Apply DA Tag

Despite rising concerns about identity theft, most Americans aren’t taking basic steps to make it harder for their information to be stolen, according to a survey Experian conducted in August 2017: Nearly 3 in 4 consumers said they’re very or somewhat concerned their email, financial accounts or social media information could be hacked. This is up from 69% in a similar survey Experian conducted in 2015. Nearly 80% of survey respondents are concerned about using a public Wi-Fi network. Yet, barely half said they take the precaution of using a password-protected Wi-Fi network when using mobile devices. 59% of respondents are annoyed by safety precautions needed to use technology — up 12% from 2015. When your customer’s identity is stolen, it can negatively impact the consumer and your business. Leverage the tools and resources that can help you protect both. Protect your customers and your business>

Synthetic identity fraud is on the rise across financial services, ecommerce, public sector, health and utilities markets. The long-term impact of synthetic identity remains to be seen and will hinge largely upon forthcoming efforts across the identity ecosystem made up of service providers, institutions and agencies, data aggregators and consumers themselves. Making measurement more challenging is the fact that much of the assumed and confirmed losses are associated with credit risk and charge offs, and lack of common and consistent definitions and confirmation criteria. Here are some estimates on the scope of the problem: Losses due to synthetic identity fraud are projected to reach more than $800 million in 2017.* Average loss per account is more than $10,000.* U.S. synthetic credit card fraud is estimated to reach $1.257 billion in 2020.* As with most fraud, there is no miracle cure. But there are best practices, and topping that list is addressing both front- and back-end controls within your organization. Synthetic identity fraud webinar> *Aite Research Group

Our national survey found that consumers struggle to find a credit card that meets their needs. They say there are too many options and it’s too time-consuming to research. What do consumers want? With 53% of survey respondents not satisfied with their current cards and 1 in 3 saying they’re likely to get a new card within 6 months, now’s the time to start personalizing offers and growing your portfolio. Start personalizing offers today>

Earlier this week, Javelin Strategy & Research announced its inaugural edition of the 2017 Identity Proofing Platform Awards. We were honored to see CrossCore as the leader – taking the award for the best overall identity proofing platform. According to the report, “Experian’s identity proofing platform is a strong performer in every category of Javelin’s FIT model. It is functional. It is innovative. And, most important, it is tailored toward the advisory’s expectations. The comprehensive nature of CrossCore makes it the market-leading solution for identity proofing.” It’s harder than ever to confidently identify your customers in today’s digital economy. You have lots of vendor solutions to choose from in the identity proofing space. And, now Javelin has made it much easier for you to select the partner that is right for your needs. Javelin’s newly minted Identity Proofing Platform Scorecard assesses current capabilities in the market to help you make that decision. And they have done a lot of the heavy lifting, looking across 23 vendors and scoring them based on three categories of their FIT model – functional, innovative, and tailored. Protecting customers is a priority for you – and for us. Here at Experian, we have a range of capabilities to help businesses manage identity proofing, and our CrossCore platform brings them all together. We launched CrossCore last year, with the goal of making the industry’s fraud and identity solutions work better for everyone. CrossCore delivers a future-proof way to modify strategies quickly, catch fraud faster, improve compliance and enhance the customer experience. We’re proud of the work we’ve done so far, integrating our products as well as adding more than 10 partners to the program. We’re pleased to see so many of our partners included in Javelin’s report. We’re working closely with our clients to pull in more partner capabilities, and further enhance our own platform to create a layered approach that supports a risk-based, adaptable strategy. As highlighted in the Javelin report, a reliance on traditional identity verification approaches are no longer sufficient or appropriate for digital channels. With CrossCore, our clients can choose the capabilities they want, when they want them, to dial in the right confidence level for each and every transaction. This is because CrossCore supports a layered approach to managing risk, allowing companies to connect multiple disparate services through a common access point. We are committed to making it easier for you to protect consumers against fraud. CrossCore is helping us all do just that.

