Data & Analytics

In Q3 2021, the average new vehicle loan amount increased 8.5% year-over-year, while the average used vehicle loan jumped more than 20% year-over year.

Global Insights Report: What Increasing Expectations of the Digital Customer Experience Mean for Your Business and Technology Investment

Data & AnalyticsDownload the new global insights report report to learn about consumer desires and business behaviors as we move further through the digital evolution.

Chatbots, reduction of manual processes and explainability were all hot topics in a recent discussion between two leading data leaders.

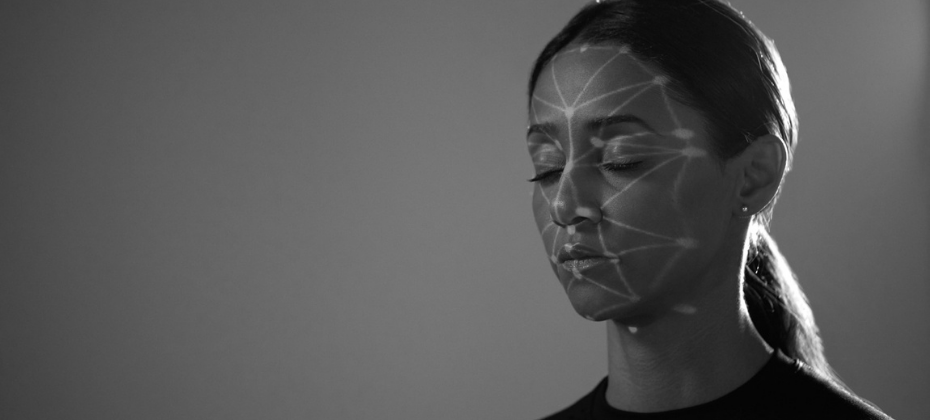

Dive into the ways artificial intelligence and digital identity interact and the benefits a clear identity strategy can have for the entire user journey.

Podcast: Advanced Analytics, Artificial Intelligence and Machine Learning in Lending

Data & AnalyticsShri Santhanam, Executive VP and GM of Experian's Global Analytics and Artificial Intelligence talks advanced analytics and AI in lending in recent podcast.

Despite used vehicle prices rising, loan-to-value (LTVs) ratios are dropping. Ultimately, lower LTVs are a positive trend for consumers because it puts them into positive equity on their vehicle faster.

Experian has made the IDC 2021 Fintech Rankings Top 100, highlighting the best global providers of financial technology. Read more!

Incorporating artificial intelligence and machine learning into your business strategy can improve decisioning and reduce risk. Read more.

The automotive finance market is beginning to level out to pre-pandemic trends in Q2 2021.

Learn how to maximize your collections efforts while reducing costs, avoiding reputational damage and fines, and improving overall engagement.

Experian discussed the benefits of FCRA data and ways this data can ease credit access for “invisible” consumers in a recent webinar hosted by AFSA.

We're considering the pros and cons of manual fraud reviews, and the benefits of applying analytics to your fraud review process.

Now that we’ve reached the midpoint of the year and economic recovery is underway, we’re taking a look at fraud threats can impact businesses and consumers.

New technologies like artificial intelligence and advanced analytics are changing the prescreen landscape for financial institutions as never before.

In our newest white paper, we explore the obstacles hindering digital identity management, and the best way to build a layered identity solution.