Fraud & Identity Management

There’s a common saying in the fraud prevention industry: where there’s opportunity, fraudsters are quick to follow. Recent advances in technology are providing ample new opportunities for cybercriminals to exploit. One of the most prevalent techniques being observed today is password spraying. From email to financial and health records, consumers and businesses are being impacted by this pervasive form of fraud. Password spraying attacks often fly under the radar of traditional security measures, presenting a unique and growing threat to businesses and individuals. What is password spraying? Also known as credential guessing, password spraying involves an attacker applying a list of commonly used passwords against a list of accounts in order to guess the correct password. When password spraying first emerged, an individual might hand key passwords to try to gain access to a user’s account or a business’s management system. Credential stuffing is a similar type of fraud attack in which an attacker gains access to a victim’s credentials in one system (e.g., their email, etc.) and then attempts to apply those known credentials via a script/bot to a large number of sites in order to gain access to other sites where the victim might be using the same credentials. Both are brute-force attack vectors that eventually result in account takeover (ATO), compromising sensitive data that is subsequently used to scam, blackmail, or defraud the victim. As password spraying and other types of fraud evolved, fraud rings would leverage “click farms” or “fraud farms” where hundreds of workers would leverage mobile devices or laptops to try different passwords in order to perpetrate fraud attacks on a larger scale. As technology has advanced, bot attacks fueled by generative AI (Gen AI) have taken the place of humans in the fraud ring. Now, instead of hand-keying passwords into systems, workers at fraud farms are able to deploy hundreds or thousands of bots that can work exponentially faster. The rise and evolution of bots Bots are not necessarily new to the digital experience — think of the chatbot on a company’s support page that helps you find an answer more quickly. These automated software applications carry out repetitive instructions mimicking human behavior. While they can be helpful, they can also be leveraged by fraudsters, to automate fraud on a brute-force attack, often going undetected resulting in substantial losses. Generation 4 bots are the latest evolution of these malicious programs, and they’re notoriously hard to detect. Because of their slow, methodical, and deliberate human-like behavior, they easily bypass network-level controls such as firewalls and popular network-layer security. Stopping Gen4 bots For any company with a digital presence or that leverages digital networks as part of doing business, the threat from Gen AI enabled fraud is paramount. The traditional stack for fighting fraud including firewalls, CAPTCHA and block lists are not enough in the face of Gen4 bots. Companies at the forefront of fighting fraud are leveraging behavioral analytics to identify and mitigate Gen AI-powered fraud. And many have turned to industry leader, Neuro ID, which is now part of Experian. Watch our on-demand webinar: The fraud bot future-shock: How to spot & stop next-gen attacks Behavioral analytics is a key component of passive and continuous authentication and has become table stakes in the fraud prevention space. By measuring how a user interacts with a form field (e.g., a website, mobile app, etc.) our behavioral analytics solutions can determine if the user is: a potential fraudster, a bot, or a genuine user familiar with the PII entered. Because it’s available at any digital engagement, behavioral data is often the most consistent signal available throughout the customer lifecycle and across geographies. It allows risky users to be rejected or put through more rigorous authentication, while trustworthy users get a better experience, protecting businesses and consumers from Gen AI-enabled fraud. As cyber threats evolve, so must our defenses. Password spraying exemplifies the sophisticated methods and technologies attackers now employ to scale their fraud efforts and gain access to sensitive information. To fight next-generation fraud, organizations must employ next-generation technologies and techniques to better defend themselves against this and other types of cyberattacks. Experian’s approach embodies a paradigm shift where fraud detection increases efficiency and accuracy without sacrificing customer experience. We can help protect your company from bot attacks, fraudulent accounts and other malicious attempts to access your sensitive data. Learn more about behavioral analytics and our other fraud prevention solutions. Learn more

Dormant fraud, sleeper fraud, trojan horse fraud . . . whatever you call it, it’s an especially insidious form of account takeover fraud (ATO) that fraud teams often can’t detect until it’s too late. Fraudsters create accounts with stolen credentials or gain access to existing ones, onboard under the fake identity, then lie low, waiting for an opportunity to attack. It takes a strategic approach to defeat the enemy from within, and fraudsters assume you won’t have the tools in place to even know where to start. Dormant fraud uncovered: A case study NeuroID, a part of Experian, has seen the dangers of dormant fraud play out in real time. As a new customer to NeuroID, this payment processor wanted to backtest their user base for potential signs of fraud. Upon analyzing their customer base’s onboarding behavioral data, we discovered more than 100K accounts were likely to be dormant fraud. The payment processor hadn’t considered these accounts suspicious and didn’t see any risk in letting them remain active, despite the fact that none of them had completed a transaction since onboarding. Why did we flag these as risky? Low familiarity: Our testing revealed behavioral red flags, such as copying and pasting into fields or constant tab switching. These are high indicators that the applicant is applying with personally identifiable information (PII) that isn’t their own. Fraud clusters: Many of these accounts used the same web browser, device, and IP address during sign-up, suggesting that one fraudster was signing up for multiple accounts. We found hundreds of clusters like these, many with 50 or more accounts belonging to the same device and IP address within our customer’s user base. It was clear that this payment processor’s fraud stack had gaps that left them vulnerable. These dormant accounts could have caused significant damage once mobilized: receiving or transferring stolen funds, misrepresenting their financial position, or building toward a bust-out. Dormant fraud thrives in the shadows beyond onboarding. These fraudsters keep accounts “dormant” until they’re long past onboarding detection measures. And once they’re in, they can often easily transition to a higher-risk account — after all, they’ve already confirmed they’re trustworthy. This type of attack can involve fraudulent accounts remaining inactive for months, allowing them to bypass standard fraud detection methods that focus on immediate indicators. Dormant fraud gets even more dangerous when a hijacked account has built trust just by existing. For example, some banks provide a higher credit line just for current customers, no matter their activities to date. The more accounts an identity has in good standing, the greater the chance that they’ll be mistaken for a good customer and given even more opportunities to commit higher-level fraud. This is why we often talk to our customers about the idea of progressive onboarding as a way to overcome both dormant fraud risks and the onboarding friction caused by asking for too much information, too soon. Progressive onboarding, dormant fraud, and the friction balance Progressive onboarding shifts from the one-size-fits-all model by gathering only truly essential information initially and asking for more as customers engage more. This is a direct counterbalance to the approach that sometimes turns customers off by asking for too much too soon, and adding too much friction at initial onboarding. It also helps ensure ongoing checks that fight dormant fraud. We’ve seen this approach (already growing popular in payment processing) be especially useful in every type of financial business. Here’s how it works: A prospect visits your site to explore options. They may just want to understand fees and get a feel for your offerings. At this stage, you might ask for minimal information — just a name and email — without requiring a full fraud check or credit score. It’s a low commitment ask that keeps things simple for casual prospects who are just browsing, while also keeping your costs low so you don’t spend a full fraud check on an uncommitted visitor. As the prospect becomes a true customer and begins making small transactions, say a $50 transfer, you request additional details like their date of birth, physical address, or phone number. This minor step-up in information allows for a basic behavioral analytics fraud check while maintaining a low barrier of time and PII-requested for a low-risk activity. With each new level of engagement and transaction value, the information requested increases accordingly. If the customer wants to transfer larger amounts, like $5,000, they’ll understand the need to provide more details — it aligns with the idea of a privacy trade-off, where the customer’s willingness to share information grows as their trust and need for services increase. Meanwhile, your business allocates resources to those who are fully engaged, rather than to one-time visitors or casual sign-ups, and keeps an eye on dormant fraudsters who might have expected no barrier to additional transactions. Progressive onboarding is not just an effective approach for dormant fraud and onboarding friction, but also in fighting fraudsters who sneak in through unseen gaps. In another case, we worked with a consumer finance platform to help identify gaps in their fraud stack. In one attack, fraudsters probed until they found the product with the easiest barrier of entry: once inside they went on to immediately commit a full-force bot attack on higher value returns. The attack