Market Trends

With 81% of Americans having a social media profile, you may wonder if social media insights can be used to assess credit risk. When considering social media data as it pertains to financial decisions, there are 3 key concerns to consider. The ECOA requires that credit must be extended to all creditworthy applicants regardless of race, religion, gender, marital status, age and other personal characteristics. Social media can reveal these characteristics and inadvertently affect decisions. Social media data can be manipulated. Individuals can represent themselves as financially responsible when they’re not. On the flip side, consumers can’t manipulate their payment history. When it comes to credit decisions, always remember that the FCRA trumps everything. Data is essential for all aspects of the financial services industry, but it’s still too early to click the “like” button for social media. Make more insightful decisions with credit attributes>

The data to create synthetic identities is available. And the marketplace to exchange and monetize that data is expanding rapidly. The fact that hundreds of millions of names, addresses, dates of birth, and Social Security numbers (SSNs) have been breached in the last year alone, provides an easy path for criminals to surgically target new combinations of data. Armed with an understanding of the actual associations of these personally identifiable information (PII) elements, fraudsters can better navigate the path to perpetrate identity theft, identity manipulation, or synthetic identity fraud schemes on a grand scale. Using information such as birth dates and addresses in combination with Social Security numbers, criminals can target new combinations of data to yield better results with lower risk of detection. Some examples of this would be: identity theft, existing account takeovers, or the deconstruction and reconstruction of those PII elements to better create effective synthetic identities. Experian has continued to evolve and innovate against fraud risks and attacks with an understanding of attack rates, vectors, and the shifting landscape in data availability and security. In doing so, we’ve historically operated under the assumption that all PII is already compromised in some way or is easily done so. Because of this, we employ a layered approach, providing a more holistic view of an identity and the devices that are used over time by that identity. Relying solely on PII to validate and verify an identity is simply unwise and ineffective in this era of data compromise. We strive to continuously cultivate the broadest and most in-depth set of traditional, innovative and alternative data assets available. To do this, we must enable the integration of diverse identity attributes and intelligence to balance risk, while maintaining a positive customer experience. It’s been quite some time since the use of basic PII verification alone has been predictive of identity risk or confidence. Instead, validation and verification is founded in the ongoing definition and association of identities, the devices commonly used by those individuals, and the historical trends in their behavior. Download our newest White Paper, Synthetic Identities: Getting real with customers, for an in-depth Experian perspective on this increasingly significant fraud risk.

Our national survey found that consumers struggle to find a credit card that meets their needs. They say there are too many options and it’s too time-consuming to research. What do consumers want? With 53% of survey respondents not satisfied with their current cards and 1 in 3 saying they’re likely to get a new card within 6 months, now’s the time to start personalizing offers and growing your portfolio. Start personalizing offers today>

Direct mail is dead. It’s so 90s. Digital is the way to reach consumers. Marketers have heard this time and again, and many have shifted their campaign focus to the digital space. But as our lives become more and more consumed by digital media, consumers are giving less time and attention to the digital messages they receive. The average lifespan of an email is now just two seconds and brand recall directly after seeing a digital ad is just 44%, compared to direct mail which has a brand recall of 75%. Further research shows direct mail marketing is one of the most effective tools for customer acquisition and loan growth. The current Data & Marketing Association (DMA) response rate report reveals the direct mail response rates for 2016 were at the highest levels since 2003. Additionally, while mailing volume has trended down since October 2016, response rates have trended up, and reached 0.68% in March 2017, up from 0.56% in October 2016. Using data and insights to tailor a direct mail campaign can yield big results. Here are some attention-grabbing tips: Identify Your Target Market: Before developing your offer and messaging strategy, begin with the customer profile you are trying to attract. Propensity models and estimated interest rates are great tools for identifying consumers who are more likely to respond to an offer. Adding them as an additional filter to a credit-qualified population can help increase response rates. Verify your Mailing List: Experian’s address verification software validates the accuracy and completeness of a physical address, flags inaccuracies, and corrects errors before they can negatively impact your campaign. Personalize the Offer: Consumers are more likely to open offers that are personalized, and appeal to their life stage, organizational affiliations or interests. Experian’s Mosiac profile report is a simple, inexpensive way to gather data-based insight into the lifestyle and demographics of your audience. Time the Offer: Timing your campaign with peak market demand is key. For example, personal loan demand is highest in the first quarter after the holidays, while student loans demand peaks in the Spring. Direct mail can help overcome digital fatigue that many consumers are experiencing, and when done right, it’s the printed piece that helps marketers boost response rates.

