Apply CIS Tag

Since 1996, The Internal Revenue Service (IRS) has issued more than 27 million individual taxpayer identification numbers (ITINs) – a 9-digit number used by individuals who are required to file or report taxes in the United States but are not eligible to obtain a Social Security number (SSN). Across the country, ITIN holders are actively contributing to their communities and the U.S. financial system. They pay bills, build businesses, contribute billions in taxes and manage their finances responsibly. Yet despite their clear engagement, many remain underrepresented within traditional lending models. Lenders have a meaningful opportunity to bridge the gap between intention and impact. By rethinking how ITIN consumers are evaluated and supported, financial institutions can: Reduce barriers that have historically held capable borrowers back Build products that reflect real borrower needs Foster trust and strengthen community relationships Drive sustainable, responsible growth Our latest white paper takes a more holistic look at ITIN consumers, highlighting their credit behaviors, performance patterns and long-term growth potential. The findings reveal a population that is not only financially engaged, but also demonstrating signs of ongoing stability and mobility. A few takeaways include: ITIN holders maintain a lower debt-to-income ratio than SSN consumers. ITIN holders exhibit fewer derogatory accounts (180–400 days past due). After 12 months, 76.9% of ITIN holders remained current on trades, a rate 15% higher than SSN consumers. With deeper insight into this segment, lenders can make more informed, inclusive decisions. Read the full white paper to uncover the trends and opportunities shaping the future of ITIN lending. Download white paper

Credit marketing is entering a new era of precision. Data privacy, personalization and digital-first expectations are rewriting the playbook for financial services marketers. The winners in 2026 won’t just optimize; they’ll orchestrate, using connected intelligence — the linking of data, AI models and insights across platforms — to find, know and grow the right customers. Our latest checklist breaks down what it takes to compete in this new environment, including how to: Master the new prospecting formula Use data to drive personalization at scale Create cohesive, compliant messaging across channels Whether your focus is to expand your portfolio, deepen existing relationships or improve marketing efficiency, this checklist can help you drive stronger, smarter growth all year round. And if you're interested in diving deeper, register for our upcoming webinar on January 15, 2026 to hear directly from Experian experts. Access checklist Register for webinar

Three winners were announced at Experian’s inaugural Vision Awards ceremony held on Tuesday, October 7 in front of more than 800 attendees at Experian’s Vision Conference held in Miami, Fla. Figure, PREMIER Bankcard and Members First Credit Union were recognized for their work in artificial intelligence, innovation and financial empowerment. The four-day gathering provided a dynamic forum for exploring the latest innovations shaping the future of data-driven decisioning. “Our Vision Awards celebrate the unique impact financial industry leaders can have when data, technology and purpose align,” said Jeff Softley, CEO, Experian North America. “We are proud to recognize these three organizations with whom we collaborate to drive opportunities and help create change for society as a whole.” The Vision Awards recognize the achievements of organizations that accelerate action. These forward-thinking institutions leverage artificial intelligence, innovation and financial empowerment to drive opportunities and create actionable change for consumers, businesses and society. Recognizing Leaders in AI, Innovation, and Financial Empowerment A panel of interdisciplinary judges reviewed nominations from across industries across the regions, evaluating submissions based on rigor, originality, and impact. The 2025 winners reflect how organizations are leveraging data and technology to advance innovation and inclusion. Excellence in AI: Figure Figure’s submission showcased how it has redefined consumer lending outreach through an AI-driven targeting engine powered by more than 90 machine learning models and 5,000+ behavioral and financial features. By combining Experian’s prescreen data with proprietary insights, Figure delivers highly precise, cost-efficient firm offers of credit — helping it become one of the top three home equity line of credit lenders in the U.S. “This win reflects more than just a successful application of AI. It represents the broader innovative culture deeply embedded in our company’s DNA,” said Ruben Padron, Chief Data Officer at Figure. “Our work with Experian has been instrumental in helping us assess creditworthiness and predict borrower intent with greater precision.” Excellence in Innovation: PREMIER Bankcard PREMIER Bankcard continues to demonstrate how financial inclusion and innovation go hand in hand. From modernizing its technology to reimagining its product suite, PREMIER has made bold strides to serve the underserved and democratize access to credit. “This award affirms our belief that financial inclusion and innovation must go hand in hand,” said Chris Thornton, Senior Vice President of Credit at PREMIER Bankcard. “We’re committed to reaching those who need it most, and Experian has proven to be an exceptional partner in that mission.” With more than 30 million customers served, PREMIER has become a leader in first-time and second-chance credit, while also giving back more than $4 billion to charitable causes through its partnership with First PREMIER Bank and founder Denny Sanford. “We’re here to change lives,” Thornton added. “That’s how we measure success — and that’s ultimately what we’re investing in.” Excellence in Financial Empowerment: Members First Credit Union Members First Credit Union was honored for its commitment to inclusive lending and community development across Michigan. In 2024 alone, the credit union’s programs helped thousands of members access fair and affordable credit, supported 166 community organizations, and contributed nearly $230,000 in donations — backed by 2,000 volunteer hours from its employees. “Our impact demonstrates how mission-driven financial institutions can meaningfully expand access, strengthen communities, and foster long-term financial health,” said Carrie Iafrate, CEO/President at Members First Credit Union. “We’re honored to receive this recognition and inspired to continue helping individuals thrive financially.” Honoring the Judges Behind the Vision The 2025 Vision Awards were evaluated by a distinguished panel of judges representing both Experian and external associations and partners in the financial inclusion community, including: Lisa Cantu-Parks, Vice President of Resource Development, Unidos Jean Carlos Rosario Mercado, Juntos Avanzamos Program Officer, Inclusiv Ian P. Moloney, Senior Vice President, Head of Policy and Regulatory Affairs, American Fintech Council Marc Morial, President and CEO, National Urban League Kevin O’Connor, Senior Vice President, Membership and Sponsorship, Consumer Bankers Association Their expertise ensured that the winners reflect the industry’s highest standards of innovation, integrity, and impact. Ian P. Moloney, Senior Vice President, Head of Policy and Regulatory Affairs, American Fintech Council, and Rhonda Spears Bell, Senior Vice President and Chief Marketing Officer, National Urban League, were at the recognition session at Vision and shared about their organizations and experience serving as a judge. Video messages were also shared from Jean Carlos Rosario Mercado of Inclusiv and Kevin O’Connor of Consumer Bankers Association, who were unable to attend the live event. “I greatly appreciated the opportunity to participate as a judge in the Experian Vision Awards because it provided me a chance to look beyond my usual day-to-day, and understand the myriad of innovations and projects going on to help consumers and the industry,” Moloney said. “The award winners tonight showcase the best of our industry, and I appreciate the opportunity to take part in highlighting their success.” “I’m inspired by the outstanding organizations we’re celebrating tonight - each making a lasting impact in our country and globally,” Spears Bell said. “I want to take a moment to recognize Experian - not only as a valued corporate partner, but as a true ally in our mission to advance financial literacy, stability, and generational wealth.” Looking Ahead: Vision Awards 2026 Experian will continue to champion progress in financial services and across all industries, and the Vision Awards offers one of the avenues through which the industry can recognize organizations driving change through responsible innovation. Submissions for the 2026 Vision Awards open on June 1, 2026. To learn more about this year’s winners and how to apply for next year’s program, visit the Vision Awards page.