wasn’t based on dormancy, but on complacency. The fraudsters assumed this consumer finance platform wouldn’t realize that a low controls onboarding for one solution could lead to ease of access to much more. And they were right. After closing that vulnerability, we helped this customer work to create progressive onboarding that includes behavior-based fraud controls for every single user, including those already with accounts, who had built that assumed trust, and for low-risk entry-points. This weeded out any dormant fraudsters already onboarded who were trying to take advantage of that trust, as they had to go through behavioral analytics and other new controls based on the risk-level of the product. Behavioral analytics gives you confidence that every customer is trustworthy, from the moment they enter the front door to even after they’ve kicked off their shoes to stay a while. Behavioral analytics shines a light on shadowy corners Behavioral analytics are proven beyond just onboarding — within any part of a user interaction, our signals detect low familiarity, high-risk behavior and likely fraud clusters. In our experience, building a progressive onboarding approach with just these two signal points alone would provide significant results — and would help stop sophisticated fraudsters from perpetrating dormant fraud, including large-scale bust outs. Want to find out how progressive onboarding might work for you? Contact us for a free demo and deep dive into how behavioral analytics can help throughout your user journey. Contact us for a free demo

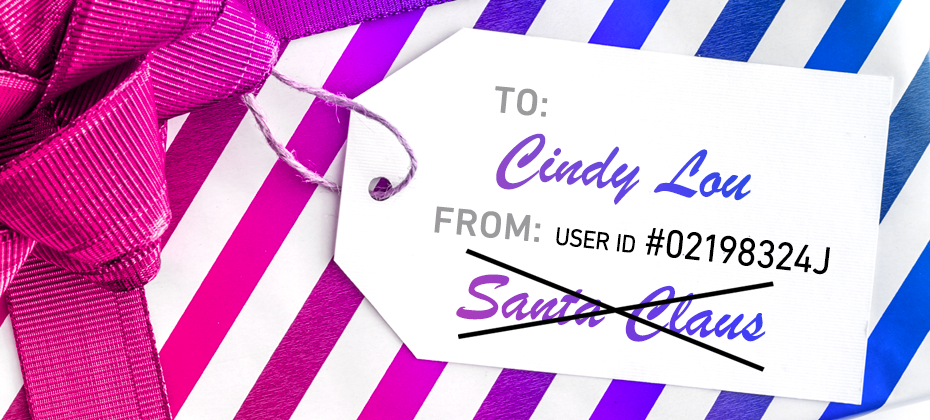

A tale of synthetic ID fraud Synthetic ID fraud is an increasing issue and affects everyone, including high-profile individuals. A notable case from Ohio involved Warren Hayes, who managed to get an official ID card in the name of “Santa Claus” from the Ohio Bureau of Motor Vehicles. He also registered a vehicle, opened a bank account, and secured an AAA membership under this name, listing his address as 1 Noel Drive, North Pole, USA. This elaborate ruse unraveled after Hayes, disguised as Santa, got into a minor car accident. When the police requested identification, Hayes presented his Santa Claus ID. He was subsequently charged under an Ohio law prohibiting the use of fictitious names. However, the court—presided over by Judge Thomas Gysegem—dismissed the charge, arguing that because Hayes had used the ID for over 20 years, "Santa Claus" was effectively a "real person" in the eyes of the law. The judge’s ruling raised eyebrows and left one glaring question unanswered: how could official documents in such a blatantly fictitious name go undetected for two decades? From Santa Claus to synthetic IDs: the modern-day threat The Hayes case might sound like a holiday comedy, but it highlights a significant issue that organizations face today: synthetic identity fraud. Unlike traditional identity theft, synthetic ID fraud does not rely on stealing an existing identity. Instead, fraudsters combine real and fictitious details to create a new “person.” Think of it as an elaborate game of make-believe, where the stakes are millions of dollars. These synthetic identities can remain under the radar for years, building credit profiles, obtaining loans, and committing large-scale fraud before detection. Just as Hayes tricked the Bureau of Motor Vehicles, fraudsters exploit weak verification processes to pass as legitimate individuals. According to KPMG, synthetic identity fraud bears a staggering $6 billion cost to banks.To perpetrate the crime, malicious actors leverage a combination of real and fake information to fabricate a synthetic identity, also known as a “Frankenstein ID.” The financial industry classifies various types of synthetic identity fraud. Manipulated Synthetics – A real person’s data is modified to create variations of that identity. Frankenstein Synthetics – The data represents a combination of multiple real people. Manufactured Synthetics – The identity is completely synthetic. How organizations can combat synthetic ID fraud A multifaceted approach to detecting synthetic identities that integrates advanced technologies can form the foundation of a sound fraud prevention strategy: Advanced identity verification tools: Use AI-powered tools that cross-check identity attributes across multiple data points to flag inconsistencies. Behavioral analytics: Monitor user behaviors to detect anomalies that may indicate synthetic identities. For instance, a newly created account applying for a large loan with perfect credit is a red flag. Digital identity verification: Implement digital onboarding processes that include online identity verification with real-time document verification. Users can upload government-issued IDs and take selfies to confirm their identity. Collaboration and data sharing: Organizations can share insights about suspected synthetic identities to prevent fraudsters from exploiting gaps between industries. Ongoing employee training: Ensure frontline staff can identify suspicious applications and escalate potential fraud cases. Regulatory support: Governments and regulators can help by standardizing ID issuance processes and requiring more stringent checks. Closing thoughts The tale of Santa Claus’ stolen identity may be entertaining, but it underscores the need for vigilance against synthetic ID fraud. As we move into an increasingly digital age, organizations must stay ahead of fraudsters by leveraging technology, training, and collaboration. Because while the idea of Spiderman or Catwoman walking into your branch may seem amusing, the financial and reputational cost of synthetic ID fraud is no laughing matter. Learn more

The digital domain is rife with opportunities, but it also brings substantial risks, especially for organizations. Among the innovative tools that have risen to prominence for fraud detection and online security is browser fingerprinting. Whether you're looking to minimize security gaps or bolster your fraud prevention strategy, understanding how this technology works can provide a significant advantage in today’s ever-evolving fraud and identity landscape. This article explores the concept, functionality, and applications of browser fingerprinting while also examining its benefits and relevance for organizations. How does browser fingerprinting work? Browser fingerprinting is a powerful technology designed to collect unique identifying information about a user’s web browser and device. By compiling data points such as browser type, operating system, time zone, and installed plugins, browser fingerprinting creates a distinct profile — or "fingerprint"— that allows websites to recognize returning users without relying on cookies. Here’s a breakdown of its key steps: Data collection: When a user visits a website, their browser sends information, such as user-agent strings or metadata, to the website's servers. This data provides insights about their browser, device, and system. Fingerprint creation: The collected information is processed to generate a unique ID or fingerprint, representing the user's specific configuration. Tracking and analyzing: These fingerprints enable websites to track and analyze user behavior, detect anomalies, and identify users without relying on traditional tracking mechanisms like cookies. For organizations, employing technology that leverages such fingerprints adds an additional layer to identity verification, detecting discrepancies that may indicate fraud attempts. What are the different techniques? Not all browser fingerprinting methods are identical; varying approaches offer different strengths. The most common techniques used today include: Canvas fingerprinting: This method utilizes the "Canvas" element in HTML5. When a website sends a command to draw a hidden image on a user's device, the way the image is rendered reveals unique characteristics about the device's graphics hardware and software. Font fingerprinting: Font fingerprinting involves analyzing the fonts installed on a user's system. Since computers and browsers render text in slightly different ways based on their configurations, the resulting variations aid in identifying users. Plugin enumeration: Browsers and devices often come equipped with plugins or extensions like Flash or Java. Analyzing which plugins are installed, their versions, and their order helps websites build unique fingerprints. What are the benefits of browser fingerprinting? For organizations, browser fingerprinting is not just a technical marvel — it’s a strategic asset. Benefits include: Enhanced fraud detection: Browser fingerprinting detects inconsistencies within user accounts, flagging unauthorized logins, synthetic identity fraud, or account takeover fraud without introducing significant friction for legitimate users. By identifying patterns that deviate from the norm, organizations can better prepare for malicious activities. Learn more about addressing account takeover fraud. Supports multi-layered security: A single security measure often isn't enough to combat advanced fraudulent schemes. Browser fingerprinting pairs seamlessly with other fraud management tools, such as behavioral analytics and risk-based authentication, to provide robust security. See how behavioral analytics can help organizations spot and stop next-generation fraud bots. Seamless user experience: Unlike cookies or authentication codes, browser fingerprinting operates passively in the background. Users remain unaware of the process, ensuring their experience is unaffected while still maintaining security. Level up with Experian's fraud prevention tools Browser fingerprinting offers organizations a game-changing tool to secure online interactions. However, given the growing complexity of fraud threats, organizations will need additional layers of insights and protection. Experian offers integrated, AI-driven fraud prevention solutions tailor-made to tackle challenges in the digital space. By leveraging advanced technologies like browser fingerprinting alongside Experian’s solutions, organizations can safeguard their operations and uphold customer trust while maintaining a frictionless user experience. Learn more about our fraud prevention solutions This article includes content created by an AI language model and is intended to provide general information.