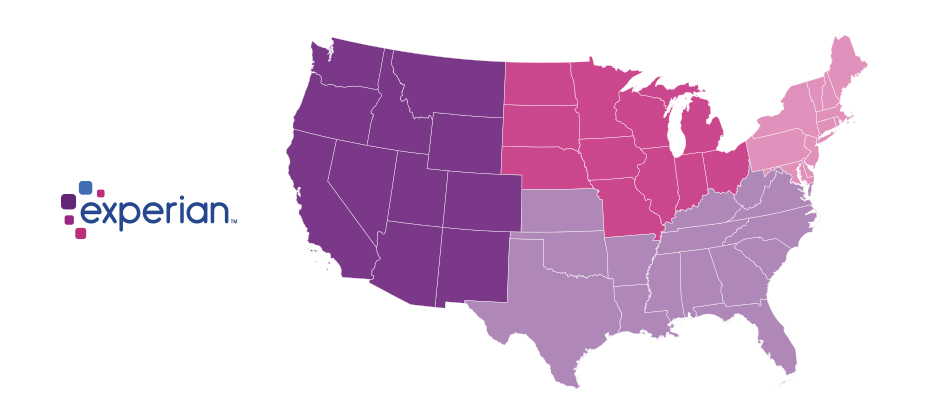

We recently analyzed millions of online transactions from the first half of 2017 to identify fraud attack rates. Here are the top 3 riskiest states for e-commerce billing and shipping fraud for H1 2017: Riskiest states for billing fraud Oregon Delaware Washington, D.C. Riskiest states for shipping fraud Oregon Delaware Florida Fraudsters are extremely creative, motivated and often connected. Protect all points of contact with your customers to prevent this growing type of fraud. Is your state in the top 10?

