuers absorb these losses — merchants lose revenue, while issuers reimburse cardholders. Network and processing costs: Every transaction attempt — even those declined during a BIN attack — still incurs network and processing fees. Merchants and issuers can end up paying for thousands of authorization requests, draining resources. Reputational damage: Today’s consumers expect seamless and secure payments. If they experience frequent declines, blocked cards or fraudulent activity, their trust in the institution or merchant erodes. How to protect against BIN attack fraud Mitigating BIN attacks requires a proactive, layered defense strategy. Financial institutions and merchants should consider: Advanced fraud detection and analytics: BIN attacks generate massive volumes of fraudulent traffic. By leveraging AI-driven analytics and machine learning, institutions and merchants can monitor for unusual transaction patterns, velocity spikes and bot-driven activity. Identity and device intelligence: Fraudsters often hide behind bots, stolen IP addresses and compromised devices. With identity verification and device intelligence solutions, merchants and institutions can better determine whether a transaction is coming from a legitimate customer or a fraudster testing card details. Multi-factor authentication (MFA): BIN attacks succeed on speed and automation, firing off thousands of transactions. MFA can help disrupt this process by requiring additional proof of identity from the customer, such as facial recognition or one-time passcodes. Credit card authentication: BIN attacks exploit the gap between payment credentials and the identity of the person using them. A solution like Experian LinkTM seamlessly connects the payment instrument with the digital identity presented for payment, helping merchants to reduce false declines, fraud and operating expenses. Build a stronger defense against BIN attacks BIN attacks are a growing threat in today’s digital payments ecosystem. But with the right safeguards in place, organizations can stay ahead. Learn how Experian can help you strengthen your fraud defenses to reduce losses and protect customer trust. Learn more

In today’s evolving economic climate, lenders face a growing challenge: how to accurately assess creditworthiness — especially for consumers with limited credit histories. That’s where cash flow insights come into play. Our latest infographic illustrates how cashflow data helps lenders achieve a more comprehensive understanding of borrowers' financial health. What you'll learn: Why cashflow data is essential for modern, inclusive lending The key financial behaviors that cash flow insights can uncover How these insights help lenders expand market reach and make more precise decisions Read the infographic to learn more. View infographic

Customer retention is crucial for lenders to maximize lifetime value, especially during economic uncertainty. Increasing customer retention rates by just 5% can boost profits by 25% to 95%. However, many lenders struggle with loyalty, as seen in Q2 2024 when mortgage servicers’ retention rates for refinances dropped to 20%, the second lowest in 17 years. Nonbanks and banks also saw significant declines. This is due to increased competition, changing economic conditions, and a lack of personalization. Key strategies for improving customer retention Lenders can improve retention by leveraging data for personalization, maintaining consistent communication, offering loyalty rewards, and utilizing retention triggers. Leverage data for personalization. Use customer data to offer tailored products and refinancing options based on financial behaviors. Using credit attributes, trended data and alternative credit data (alternative financial services data, cashflow attributes, etc.) can help provide deeper insights of your customers. Maintain consistent communication. Keep customers informed with regular updates about interest rate changes or new loan products. Use a variety of communication channels, including email and in-app messaging, to ensure customers are kept in the loop. Ensure your customer service team is always available and responsive, offering clear answers to any financial concerns. Offer loyalty rewards. Develop programs that reward repeat business and referrals. Offer special rates or discounts for returning customers or for those who refer friends and family to your services. Increase customer lifetime value (LTV) by offering additional services like financial planning or credit score monitoring. Utilize retention triggers. Identify key events for engagement with automated retention triggers. For example, a borrower who has a mortgage with a fixed rate may be less likely to consider refinancing unless prompted. Experian’s Retention TriggersSM can notify lenders when refinancing might be beneficial to their customer, offering them personalized incentives or new product options at the right time. Why Experian’s Retention Triggers? By integrating Experian’s Retention Triggers, lenders can keep borrowers engaged, increase retention, and boost profitability even in tough economic times. Advanced data insights: Gain deeper insights into your customers’ behavior to identify those at risk of leaving and take proactive action. Personalized engagement: Automate personalized communications based on customer behaviors, ensuring timely engagement. Increased revenue: By offering personalized, timely and relevant offers, you can increase the likelihood of retaining your customers and growing your revenue. Make customer retention a priority In today’s challenging economic climate, lenders who focus on personalized experiences, consistent communication, and relevant offers will stand out and retain borrowers. Leverage tools like Experian’s Retention Triggers to proactively engage customers, reduce churn, and foster long-term relationships for increased profitability and success. Learn more