Day 1 of Vision 2025 is in the books – and what a start. From bold keynotes to breakout sessions and networking under the Miami sun, the energy and inspiration were undeniable. A wave of change: Jeff Softley opens Vision 2025 The day kicked off with a powerful keynote from Jeff Softley, Experian North America CEO, who issued a call to action for the industry: to not just adapt to change, but to lead it. “It isn’t a ripple – it’s a tidal wave of technology,” Jeff said. “Together we ride this wave with confidence.” His keynote set the tone for a day centered on innovation and the future of financial services – where technology, insight and trust converge to create lasting impact. Jeff continues this conversation in the latest Experian Exchange episode, where he explores three forces shaping the industry: the rise of AI, the demand for personalized digital experiences and the mission to expand credit access for all. Turning vision into action: Alex Lintner on agentic AI Building on Jeff’s message, Alex Lintner, CEO of Experian Software and Technology, took the stage to show how Experian is turning innovation into measurable results. His keynote explored how agentic and advanced AI capabilities are redefining financial services ROI and powering the next generation of the Ascend Platform™. For a deeper look into how Experian is reshaping the economics of credit and fraud decisioning, read the latest American Banker feature. Unfiltered insights from “Mr. Wonderful” The day’s highlight came from Kevin O’Leary, investor, entrepreneur and the always-candid “Mr. Wonderful.” With his trademark wit and honesty, Kevin shared sharp insights on thriving in a disruptive economy, offering candid advice on leadership, risk and opportunity. He even gave attendees a peek behind the Shark Tank curtain, revealing a few surprises and the mindset that drives his bold business decisions. Breakouts that inspired and informed The conference floor buzzed with energy as attendees joined breakout sessions on fraud defense, AI-driven personalization, regulatory trends and consumer insights. Sessions highlighted how Experian’s unified value proposition is fueling double-digit growth, how to future-proof credit risk strategies and how data and innovation are redefining customer engagement across the lifecycle. Hands-on innovation and connection The Innovation Showcase gave attendees an up-close look at Experian’s latest tools and technologies in action. Meanwhile, friendly competition kept the excitement high through the Vision mobile app leaderboard – with every check-in and connection earning points toward the top spot. Networking beyond the conference hall walls As the sun set, Vision 2025 shifted into high gear with unforgettable networking events across Miami – from golf at the Miller Course to art walks, brewery tours and a scenic cruise through Biscayne Bay. An evening to remember The day closed with the first-ever Vision Awards Dinner, celebrating standout leaders who are shaping the future of financial services. Up Next: Day 2 The momentum continues tomorrow as more keynote speakers take the stage. Stay tuned for more insights, innovation, and inspiration from Vision 2025.