National Hispanic Heritage Month is observed each year from Sept. 15 to Oct. 15, by celebrating the histories, cultures and contributions of American citizens whose ancestors came from Spain, Mexico, the Caribbean and Central and South America. With one in six U.S. residents being Hispanic, all communities are impacted by the contributions of Hispanics—and now is a great time for financial institutions to reflect upon their largest growth opportunity. What is the best way to reach Hispanic consumers? What are the nuances of the Hispanic market? What are some of the myths FIs have about the Hispanic community? Miriam De Dios Woodward, CEO of Coopera, a Hispanic market strategy firm that helps credit unions reach and serve the Hispanic consumer segment, recently chatted with Experian about serving the Hispanic market. Here she shares her thoughts: Are there special considerations or insights credit unions should know when serving the Hispanic market? It’s very important to understand the Hispanic market is nuanced. There are 22 Spanish-speaking Latin American countries from which prospective Hispanic credit union members may hail. Add to that the fact, many U.S.-born Hispanics think, speak and behave differently than their parents and grandparents. Layer over this the existence of segments like small business owners or Millennials and you can begin to see the complexities involved with targeting and serving a multi-faceted Hispanic market. A smart Hispanic membership growth strategy will be based on segmentation, so credit unions should be willing to invest upfront in good market research. You have to understand what your local Hispanic community really looks like before you can mobilize your teams and leadership around serving them well. Are there particular consumer trends you have seen in the Hispanic community that impact the financial services space? The increasing digitization of financial services is a trend that definitely impacts Hispanic consumers. That’s because Hispanics typically over-index in studies that look at consumer use of connected devices, online banking and social media. A good Hispanic membership growth strategy will take mobile and digital products and services into account and will be tailored to the specific needs of local Hispanic communities. People often assume the Hispanic market is largely centered in states like California, Arizona, Texas and New Mexico. Are you finding that credit unions outside of these southwestern states are discovering they too need to build out a strategy in partnering with this consumer base? Absolutely. Hispanic population growth is happening far beyond so-called “gateway states” like those you mention above. In fact, states such as North Dakota, Kentucky, Louisiana, Delaware and Maryland actually saw the largest Hispanic population growth between 2007 and 2014. Midwestern states, too, are discovering just as many opportunities for engagement with their own growing numbers of Hispanic residents. Iowa and Wisconsin, for instance, each experienced explosive growth rates and now count Hispanics among one of the largest, fastest-growing and youngest groups in their cities. With a comprehensive and strategic approach to Hispanic membership growth, credit unions in unexpected places can become the preferred financial institution for this important segment. That’s because a great number of Hispanics in the U.S. are not tethered to an existing financial relationship. For more on this, check out our recent white paper Hispanic Member Growth Not Just for 'Gateway States' Anymore. What are the biggest myths financial services companies have about the Hispanic community? While there continue to be many misconceptions about the multifaceted Hispanic community, the following three continue to prevail most heavily. Myth: Hispanic consumers are only interested in transaction-based products. Check cashing and remittances are necessary services for many first generation Hispanic segments. At the same time, many of these consumers are interested in long-term relationships. Our own research indicates product penetration increases at a faster rate among Hispanic members as compared to non-Hispanic members when credit unions execute a strategic plan. Myth: The majority of Hispanics are undocumented. This misperception has been somewhat renewed this year with all the political back and forth on the subject of immigration. That’s why it’s so important for credit unions to educate – from the inside out – stakeholders on the facts. Many people do not know, for instance, that of the country's more than 52 million Hispanics, most are native-born Americans, and nearly three in four are U.S. citizens. Myth: The law prevents us from serving immigrants. There are many forms of acceptable government issued identification, such as passports and consular cards that are in full compliance with the Patriot Act and Customer Identification Program rules. In addition, financial institutions can compliantly lend to individuals who have Individual Taxpayer Identification Numbers. In fact, the NCUA wants credit unions to serve Hispanic members, including Hispanic immigrants. For more on this, check out the recording of the NCUA hosted panel, “Unique Challenges and Opportunities Serving Hispanic Credit Union Members.” For a credit union seeking to build a relationship with this community, what are your recommendations? Are there particular products or touchpoints they should focus on? Solidifying the right organizational mentality first is an important best practice. Building buy-in, doing the market research, developing a comprehensive strategy based on segmentation and defining what success truly looks like – these are all a part of laying the foundation for success with the Hispanic market. Credit unions should also be smart about talking to and partnering with local organizations that already know – and are trusted by – Hispanic residents. Conducting focus groups with the leaders of these groups and the people they serve can give credit unions a wealth of information about the makeup of their local Hispanic community and the value they might bring to the community.

We use our laptops and mobile phones every day to communicate with our friends, family, and co-workers. But how do software programs communicate with each other? APIs--Application Programming Interfaces--are the hidden backbone of our modern world, allowing software programs to communicate with one another. Behind the scenes of every app and website we use, is a mesh of systems “talking” to each other through a series of APIs. Today, the API economy is quickly changing how the world interacts. Everything from photo sharing, to online shopping, to hailing a cab is happening through APIs. Because of APIs, technical innovation is happening at a faster pace than ever. We caught up with Edgar Uaje, senior product manager at Experian, to find out more about APIs in the financial services space. What exactly are APIs and why are they so important? And how do they apply to B2B? APIs are the building blocks of many of our applications that exist today. They are an intermediary that allows application programs to communicate, interact, and share data with various operating systems or other control programs. In B2B, APIs allow our clients to consume our data, products, and services in a standard format. They can utilize the APIs for internal systems to feed their risk models or external applications for their customers. As Experian has new data and services available, our clients can quickly access the data and services. Are APIs secure? APIs are secure as long as the right security measures are put in place. There are many security measures that can be utilized such as authentication, authorization, channel encryption and payload encryption. Experian takes security seriously and ensures that the right security measures are put in place to protect our data. For example, one of the recent APIs that was built this year utilizes OAuth, channel encryption, and payload encryption. The central role of APIs is promoting innovation and rapid but stable evolution, but they seem to only have taken hold selectively in much of the business world. Is the world of financial services truly ready for APIs? APIs have been around for a long time, but they are getting much more traction recently. Financial tech and online market place lending companies are leading the charge of consuming data, products, and services through APIs because they are nimble and fast. With standard API interfaces, these companies can move as fast as their development teams can. The world of financial services is evolving, and the time is now for them to embrace APIs in day-to-day business. How can APIs benefit a bank or credit union, for example? APIs can benefit a bank or credit union by allowing them to consume Experian data, products, and services in a standard format. The value to them is faster speed to market for applications (internal/external), ease of integration, and control over the user’s experience. APIs allow a bank or credit union to quickly develop new and innovative applications quickly, with the support of their development teams. Can you tell us more about the API Developer Portal? Experian will publish the documentation of our available APIs on our Developer Portal over time as they become available. Our clients will have a one-stop shop to view available APIs, review API documentation, obtain credentials, and test APIs. This is simplifying data access by utilizing REST API, making it easier for our clients.