The collections space has been migrating from traditional mail and outbound calls to electronic payment portals, digital collections and virtual negotiators. Now that collectors have had time to test virtual collections, we’ve collected some data points. Here are a few: On average, 52% of consumers who visit a digital site will proceed to a payment schedule if the right offer is made. 21% of the visits were outside the core hours of 8 a.m. to 8 p.m., an indication that traditional business hours don’t always work. Of the consumers who committed to a payment plan, only 56% did it in a single visit. The remaining 44% did so mostly later that day or on a subsequent day. As more financial institutions test this new virtual approach, we anticipate customer satisfaction and resolutions will continue to climb. Get your debt collections right>

With 1 in 6 U.S. residents being Hispanic, now is a great time for financial institutions to reflect on their largest growth opportunity. Here are 3 misconceptions about the multifaceted Hispanic community that are prevalent in financial institutions: Myth 1: Hispanic consumers are only interested in transaction-based products. In truth, product penetration increases faster among Hispanic members compared with non-Hispanic members when there’s a strategic plan in place. Myth 2: Most Hispanics are undocumented. The facts show that of the country’s more than 52 million Hispanics, most are native-born Americans and nearly 3 in 4 are U.S. citizens. Myth 3: The law prevents us from serving immigrants. Actually, financial institutions can compliantly lend to individuals who have an Individual Taxpayer Identification Number. There are many forms of acceptable government-issued identification, such as passports and consular identification cards. Solidifying the right organizational mentality, developing a comprehensive strategy based on segmentation, and defining what success truly looks like. These are all part of laying the foundation for success with the Hispanic market. Learn more>

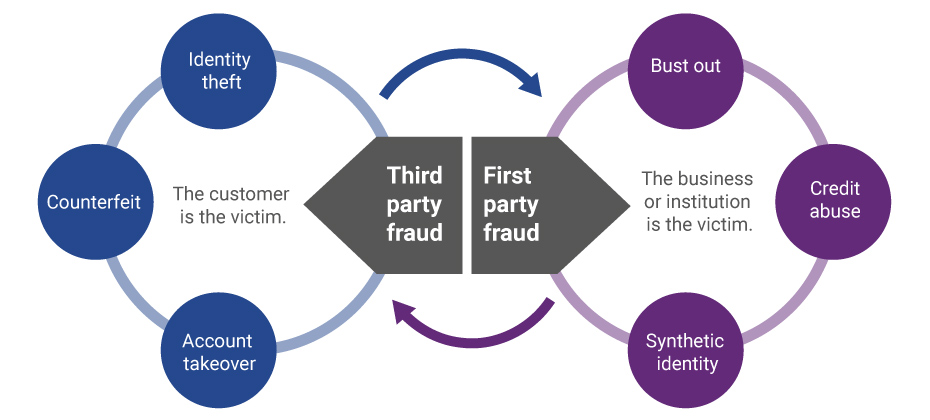

Evolution of first-party fraud to third Third-party and first-party schemes are now interchangeable, and traditional fraud detection practices are less effective in fighting these evolving fraud types. Fighting this shifting problem is a challenge, but it isn’t impossible. To start, incorporate new and more robust data into your identity verification program and provide consistent fraud classification and tagging. Learn more>

We recently analyzed millions of online transactions from the first half of 2017 to identify fraud attack rates. Here are the top 3 riskiest states for e-commerce billing and shipping fraud for H1 2017: Riskiest states for billing fraud Oregon Delaware Washington, D.C. Riskiest states for shipping fraud Oregon Delaware Florida Fraudsters are extremely creative, motivated and often connected. Protect all points of contact with your customers to prevent this growing type of fraud. Is your state in the top 10?

Cybersecurity cannot be successful if siloed. The entire organization must be part of the effort. Take these steps to ensure a more engaged relationship between cybersecurity teams, C-suite executives and other departments: Make the company’s chief information officer accountable directly to the chief executive officer and/or the board. Train employees at every level to spot security risks and to understand their role in protecting the entire organization from cyberattacks. Put cybersecurity on the agenda for every board and executive-level meeting, and incorporate it into quarterly state-of-the-company, all-hands meetings. With cybersecurity threats evolving and escalating daily, companies need to make engagement a priority that starts at the top and continues through every level of the organization. Increasing engagement in cybersecurity >