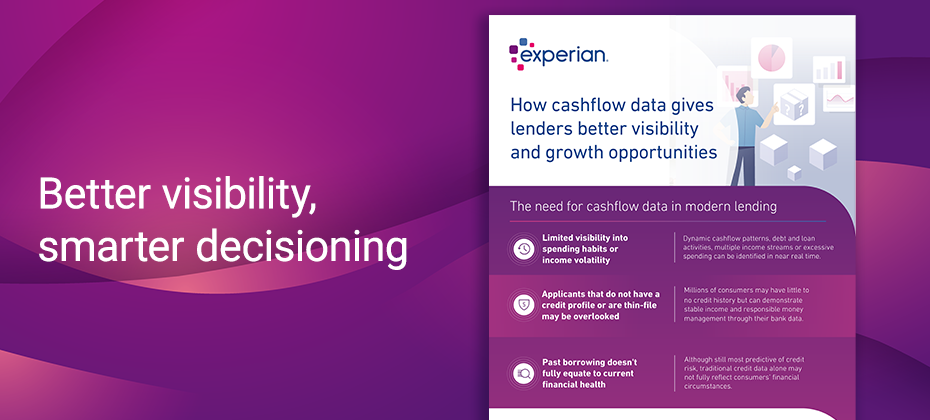

In today’s evolving economic climate, lenders face a growing challenge: how to accurately assess creditworthiness — especially for consumers with limited credit histories. That’s where cash flow insights come into play. Our latest infographic illustrates how cashflow data helps lenders achieve a more comprehensive understanding of borrowers' financial health. What you'll learn: Why cashflow data is essential for modern, inclusive lending The key financial behaviors that cash flow insights can uncover How these insights help lenders expand market reach and make more precise decisions Read the infographic to learn more. View infographic

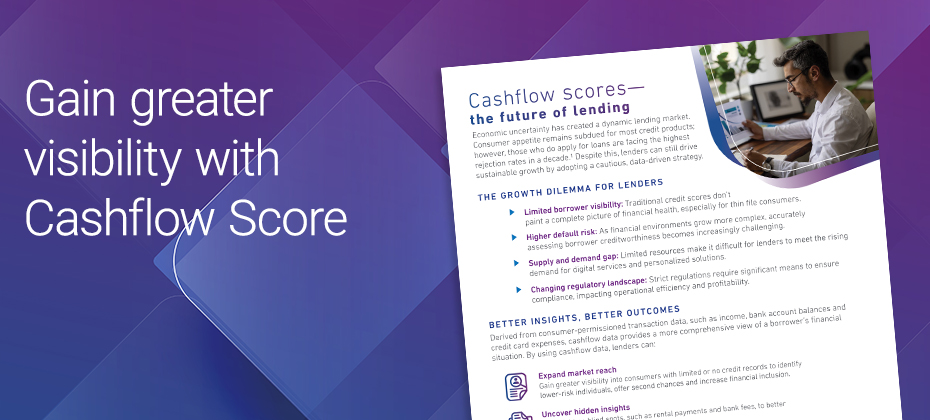

Consumers are experiencing the highest loan rejection rates in a decade, driven by strict lending standards.1 While crucial for mitigating risk, these measures can also limit growth opportunities for financial institutions. Our latest one pager explores how cash flow data, obtained from consumer-permissioned transaction data, empowers lenders with unique insights into consumers’ financial health, enabling them to expand their portfolios while managing risk effectively. Read the full one pager to learn how cashflow data can help you make smarter, more confident lending decisions. Access one pager 12024 Q4 Lending Conditions Chartbook, Experian.

In the latest episode of “The Chrisman Commentary” podcast, Experian experts Joy Mina, Director of Product Commercialization, and David Fay, Solution Consultant, talk about reducing mortgage pipeline fallout and improving loan pull-through rate. Listen to the full episode for all the details and check out the previous episode to explore how lenders can navigate a tight mortgage market, from rates to equity. Listen to podcast