Consumers are experiencing the highest loan rejection rates in a decade, driven by strict lending standards.1 While crucial for mitigating risk, these measures can also limit growth opportunities for financial institutions. Our latest one pager explores how cash flow data, obtained from consumer-permissioned transaction data, empowers lenders with unique insights into consumers’ financial health, enabling them to expand their portfolios while managing risk effectively. Read the full one pager to learn how cashflow data can help you make smarter, more confident lending decisions. Access one pager 12024 Q4 Lending Conditions Chartbook, Experian.

As consumer credit behaviors change, staying informed is crucial for credit unions. Experian’s new State of Credit Unions Report offers a comprehensive analysis of consumer credit trends from January 2022 to October 2024, with a particular focus on auto loans, unsecured personal loans and unsecured credit cards. The report covers: Trends in originations and delinquencies among credit union members How credit unions fare against other fintech lenders and regional banks Strategies to attract new members and mitigate portfolio risk Discover key insights into the consumer credit landscape and how credit unions stack up against other financial institutions. Download the report

With cybersecurity threats on the rise, organizations are turning to token-based authentication as a secure and efficient solution to safeguard sensitive data and systems. Data breaches impacted 1.1 billion individuals in 2024, a staggering 490% increase from the previous year.1 Token-based authentication is a method of verifying a user's identity through digital tokens rather than traditional means such as passwords. These tokens are temporary and serve as access keys, allowing users to securely interact with systems, applications, and networks. The goal of token authentication is to strengthen security while improving the user experience. Instead of relying solely on static credentials (like passwords), which can be intercepted or stolen, leveraging a type of multi-factor authentication like tokens adds an additional layer of security by functioning as dynamic access credentials. How token-based authentication works Token authentication unfolds through a series of steps to ensure robust security. Here's a simplified breakdown of how it works in practice: User request and authentication: When a user attempts to log in, they provide their credentials (e.g., username and password). These credentials are verified by the authentication server. Token generation: After verifying the user's credentials, the server generates a token — a cryptographically secured string often containing information like the user's ID and permissions. Token sent to the user: The generated token is sent back to the user or their device to confirm authentication. Token usage for access: Now authenticated, the user uses the token to access the system or application. The token is passed along with each request to ensure the user is authorized to proceed. Token validation: Each time a token is presented to the server, its integrity and expiration are verified. If the token is valid, access is granted; if not, the session is terminated. Token expiration and renewal: Tokens are typically temporary and expire after a set period. Users must either re-authenticate or renew the token for continued access. This limits the time window during which a stolen token can be misused. Types of token authentication methods Token authentication comes in different forms to meet various use case requirements. Common types include: JSON Web Tokens (JWT) Lightweight, self-contained, and easily transferred between clients and servers, JWT is one of the most widely used token formats. It includes claims, which are bits of information about a user encoded within the token, such as roles and permissions. Example: A financial application uses JWTs to ensure only registered users can access private account data. OAuth tokens OAuth is an industry-standard authorization protocol that uses tokens to grant limited access to applications without revealing the user's credentials. It’s often used for third-party service integration. Example: When you log into an e-commerce platform using your Google credentials, OAuth tokens authorize access. Session tokens These are temporary tokens stored on the server to track authenticated sessions, commonly used in web applications to ensure secure browsing. Example: Online banking platforms rely on session tokens for secure user sessions. Refresh tokens Refresh tokens are designed to renew access tokens without requiring the user to log in repeatedly. They extend session durations while maintaining a high-security standard. Example: A subscription service app uses refresh tokens to maintain a seamless user experience without frequent logouts. Benefits of token-based authentication Token-based authentication offers several advantages that make it a preferred security measure for organizations of all sizes. Enhanced security: Tokens reduce the risk of breaches as they are temporary and encrypted. They’re also specific to sessions, applications, or devices, meaning unauthorized users cannot reuse stolen tokens effectively. Elimination of password reliance: Tokens reduce dependence on static passwords, which are often reused and susceptible to brute-force attacks. This bolsters an organization’s overall cybersecurity posture. Improved user experience: Token authentication allows for more seamless interactions by minimizing the need for repeated logins. With features like single sign-on (SSO), users enjoy convenient access to multiple platforms with a single token. Scalability: Tokens are flexible and can adapt to varied business use cases, making them ideal for organizations of all scales. For instance, application programming interfaces (APIs) and microservices can communicate securely via token exchanges. Supports compliance: Token-based authentication helps organizations meet regulatory compliance requirements by offering robust access control and audit trails. This is critical for industries like finance, healthcare, and e-commerce. Cost efficiency: While implementing token-based authentication may require an initial investment, it reduces long-term risks and costs associated with data breaches, system downtime, and customer trust. How Experian can help strengthen your authentication process At Experian, we recognize that strong security measures should never compromise the user experience. That's why we offer cutting-edge identity solutions tailored to meet the needs of organizations. Our tools allow you to integrate token-based authentication seamlessly into your systems while ensuring compliance with security best practices and industry regulations. Are you ready to take your business's security and user experience to the next level? Visit us online today. Learn more 12024-2025 Data Breach Response Guide, Experian, 2024. This article includes content created by an AI language model and is intended to provide general information.