Since the advent of the internet, our lives have changed drastically for the better. We can perform many of life’s daily activities from the comfort of our own home. According to Aite, in 2016 alone 36 million Americans made some form of mobile payment — paying a bill, purchasing something online, paying for fast food or making a mobile wallet purchase at a retailer. Simply put, the internet has made our lives easier. But with the good also comes the bad. While most consumers have moved to the digital world, so have fraudsters. With minimal risk and high reward at stake, e-commerce fraud attacks have increased dramatically over the last few years, with no signs of slowing down. We recently analyzed millions of transactions from the first half of 2017 to identify fraud attack rates based on billing and shipping addresses and broke down the findings into various geographic trends. Fraud attack rates represent the attempted fraudulent e-commerce transactions against the population of overall e-commerce orders. Consumers living out West and in the South have experienced more than their fair share of fraud. During the first half of 2017, the West and the South were the top two regions for both billing and shipping attacks. While both regions were at the top during the same time last year, the attacks themselves have increased substantially. Given the proximity to seaports and major international airports, this is somewhat unsurprising — particularly for shipping fraud — as many fraudsters will leverage reshippers to transport goods soon after delivery. .dataTb{margin:20px auto;width:100%}.dataTb:after{clear:both}.dataTb table{}.dataTb td,.dataTb th{border:1px solid #ddd;padding:.8em}.dataTb th{background:#F4F4F4}.tbL{float:left;width:49%}.tbR{float:right;width:49%;margin:0 0 0 2%} Shipping: Riskiest Regions Region Attack rate West 38.1 South 32.1 Northeast 27.0 North Central 20.7 Billing: Riskiest Regions Region Attack rate West 37.2 South 32.9 Northeast 27.3 North Central 24.0 At the state level, the top three shipping fraud states remained the same as 2016 — Delaware, Oregon and Florida — but the order changed. Oregon was the most targeted, with a fraud rate of 135.2 basis points, more than triple its rate at in the end of 2016. Though no longer in the top spot, Delaware saw alarming spikes as well, with shipping attack rates nearly triple last year’s rate at 128.6 basis points and billing attacks at 79.6 basis points. .dataTb{margin:20px auto;width:100%}.dataTb:after{clear:both}.dataTb table{}.dataTb td,.dataTb th{border:1px solid #ddd;padding:.8em}.dataTb th{background:#F4F4F4}.tbL{float:left;width:49%}.tbR{float:right;width:49%;margin:0 0 0 2%} Shipping: Riskiest States State Attack rate Oregon 135.2 Delaware 128.2 Florida 57.4 New York 45.0 Nevada 36.9 California 36.9 Georgia 33.5 Washington, D.C 30.8 Texas 29.6 Illinois 29.4 Billing: Riskiest States Region Attack rate Oregon 87.5 Delaware 79.6 Washington, D.C. 63.0 Florida 47.4 Nevada 38.8 California 36.9 Arkansas 36.6 New York 35.5 Vermont 34.2 Georgia 33.4 Diving a bit deeper, ZIPTM codes in Miami, Fla., make up a significant portion of the top 10 ZIP CodeTM lists for shipping and billing attacks — in fact, many of the same ZIP codes appear on both lists. The other ZIP Code that appears on both lists is South El Monte, Calif., which has a high percentage of industrial properties — common targets for fraudsters to ship packages, then reship overseas. You can download the top 100 riskiest Zip Codes in the U.S. for H1 2017. .dataTb{margin:20px auto;width:100%}.dataTb:after{clear:both}.dataTb table{}.dataTb td,.dataTb th{border:1px solid #ddd;padding:.8em}.dataTb th{background:#F4F4F4}.tbL{float:left;width:49%}.tbR{float:right;width:49%;margin:0 0 0 2%} Shipping: Top 10 riskiest ZIP™ Codes ZIP Code Attack rate 33122 [Miami, Fla.] 2409.4 91733 [South El Monte, Calif.] 1655.5 33198 [Miami, Fla.] 1295.2 33166 [Miami, Fla.] 1266.0 33195 [Miami, Fla.] 1037.3 33192 [Miami, Fla.] 893.9 97251 [Portland, Ore.] 890.6 07064 [Port Reading, NJ] 808.9 89423 [Minden, Nev.] 685.5 77072 [Houston, Tex.] 629.3 Billing: Top 10 riskiest ZIP™ Codes ZIP Code Attack rate 77060 [Houston, Tex.] 1337.6 33198 [Miami, Fla.] 1215.6 33122 [Miami, Fla.] 1106.2 33166 [Miami, Fla.] 1037.4 91733 [South El Monte, Calif.] 780.1 33195 [Miami, Fla.] 713.7 97252 [Portland, Ore.] 670.8 33191 [Miami, Fla.] 598.8 33708 [St. Petersburg, Fla.] 563.6 33792 [Miami, Fla.] 493.0 As e-commerce fraud continues to grow, businesses need to be proactive to keep themselves and their customers safe. That means incorporating multiple, layered fraud prevention strategies that work together seamlessly — for example, understanding details about users and their devices, knowing how users interact with the business and evaluating previous transaction history. This level of insight can help businesses distinguish real customers from nefarious ones without impacting the customer experience. While businesses are ultimately responsible for the safety of customers and their data, the onus doesn’t rest solely with them. Consumers should also be vigilant when it comes to protecting their digital identities and payment information. That means creating strong, unique passwords; actively monitoring online accounts; and using two-factor authentication to secure account access. At the end of the day, e-commerce fraud is a challenge that businesses and consumers will experience for the foreseeable future. But rising attack rates don’t have to spell doom and gloom for the industry. E-commerce growth is still extremely strong, as consumers interact through multiple channels (in-store, mobile and web) and expect a personalized experience. Establishing trust and verifying digital identities are key to meeting these latest expectations, which provide new opportunities for businesses and consumers to interact seamlessly and transact securely. With multiple safeguards in place, businesses have a variety of options to protect their customers and their brand reputation. Experian is a nonexclusive full-service provider licensee of the United States Postal Service®. The following trademarks are owned by the United States Postal Service®: ZIP and ZIP Code. The price for Experian’s services is not established, controlled or approved by the United States Postal Service.