We are squarely in the holiday shopping season. From the flurry of promotional emails to the endless shopping lists, there are many to-dos and even more opportunities for financial institutions at this time of year. The holiday shopping season is not just a peak period for consumer spending; it’s also a critical time for financial institutions to strategize, innovate, and drive value. According to the National Retail Federation, U.S. holiday retail sales are projected to approach $1 trillion in 2024, , and with an ever-evolving consumer behavior landscape, financial institutions need actionable strategies to stand out, secure loyalty, and drive growth during this period of heightened spending. Download our playbook: "How to prepare for the Holiday Shopping Season" Here’s how financial institutions can capitalize on the holiday shopping season, including key insights, actionable strategies, and data-backed trends. 1. Understand the holiday shopping landscape Key stats to consider: U.S. consumers spent $210 billion online during the 2022 holiday season, according to Adobe Analytics, marking a 3.5% increase from 2021. Experian data reveals that 31% of all holiday purchases in 2022 occurred in October, highlighting the extended shopping season. Cyber Week accounted for just 8% of total holiday spending, according to Experian’s Holiday Spending Trends and Insights Report, emphasizing the importance of a broad, season-long strategy. What this means for financial institutions: Timing is crucial. Your campaigns are already underway if you get an early start, and it’s critical to sustain them through December. Focus beyond Cyber Week. Develop long-term engagement strategies to capture spending throughout the season. 2. Leverage Gen Z’s growing spending power With an estimated $360 billion in disposable income, according to Bloomberg, Gen Z is a powerful force in the holiday market. This generation values personalized, seamless experiences and is highly active online. Strategies to capture Gen Z: Offer digital-first solutions that enhance the holiday shopping journey, such as interactive portals or AI-powered customer support. Provide loyalty incentives tailored to this demographic, like cash-back rewards or exclusive access to services. Learn more about Gen Z in our State of Gen Z Report. To learn more about all generations' projected consumer spending, read new insights from Experian here, including 45% of Gen X and 52% of Boomers expect their spending to remain consistent with last year. 3. Optimize pre-holiday strategies Portfolio Review: Assess consumer behavior trends and adjust risk models to align with changing economic conditions. Identify opportunities to engage dormant accounts or offer tailored credit lines to existing customers. Actionable tactics: Expand offerings. Position your products and services with promotional campaigns targeting high-value segments. Personalize experiences. Use advanced analytics to segment clients and craft offers that resonate with their holiday needs or anticipate their possible post-holiday needs. 4. Ensure top-of-mind awareness During the holiday shopping season, competition to be the “top of wallet” is fierce. Experian’s data shows that 58% of high spenders shop evenly across the season, while 31% of average spenders do most of their shopping in December. Strategies for success: Early engagement: Launch educational campaigns to empower credit education and identity protection during this period of increased transactions. Loyalty programs: Offer incentives, such as discounts or rewards, that encourage repeat engagement during the season. Omnichannel presence: Utilize digital, email, and event marketing to maintain visibility across platforms. 5. Combat fraud with multi-layered strategies The holiday shopping season sees an increase in fraud, with card testing being the number one attack vector in the U.S. according to Experian’s 2024 Identity and Fraud Study. Fraudulent activity such as identity theft and synthetic IDs can also escalate. Fight tomorrow’s fraud today: Identity verification: Use advanced fraud detection tools, like Experian’s Ascend Fraud Sandbox, to validate accounts in real-time. Monitor dormant accounts: Watch these accounts with caution and assess for potential fraud risk. Strengthen cybersecurity: Implement multi-layered strategies, including behavioral analytics and artificial intelligence (AI), to reduce vulnerabilities. 6. Post-holiday follow-up: retain and manage risk Once the holiday rush is over, the focus shifts to managing potential payment stress and fostering long-term relationships. Post-holiday strategies: Debt monitoring: Keep an eye on debt-to-income and debt-to-limit ratios to identify clients at risk of defaulting. Customer support: Offer tailored assistance programs for clients showing signs of financial stress, preserving goodwill and loyalty. Fraud checks: Watch for first-party fraud and unusual return patterns, which can spike in January. 7. Anticipate consumer trends in the New Year The aftermath of the holidays often reveals deeper insights into consumer health: Rising credit balances: January often sees an uptick in outstanding balances, highlighting the need for proactive credit management. Shifts in spending behavior: According to McKinsey, consumers are increasingly cautious post-holiday, favoring savings and value-based spending. What this means for financial institutions: Align with clients’ needs for financial flexibility. The holiday shopping season is a time that demands precise planning and execution. Financial institutions can maximize their impact during this critical period by starting early, leveraging advanced analytics, and maintaining a strong focus on fraud prevention. And remember, success in the holiday season extends beyond December. Building strong relationships and managing risk ensures a smooth transition into the new year, setting the stage for continued growth. Ready to optimize your strategy? Contact us for tailored recommendations during the holiday season and beyond. Download the Holiday Shopping Season Playbook

Despite being a decades-old technology, behavioral analytics is often still misunderstood. We’ve heard from fraud, identity, security, product, and risk professionals that exploring a behavior-based fraud solution brings up big questions, such as: What does behavioral analytics provide that I don’t get now? (Quick answer: a whole new signal and an earlier view of fraud) Why do I need to add even more data to my fraud stack? (Quick answer: it acts with your stack to add insights, not overload) How is this different from biometrics? (Quick answer: while biometrics track characteristics, behavioral analytics tracks distinct actions) These questions make sense — stopping fraud is complex, and, of course, you want to do your research to fully understand what ROI any tool will add. NeuroID, now part of Experian, is one of the only behavioral analytics-first businesses built specifically for stopping fraud. Our internal experts have been crafting behavioral-first solutions to detect everything from simple script fraud bots through to generative AI (genAI) attacks. We know how behavioral analytics works best within your fraud stack, and how to think strategically about using it to stop fraud rings, bot fraud, and other third-party fraud attacks. This primer will provide answers to the biggest questions we hear, so you can make the most informed decisions when exploring how our behavioral analytics solutions could work for you. Q1. What is behavioral analytics and how is it different from behavioral biometrics? A common mistake is to conflate behavioral analytics with behavioral biometrics. But biometrics rely on unique physical characteristics — like fingerprints or facial scans — used for automated recognition, such as unlocking your phone with Face ID. Biometrics connect a person’s data to their identity. But behavioral analytics? They don’t look at an identity. They look at behavior and predict risk. While biometrics track who a person is, behavioral analytics track what they do. For example, NeuroID’s behavioral analytics observes every time someone clicks in a box, edits a field, or hovers over a section. So, when a user’s actions suggest fraudulent intent, they can be directed to additional verification steps or fully denied. And if their actions suggest trustworthiness? They can be fast-tracked. Or, as a customer of ours put it: "Using NeuroID decisioning, we can confidently reject bad actors today who we used to take to step-up. We also have enough information on good applicants sooner, so we can fast-track them and say ‘go ahead and get your loan, we don’t need anything else from you.’ And customers really love that." - Mauro Jacome, Head of Data Science for Addi (read the full Addi case study here). The difference might seem subtle, but it’s important. New laws on biometrics have triggered profound implications for banks, businesses, and fraud prevention strategies. The laws introduce potential legal liabilities, increased compliance costs, and are part of a growing public backlash over privacy concerns. Behavioral signals, because they don’t tie behavior to identity, are often easier to introduce and don’t need the same level of regulatory scrutiny. The bottom line is that our behavioral analytics capabilities are unique from any other part of your fraud stack, full-stop. And it's because we don’t identify users, we identify intentions. Simply by tracking users’ behavior on your digital form, behavioral analytics powered by NeuroID tells you if a user is human or a bot; trustworthy or risky. It looks at each click, edit, keystroke, pause, and other tiny interactions to measure every users’ intention. By combining behavior with device and network intelligence, our solutions provide new visibility into fraudsters hiding behind perfect PII and suspicious devices. The result is reduced fraud costs, fewer API calls, and top-of-the-funnel fraud capture with no tuning or model integration on day one. With behavioral analytics, our customers can detect fraud attacks in minutes, instead of days. Our solutions have proven results of detecting up to 90% of fraud with 99% accuracy (or <1% false positive rate) with less than 3% of your population getting flagged. Q2. What does behavioral analytics provide that I don’t get now? Behavioral analytics provides a net-new signal that you can’t get from any other tools. One of our customers, Josh Eurom, Manager of Fraud for Aspiration Banking, described it this way: “You can quantify some things very easily: if bad domains are coming through you can identify and stop it. But if you see things look odd, yet you can’t set up controls, that’s where NeuroID behavioral analytics come in and captures the unseen fraud.” (read the full Aspiration story here) Adding yet another new technology with big promises may not feel urgent. But with genAI fueling synthetic identity fraud, next-gen fraud bots, and hyper-efficient fraud ring attacks, time is running out to modernize your stack. In addition, many fraud prevention tools today only focus on what PII is submitted — and PII is notoriously easy to fake. Only behavioral analytics looks at how the data is submitted. Behavioral analytics is a crucial signal for detecting even the most modern fraud techniques. Watch our webinar: The Fraud Bot Future-Shock: How to Spot and Stop Next-Gen Attacks Q3. Why do I need to add even more data to my fraud stack? Balancing fraud, friction, and financial impact has led to increasingly complex fraud stacks that often slow conversions and limit visibility. As fraudsters evolve, gaps grow between how quickly you can keep up with their new technology. Fraudsters have no budget constraints, compliance requirements, or approval processes holding them back from implementing new technology to attack your stack, so they have an inherent advantage. Many fraud teams we hear from are looking for ways to optimize their workflows without adding to the data noise, while balancing all the factors that a fraud stack influences beyond overall security (such as false positives and unnecessary friction). Behavioral analytics is a great way to work smarter with what you have. The signals add no friction to the onboarding process, are undetectable to your customers, and live on a pre-submit level, using data that is already captured by your existing application process. Without requiring any new inputs from your users or stepping into messy biometric legal gray areas, behavioral analytics aggregates, sorts, and reviews a broad range of cross-channel, historical, and current customer behaviors to develop clear, real-time portraits of transactional risks. By sitting top-of-funnel, behavioral analytics not only doesn’t add to the data noise, it actually clarifies the data you currently rely on by taking pressure off of your other tools. With these insights, you can make better fraud decisions, faster. Or, as Eurom put it: “Before NeuroID, we were not automatically denying applications. They were getting an IDV check and going into a manual review. But with NeuroID at the top of our funnel, we implemented automatic denial based on the risky signal, saving us additional API calls and reviews. And we’re capturing roughly four times more fraud. Having behavioral data to reinforce our decision-making is a relief.” The behavioral analytics difference Since the world has moved online, we’re missing the body language clues that used to tell us if someone was a fraudster. Behavioral analytics provides the digital body language differentiator. Behavioral cues — such as typing speed, hesitation, and mouse movements — highlight riskiness. The cause of that risk could be bots, stolen information, fraud rings, synthetic identities, or any combination of third-party fraud attack strategies. Behavioral analytics gives you insights to distinguish between genuine applicants and potentially fraudulent ones without disrupting your customer’s journey. By interpreting behavioral patterns at the very top of the onboarding funnel, behavior helps you proactively mitigate fraud, reduce false positives, and streamline onboarding, so you can lock out fraudsters and let in legitimate users. This is all from data you already capture, simply tracking interactions on your site. Stop fraud, faster: 5 simple uses where behavioral analytics shine While how you approach a behavioral analytics integration will vary based on numerous factors, here are some of the immediate, common use cases of behavioral analytics. Detecting fraud bots and fraud rings Behavioral analytics can identify fraud bots by their frameworks, such as Puppeter or Stealth, and through their behavioral patterns, so you can protect against even the most sophisticated fourth-generation bots. NeuroID provides holistic coverage for bot and fraud ring detection — passively and with no customer friction, often eliminating the need for CAPTCHA and reCAPTCHA. With this data alone, you could potentially blacklist suspected fraud bot and fraud ring attacks at the top of the fraud prevention funnel, avoiding extra API calls. Sussing out scams and coercions When users make account changes or transactions under coercion, they often show unfamiliarity with the destination account or shipping address entered. Our real-time assessment detects these risk indicators, including hesitancy, multiple corrections, and slow typing, alerting you in real-time to look closer. Stopping use of compromised cards and stolen IDs Traditional PII methods can fall short against today’s sophisticated synthetic identity fraud. Behavioral analytics uncovers synthetic identities by evaluating how PII is entered, instead of relying on PII itself (which is often corrupted). For example, our behavioral signals can assess users’ familiarity with the billing address they’re entering for a credit card or bank account. Genuine account holders will show strong familiarity, while signs of unfamiliarity are indicators of an account under attack. Detecting money mules Our behavioral analytics solutions track how familiar users are with the addresses they enter, conducting a real-time, sub-millisecond familiarity assessment. Risk markers such as hesitancy, multiple corrections, slow typing speed raise flags for further exploration. Stopping promotion and discount abuse Our behavioral analytics identifies risky versus trustworthy users in promo and discount fields. By assessing behavior, device, and network risk, we help you determine if your promotions attract more risky than trustworthy users, preventing fraudsters from abusing discounts. Learn more about our behavioral analytics solutions. Learn more Watch webinar

With cyber threats intensifying and data breaches rising, understanding how to respond to incidents is more important than ever. In this interview, Michael Bruemmer, Head of Global Data Breach Resolution at Experian, is joined by Matthew Meade, Chair of the Cybersecurity, Data Protection & Privacy Group at Eckert Seamans, to discuss the realities of data breach response. Their session, “Cyber Incident Response: A View from the Trenches,” brings insights from the field and offers a preview of Experian's 2025 Data Breach Industry Forecast, including the role of generative artificial intelligence (AI) in data breaches. From the surge in business email compromises (BEC) to the relentless threat of ransomware, Bruemmer and Meade dive into key issues facing organizations big and small today. Drawing from Experian's experience handling nearly 5,000 breaches this year, Bruemmer sheds light on effective response practices and reveals common pitfalls. Meade, who served as editor-in-chief for the Sedona Conference’s new Model Data Breach Notification Law, explains the implications of these regulatory updates for organizations and highlights how standardized notification practices can improve outcomes. Bruemmer and Meade’s insights offer a proactive guide to tackling tomorrow’s cyber threats, making it a must-listen for anyone aiming to stay one step ahead. Listen to the full interview for a valuable look at both the current landscape and what's next. Click here for more insight into safeguarding your organization from emerging cyber threats.

