Industries

Over the last year and a half, strong trends emerged in how businesses and consumers interact online - specifically when validating identities and preventing fraud. We initially explored these trends at a global level, and now we've explored U.S.-specific insights into online security, the customer experience, and digital activities and operations. Download the North America findings report to learn more about business and consumer fraud and identity trends impacting the way we live, work, and interact. Review your fraud strategy

Millions of consumers lack credit history and/or have difficulty obtaining credit from mainstream financial institutions. As a result, the use of expanded Fair Credit Reporting Act (FCRA) – or alternative – data has continued to gain popularity among lenders and financial intuitions to enrich decisions across the entire lending lifecycle to meet the financial needs of their consumers. Experian presented in a recent webinar hosted by AFSA, where Alpa Lally, Vice President of Product Management, and David Elmore, Automotive Solutions Consultant, had a chance to speak about the benefits of FCRA data, and ways lenders can leverage this data to ease access to credit for “invisible” and below prime consumers. Watch the full webinar, “FCRA Data: The Key to Unlocking Credit Universe” and learn more about: How expanded FCRA data is being used throughout the lending lifecycle The benefits of leveraging FCRA data including providing a more holistic view of a consumer’s credit profile and behavior beyond financial services, leading to smarter, more informed lending decisions The lift FCRA data can offer when augmented with traditional credit data This webinar is a part of AFSA’s partner webinar series. To learn more about FCRA data and explore related content, please visit our FCRA Alternative Credit Data Resources Page. Learn More About FCRA-Alternative Credit Data

Have you ever wanted to ask a customer to sign an AutoCheck vehicle history report to indicate they have received and reviewed the report and they are aware of the status of the vehicle they are purchasing?

As lenders and consumers emerge from the pandemic, predicting the attributes of the “new normal” will be difficult. Consumer demand, credit characteristics and economic conditions have all been affected by the pandemic – changing the way we think about doing business. Regulators and legislators have also developed new priorities and expectations for financial institutions. Clint Ivester, Experian’s Solutions Consultant and VP of Sales, joined Lee Gilley and Jonathan Kkolodziej, Partners for Bradley, to share their observations from the past year at AFSA’s 2021 Independents Conference. They also discussed recommendations financial institutions should consider to achieve the best possible posture with respect to compliance and business readiness. Here are a few Q&A highlights: Q: How are stimulus packages and increased government spending affecting economic conditions? A: [Ivester]: Our Experian forecast shows that the economy will grow 6% in 2021. That is well above the 2.5% average we have seen over the last four decades and highest rate since 1983. While the economy is oriented toward growth, how strong that growth is going to be will really depend on how well things go when the “training wheels” are taken off, how robust the recovery is for lower-income workers, and how consumer spending habits have been altered by the pandemic. *Data sources include Bureau of Economic Analysis and Experian’s “COVID-19 Economics Scenarios” April 2021 Report Q: How should businesses be assessing future consumer demand, conditions, and broader economic conditions over the next few quarters? A: [Ivester]: To answer this question, we should consider some factors including unemployment. What happens with lower income workers will have a big impact on where consumer spending goes post-stimulus. While the overall economy is set for solid growth there are still 8 million people out of work with the vast majority being lower income workers. Employment for lower income workers is still down more than 20%. These workers are set to lose the most by the phase out of the federal pandemic unemployment programs and are the highest risk to lose all unemployment benefits. However, if we see a strong jobs recovery – as is very possible – in bars, restaurants, hotels and other industries, these individuals will return to more normal spending habits and consumer spending should remain robust. *Data source includes Opportunity Insights Economic Tracker Watch the full session to hear more about the discussion. For more resources and content on this topic, please visit our Look Ahead Resources page or contact us for more information.

