E-commerce / Retail

As we approach the one-year anniversary of the EMV liability shift, we have seen an increase in e-commerce fraud — to the tune of 15% higher than last year.

In this new Telephone Consumer Protection Act (TCPA) era, calling your customers isn’t a thing of the past. It’s still okay to reach out to your clients by phone, whether to offer a new product or collect on an overdue bill. But strict compliance with TCPA rules is critical for any business that contacts customers by phone. Some of the very best ways you can protect yourself from TCPA exposure is to follow four steps when creating your dialing strategy: Customer consent: It’s important to maintain and update your customers’ contact preferences and consent to call them. Simply having a phone number on an application isn’t sufficient. Companies are required to have written permission, such as “I consent to calling my cell phone when there’s a problem …” Remember, permission may only be granted by the party who subscribes to the cellular service or who regularly uses that cell phone number. Landline or wireless?: Your database should also include the phone type for the telephone numbers you have for your customers. The dialing rules differ depending on the phone type, so it’s critical to know the type of phone you are calling or texting. Verify ownership: Ownership of cell phones should especially be validated to ensure the number hasn’t been reassigned and that the person who gave consent still owns the phone. One call can be made to a reassigned number with no liability, assuming you have no knowledge the number has changed. Repeating the action could lead to fines from $500 to $1,500 per infraction. Scrub Your Database: Have practices in place to remove any confirmed reassigned phone numbers from your database. This will help to improve your right-party contact rate and save you from potential TCPA headaches. No one disagrees that calling cell numbers is a risky business, but it can be done if you set the proper workflow in motion. Click here to learn more about Experian solutions that will help to reduce your TCPA compliance risk.

Experian analyzes e-commerce fraud attack rates bi-annually. The 2016 e-commerce fraud attack rates look to be at least 15% higher than last year’s total.

Most businesses are familiar with credit bureaus today, but myths still exist around reporting credit data. Let's examine the top three and bust them.

Experian conducted a joint-survey that uncovered insights into the topic of conversational commerce and voice assistants. The survey asked about general consumer satisfaction with the voice-recognition capabilities of Amazon's Alexa relative to other smart voice assistants such as Siri and Google.

Experian estimates card-to-card consumer balance transfer activity to be between $35 and $40 billion a year, representing a sizeable opportunity for proactive lenders seeking to grow their revolving product line. This opportunity, however, is a threat for reactive lenders that only measure portfolio attrition instead of working to retain current customers. While billions of dollars are transferred every year, this activity represents only a small percentage of the total card population. And given the expense of direct marketing, lenders seeking to capitalize on and protect their portfolio from balance transfer activity must leverage data insights to make more informed decisions. Predicting a consumer’s future propensity to engage in card-to-card balance transfers starts with trended data. A credit score is a snapshot in time, but doesn’t reveal deep insights about a consumer’s past balance transfer activity. Lenders that rely only on current utilization will group large populations of balance revolvers into one bucket – and many of these individuals will have no intention of transferring to another product in the near future. Still, balance transfer activity can be identified and predicted by utilizing trended data. By analyzing the spend and payment data over time to see when one (or multiple) trade’s payment approximately matches another trade’s spend, we have the logic that suggests there has been a card-to-card transfer. What most people don’t realize is that trended data is difficult to work with. With 24 months of history on five fields, a single trade includes 120 data points. That’s 720 data points for a consumer with six trades on file and 72,000,000 for a file with 100,000 records, not to mention the other data fields in the file. It’s easy to see why even the most sophisticated organizations become paralyzed working with trended data. While teams of analysts get buried in the data, projects drag, costs swell, and eventually the world changes as rates climb and fall. By the time the analysis is complete, it must be recalibrated. But there is a solution. Experian has developed powerful predictions tools that combine past balance transfer history, historical transfer amounts, current trades carried and utilized, payments, and spend. Combined, these data fields can help identify consumers who are most likely to transfer a balance in the future. With Experian’s Balance Transfer Index the highest scoring 10 percent of consumers capture nearly 70 percent of total balance transfer dollars. Imagine the impact on ROI of reducing 90 percent of the marketing cost of your next balance transfer campaign and still reaching 70 percent of the balance transfer activity. Balance transfer activity represents a meaningful dollar opportunity for growth, but is concentrated in a small percentage of the population making predictive analytics key to success. Trended data is essential for identifying those opportunities, but financial institutions must assess their capabilities when it comes to managing the massive data attached. The good news is that regardless of financial institution size, solutions now exist to capture the analytics and provide meaningful and actionable insights to lenders of all sizes.

First annual global fraud report covering the convergence of growth strategies and fraud threats and prevention.

All customers are not created equal - at least when it comes to ability to pay. So what are the natural moments for a lender to assess?

Financial health open doors for people, creating opportunities for credit, cars, homes and stability. So how can you get "healthy?"

In an attempt to stay ahead of the speed of fraud, systems have become more complex, more expensive and even more difficult to manage.

While organizations increasingly rely on data to make decisions, when it comes to data accuracy, too many wait to correct errors rather than implement proactive solutions.

Definition of first-party versus third-party fraud trends and shared actual case study of a first-party fraud scheme.

Fraud Solutions Made Easy — solving new fraud problems by Adapting Legacy Solutions

Led a session about call center authentication. After introductions and a discussion about existing call center identity authentication techniques...

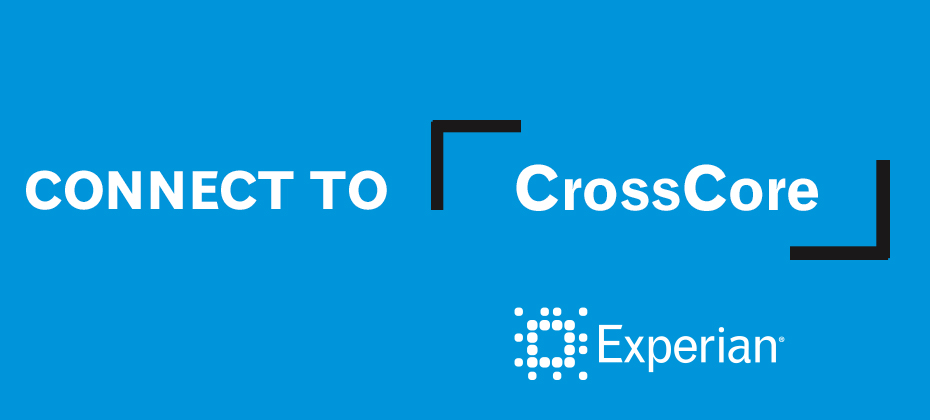

Experian launches industry’s first smart plug-and-play fraud platform allowing companies to connect their solutions, Experian products, and third-party vendors in one place.