As online accounts become essential for activities ranging from shopping and social media to banking, "account farming" has emerged as a significant fraud risk. This practice involves creating fake or unauthorized accounts en masse, often for malicious purposes. Understanding how account farming works, why it’s done and how businesses can protect themselves is crucial for maintaining data integrity, safeguarding customer trust and protecting your bottom line. How does account farming work? Account farming is the process of creating and cultivating multiple user accounts, often using fake or stolen identities. These accounts may look like legitimate users, but they’re controlled by a single entity or organization, usually with fraudulent intent. Here’s a breakdown of the typical steps involved in account farming: Identity generation: Account farmers start by obtaining either fake or stolen personal information. They may buy these datasets on the dark web or scrape publicly available information to make each account seem legitimate. Account creation: Using bots or manual processes, fraudsters create numerous accounts on a platform. Often, they’ll employ automated tools to expedite this process, bypassing CAPTCHA or reCAPTCHA systems or using proxy servers to mask their IP addresses and avoid detection. Warm-up phase: After initial creation, account farmers often let the accounts sit for a while, engaging in limited, non-suspicious activity to avoid triggering security alerts. This “warming up” process helps the accounts seem more authentic. Activation for fraudulent activity: Once these accounts reach a level of credibility, they’re activated for the intended purpose. This might include spamming, fraud, phishing, fake reviews or promotional manipulation. Why is account farming done? There are several reasons account farming has become a widespread problem across different industries. Here are some common motivations: Monetary gain: Fraudsters use farmed accounts to commit fraudulent transactions, like applying for loans and credit products, accessing promotional incentives or exploiting referral programs. Spam and phishing: Fake accounts enable widespread spam campaigns or phishing attacks, compromising customer data and damaging brand reputation. Data theft: By creating and controlling multiple accounts, fraudsters may access sensitive data, leading to further exploitation or resale on the dark web. Manipulating metrics and market perception: Some industries use account farming to boost visibility and credibility falsely. For example, on social media, fake accounts can be used to inflate follower counts or engagement metrics. In e-commerce, fraudsters may create fake accounts to leave fake reviews or upvote products, falsely boosting perceived popularity and manipulating purchasing decisions. How does account farming lead to fraud risks? Account farming is a serious problem that can expose businesses and their customers to a variety of risks: Financial loss: Fake accounts created to exploit promotional offers or referral programs can cause victims to experience significant financial losses. Additionally, businesses can incur costs from chargebacks or fraudulent refunds triggered by these accounts. Compromised customer experience: Legitimate customers may suffer from poor experiences, such as spam messages, unsolicited emails or fraudulent interactions. This leads to diminished brand trust, which is costly to regain. Data breaches and compliance risks: Account farming often relies on stolen data, increasing the risk of data breaches. Businesses subject to regulations like GDPR or CCPA may face hefty fines if they fail to protect consumer information adequately. READ MORE: Our Data Breach Industry Forecast predicts what’s in store for the coming year. How can businesses protect themselves from account farming fraud? As account farming tactics evolve, businesses need a proactive and sophisticated approach to detect and prevent these fraudulent activities. Experian’s fraud risk management solutions provide multilayered and customizable solutions to help companies safeguard themselves against account farming and other types of fraud. Here’s how we can help: Identity verification solutions: Experian’s fraud risk and identity verification platform integrates multiple verification methods to confirm the authenticity of user identities. Through real-time data validation, businesses can verify the legitimacy of user information provided at the account creation stage, detecting and blocking fake identities early in the process. Its flexible architecture allows companies to adapt their identity verification process as new fraud patterns emerge, helping them stay one step ahead of account farmers. Behavioral analytics: One effective way to identify account farming is to analyze user behavior for patterns consistent with automated or scripted actions (AKA “bots”). Experian’s behavioral analytics solutions, powered by NeuroID, use advanced machine learning algorithms to identify unusual behavioral trends among accounts. By monitoring how users interact with a platform, we can detect patterns common in farmed accounts, like uniform interactions or repetitive actions that don’t align with human behavior. Device intelligence: To prevent account farming fraud, it’s essential to go beyond user data and examine the devices used to create and access accounts. Experian’s solutions combine device intelligence with identity verification to flag suspicious devices associated with multiple accounts. For example, account farmers often use virtual machines, proxies or emulators to create accounts without revealing their actual location or device details. By identifying and flagging these high-risk devices, we help prevent fraudulent accounts from slipping through the cracks. Velocity checks: Velocity checks are another way to block fraudulent account creation. By monitoring the frequency and speed at which new accounts are created from specific IP addresses or devices, Experian’s fraud prevention solutions can identify spikes indicative of account farming. These velocity checks work in real-time, enabling businesses to act immediately to block suspicious activity and minimize the risk of fake account creation. Continuous monitoring and risk scoring: Even after initial account creation, continuous monitoring of user activity helps to identify accounts that may have initially bypassed detection but later engage in suspicious behavior. Experian’s risk scoring system assigns a fraud risk score to each account based on its behavior over time, alerting businesses to potential threats before they escalate. Final thoughts: Staying ahead of account farming fraud Preventing account farming is about more than just blocking bots — it’s about safeguarding your business and its customers against fraud risk. By understanding the mechanics of account farming and using a multi-layered approach to fraud detection and identity verification, businesses can protect themselves effectively. Ready to take a proactive stance against account farming and other evolving fraud tactics? Explore our comprehensive solutions today. Learn More This article includes content created by an AI language model and is intended to provide general information.