Lately, I’ve been surprised by the emphasis that some fraud prevention practitioners still place on manual fraud reviews and treatment. With the market’s intense focus on real-time decisions and customer experience, it seems that fraud processing isn’t always keeping up with the trends. I’ve been involved in several lively discussions on this topic. On one side of the argument sit the analytical experts who are incredibly good at distilling mountains of detailed information into the most accurate fraud risk prediction possible. Their work is intended to relieve users from the burden of scrutinizing all of that data. On the other side of the argument sits the human side of the debate. Their position is that only a human being is able to balance the complexity of judging risk with the sensitivity of handling a potential customer. All of this has led me to consider the pros and cons of manual fraud reviews. The Pros of Manual Review When we consider the requirements for review, it certainly seems that there could be a strong case for using a manual process rather than artificial intelligence. Human beings can bring knowledge and experience that is outside of the data that an analytical decision can see. Knowing what type of product or service the customer is asking for and whether or not it’s attractive to criminals leaps to mind. Or perhaps the customer is part of a small community where they’re known to the institution through other types of relationships—like a credit union with a community- or employer-based field of membership. In cases like these, there are valuable insights that come from the reviewer’s knowledge of the world outside of the data that’s available for analytics. The Cons of Manual Review When we look at the cons of manual fraud review, there’s a lot to consider. First, the costs can be high. This goes beyond the dollars paid to people who handle the review to the good customers that are lost because of delays and friction that occurs as part of the review process. In a past webinar, we asked approximately 150 practitioners how often an application flagged for identity discrepancies resulted in that application being abandoned. Half of the audience indicated that more than 50% of those customers were lost. Another 30% didn’t know what the impact was. Those potentially good customers were lost because the manual review process took too long. Additionally, the results are subjective. Two reviewers with different levels of skill and expertise could look at the same information and choose a different course of action or make a different decision. A single reviewer can be inconsistent, too—especially if they’re expected to meet productivity measures. Finally, manual fraud review doesn’t support policy development. In another webinar earlier this year, a fraud prevention practitioner mentioned that her organization’s past reliance on manual review left them unable to review fraud cases and figure out how the criminals were able to succeed. Her organization simply couldn’t recreate the reviewer’s thought process and find the mistake that lead to a fraud loss. To Review or Not to Review? With compelling arguments on both sides, what is the best practice for manually reviewing cases of fraud risk? Hopefully, the following list will help: DO: Get comfortable with what analytics tell you. Analytics divide events into groups that share a measurable level of fraud risk. Use the analytics to define different tiers of risk and assign each tier to a set of next steps. Start simple, breaking the accounts that need scrutiny into high, medium and low risk groups. Perhaps the high risk group includes one instance of fraud out of every five cases. Have a plan for how these will be handled. You might require additional identity documentation that would be hard for a criminal to falsify or some other action. Another group might include one instance in every 20 cases. A less burdensome treatment can be used here – like a one-time-passcode (OTP) sent to a confirmed mobile number. Any cases that remain unverified might then be asked for the same verification you used on the high-risk group. DON’T: Rely on a single analytical score threshold or risk indicator to create one giant pile of work that has to be sorted out manually. This approach usually results in a poor experience for a large number of customers, and a strong possibility that the next steps are not aligned to the level of risk. DO: Reserve manual review for situations where the reviewer can bring some new information or knowledge to the cases they review. DON’T: Use the same underlying data that generated the analytics as the basis of a review. Consider two simplistic cases that use a new address with no past association to the individual. In one case, there are several other people with different surnames that have recently been using the same address. In the other, there are only two, and they share the same surname. In the best possible case, the reviewer recognizes how the other information affects the risk, and they duplicate what the analytics have already done – flagging the first application as suspicious. In other cases, connections will be missed, resulting in a costly mistake. In real situations, automated reviews are able to compare each piece of information to thousands of others, making it more likely that second-guessing the analytics using the same data will be problematic. DO: Focus your most experienced and talented reviewers on creating fraud strategies. The best way to use their time and skill is to create a cycle where risk groups are defined (using analytics), a verification treatment is prescribed and used consistently, and the results are measured. With this approach, the outcome of every case is the result of deliberate action. When fraud occurs, it’s either because the case was miscategorized and received treatment that was too easy to discourage the criminal—or it was categorized correctly and the treatment wasn’t challenging enough. Gaining Value While there is a middle ground where manual review and skill can be a force-multiplier for strong analytics, my sense is that many organizations aren’t getting the best value from their most talented fraud practitioners. To improve this, businesses can start by understanding how analytics can help group customers based on levels of risk—not just one group but a few—where the number of good vs. fraudulent cases are understood. Decide how you want to handle each of those groups and reserve challenging treatments for the riskiest groups while applying easier treatments when the number of good customers per fraud attempt is very high. Set up a consistent waterfall process where customers either successfully verify, cascade to a more challenging treatment, or abandon the process. Focus your manual efforts on monitoring the process you’ve put in place. Start collecting data that shows you how both good and bad cases flow through the process. Know what types of challenges the bad guys are outsmarting so you can route them to challenges that they won’t beat so easily. Most importantly, have a plan and be consistent. Be sure to keep an eye out for a new post where we’ll talk about how this analytical approach can also help you grow your business. Contact us

