Market Trends

Recent research shows Hispanics—especially Millennials who are entering their home-buying years—are particularly eager for homeownership.

In 2017, we saw an increase of more than 30 percent in e-commerce fraud attacks compared with 2016.

Do you have a client who is applying for credit but has placed a security freeze on his Experian file? Here’s how you can help.

Kathleen Peters, SVP of Product Management for Global Fraud and Identity, and recently included in the Top 100 influencers in Identity.

In helping lenders with new product launches, there are common areas of focus and specific steps to move from initial business case to tactical planning.

Many consumers would give the right bank or retailer their data in exchange for personalized marketing offers in their inbox, social feeds and mailbox.

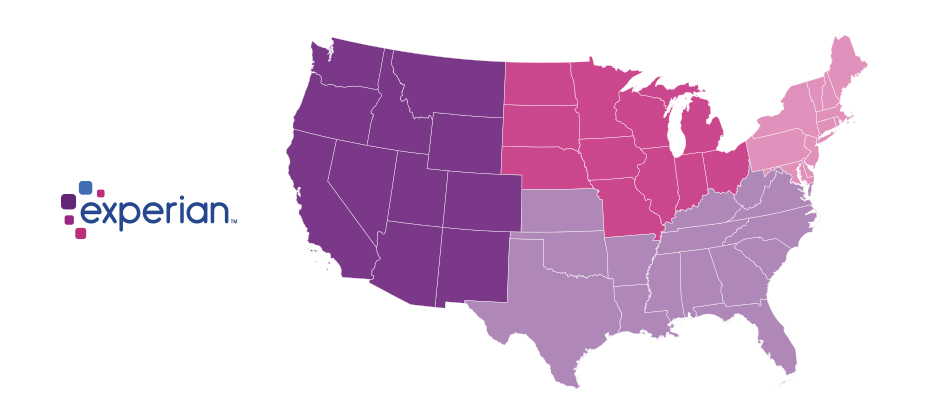

Experian’s 8th annual State of Credit report reveals the nation’s average credit score is up two points year-over-year to 675.

Podcast to discuss the emergence of synthetic identity fraud, its true financial impact and how organizations can begin to fight back.

As we enter the holiday season, headlines abound around the shifts and trends in retail. Here from retail expert John Squire on the latest evolutions in the space.

With 81% of Americans having a social media profile, you may wonder if social media insights can be used to assess credit risk. When considering social media data as it pertains to financial decisions, there are 3 key concerns to consider.

Synthetic id fraud in a post breach world

Our national survey found that consumers struggle to find a credit card that meets their needs. They say there are too many options and it’s too time-consuming to research. Here's what they want:

Direct mail is dead. It’s so 90s. Digital is the way to reach consumers. Marketers have heard this time and again, but is it true?

We recently analyzed millions of online transactions from the first half of 2017 to identify fraud attack rates. Here are the top 3 riskiest states for e-commerce billing and shipping fraud for H1 2017

All communities are impacted by the contributions of Hispanics, and now is the time for FIs to reflect upon their largest growth opportunity.