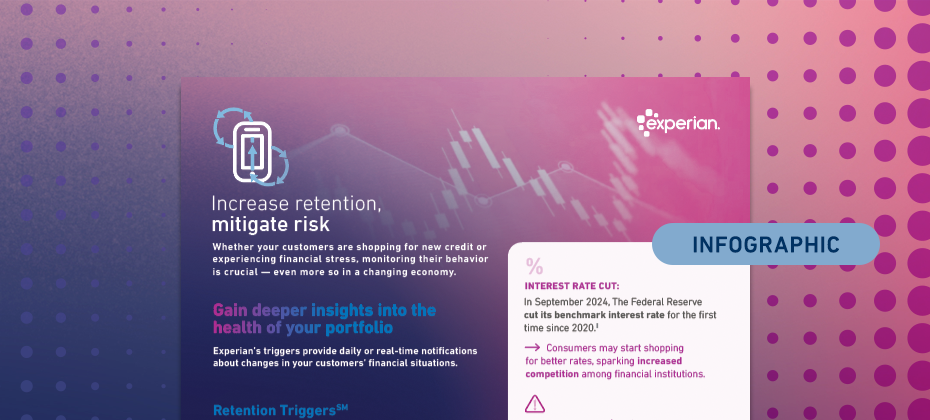

Whether consumers are shopping for new credit or experiencing financial stress, monitoring their behavior is crucial — even more so in an ever-changing economy. Our latest infographic explores economic trends impacting consumers’ financial behaviors and how Experian’s Risk and Retention TriggersSM enable lenders to detect early signs of risk or churn. Key highlights include: Credit card balances climbed to $1.17 trillion in Q3 2024. As prices of goods and services remain elevated, consumers may continue to experience financial stress, potentially leading to higher delinquency rates. Increasing customer retention rates by 5% can boost profits by 25% to 95%. View the infographic to learn how Risk and Retention Triggers can help you advance your portfolio management strategy. Access infographic

The credit card market is rapidly evolving, driven by technological advancements, economic volatility, and changing consumer behaviors. Our new 2025 State of Credit Card Report provides an in-depth analysis of the credit card landscape and strategy considerations for financial institutions. Findings include: Credit card debt reached an all-time high of $1.17 trillion in Q3 2024. About 19 million U.S. households were considered underbanked in 2023. Bot-led fraud attacks doubled from January to June 2024. Read the full report for critical insights and strategies to navigate a shifting market. Access report