If it looks like a bank and acts like a bank, there’s a good chance the company behind that financial services transaction may not actually be a bank – but a fintech. Born out of Silicon Valley, New York and tech hubs in between, fintechs have been categorically unfettered from regulation and driven by a focus on customer acquisition and revenue growth. Today, the fintech market represents hundreds of billions of dollars globally and has been disrupting financial services with the goal of delightful customer experiences and democratizing access to credit and banking. Their success has led many fintechs to update their strategy and growth targets and set their sites outside of core banking to other sectors including payments, alternative lending, insurance, capital markets, personal wealth management, alternative lending and others. Depending on the strategy, many are seeking a bank charter, or a partnership with a chartered financial institution to accomplish their new growth goals. Meanwhile, all this disruption has caught the attention of banks and credit unions who are keen to work with these marketplace lenders to grow deposits and increase fee-revenue streams. Historically, obtaining a bank charter was an onerous process, which led many fintechs to actively seek out partnerships with financial institutions in order to leverage their chartered status without the regulatory hurdles of becoming a bank. In fact, fintech and FI partnerships have boomed in the last few years, growing more than five times over the past decade. Gone are the days of the zero-sum game that benefits solely the bank or the fintech. Today, there are more than 30 partner banks representing hundreds of fintech relationships and financial services. These partnerships vary in size and scope from household names like Goldman Sachs, which powers the Apple credit card, to Hatch Bank, which has $68 million in assets and started with a single fintech partner, HM Bradley.[1] But which scenario is right for your fintech? Much of that depends on which markets and lines of business round out your growth strategy and revenue goals. Regardless of what framework you determine is right for your fintech, you need to work with partners who have access to the freshest data and models and a firm handle on the regulatory and compliance landscape. Experian can help you navigate the fintech regulatory environment and think through if partnering with a bank or seeking your own fintech charter is the best match for your growth plan. In the meantime, check out this new eBook for more information on the bank charter process and benefits, fintech-FI partnerships and the implications of the Office of the Comptroller of the Currency (OCC) new fintech charter. Read now Explore Fintech solutions [1] https://a16z.com/2020/06/11/the-partner-bank-boom/

For credit unions, having the right income and employment verification tools in place helps to create an application process that is easy and low friction for both new and existing members. Digital first is member first The digital evolution created an expectation for online experiences that are simple, fast, and convenient. Attracting and building trusted, loyal relationships and paving the way for new revenue-generating opportunities now hinges on a lender's ability to provide experiences that meet those expectations. At the same time, market volatility and economic uncertainty are driving catalysts behind the need for credit unions to gain a more holistic view of a member’s financial stability. To gain a competitive advantage in today’s lending environment, credit unions need income and employment verification solutions that balance two often polarizing business drivers: member experience and risk management. While verified income and employment data is key to understanding stability, it’s equally important to streamline the verification process and make it as frictionless as possible for borrowers. With these things in mind, here are three considerations to help credit unions ensure their income and employment verification process creates a favorable member experience. The more payroll records, the better Eliminate friction for members by tapping into a network of millions of unique employer payroll records. Gaining instant access into a database of this scale helps enable decisions in real-time, eliminates the cost and complexity of many existing verification processes, and allows members to skip cumbersome steps like producing paystubs. Create a process with high configuration and flexibility Verification is not a one-size-fits-all process. In some cases, it might be advantageous to tailor a verification process. Make sure your program is flexible, scalable and highly configurable to meet your evolving business needs. It should also have seamless integration options to plug and play into your current operations with ease. The details are in the data When it comes to income and employment verification, make sure that you are leveraging the most comprehensive source of consumer information. It’s important that your program is powered by quality data from a wealth of datasets that extend beyond traditional commercial businesses to ensure you are getting the most comprehensive view. Additionally, look to leverage a network of exclusive employer payroll records. With both assets, make sure you understand how frequently the data is refreshed to be certain your decisioning process is using the freshest and highest-quality data possible. Implementing the right solution By including a real-time income and employment verification solution in your credit union’s application process, you can improve the member experience, minimize cost and risk, and make better and faster decisions. To learn more about Experian’s income and employment verification solutions, or for a complimentary demo, feel free to contact an expert today. Learn more Contact us

Earlier this year, we shared our predictions for five fraud threats facing businesses in 2021. Now that we’ve reached the midpoint of the year and economic recovery is underway, we’re taking another look at how these threats can impact businesses and consumers. Putting a Face to Frankenstein IDs: Synthetic identity fraudsters will attempt to bypass fraud detection methods by using AI to combine facial characteristics from different people to form a new identity. Overexposure: As many as 80% of SSNs may have been exposed on the dark web, creating opportunities for account application fraud. The Heist: Surges in data breaches, advances in automation, expanded online banking services and vulnerabilities exposed from social engineering mistakes have lead to rises in account takeover fraud. Overstimulated: Opportunistic fraudsters may take advantage of ongoing relief payments by using stolen data from consumers. Behind the Times: Businesses with lackluster fraud prevention tools and insufficient online security technology will likely experience more attacks and suffer larger losses. To learn more about upcoming fraud threats and how to protect your business, download our new infographic and check out Experian’s fraud prevention solutions. Download infographic Request a call