The advent of artificial intelligence (AI) is significantly transforming the landscape of real estate fraud, enabling criminals to execute complex schemes like deed theft with greater ease. A notable case involves Spelling Manor, a $137.5 million mansion in Los Angeles, where the owner alleges they are entangled in deed fraud. Scammers reportedly filed fraudulent documents that have prevented the owner from selling the estate, thwarting offers from buyers, including former Google CEO Eric Schmidt. Understanding deed/title fraud Deed fraud, also known as title or property fraud, occurs when someone illegally transfers ownership of a property without the owner’s knowledge or consent. Typically, fraudsters create fake documents or forge the owner’s signature on a deed to make it look like the property has been legally transferred to them. Once the title is in their name, they may try to sell or mortgage the property, leaving the original owner unaware until it’s too late. How deed fraud works Identify a target: Fraudsters often look for properties that appear vulnerable, such as vacant land, unoccupied homes, or properties owned by elderly individuals who may not check their records frequently. Forge documentation: Using fake IDs and forged signatures, scammers create documents that appear to show a legitimate transfer of ownership. With modern technology, these documents can look highly convincing. Record the fake deed: Fraudsters then file these documents with the local county clerk or recorder’s office. This officially changes the ownership records, making it seem as if the scammer is the legitimate owner. Exploit the ownership: Once listed as the owner, the fraudster may sell the property to an unsuspecting buyer, take out loans against it, or even rent it out. The impact on victims In the summer of 2024, Elvis Presley’s family got confronted to a forged deed scam. A fake firm, Naussany Investments, falsely claimed Lisa Marie Presley owed millions and used Graceland as collateral. They placed a foreclosure notice and attempted to auction the estate. Riley Keough filed a lawsuit, exposing the firm as fraudulent and halting the foreclosure through a judge’s injunction. Lisa Jeanine Findley, who forged documents and posed as firm employees, was arrested and charged with deed forgery fraud and identity theft. She faces up to 22 years in prison if convicted. The FBI's Internet Crime Complaint Center does not specifically monitor deed fraud. However, in 2023, it processed a total of 9,521 real estate-related complaints defined as the loss of funds from a real estate investment, resulting in more than $145 million in losses. Victims of deed fraud can face severe financial and legal issues. They may discover the fraud only when trying to sell, refinance, or even pay taxes on the property. Reversing deed fraud typically requires a costly and time-consuming legal process, as courts must determine that the transfer was fraudulent and restore the original owner’s rights. Prevention and safeguards There are several preventive measures and fraud prevention solutions that can be established to help mitigate the risks associated with deed/title fraud. These include: For lending institutions: Enhanced ID verification: Implement multi-factor identity checks at the loan approval stage. Regular portfolio audits: Conduct periodic audits to detect unusual property transfers and title changes in their loan portfolios. For title companies: AI-driven document verification tools: Use machine learning algorithms to identify inconsistencies in deed and ownership documents. Real-time fraud monitoring: Employ analytics to track suspicious behavior patterns, such as rapid ownership changes. Seller authentication: Require biometric or multi-step identity verification for anyone claiming ownership or initiating sales. For realtors: Training and awareness: Educate realtors on how to spot warning signs of fraudulent listings and seller impersonations. Pre-transaction verification: Collaborate with title companies to validate ownership early in the listing process. Acting with the right solution Mortgage fraud is a constant threat that demands ongoing vigilance and adaptability. As fraudsters evolve their tactics, the mortgage industry must stay one step ahead to safeguard homeowners and lenders alike. With concerns over deed/title-related fraud rising, it is vital to raise awareness, strengthen preventive measures, and foster collaboration to protect the integrity of the mortgage market. By staying informed and implementing robust safeguards, we can collectively combat and prevent mortgage fraud from disrupting the financial security of individuals and the industry. Experian mortgage powers advanced capabilities across the mortgage lifecycle by gaining market intelligence, enhancing customer experience to remove friction and tapping into industry leading data sources to gain a complete view of borrower behavior. Visit our website to see how these solutions can help your business prevent deed fraud. Learn more

The risk of identity theft continues to grow yearly for consumers and businesses alike. Identity theft and fraud cases have nearly tripled over the past ten years, with cybercrime losses totaling more than $10 billion this year alone.[1] An effective way for organizations to combat these threats is to implement a policy of identity risk management. Identity risk management Identity risk management refers to the methods used by organizations to anticipate potential fraud threats, protect themselves and their consumers from those vulnerabilities, resolve any fraud incidents that may occur, and prevent future fraud events from happening again. Businesses can implement these methods through a variety of tools and technologies designed to detect fraud risks and mitigate them as quickly and efficiently as possible. By recognizing the risks of identity theft, helping consumers who fall victim to fraud, and preventing identity theft in the future, financial institutions can take an effective approach to identity risk management and ensure that their business is protected and their consumers stay safe. Recognizing risks of identity theft Identifying high-risk situations Inform consumers about high-risk situations that could lead to identity theft. Emphasize the dangers of data breaches, cyber-attacks, phishing scams, and social engineering tactics. Advise them to be cautious with personal documents and to avoid using public Wi-Fi for sensitive transactions. By raising awareness, financial institutions can help consumers stay vigilant. Risk-based authentication solutions can also help minimize risk with adaptive authentication methods. With sophisticated risk assessment and a combination of front- and back-end authentication methods, organizations can optimize the consumer experience and their identity risk management simultaneously. Protecting vulnerable information Guide consumers on safeguarding their most vulnerable information. Explain the importance of protecting Social Security numbers, credit card and bank account details, PINs, passwords, and medical records. Offer tips on securing this information and the potential consequences of it falling into the wrong hands. Providing practical advice, such as using password managers, enabling multifactor authentication, and regularly updating passwords, can significantly enhance your consumers’ security. Additionally, offering secure storage solutions for sensitive documents can further protect their information. Helping consumers who fall victim to fraud Providing immediate support If a consumer falls victim to identity theft, financial institutions should be ready to provide immediate support. Establish a clear protocol for reporting fraud and ensure that consumer service representatives are trained to handle such situations. Assist consumers in contacting their banks and credit card companies to report fraud and prevent further unauthorized transactions. Having a dedicated fraud response team can streamline this process and provide consumers with the reassurance that their issue is being handled by experts. This team can also offer personalized advice and support, making the recovery process less daunting for the victim. Helping restore identity To support consumers in the process of restoring their identity, financial institutions can offer identity restoration services as part of their consumer support. These services can include helping consumers navigate the complexities of repairing their credit, disputing fraudulent charges, and securing their accounts against future threats. Preventing identity theft in the future Enhancing personal security measures Encourage consumers to strengthen their personal security measures. Promote the use of strong, unique passwords and two-factor authentication (2FA) for all accounts. Advise them to regularly update and patch their software and devices. Offer services like secure document shredding to prevent thieves from accessing sensitive information. Financial institutions can also strengthen their identity risk management efforts by implementing robust security measures within their own systems. Demonstrating a commitment to security can build trust and encourage consumers to adopt similar practices. Implementing monitoring and alerts Financial institutions can offer identity theft protection services that include regular monitoring of credit reports and account alerts for suspicious activities. Educate consumers on the importance of closely monitoring their financial statements and bills to detect any unauthorized transactions early. Providing tools such as mobile apps that offer real-time alerts for suspicious activities can empower consumers to take immediate action if something seems amiss. Additionally, offering complimentary credit monitoring services can add an extra layer of protection. Leveraging data Data and analytics are among the most powerful tools at a financial institution’s disposal. By leveraging advanced analytics, institutions can identify patterns and anomalies that may indicate fraudulent activity. Machine learning algorithms can analyze vast amounts of transaction data in real- time, flagging suspicious behavior before it escalates into fraud. This proactive approach not only helps in early detection but also minimizes the impact on the consumer. Moreover, data analytics can streamline and improve the consumer experience by reducing false positives and ensuring that legitimate transactions are not unnecessarily flagged. This balance between security and convenience is crucial in maintaining consumer trust and satisfaction. Financial institutions can use these insights to tailor their fraud prevention strategies, using digital identity management solutions to provide more value to consumers. Behavioral analytics Fraud detection technology, such as behavioral analytics, is continually evolving as hacking methods become increasingly sophisticated. Insights from behavioral analytics can help mitigate fraud in real time and prevent identity theft, account takeover, and bot attacks — empowering businesses to provide a seamless consumer experience. Experian’s recent acquisition of NeuroID, an industry leader in behavioral analytics, means we now offer even more modern and frictionless capabilities, enhancing our fraud risk suite by providing a new layer of insight into digital behavioral signals and analytics throughout the consumer lifecycle. This additional level of defense against fraud can empower businesses to ensure that their consumers are safe and secure online. Identity management solutions Consumers are more at risk of identity theft than ever before, and it’s the responsibility of financial institutions to provide protection and support to the people they do business with. Offering identity management solutions can help organizations feel safe and secure about their consumer and business data without adding friction or functioning outside of their risk tolerance. Experian’s identity management tools allow financial institutions to confirm the identities of businesses and consumers with minimal friction, balancing end-user experience with enhanced security. This allows organizations to easily manage authentication events with confidence. Next steps Financial institutions have a vital role in helping consumers manage their risk of identity theft. By recognizing vulnerabilities, providing support to victims, and implementing preventive measures, financial institutions can protect their consumers’ personal information and financial well-being. Proactive identity risk management not only benefits consumers but also builds trust and loyalty with your brand. Protect your business from identity fraud today. Discover how Experian’s cutting-edge identity risk management solutions can safeguard your consumers and streamline your operations. Learn more about our identity management solutions This article includes content created by an AI language model and is intended to provide general information. [1] IdentityTheft.org. 2024 Identity Theft Facts and Statistics.