With cybersecurity threats on the rise, organizations are turning to token-based authentication as a secure and efficient solution to safeguard sensitive data and systems. Data breaches impacted 1.1 billion individuals in 2024, a staggering 490% increase from the previous year.1 Token-based authentication is a method of verifying a user's identity through digital tokens rather than traditional means such as passwords. These tokens are temporary and serve as access keys, allowing users to securely interact with systems, applications, and networks. The goal of token authentication is to strengthen security while improving the user experience. Instead of relying solely on static credentials (like passwords), which can be intercepted or stolen, leveraging a type of multi-factor authentication like tokens adds an additional layer of security by functioning as dynamic access credentials. How token-based authentication works Token authentication unfolds through a series of steps to ensure robust security. Here's a simplified breakdown of how it works in practice: User request and authentication: When a user attempts to log in, they provide their credentials (e.g., username and password). These credentials are verified by the authentication server. Token generation: After verifying the user's credentials, the server generates a token — a cryptographically secured string often containing information like the user's ID and permissions. Token sent to the user: The generated token is sent back to the user or their device to confirm authentication. Token usage for access: Now authenticated, the user uses the token to access the system or application. The token is passed along with each request to ensure the user is authorized to proceed. Token validation: Each time a token is presented to the server, its integrity and expiration are verified. If the token is valid, access is granted; if not, the session is terminated. Token expiration and renewal: Tokens are typically temporary and expire after a set period. Users must either re-authenticate or renew the token for continued access. This limits the time window during which a stolen token can be misused. Types of token authentication methods Token authentication comes in different forms to meet various use case requirements. Common types include: JSON Web Tokens (JWT) Lightweight, self-contained, and easily transferred between clients and servers, JWT is one of the most widely used token formats. It includes claims, which are bits of information about a user encoded within the token, such as roles and permissions. Example: A financial application uses JWTs to ensure only registered users can access private account data. OAuth tokens OAuth is an industry-standard authorization protocol that uses tokens to grant limited access to applications without revealing the user's credentials. It’s often used for third-party service integration. Example: When you log into an e-commerce platform using your Google credentials, OAuth tokens authorize access. Session tokens These are temporary tokens stored on the server to track authenticated sessions, commonly used in web applications to ensure secure browsing. Example: Online banking platforms rely on session tokens for secure user sessions. Refresh tokens Refresh tokens are designed to renew access tokens without requiring the user to log in repeatedly. They extend session durations while maintaining a high-security standard. Example: A subscription service app uses refresh tokens to maintain a seamless user experience without frequent logouts. Benefits of token-based authentication Token-based authentication offers several advantages that make it a preferred security measure for organizations of all sizes. Enhanced security: Tokens reduce the risk of breaches as they are temporary and encrypted. They’re also specific to sessions, applications, or devices, meaning unauthorized users cannot reuse stolen tokens effectively. Elimination of password reliance: Tokens reduce dependence on static passwords, which are often reused and susceptible to brute-force attacks. This bolsters an organization’s overall cybersecurity posture. Improved user experience: Token authentication allows for more seamless interactions by minimizing the need for repeated logins. With features like single sign-on (SSO), users enjoy convenient access to multiple platforms with a single token. Scalability: Tokens are flexible and can adapt to varied business use cases, making them ideal for organizations of all scales. For instance, application programming interfaces (APIs) and microservices can communicate securely via token exchanges. Supports compliance: Token-based authentication helps organizations meet regulatory compliance requirements by offering robust access control and audit trails. This is critical for industries like finance, healthcare, and e-commerce. Cost efficiency: While implementing token-based authentication may require an initial investment, it reduces long-term risks and costs associated with data breaches, system downtime, and customer trust. How Experian can help strengthen your authentication process At Experian, we recognize that strong security measures should never compromise the user experience. That's why we offer cutting-edge identity solutions tailored to meet the needs of organizations. Our tools allow you to integrate token-based authentication seamlessly into your systems while ensuring compliance with security best practices and industry regulations. Are you ready to take your business's security and user experience to the next level? Visit us online today. Learn more 12024-2025 Data Breach Response Guide, Experian, 2024. This article includes content created by an AI language model and is intended to provide general information.

As Valentine’s Day approaches, hearts will melt, but some will inevitably be broken by romance scams. This season of love creates an opportune moment for scammers to prey on individuals feeling lonely or seeking connection. Financial institutions should take this time to warn customers about the heightened risks and encourage vigilance against fraud. In a tale as heart-wrenching as it is cautionary, a French woman named Anne was conned out of nearly $855,000 in a romance scam that lasted over a year. Believing she was communicating with Hollywood star Brad Pitt; Anne was manipulated by scammers who leveraged AI technology to impersonate the actor convincingly. Personalized messages, fabricated photos, and elaborate lies about financial needs made the scam seem credible. Anne’s story, though extreme, highlights the alarming prevalence and sophistication of romance scams in today’s digital age. According to the Federal Trade Commission (FTC), nearly 70,000 Americans reported romance scams in 2022, with losses totaling $1.3 billion—an average of $4,400 per victim. These scams, which play on victims’ emotions, are becoming increasingly common and devastating, targeting individuals of all ages and backgrounds. Financial institutions have a crucial role in protecting their customers from these schemes. The lifecycle of a romance scam Romance scams follow a consistent pattern: Feigned connection: Scammers create fake profiles on social media or dating platforms using attractive photos and minimal personal details. Building trust: Through lavish compliments, romantic conversations, and fabricated sob stories, scammers forge emotional bonds with their targets. Initial financial request: Once trust is established, the scammer asks for small financial favors, often citing emergencies. Escalation: Requests grow larger, with claims of dire situations such as medical emergencies or legal troubles. Disappearance: After draining the victim’s funds, the scammer vanishes, leaving emotional and financial devastation in their wake. Lloyds Banking Group reports that men made up 52% of romance scam victims in 2023, though women lost more on average (£9,083 vs. £5,145). Individuals aged 55-64 were the most susceptible, while those aged 65-74 faced the largest losses, averaging £13,123 per person. Techniques scammers use Romance scammers are experts in manipulation. Common tactics include: Fabricated sob stories: Claims of illness, injury, or imprisonment. Investment opportunities: Offers to “teach” victims about investing. Military or overseas scenarios: Excuses for avoiding in-person meetings. Gift and delivery scams: Requests for money to cover fake customs fees. How financial institutions can help Banks and financial institutions are on the frontlines of combating romance scams. By leveraging technology and adopting proactive measures, they can intercept fraud before it causes irreparable harm. 1. Customer education and awareness Conduct awareness campaigns to educate clients about common scam tactics. Provide tips on recognizing fake profiles and unsolicited requests. Share real-life stories, like Anne’s, to highlight the risks. 2. Advanced data capture solutions Implement systems that gather and analyze real-time customer data, such as IP addresses, browsing history, and device usage patterns. Use behavioral analytics to detect anomalies in customer actions, such as hesitation or rushed transactions, which may indicate stress or coercion. 3. AI and machine learning Utilize AI-driven tools to analyze vast datasets and identify suspicious patterns. Deploy daily adaptive models to keep up with emerging fraud trends. 4. Real-time fraud interception Establish rules and alerts to flag unusual transactions. Intervene with personalized messages before transfers occur, asking “Do you know and trust this person?” Block transactions if fraud is suspected, ensuring customers’ funds are secure. Collaborating for greater impact Financial institutions cannot combat romance scams alone. Partnerships with social media platforms, AI companies, and law enforcement are essential. Social media companies must shut down fake profiles proactively, while regulatory frameworks should enable banks to share information about at-risk customers. Conclusion Romance scams exploit the most vulnerable aspects of human nature: the desire for love and connection. Stories like Anne’s underscore the emotional and financial toll these scams take on victims. However, with robust technological solutions and proactive measures, financial institutions can play a pivotal role in protecting their customers. By staying ahead of fraud trends and educating clients, banks can ensure that the pursuit of love remains a source of joy, not heartbreak. Learn more