As stimulus-generated fraud wanes, we anticipate a return of more traditional forms of fraud, including account opening fraud. As businesses embrace the digital evolution and look ahead to responsible growth, it’s important to balance the customer experience with the risks associated with account opening fraud. Preventing account opening fraud requires a layered fraud and identity management strategy that allows you to approve good customers while keeping criminals out. With the right tools in place, you can optimize the customer experience while still keeping risk low. Download infographic Review your fraud strategy

Experian’s Q1 2021 Automotive Market Trends Review revealed that some of the once-consistent new registration generational trends have reversed.

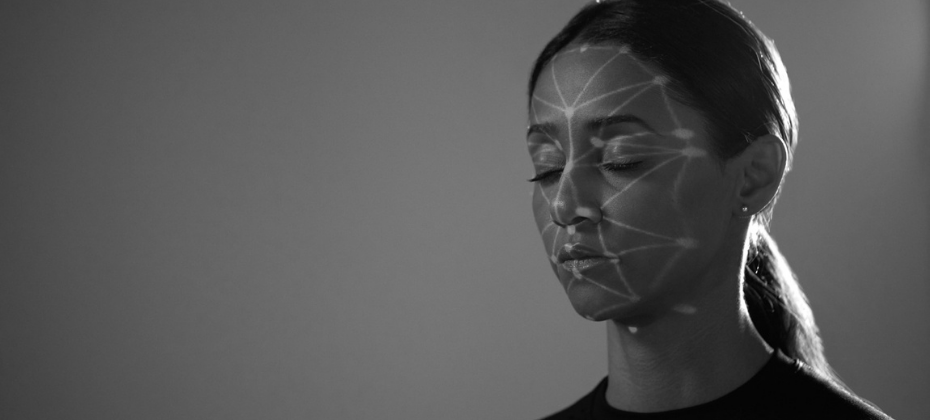

Over the past year and a half, the development of digital identity has shifted the ways businesses interact with consumers. Companies across every industry have incorporated digital services, biometrics, and other verification tools to enhance the consumer experience without increasing risk. Changing consumer expectations A digital identity strategy is no longer a nice-to-have, it’s table stakes. Consumers expect to be recognized across platforms and have a seamless experience every time. 89% of consumers use mobile banking 80% of companies now have a customer recognition strategy in place 55% of banking customers say they plan to visit the bank branch less often moving forward Businesses are responding to these changing expectations while working to grow during the economic recovery – trying to balance consumer experience with risk appetite and bottom-line goals. The present state of digital identity Digital identity strategies require both standardization and interoperability. The first provides the ability to consistently capture data and characteristics that can be used to recognize a specific individual. The second allows businesses to resolve an identity to a specific person – recognizing a phone number, user ID and password, or a device – and use that information to determine if the user of the identity is in fact the identity owner. There are some roadblocks on the road to a seamless digital identity strategy. Issues include a lack of consumer trust and an ambiguous regulatory landscape – creating friction on both ends of the equation. Recipe for success To succeed, businesses need a framework that can reliably use different combinations of physical and digital identity data to determine that the person behind the identity is a known, verified, and unique individual. A one-size-fits-all solution doesn’t exist. However, a layered approach allows businesses to modernize identity, providing the services consumers want and expect while remaining agile in an ever-changing environment. In our newest white paper, developed in partnership with One World Identity, we explore the obstacles hindering digital identity management, and the best way to build a layered solution that is flexible, trustworthy, and inclusive. To learn more, download our “Capturing the Digital Evolution Through a Layered Approach” white paper. Download white paper

The AutoCheck® Elite program enables auto dealerships to better understand the vehicles in their market. And, right now, making strategic decisions about stocking the right inventory and marketing to the right consumers has never been more important.

In the Q1 2021 Market Trends Review, we explore the average age myth and highlight other ways to inform aftermarket strategy.