Today’s fast-paced, digital-first hiring environment calls for a more comprehensive approach to pre-employment screening. With growing pressure on employers and HR teams to make swift, accurate, and secure hiring decisions, having access to the tools and data to enhance efficiency and security is more important than ever. By evolving beyond traditional screening methods, background screeners can better meet these needs and deliver added value to their clients. Fraud remains a significant challenge. In fact, fraud scams resulted in a staggering $485.6 billion in losses in 20231 — and hiring teams aren’t exempt from these risks. Fraudulent resumes, synthetic identities, and the risk of non-compliance with evolving regulations create a challenging landscape for pre-employment verifications. What if there was a way to make smarter, faster, and more secure hiring decisions? This article explores how background screeners can optimize pre-employment verification processes, reduce fraud risks, and ensure compliance — all while delivering a positive candidate experience. What is pre-employment screening? Employers conduct pre-employment screenings to thoroughly evaluate job candidates and make informed hiring decisions. It’s designed to verify key details about candidates, such as their identity, employment history, and references among others to assess their suitability for a role and ensure compliance with industry regulations. Enhancing traditional screening processes For decades, pre-employment background checks have been a cornerstone of the hiring process. While effective, many traditional methods face challenges in keeping up with the evolving demands of modern hiring. Delays in hiring: Background checks can oftentimes rely on manual processes, which could extend timelines leading to delays of days or even weeks. This not only slows down hiring cycles but can make it harder for employers to compete for top talent in a tight labor market. Errors and inaccuracies: Human errors, incomplete data, and inconsistencies across systems can lead to missed insights or red flags. Fraudulent activity: As hiring becomes increasingly digital, identity theft and synthetic identities present growing challenges to verifying candidate-provided data. Regulatory challenges: With regulations like the Equal Employment Opportunity Commission (EEOC) and Fair Credit Reporting Act (FCRA), companies must navigate complex compliance requirements to avoid legal and financial repercussions. 1 in 3 HR professionals report losing top candidates due to slow pre-employment screening processes.2 These challenges highlight the opportunity to build on existing screening practices with tools that enhance speed, provide actionable insights and prevent fraud. Adapting to the evolving fraud landscape Employment fraud is becoming increasingly sophisticated, fueled by trends like the rise of remote work and digital applications. In fact, the employment sector accounted for 45% of all false document submissions in 2023, making it the most targeted industry for fraud.3 From fake references and degrees to synthetic identities created using stolen personal information, the risks are higher than ever. Synthetic identity fraud: This form of fraud — where fake identities are created by combining real and fabricated data — makes up more than 80% of all new account fraud.4 Fake credentials: Many candidates falsify qualifications or work histories to enhance their chances of securing a role. Compliance risks: Failure to verify candidate information accurately can result in legal penalties, brand reputation damage, or internal security breaches. Modernizing pre-employment screening The good news? Experian offers advanced solutions that complement existing screening processes, empowering background screeners to deliver more efficient, secure and reliable results for their clients looking to higher faster, and with greater confidence. Gain a more holistic view of a candidate’s risk profile: Experian’s nationwide database contains files on more than 245 million credit-active consumers, providing the most current, accurate, and comprehensive information available in the industry. Conduct real-time identity verification: Leverage a range of identity verification solutions to authenticate and verify a candidate’s identity by accessing a breadth set of non-credit and credit data sources to create a robust social footprint that defines each consumer as unique individuals. Integrate advanced fraud detection: Powered by purpose-built analytics and machine learning algorithms, Experian’s fraud detection tools can detect synthetic identities, inconsistencies, and other red flags while ensuring a seamless candidate experience. Enhance compliance efforts: Experian’s solutions are designed to help businesses navigate complex compliance requirements with ease. Fraud prevention playbook in preemployment Uncover essential strategies for fraud prevention and identity verification in employment screening. Download now The pre-employment screening landscape is evolving, and staying ahead requires tools that enhance the efficiency and effectiveness of your processes. Experian’s advanced solutions are designed to complement your existing screening services, helping you reduce fraud risks, maintain compliant, and deliver data-driven insights that empower smarter hiring decisions. Get started today Ready to transform your pre-employment verification process with fraud mitigation and identity verification solutions? Explore our innovative solutions today. Learn more 1 Nasdaq finds scams led to $486 billion in losses in 2023, 2024. 2 Research reveals Candidates’ Frustrations with Hiring Process, 2024. 3 Employment Identity Fraud: Do You Know Who You’re Hiring, 2024. 4 Report: Synthetic identity fraud is growing, 2024.