Debt collectors face a multitude of challenges when it comes to contacting the right people at the right time and improving their processes for collections. We interviewed Matt Baltzer, Senior Product Management Director at Experian, to learn more about how his team is helping debt collectors engage their customers and optimize their collection strategies.

In today's evolving financial landscape, debt collection remains a critical function for financial institutions. However, traditional methods often fall short in efficiency and customer satisfaction. Enter artificial intelligence (AI), a game-changer poised to revolutionize the debt collection industry. This blog post explores the benefits and uses of AI in debt collection, shedding light on how financial institutions can leverage this technology to enhance their strategies. Understanding AI in debt collection Artificial intelligence, which encompasses machine learning, natural language processing, and other advanced technologies, is transforming various industries, including debt collection. AI in debt collection involves using these technologies to automate and optimize processes, making them more efficient and effective. Examples of AI technologies in debt collection include predictive analytics, chatbots, and automated communication systems. Predictive analytics. Predictive debt collection analytics is a powerful tool in AI collections. By analyzing patterns and trends in debtor behavior, AI can forecast the likelihood of repayment. This information allows financial institutions to tailor their collection strategies to individual debtors, improving the chances of successful recovery. Chatbots and virtual assistants. AI-powered chatbots and virtual assistants handle routine customer interactions, providing instant responses to common queries. These tools can escalate complex issues to human agents when necessary, ensuring that customers receive the appropriate level of support. By automating routine tasks, chatbots free up human agents to focus on more complex cases. Automated communication. AI can automate communication with debtors, sending payment reminders and notifications through various channels such as email, SMS, and phone calls. These messages can be customized based on debtor profiles, ensuring that communication is personalized and effective. Automated communication helps maintain consistent contact with debtors, increasing the likelihood of timely payments. Key benefits of AI-powered debt collection Beyond practical applications, AI delivers substantial value across an organization’s debt collection strategy. From streamlining operations to improving customer engagement and decision-making, the benefits outlined below illustrate how AI helps financial institutions reduce costs, optimize resources, and achieve better outcomes. Improved operational efficiency. One of the most significant advantages of AI in debt collection is improved operational efficiency. AI can automate repetitive tasks such as sending payment reminders and processing payments, reducing the need for manual intervention. This automation speeds up the process, reduces costs, and minimizes human errors, ensuring more accurate and timely collections. Better decision-making. AI collections leverage predictive analytics to assess debtor risk and provide data-driven insights. This information enables financial institutions to develop more effective collection strategies and prioritize high-risk accounts. By making informed decisions based on predictive models, institutions can optimize collections processes and increase their chances of successful debt recovery. More cost savings. Automation through AI can lead to significant cost savings. Financial institutions can achieve higher profitability by reducing the need for human intervention and lowering operational costs. Additionally, increased recovery rates due to better cure strategies contribute to overall cost efficiency. Enhanced customer experience. AI-driven chatbots and virtual assistants can provide personalized communication, enhancing the customer experience. These AI tools are available 24/7, allowing customers to get instant responses to their queries at any time. By offering a seamless and responsive service, financial institutions can improve customer satisfaction and engagement strategies. Challenges and considerations While AI offers numerous benefits, there are challenges and considerations to keep in mind. Data privacy and security are paramount, as financial institutions must ensure compliance with regulations such as General Data Protection Regulation (GDPR) and California Consumer Privacy Act (CCPA). Balancing automation with the need for a human touch is also crucial, as some customers may prefer interacting with human agents. Additionally, addressing potential biases in AI algorithms is essential to ensure fair and equitable treatment of all debtors. Our debt management and collection solutions The future of AI in debt collection looks promising, with emerging technologies poised to make a significant impact. Integration of AI with other technologies such as blockchain and the Internet of Things (IoT) could further enhance the efficiency and security of debt collection processes. As AI continues to evolve, financial institutions must stay abreast of these trends to remain competitive and effective in their collection strategies. With more than 25 years of experience and a comprehensive suite of collection products, our enhanced decisioning, improved processes, and account prioritization can enable your organization to move toward a customer-centric approach that helps reduce losses and control costs. AI in debt collection offers a myriad of benefits, from improved efficiency and enhanced customer experience to better decision-making and cost savings. By leveraging AI technologies such as predictive analytics, chatbots, and automated communication, financial institutions can optimize their debt collection strategies and achieve higher recovery rates. As the industry continues to evolve, embracing AI will be crucial for financial institutions looking to stay ahead of the curve. Discover how Experian’s AI-powered debt management and collection solutions can help you recover more while improving customer relationships. Learn more