Since the advent of the internet, our lives have changed drastically for the better. We can perform many of life’s daily activities from the comfort of our own home. According to Aite, in 2016 alone 36 million Americans made some form of mobile payment — paying a bill, purchasing something online, paying for fast food or making a mobile wallet purchase at a retailer. Simply put, the internet has made our lives easier. But with the good also comes the bad. While most consumers have moved to the digital world, so have fraudsters. With minimal risk and high reward at stake, e-commerce fraud attacks have increased dramatically over the last few years, with no signs of slowing down. We recently analyzed millions of transactions from the first half of 2017 to identify fraud attack rates based on billing and shipping addresses and broke down the findings into various geographic trends. Fraud attack rates represent the attempted fraudulent e-commerce transactions against the population of overall e-commerce orders. Consumers living out West and in the South have experienced more than their fair share of fraud. During the first half of 2017, the West and the South were the top two regions for both billing and shipping attacks. While both regions were at the top during the same time last year, the attacks themselves have increased substantially. Given the proximity to seaports and major international airports, this is somewhat unsurprising — particularly for shipping fraud — as many fraudsters will leverage reshippers to transport goods soon after delivery. .dataTb{margin:20px auto;width:100%}.dataTb:after{clear:both}.dataTb table{}.dataTb td,.dataTb th{border:1px solid #ddd;padding:.8em}.dataTb th{background:#F4F4F4}.tbL{float:left;width:49%}.tbR{float:right;width:49%;margin:0 0 0 2%} Shipping: Riskiest Regions Region Attack rate West 38.1 South 32.1 Northeast 27.0 North Central 20.7 Billing: Riskiest Regions Region Attack rate West 37.2 South 32.9 Northeast 27.3 North Central 24.0 At the state level, the top three shipping fraud states remained the same as 2016 — Delaware, Oregon and Florida — but the order changed. Oregon was the most targeted, with a fraud rate of 135.2 basis points, more than triple its rate at in the end of 2016. Though no longer in the top spot, Delaware saw alarming spikes as well, with shipping attack rates nearly triple last year’s rate at 128.6 basis points and billing attacks at 79.6 basis points. .dataTb{margin:20px auto;width:100%}.dataTb:after{clear:both}.dataTb table{}.dataTb td,.dataTb th{border:1px solid #ddd;padding:.8em}.dataTb th{background:#F4F4F4}.tbL{float:left;width:49%}.tbR{float:right;width:49%;margin:0 0 0 2%} Shipping: Riskiest States State Attack rate Oregon 135.2 Delaware 128.2 Florida 57.4 New York 45.0 Nevada 36.9 California 36.9 Georgia 33.5 Washington, D.C 30.8 Texas 29.6 Illinois 29.4 Billing: Riskiest States Region Attack rate Oregon 87.5 Delaware 79.6 Washington, D.C. 63.0 Florida 47.4 Nevada 38.8 California 36.9 Arkansas 36.6 New York 35.5 Vermont 34.2 Georgia 33.4 Diving a bit deeper, ZIPTM codes in Miami, Fla., make up a significant portion of the top 10 ZIP CodeTM lists for shipping and billing attacks — in fact, many of the same ZIP codes appear on both lists. The other ZIP Code that appears on both lists is South El Monte, Calif., which has a high percentage of industrial properties — common targets for fraudsters to ship packages, then reship overseas. You can download the top 100 riskiest Zip Codes in the U.S. for H1 2017. .dataTb{margin:20px auto;width:100%}.dataTb:after{clear:both}.dataTb table{}.dataTb td,.dataTb th{border:1px solid #ddd;padding:.8em}.dataTb th{background:#F4F4F4}.tbL{float:left;width:49%}.tbR{float:right;width:49%;margin:0 0 0 2%} Shipping: Top 10 riskiest ZIP™ Codes ZIP Code Attack rate 33122 [Miami, Fla.] 2409.4 91733 [South El Monte, Calif.] 1655.5 33198 [Miami, Fla.] 1295.2 33166 [Miami, Fla.] 1266.0 33195 [Miami, Fla.] 1037.3 33192 [Miami, Fla.] 893.9 97251 [Portland, Ore.] 890.6 07064 [Port Reading, NJ] 808.9 89423 [Minden, Nev.] 685.5 77072 [Houston, Tex.] 629.3 Billing: Top 10 riskiest ZIP™ Codes ZIP Code Attack rate 77060 [Houston, Tex.] 1337.6 33198 [Miami, Fla.] 1215.6 33122 [Miami, Fla.] 1106.2 33166 [Miami, Fla.] 1037.4 91733 [South El Monte, Calif.] 780.1 33195 [Miami, Fla.] 713.7 97252 [Portland, Ore.] 670.8 33191 [Miami, Fla.] 598.8 33708 [St. Petersburg, Fla.] 563.6 33792 [Miami, Fla.] 493.0 As e-commerce fraud continues to grow, businesses need to be proactive to keep themselves and their customers safe. That means incorporating multiple, layered fraud prevention strategies that work together seamlessly — for example, understanding details about users and their devices, knowing how users interact with the business and evaluating previous transaction history. This level of insight can help businesses distinguish real customers from nefarious ones without impacting the customer experience. While businesses are ultimately responsible for the safety of customers and their data, the onus doesn’t rest solely with them. Consumers should also be vigilant when it comes to protecting their digital identities and payment information. That means creating strong, unique passwords; actively monitoring online accounts; and using two-factor authentication to secure account access. At the end of the day, e-commerce fraud is a challenge that businesses and consumers will experience for the foreseeable future. But rising attack rates don’t have to spell doom and gloom for the industry. E-commerce growth is still extremely strong, as consumers interact through multiple channels (in-store, mobile and web) and expect a personalized experience. Establishing trust and verifying digital identities are key to meeting these latest expectations, which provide new opportunities for businesses and consumers to interact seamlessly and transact securely. With multiple safeguards in place, businesses have a variety of options to protect their customers and their brand reputation. Experian is a nonexclusive full-service provider licensee of the United States Postal Service®. The following trademarks are owned by the United States Postal Service®: ZIP and ZIP Code. The price for Experian’s services is not established, controlled or approved by the United States Postal Service.