The digital domain is rife with opportunities, but it also brings substantial risks, especially for organizations. Among the innovative tools that have risen to prominence for fraud detection and online security is browser fingerprinting. Whether you're looking to minimize security gaps or bolster your fraud prevention strategy, understanding how this technology works can provide a significant advantage in today’s ever-evolving fraud and identity landscape. This article explores the concept, functionality, and applications of browser fingerprinting while also examining its benefits and relevance for organizations. How does browser fingerprinting work? Browser fingerprinting is a powerful technology designed to collect unique identifying information about a user’s web browser and device. By compiling data points such as browser type, operating system, time zone, and installed plugins, browser fingerprinting creates a distinct profile — or "fingerprint"— that allows websites to recognize returning users without relying on cookies. Here’s a breakdown of its key steps: Data collection: When a user visits a website, their browser sends information, such as user-agent strings or metadata, to the website's servers. This data provides insights about their browser, device, and system. Fingerprint creation: The collected information is processed to generate a unique ID or fingerprint, representing the user's specific configuration. Tracking and analyzing: These fingerprints enable websites to track and analyze user behavior, detect anomalies, and identify users without relying on traditional tracking mechanisms like cookies. For organizations, employing technology that leverages such fingerprints adds an additional layer to identity verification, detecting discrepancies that may indicate fraud attempts. What are the different techniques? Not all browser fingerprinting methods are identical; varying approaches offer different strengths. The most common techniques used today include: Canvas fingerprinting: This method utilizes the "Canvas" element in HTML5. When a website sends a command to draw a hidden image on a user's device, the way the image is rendered reveals unique characteristics about the device's graphics hardware and software. Font fingerprinting: Font fingerprinting involves analyzing the fonts installed on a user's system. Since computers and browsers render text in slightly different ways based on their configurations, the resulting variations aid in identifying users. Plugin enumeration: Browsers and devices often come equipped with plugins or extensions like Flash or Java. Analyzing which plugins are installed, their versions, and their order helps websites build unique fingerprints. What are the benefits of browser fingerprinting? For organizations, browser fingerprinting is not just a technical marvel — it’s a strategic asset. Benefits include: Enhanced fraud detection: Browser fingerprinting detects inconsistencies within user accounts, flagging unauthorized logins, synthetic identity fraud, or account takeover fraud without introducing significant friction for legitimate users. By identifying patterns that deviate from the norm, organizations can better prepare for malicious activities. Learn more about addressing account takeover fraud. Supports multi-layered security: A single security measure often isn't enough to combat advanced fraudulent schemes. Browser fingerprinting pairs seamlessly with other fraud management tools, such as behavioral analytics and risk-based authentication, to provide robust security. See how behavioral analytics can help organizations spot and stop next-generation fraud bots. Seamless user experience: Unlike cookies or authentication codes, browser fingerprinting operates passively in the background. Users remain unaware of the process, ensuring their experience is unaffected while still maintaining security. Level up with Experian's fraud prevention tools Browser fingerprinting offers organizations a game-changing tool to secure online interactions. However, given the growing complexity of fraud threats, organizations will need additional layers of insights and protection. Experian offers integrated, AI-driven fraud prevention solutions tailor-made to tackle challenges in the digital space. By leveraging advanced technologies like browser fingerprinting alongside Experian’s solutions, organizations can safeguard their operations and uphold customer trust while maintaining a frictionless user experience. Learn more about our fraud prevention solutions This article includes content created by an AI language model and is intended to provide general information.