We regularly hear from clients that charge-offs are increasing and they’re struggling to keep up with the credit loss. Many clients use the same debt collection strategy they’ve used for years – when businesses or consumers can’t repay a loan, the creditor or collection agency aggressively contacts them via phone or mail to obtain repayment – never considering the customer experience for the debtor. Our data shows that consumers accounted for $37.24 billion in bankcard charge-offs in Q2 2017, a 17.1 percent increase from Q2 2016. Absorbing credit losses at such a high rate can impact the sustainability of the institution. Clearly the process could use some adjusting. Traditionally, debt collection has been solely about the money. The priority was ensuring that as much of the outstanding debt as possible was repaid. But collecting needs to be about more than that. It also should focus on the customer and his or her individual situation. When it comes to debt collection, customers should not all be treated the same way. I recently shared some tips in Credit Union Business Magazine about how to actively engage and collect from members. The same holds true for other financial institutions – they need to know the difference between a customer who has simply forgotten to make a payment and one who is dealing with financial hardship. As an example, if a person is current on his or her mortgage payment but has slipped behind on his or her credit card payment, that doesn’t necessarily signify financial hardship. It’s an opportunity to work with the customer to manage the debt and get back to current. Modern financial institutions build acquisition and customer management strategies targeted at individuals, so why should the collection process be any different? The challenge is keeping the customer at the center while also managing against potential increases in delinquencies. This holistic approach may be slightly more complex, but technology and analytics will simplify the process and bring about a more engaging experience for customers. The Power of Data and Technology Instead of relying on the same outdated collections approach – which results in uncomfortable exchanges on the phone that don’t ensure repayment –leverage data to your advantage. The data and technology exists to help you make more informed decisions, such as: What’s the most effective communication channel to reach the defaulting customer? When should you contact him or her? How often? The best course of action could be high-touch outreach, but sometimes doing nothing is the right approach. It all depends on the situation. Data and analytics can help uncover which customers are most likely to pay on their own and those who may need a little more help, allowing you to adjust your treatment strategy accordingly. By catering to the preferences of the customer, there’s a greater chance for a positive experience on both sides. The results: less charge-off debt, higher customer satisfaction and a stronger relationship. Explore the Digital Age In 2016, 36 million Americans made some form of mobile payment—paying a bill, purchasing something online, or paying for fast food, or making a Mobile Wallet purchase at a retailer. By 2020, nearly 184 million consumers will have done so, according to Aite. Consumers expect and deserve convenience. In the digital world, financial institutions have an opportunity to provide that expectation and then some. Imagine a customer being able to negotiate and manage his or her past-due account virtually, in the privacy of his or her own home, when it’s most convenient, to set their payment dates and terms. Luckily, the technology exists to make this vision a reality. Customers, not money, need to be at the heart of every debt collections strategy. Gone are the days of mass phone calls to debtors. That strategy made consumers unhappy, embarrassed and resentful. Successful debt collection comes down to a basic philosophy: Treat customers and his or her unique situation individually rather than as a portfolio profile. The creditors who live by that philosophy have an opportunity to reap the rewards on the back-end.