Premier Awards Program Recognizes Breakthrough Financial Technology Products and Companies Experian’s Ascend Intelligence Services was selected as a winner of the “Consumer Lending Innovation Award” category in the fifth annual Fintech Breakthrough Awards conducted by Fintech Breakthrough, an independent market intelligence organization that recognizes the top companies, technologies and products in the global fintech market today. The Fintech Breakthrough Awards is the premier awards program founded to recognize the fintech innovators, leaders and visionaries from around the world in a range of categories, including digital banking, personal finance, lending, payments, investments, RegTech, InsurTech and many more. The 2021 Fintech Breakthrough Awards attracted more than 3,850 nominations from across the globe. One of the latest developments on Experian's trusted, award-winning Ascend platform, Ascend Intelligence Services empowers financial services firms with Experian’s revolutionary managed analytics solutions and services, delivered on a modern-tech AI platform. Ascend Intelligence Services includes rapid model development, seamless deployment, optimized decision strategies, ongoing performance monitoring and continuous retraining. The technology-enabled service uses a secure cloud-based AI platform to harness the power of machine learning, and deliver unique capabilities covering the entire credit lifecycle, through an easy-to-use web portal. “To stay ahead of the latest economic conditions, fintechs need high-quality analytical models running on large and varied data sets that empower them to act quickly and decisively. The breakthrough Ascend Intelligence Services platform answers this immediate market need,” said James Johnson, Managing Director, Fintech Breakthrough. “Congratulations to Experian and the Ascend team on winning our ‘Consumer Lending Innovation Award’ for 2021 with this game-changing solution.” “Data scientists are spending too much time on manual, repetitive and low value-add tasks, and organizations cannot afford to do this is in a state of constant change,” said Srikanth Geedipalli, Experian’s SVP Global Analytics/AI Products. “While building and deploying high-quality analytical models can be time-consuming and expensive, Ascend Intelligence Services streamlines this process by harnessing the power of machine learning and Experian’s rich data assets to drive better, faster and smarter decisions. We have been able to deliver analytical solutions to clients up to 4X faster, significantly improving decision automation rates and increasing approval rates by double digits. We are proud that Ascend Intelligence Services is being recognized as a breakthrough solution in the 2021 Fintech Breakthrough Awards program,” he said. Ascend Intelligence Services is comprised of four modules: Ascend Intelligence Services Challenger™ is a powerful, dynamic and collaborative model development service that enables Experian to rapidly build a model and quantify the benefit to business. Businesses can review, comment on and approve the model, all from within the web portal, while it’s being built. The resulting score is available for testing through an API endpoint and can be deployed in production with a few easy steps. Reports are customizable, downloadable and regulatory compliant. Ascend Intelligence Services Pulse™ is a proactive model monitoring and validation service, which aids companies in monitoring the health of models that drive their business decisions. Pulse, provides convenient dashboards that include a model health index, performance summary, stress-testing results, model risk management reporting, model health alerts and more. Additionally, Pulse automatically builds challengers for champion models, providing an estimated performance lift and financial benefit. Ascend Intelligence Services Strategy Advance™ is a powerful business strategy development service, enabling clients to make optimal lending decisions on their applicants. Strategy Advance uses Experian’s powerful optimization engine to build the right credit policy for clients, including sophisticated decision rules, model overlays and client specified knock-out rules. The resulting decision is available for testing through an API endpoint and can be deployed in production with a few easy steps. Ascend Intelligence Services Limit™ is a credit limit optimization service, enabling clients to make the right credit limit decisions at account origination and during account management. Limit uses Experian’s data, predictive risk and balance models and our powerful optimization engine to design the right credit limit strategy that maximizes product usage, while keeping losses low. The limit decision is available for testing through an API endpoint and can be deployed in production with a few easy steps. To learn more about how Ascend Intelligence Services can support your business, please explore our solutions page. Learn more For a list of all award winners selected for the Fintech Breakthrough Awards, read the full press release here.

The pandemic changed nearly everything – and consumer credit is no exception. Data, analytics, and credit risk decisioning are gaining an even more significant role as we grow closer to the end of the global crisis. Consumers face uneven roads to recovery, and while some are ready to spend again, others are still dealing with pandemic-related financial stress. We surveyed nearly 9,000 consumers and 2,700 businesses worldwide about how consumers are stabilizing their finances and businesses are returning to growth for our new Global Decisioning Report. In this report, we dive into: Key business priorities in 2021 Financial concerns for consumers How to navigate an uneven recovery Business priorities for the year ahead The importance of the online experience As we begin to near the end of the pandemic, businesses need to prioritize technology that enables a responsive, flexible, efficient and confident approach. This can be done by leveraging advanced data and analytics and integrating machine learning tools into model development. By investing in the right credit risk decisioning tools now, you can help ensure your future. Download the report