Property managers and landlords nationwide aim to attract reliable, long-term tenants. Gaining insight into modern renters—their tenant data, financial situations, lifestyle choices, and key priorities—gives proactive property owners and managers a competitive edge in appealing to the ideal tenant. While certain elements of the rental landscape are not within the control of market professionals, knowledge is power, and understanding the preferences, spending habits, and profiles of today’s renters can inform their business approach and success. To understand today’s renter, Experian® took a deep dive into the tenant data of the rental market landscape in its 2024 report on the U.S. rental market. Among the principal findings, Generation Z and younger millennials' dominance in this sector is rising. Today’s Renter Profile Experian research reveals movements in the demographics of the average U.S. renter, now dominated by younger individuals and lower average-income consumers. These renters face challenges as they navigate the rising costs of securing housing. The 2024 rental report delves into these changes, highlighting age and income level shifts in tenant data. Critical to property managers and landlords, this information offers an understanding of their customer base and provides insight into the rental market landscape. Gen Z on the Rise: Gen Z alone accounts for 30.5% of all renters, and their numbers are increasing, up 3.5% over a year. Gen Z and younger millennials (adults under 35) represent over 50% of the rental population. Income Declines: From January 2023 to January 2024, the tenant data showed the average income of RentBureau® renters fell from $53,100 to $52,600[1]. Higher Rent Costs: In 2024, over 50% of renters paid $1,500+ per month, with the average U.S. renter's monthly payment of $1,713. Gen Z,the youngest renter population, spends an average of $1,600 monthly on rent. This context plays an important role in examining the state of the 2024 rental market. Propensity to Move In addition to age and economic well-being, landlords should take a keen interest in tenant data related to renters’ moving habits, as these provide valuable insights into behavior and market trends. Landlords generally prefer longer-term leaseholders, and renters who stay longer provide more stability to property management efforts. Not surprisingly, generational trends appear here as well. While over 90% of all renters retained one lease over a 2-year period, tenant data indicates that Gen Z and younger millennial renters tend to move more than other age groups. This tendency stems from various factors, including a willingness to relocate to more affordable regions or areas that better suit their lifestyle preferences. With today’s evolving work environment, remote work has opened new possibilities. Again, the overarching trend is that renters stay in one place for two years. In fact, this represents 92.5% of all renters. Signs of Overall Renter Financial Health Housing is a significant monthly cost of living expense, especially for many younger adults just starting out and lower-income individuals and families. The percentage of a renter’s monthly income allocated to rental costs clearly indicates housing affordability. This tenant data reflects that higher rent-to-income ratios (RTIs) signify that renters have less financial flexibility, as a larger portion of their monthly income is allocated to rent, leaving less available for essentials, savings, and discretionary spending. On average, renters spend over 44% of their monthly income on rent, and low-to-moderate-income renters dedicate over 50% to rent. General guidelines suggest that the percentage should be no more than 30%. Higher rental costs and declining annual incomes disproportionately impact those with fewer financial means. Credit and Other Signs Landlords and property managers value tenant data, such as renter applicants' stability. Indicators such as overall credit quality and negative payment history provide valuable insights into economic well-being. While negative payment history has improved slightly, the market shows a rise in delinquencies. Experian’s research highlights that while credit scores for the general U.S. population are on the rise, the trends for renters tell a slightly different story. Between May 2023 and May 2024, tenant data revealed a 2% increase in renters fell into the near-prime and subprime credit categories. Although the implications for the future remain uncertain, this data, combined with other analytics, may offer clues about market trends and opportunities. The Future The demand for rentals remains high, particularly among young adults and lower-income households. As the economy and market forces fluctuate, so do the financial pressures on renters and rental housing availability and costs. The role of young adults and lower-income households in the rental market will continue. Landlords and property managers must tune in to demographic realities in their efforts to develop risk management and success strategies. To learn more about the state of the U.S. rental market, download Experian’s 2024 rental report. [1] RentBureau income is based on modeled income, which is estimated using credit data and other predictive factors.