We regularly hear from clients that charge-offs are increasing and they’re struggling to keep up with the credit loss. Many clients use the same debt collection strategy they’ve used for years – when businesses or consumers can’t repay a loan, the creditor or collection agency aggressively contacts them via phone or mail to obtain repayment – never considering the customer experience for the debtor. Our data shows that consumers accounted for $37.24 billion in bankcard charge-offs in Q2 2017, a 17.1 percent increase from Q2 2016. Absorbing credit losses at such a high rate can impact the sustainability of the institution. Clearly the process could use some adjusting. Traditionally, debt collection has been solely about the money. The priority was ensuring that as much of the outstanding debt as possible was repaid. But collecting needs to be about more than that. It also should focus on the customer and his or her individual situation. When it comes to debt collection, customers should not all be treated the same way. I recently shared some tips in Credit Union Business Magazine about how to actively engage and collect from members. The same holds true for other financial institutions – they need to know the difference between a customer who has simply forgotten to make a payment and one who is dealing with financial hardship. As an example, if a person is current on his or her mortgage payment but has slipped behind on his or her credit card payment, that doesn’t necessarily signify financial hardship. It’s an opportunity to work with the customer to manage the debt and get back to current. Modern financial institutions build acquisition and customer management strategies targeted at individuals, so why should the collection process be any different? The challenge is keeping the customer at the center while also managing against potential increases in delinquencies. This holistic approach may be slightly more complex, but technology and analytics will simplify the process and bring about a more engaging experience for customers. The Power of Data and Technology Instead of relying on the same outdated collections approach – which results in uncomfortable exchanges on the phone that don’t ensure repayment –leverage data to your advantage. The data and technology exists to help you make more informed decisions, such as: What’s the most effective communication channel to reach the defaulting customer? When should you contact him or her? How often? The best course of action could be high-touch outreach, but sometimes doing nothing is the right approach. It all depends on the situation. Data and analytics can help uncover which customers are most likely to pay on their own and those who may need a little more help, allowing you to adjust your treatment strategy accordingly. By catering to the preferences of the customer, there’s a greater chance for a positive experience on both sides. The results: less charge-off debt, higher customer satisfaction and a stronger relationship. Explore the Digital Age In 2016, 36 million Americans made some form of mobile payment—paying a bill, purchasing something online, or paying for fast food, or making a Mobile Wallet purchase at a retailer. By 2020, nearly 184 million consumers will have done so, according to Aite. Consumers expect and deserve convenience. In the digital world, financial institutions have an opportunity to provide that expectation and then some. Imagine a customer being able to negotiate and manage his or her past-due account virtually, in the privacy of his or her own home, when it’s most convenient, to set their payment dates and terms. Luckily, the technology exists to make this vision a reality. Customers, not money, need to be at the heart of every debt collections strategy. Gone are the days of mass phone calls to debtors. That strategy made consumers unhappy, embarrassed and resentful. Successful debt collection comes down to a basic philosophy: Treat customers and his or her unique situation individually rather than as a portfolio profile. The creditors who live by that philosophy have an opportunity to reap the rewards on the back-end.