U.S. federal prosecutors have indicted Michael Smith of North Carolina for allegedly orchestrating a $10 million fraud scheme involving AI-generated music. Smith is accused of creating fake bands and using AI tools to produce hundreds of tracks, which were streamed by fake listeners on platforms like Spotify, Apple Music, and Amazon Music. Despite the artificial engagement, the scheme generated real royalty payments, defrauding these streaming services. This case marks the first prosecution of its kind and highlights a growing financial risk: the potential for rapid, large-scale fraud in digital platforms when content and engagement can be easily fabricated. A new report from Imperva Inc. highlights the growing financial burden of unsecure APIs and bot attacks on businesses, costing up to $186 billion annually. Key findings highlight the heavy economic burden on large companies due to their complex and extensive API ecosystems, often unsecured. Last year, enterprises managed about 613 API endpoints on average, a number expected to grow, increasing associated risks. APIs exposure to bot attacks Bot attacks, similar to those seen in streaming fraud, are also plaguing financial institutions. The risks are significant, weakening both security and financial stability. 1. Fraudulent transactions and account takeover Automated fraudulent transactions: Bots can perform high volumes of small, fraudulent transactions across multiple accounts, causing financial loss and overwhelming fraud detection systems. Account takeover: Bots can attempt credential stuffing, using compromised login data to access user accounts. Once inside, attackers could steal funds or sensitive information, leading to significant financial and reputational damage. 2. Synthetic identity fraud Creating fake accounts: Bots can be used to generate large numbers of synthetic identities, which are then used to open fake accounts for money laundering, credit fraud, or other illicit activities. Loan or credit card fraud: Using fake identities, bots can apply for loans or credit cards, withdrawing funds without intent to repay, resulting in significant losses for financial institutions. 3. Exploiting API vulnerabilities API abuse: Just as bots exploit API endpoints in streaming services, they can also target vulnerable APIs in financial platforms to extract sensitive data or initiate unauthorized transactions, leading to significant data breaches. Data exfiltration: Bots can use APIs to extract financial data, customer details, and transaction records, potentially leading to identity theft or data sold on the dark web. Bot attacks targeting financial institutions can result in extensive fraud, data breaches, regulatory fines, and loss of customer trust, causing significant financial and operational consequences. Safeguarding financial integrity To safeguard your business from these attacks, particularly via unsupervised APIs, a multi-layered defense strategy is essential. Here’s how you can protect your business and ensure its financial integrity: 1. Monitor and analyze data patterns Real-time analytics: Implement sophisticated monitoring systems to track user behavior continuously. By analyzing user patterns, you can detect irregular spikes in activity that may indicate bot-driven attacks. These anomalies should trigger alerts for immediate investigation. AI, machine learning, and geo-analysis: Leverage AI and machine learning models to spot unusual behaviors that can signal fraudulent activity. Geo-analysis tools help identify traffic originating from regions known for bot farms, allowing you to take preventive action before damage occurs. 2. Strengthen API access controls Limit access with token-based authentication: Implement token-based authentication to limit API access to verified applications and users. This reduces the chances of unauthorized or bot-driven API abuse. Control third-party integrations: Restrict API access to only trusted and vetted third-party services. Ensure that each external service is thoroughly reviewed to prevent malicious actors from exploiting your platform. 3. Implement robust account creation procedures PII identity verification solutions: Protect personal or sensitive data through authenticating someone`s identity and helping to prevent fraud and identity theft. Email and phone verification: Requiring email or phone verification during account creation can minimize the risk of mass fake account generation, a common tactic used by bots for fraudulent activities. Combating Bots as a Service: Focusing on intent-based deep behavioral analysis (IDBA), even the most sophisticated bots can be spotted, without adding friction. 4. Establish strong anti-fraud alliances Collaborate with industry networks: Join industry alliances or working groups that focus on API security and fraud prevention. Staying informed about emerging threats and sharing best practices with peers will allow you to anticipate new attack strategies. 5. Continuous customer and account monitoring Behavior analysis for repeat offenders: Monitor for repeat fraudulent behavior from the same accounts or users. If certain users or transactions display consistent signs of manipulation, flag them for detailed investigation and potential restrictions. User feedback loops: Encourage users to report any suspicious activity. This crowd-sourced intelligence can be invaluable in identifying bot activity quickly and reducing the scope of damage. 6. Maintain transparency and accountability Audit and report regularly: Offer regular, transparent reports on API usage and your anti-fraud measures. This builds trust with stakeholders and customers, as they see your proactive steps toward securing the platform. Real-time dashboards: Provide users with real-time visibility into their data streams or account activities. Unexplained spikes or dips can be flagged and investigated immediately, providing greater transparency and control. Conclusion Safeguarding your business from bot attacks and API abuse requires a comprehensive, multi-layered approach. By investing in advanced monitoring tools, enforcing strict API access controls, and fostering collaboration with anti-fraud networks, your organization can mitigate the risks posed by bots while maintaining credibility and trust. The right strategy will not only protect your business but also preserve the integrity of your platform. Learn more

In this article...Understanding the scope of fintech fraudThe importance of fintech fraud preventionSynthetic identity (ID) fraud: A growing threatHow fintech fraud detection and prevention are evolvingGet started today The integration of technology with traditional financial services has unlocked unprecedented convenience and opportunities for consumers and businesses alike. However, this digital shift has opened the door for more sophisticated fraud tactics. With fraudsters continuously refining their methods, fintech companies must invest in advanced fintech fraud detection and prevention solutions. Understanding the scope of fintech fraud As fintech platforms expand, they also attract the attention of cybercriminals. The accessibility of digital financial services can create vulnerabilities that fraudsters exploit, executing everything from personal account takeovers to larger-scale breaches involving synthetic identities. Source: Experian’s U.S. Identity & Fraud Report To counter these threats, fintech companies must deploy innovative fraud management solutions powered by artificial intelligence (AI), machine learning (ML), and advanced analytics. Unlike traditional methods that often rely on static rules and manual reviews, these solutions can process vast amounts of data, learn from historical patterns, and detect anomalies in real-time. This allows organizations to identify suspicious activities before they lead to significant losses. The importance of fintech fraud prevention While detecting fraud is crucial, preventing it from occurring in the first place is even more important. Fraud prevention solutions aim to create robust systems that stop fraudsters in their tracks before they can cause damage. With the rise of digital financial services, the need for proactive fraud prevention measures has never been greater. These solutions protect both consumers and businesses from financial harm, reducing the risk of financial loss and reputational damage. Advanced fraud prevention solutions employ multilayered strategies, combining AI-driven fraud detection tools with methods such as multifactor authentication and biometric identity verification. These tools create an extra layer of security, making it difficult for fraudsters to access sensitive data or execute fraudulent transactions. Experian’s fraud prevention solutions offer businesses a comprehensive suite of tools designed to prevent various types of fraud. From real-time transaction monitoring to sophisticated user authentication methods, these solutions provide the protection businesses need to stay ahead of evolving fraud tactics. Synthetic identity (ID) fraud: A growing threat One of the most concerning forms of fraud that fintech companies