As we step into 2025, the convergence of credit and fraud risk has become more pronounced than ever. With fraudsters leveraging emerging technologies and adapting rapidly to new defenses, risk managers need to adopt forward-thinking strategies to protect their organizations and customers. Here are the top fraud trends and actionable resolutions to help you stay ahead of the curve this year. 1. Combat synthetic identity fraud with advanced AI models The trend: Synthetic identity fraud is surging, fueled by data breaches and advanced AI tooling. Fraudsters are combining genuine credentials with fabricated details, creating identities that evade traditional detection methods. Resolution: Invest in sophisticated identity validation tools that leverage advanced AI models. These tools can differentiate between legitimate and fraudulent identities, ensuring faster and more accurate creditworthiness assessments. Focus on integrating these solutions seamlessly into your customer onboarding process to enhance both security and user experience. 2. Strengthen authentication against deepfakes The trend: Deepfake technology is putting immense pressure on existing authentication systems, particularly in high-value transactions and account takeovers. Resolution: Adopt a multilayered authentication strategy that combines voice and facial biometrics with ongoing transaction monitoring. Dynamic authentication methods that evolve based on user behavior and fraud patterns can effectively counter these advanced threats. Invest in solutions that ensure digital interactions remain secure without compromising convenience. 3. Enhance detection of payment scams and APP fraud The trend: Authorized Push Payment (APP) fraud and scams are increasingly difficult to detect because they exploit legitimate customer behaviors. Resolution: Collaborate with industry peers and explore centralized consortia to share insights and develop robust detection strategies. Focus on monitoring both inbound and outbound transactions to identify anomalies, particularly payments to mule accounts. 4. Optimize Your Fraud Stack for Efficiency and Effectiveness The trend: Outdated device and network solutions are no match for GenAI-enhanced fraud tactics. Resolution: Deploy a layered fraud stack with persistent device ID technology, behavioral analytics, and GenAI-driven anomaly detection. Begin with frictionless first-tier tools to filter out low-hanging fraud vectors, reserving more advanced and costly tools for sophisticated threats. Regularly review and refine your stack to ensure it adapts to evolving fraud patterns. 5. Build collaborative relationships with fraud solution vendors The trend: Vendors offer unparalleled industry insights and long-tail data to help organizations prepare for emerging fraud trends. Resolution: Engage in reciprocal knowledge-sharing with your vendors. Leverage advisory boards and industry insights to stay informed about the latest attack vectors. Choose vendors who provide transparency and are invested in your fraud mitigation goals, turning product relationships into strategic partnerships. Turning resolutions into reality Fraudsters are becoming more ingenious, leveraging GenAI and other technologies to exploit vulnerabilities. To stay ahead of fraud in 2025, let us make fraud prevention not just a resolution but a commitment to safeguarding trust and security in a rapidly evolving landscape. Learn more

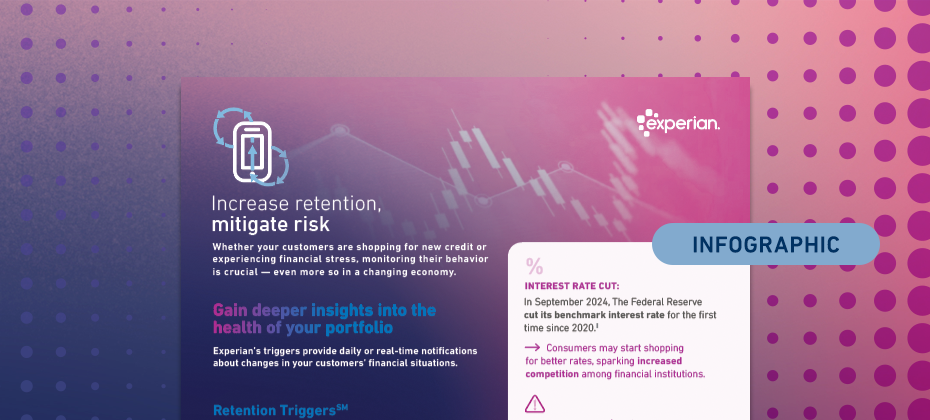

Whether consumers are shopping for new credit or experiencing financial stress, monitoring their behavior is crucial — even more so in an ever-changing economy. Our latest infographic explores economic trends impacting consumers’ financial behaviors and how Experian’s Risk and Retention TriggersSM enable lenders to detect early signs of risk or churn. Key highlights include: Credit card balances climbed to $1.17 trillion in Q3 2024. As prices of goods and services remain elevated, consumers may continue to experience financial stress, potentially leading to higher delinquency rates. Increasing customer retention rates by 5% can boost profits by 25% to 95%. View the infographic to learn how Risk and Retention Triggers can help you advance your portfolio management strategy. Access infographic