There’s a consensus that too many C-suite executives are disengaged with their organization’s cybersecurity efforts. That indifference can seriously hamper an organization’s ability to quickly and effectively respond to an incident. To best protect the organization, cybersecurity professionals should take the following steps to increase engagement: Pinpoint the greatest cybersecurity issues your organization faces and create descriptive verbiage that simplifies these risks. Engage in one-on-one meetings with key leaders to help them understand how cybersecurity risks affect not only the overall organization, but their domain as well. Stage a cybersecurity simulation exercise for your C-suite executives in which members role-play a data breach scenario. Leadership is not the only department that should be invested in protecting the organization. Next week, we’ll look at how to engage the entire organization in cybersecurity efforts. If you’d like, you can jump ahead and read it now. Increasing engagement in cybersecurity

Leadership and Cybersecurity Multiple studies suggest many executives aren’t as engaged as they should be when ensuring their organizations are prepared to mitigate and manage cybersecurity risks. Insights from our Fourth Annual Data Breach Preparedness Survey, conducted by the Ponemon Institute, support this sentiment. Of the privacy, compliance and IT professionals polled: 57% said their company’s board, chairman and chief executive officer were not informed about or involved in data breach response planning. 60% have leadership who don’t want to know immediately when a material breach occurs. 66% have a board that doesn’t understand the specific cybersecurity threats their organization faces. 74% said their board isn’t willing to take ownership for successful incident response plan implementation. For organizations to protect themselves, cybersecurity professionals need to create greater engagement among the organization’s leadership. Next week, we’ll look at how they can accomplish this. If you’d like, you can jump ahead and read it now. Fourth Annual Data Breach Preparedness Survey

There’s no shortage of headlines alluding to a student loan crisis. But is there a crisis brewing or is this just a headline grab? Let’s look at the data over the past 4 years to find out. Outstanding student loan (should be loan) debt grew 21%, reaching a high of $1.49 trillion in Q4 2016. Over the past 4 years, student loan trades grew 4%, with a slight decline from 2015 to 2016. Average balance per trade grew 17% to reach $8,210. Number of overall student loan trades per consumer is down 5% to just 3.85. The average person with a student loan balance had just over $32,000 outstanding at the end of 2016 — a rise of 15%. While we’re seeing some increases, the data tells us this is a media headline grab. If students are educated about the debt they’re acquiring and are confident they can repay it, student loan debt shouldn’t be a crippling burden. More student loan insights

Did you know that 80% of all data migrations fail? Like any large project, data migration relies heavily on many variables. Successful data migration depends on attention to detail, no matter how small. Here are 3 items essential to a successful data migration: Conduct a Pre-Migration Impact Assessment to identify the necessary people, processes and technology needed. Ensure accurate, high-quality data to better streamline the migration process and optimize system functionality. Assemble the right team, including an experienced leader and business users, to ensure timely and on-budget completion. 35% of organizations plan to migrate data this year. If you’re among them, use this checklist to create the right plan, timeline, budget, and team for success.