face is synthetic ID fraud. This type of fraud involves the creation of a fake identity using a combination of real and fabricated information. Fraudsters often steal pieces of personal data — such as Social Security numbers or addresses—and then combine them with fictional information to create a new, synthetic identity. These synthetic identities can be used to open bank accounts, apply for credit cards, or take out loans, leaving businesses and consumers vulnerable to significant financial losses. Synthetic ID fraud is particularly difficult to detect because the synthetic identity often looks legitimate to traditional verification systems. As a result, fintech companies must deploy sophisticated fraud detection systems that can identify synthetic identities before they’re used to commit fraud. Machine learning algorithms, for instance, can analyze behavioral data, detecting discrepancies that may indicate a synthetic identity. Experian is ranked #1 by the Center for Financial Professionals (CeFPro®) for Identity and Fraud. The ranking appeared in CeFPro’s Fintech Leaders Report, a comprehensive annual study of the fintech industry. How fintech fraud detection and prevention are evolving As fraudsters continue to evolve their tactics, fintech companies must remain one step ahead by investing in cutting-edge fraud detection and prevention technologies. Real-time monitoring, predictive analytics, and biometrics are just a few of the technologies shaping the future of fraud detection. By integrating these technologies into their fraud management processes, fintech companies can offer a more secure and seamless experience for their users. With the acquisition of NeuroID, an industry leader in behavioral analytics, Experian has amplified its fraud risk suite by providing a new layer of insight into digital behavioral signals and analytics. Available through our fraud solutions on the Experian Ascend PlatformTM, clients can proactively monitor and analyze a user’s real-time digital behavior, allowing them to confidently navigate the online landscape and provide frictionless customer experiences. Get started today As the fraud landscape continues to evolve, fintech companies must adopt comprehensive solutions to stay ahead of emerging threats. By doing so, they can protect themselves and their customers, ensuring the continued success of digital financial services in the years to come. To learn more, check out our fraud management and fintech solutions. Fraud management solutions Fintech solutions

Online fraud has increased exponentially over the past few years, with the Federal Trade Commission (FTC) data showing that consumers reported losing more than $10 billion to fraud in 2023. This marks the first time that fraud losses have reached that benchmark, and it’s a 14% increase over reported losses in 2022. As a result, e-commerce merchants and retailers have reacted by adding friction to e-commerce interactions. The risk is that a legitimate user may be denied a purchase because they have incorrectly been labeled a fraudster — a “false decline.” Now, as the holiday shopping season approaches, e-commerce merchants expect a surge in online spending and transactions, which in turn creates concern for an uptick in false declines. In a recent webinar, Experian experts Senior Vice President of Business Development and eCommerce Dave Tiezzi and Senior Director of Product Management Jose Pallares explored strategies for how e-commerce merchants can determine the risk level of a transaction and ensure that they do not miss out on genuine purchases and good customers. Below are a few key perspectives from our speakers: What are the biggest challenges posed by online card transactions? DT: One of the biggest issues merchants face is false declines. In the report, The E-Commerce Fraud Enigma: The Quest to Maximize Revenue While Minimizing Fraud Experian and Aite-Novarica Group (now Datos Insights) found that 1.16% of all sales are unnecessarily rejected by merchants. While this percentage may seem small, it represents significant revenue loss during the high-volume holiday shopping season. The report also highlights that 16% of all attempted online transactions encounter some form of friction due to suspected fraud. Alarmingly, 70% of that friction is unnecessary, meaning it’s not preventing fraud but instead disrupting the purchasing process for legitimate customers. This friction translates into a poor online shopping experience, often resulting in cart abandonment, lost sales and a decline in customer loyalty. What are the key consumer trends and expectations for the upcoming holiday season? DT: Experian's 2024 Holiday Spending Trends and Insights Report reveals that while 35% of holiday shopping in 2023 occurred in December, peaking at 9% the week before Christmas, Cyber Week in November also represented 8% of total holiday sales. This highlights the importance for merchants to be prepared well before the holiday rush begins in November and extends through December. As they gear up for this high-volume season, merchants must also prioritize meeting consumer expectations for speed, ease and security—which are top-of-mind for consumers. According to our 2024 U.S. Identity & Fraud Report, 63% of consumers consider it extremely or very important for businesses to recognize them online, while 81% say they’re more trusting of businesses that can accomplish easy and accurate identification. They’re also wary of fraud, ranking identity theft (84%) and stolen credit card information (80%) as their top online security concerns. Considering these trends, it’s important for merchants to ensure seamless and secure transactions this holiday season. False declines are a persistent problem for e-commerce merchants, especially during the holidays. How can merchants minimize these declines while protecting consumers from fraud? What best practices can merchants adopt to address these risks? JP: False declines often result from overly cautious fraud detection systems that flag legitimate transactions as suspicious. While it’s essential to prevent fraud, turning away legitimate customers can severely impact both revenue and customer satisfaction. To minimize false declines, merchants should leverage advanced fraud prevention tools that combine multiple data points and behavioral insights. This approach goes beyond basic fraud detection by using attributes such as customer behavior, transaction patterns and real-time data analysis. Solutions incorporating NeuroID’s behavioral analytics and signals can also better assess whether a transaction is genuine based on the user’s interaction patterns, helping merchants filter out bad actors and make more informed decisions without disrupting the customer experience. What actionable strategies should e-commerce brands or merchants implement now to reduce cart abandonment and ensure a successful holiday season? JP: One of the most effective tools we offer is Experian Link™, a credit card owner verification solution designed to reduce false declines while protecting against fraud. Experian Link helps e-commerce merchants and additional retailers accurately assess transaction risk by answering a key question: Does this consumer own the credit card they presented for payment? This ensures that legitimate customers aren’t mistakenly turned away while suspicious transactions are properly flagged for further review. By adopting a multilayered identity and fraud prevention strategy, merchants can significantly reduce false declines, offer a frictionless checkout experience and maintain robust fraud defenses—all of which are essential for a successful holiday shopping season. Are there any examples of a retailer successfully leveraging credit card owner verification solutions? What were the results? JP: Yes. We recently partnered with a leading U.S. retailer with a significant online presence. Their primary goals were to reduce customer friction, increase conversion and identify their customers accurately. By leveraging Experian Link and its positive signals, the retailer could refine, test and optimize their auto-approval strategies. As a result, the retailer saw an additional $8 million in monthly revenue from transactions that would have otherwise been declined. They also achieved a 10% increase in auto-approvals, reducing operating expenses and customer friction. By streamlining backend processes, they delivered a more seamless shopping experience for their customers. Stay ahead this holiday season For more expert insights on boosting conversions and enhancing customer loyalty, watch our on-demand webinar, Friction-Free Festivities: Strategies to Maximize Conversion and Reduce False Declines, hosted by the Merchant Risk Council (MRC). Additionally, visit us online to learn more about how Experian Link can transform your business strategy. Watch on-demand webinar Visit us The webinar is available to MRC members. If you’re already a member, you can access this resource here. Not a member? Our team would be happy to schedule a demo on Experian Link and discuss strategies to help your business grow. Get in touch today.