In 2024, the housing market defied recession fears, with mortgage and home equity growth driven by briefly lower interest rates, strong equity positions, generally positive economic indicators, and stock market appreciation. This performance is notable because, in 2023, economists’ favorite hobby was predicting a recession in 2024. Following a period of elevated inflation, driven largely by loose monetary policy, expansionary fiscal policy, and supply chain disruptions brought on by COVID, economists were certain that the US economy would shrink. However, the economy continued outperforming expectations, even as unemployment rose modestly (Figure 2) and inflation cooled (Figure 3). Source: FRED (Figure 1, Figure 2, Figure 3). So, a good economy is good for the mortgage and home equity markets, right? Generally speaking, this statement was true. As monitored by Experian’s credit database, mortgage originations increased by approximately thirty percent year over year as of November 2024 (Figure 4), and Q3 ’24 pre-tax profit for Independent Mortgage Banks (IMBs) averaged $701 per loan.1 So, business in home lending is good — certainly better than it was during the period when the Fed was raising rates, origination volumes shrank as opposed to grew, and IMB profit per loan turned negative. Source: Experian Ascend Insights Dashboard. What constituted this growth in mortgage lending? As we all know, the Fed has lowered interest rates by 100bps since they started reducing rates in September. The market had priced in the September cut weeks prior to the actual announcement (Figure 5), and the market enjoyed a spike in refinance volume as a result (Figure 6). However, in the lead-up to and following the US presidential election, interest rates spiked back up due to the market’s expectations around future economic activity, which will dampen pressure on refinance volumes even after the recent additional rate drop. The impact of further rate drops on mortgage rates is unclear, and refinance volume still constitutes only around three percent of overall origination volume. Source: Figure 5, Figure 6 (Experian Ascend Insights Dashboard). The shift to a purchase-driven housing market What does this all mean? Our view is that pockets of refinance volume (rate and term, VA, FHA, cashout) are available to those lenders with a sophisticated targeting strategy. However, the data also very clearly indicates that this market is still very much a purchase market in terms of opportunity for originations growth. This position should not surprise long-time mortgage lenders, given that purchase volume has always constituted a significant majority of origination volume. However, this market is a different purchase market than lenders may be used to. This purchase market is different because of unprecedented statistics about the housing market itself. The average age of a first-time homebuyer recently reached a record high of 38. The average age of overall homebuyers in November of this year similarly jumped to a new record high of 56, with homes being “wildly unaffordable for young people.” Twenty-six percent of home purchases are all-cash, another record high, and homeowners have an aggregate net equity position of $17.6 trillion, fueling those all-cash purchases. The market is expensive both from an interest rate perspective and a housing price-level perspective, and those trends are driving who is buying homes and how they are buying them.2 Opportunities for lenders in 2025 What do these housing market dynamics mean for lenders? To begin with, lenders should not spend money marketing mortgages to consumers in their 50s and 60s with large equity positions. These consumers are likely to be in the 26 percent all-cash buyer cohort, and that money will be wasted since mortgages are no longer so cheap that even cash-rich buyers would take them. Further, this equity-rich generation has children, and nearly 40% of those children borrow from the bank of mom and dad to purchase their first home. Since roughly a quarter (albeit a shrinking quarter) of homebuyers are first-time homebuyers, and since 40% of those rely on help from parents to facilitate that purchase, it may make sense for lenders to identify those consumers with 1) children and 2) significant equity positions and to offer products like cash-out refinances or home equity loans/lines to help facilitate those first-time purchases. Data is critical to executing these kinds of novel marketing strategies. It is one thing to develop these marketing and growth strategies in principle and another entirely to efficiently find the consumers that meet the criteria and give them a compelling offer. Consider home equity originations. As Figure 7 illustrates, HELOC originations are strong but have completely stalled from a growth rate perspective. As Figure 8 illustrates, this is despite the market's continued growth in direct mail marketing investment. Although HELOC origination volumes are a fraction of mortgage—around $27b per month for HELOC versus $182b per month for mortgage—there are significantly more home equity direct mail offers being sent per month (39 million) for home equity products as there are for mortgage (31 million) as of October ’24.3 This all means that although many lenders have wised up to the home equity opportunity to the point of saturating the market with offers, few have successfully leveraged targeting data and analytics to craft sufficiently compelling offers to those consumers to convert those marketing leads into booked loans. Source: Figure 7 (Experian Ascend Insights Dashboard), Figure 8 (Mintel). Adapting to a resilient housing market In summary, the housing market, comprised of mortgage and home equity products, has experienced persistent growth over the past year. Many who are reading this note will have benefitted from that growth. However, as we have identified, in many respects housing market growth has 1) been concentrated to some key borrower demographics and 2) many lenders are investing in marketing campaigns that are not efficiently reaching or convincing that key housing demographic to book loans, whether it be a home equity or mortgage product. As such, as we move into 2025, Experian advises our clients to focus on the following three themes to ensure they benefit from this trend of growth into the new year: Ensure you effectively differentiate your marketing targeting, collateral, and offers for the various demographics in the market. Ensure your origination experiences for mortgage and home equity products are modern and efficient. Lenders who force all borrowers through a painful, manual legacy process will waste marketing dollars and experience pipeline fallout. Although the market is growing, other lenders are coming for your current customers. They could be coming for purchase activity, refinance opportunities, or they may be using home equity products to encroach on your existing mortgage relationship. As such, capitalizing on growth in 2025 is not merely about gaining new customers; it is also about retaining your existing book of business using high-quality data and analytics. Learn more 1 Although December numbers are available for year-over-year comparison, we excluded them due to the holiday period's strong seasonality patterns. 2 The Case-Shiller index recently topped out at record levels. 3 Mintel/Comperemedia data.