School is nearly back in session. You know what that means? The next wave of college students is taking out their first student loans. It’s a milestone moment – and likely the first trade on the credit file for many of these individuals. According to the College Board, the average cost of tuition and fees for the 2016–2017 school year was $33,480 at private colleges, $9,650 for state residents at public colleges, and $24,930 for out-of-state residents attending public universities. So really, regardless of where students go, the cost of a college education is big. In fact, from January 2006 to July 2016, the Consumer Price Index for college tuition and fees increased 63 percent. So, unless mom and dad did a brilliant job saving, chances are many of today’s students will take on at least some debt to foot the college bill. But it’s not just the young who are consumed by student loan debt. In Experian’s latest State of Student Lending report, we dive into how the $1.4 trillion in student loan debt for Americans is impacting all generations in regards to credit scores, debt load and delinquencies. The document additionally looks at geographical trends, noting which states have the most consumers with student loan debt and which ones have the least. Overall, we discovered 13.4% of U.S. consumers have one or more student loan balances on their credit file with an average total balance of $34k. Additionally, these consumers have an average of 3.7 student loans with 1.2 student loans in deferment. The average VantageScore® credit score for student loan carriers is 650. As we looked across the generations, every group – from the Silents (age 70+) to Gen Z (oldest are between 18 to 20) had some student loan debt. While we can make assumptions that the Silents and Boomers are likely taking out these loans to support the educational pursuits of their children and grandchildren, it can be mixed for Gen X, who might still be paying off their own loans and/or supporting their own kids. Gen X members also reported the largest average student loan total balance at $39,802. Gen Z, the newest members to the credit file, have just started to attend college, thus their generation has the largest percent of student loan balances in deferment at 77%. Their average student loan total balance is also the lowest of all generations at $11,830, but that is to be expected given their young ages. In regards to geographical trends, the Northern states tended to sport the highest average student loan total balances, with consumers in Washington D.C. winning that race with $52.5k. Southern states, on the other hand, reported higher percentages of consumers with student loan balances 90+ days past due. South Carolina, Louisiana, Mississippi, Arkansas and Texas held the top spots in the delinquency category. Access the complete State of Student Lending report. Data from this report is representative of student loan data on file as of June 2017.

There’s no shortage of headlines alluding to a student loan crisis. But is there a crisis brewing or is this just a headline grab? Let’s look at the data over the past 4 years to find out. Outstanding student loan (should be loan) debt grew 21%, reaching a high of $1.49 trillion in Q4 2016. Over the past 4 years, student loan trades grew 4%, with a slight decline from 2015 to 2016. Average balance per trade grew 17% to reach $8,210. Number of overall student loan trades per consumer is down 5% to just 3.85. The average person with a student loan balance had just over $32,000 outstanding at the end of 2016 — a rise of 15%. While we’re seeing some increases, the data tells us this is a media headline grab. If students are educated about the debt they’re acquiring and are confident they can repay it, student loan debt shouldn’t be a crippling burden. More student loan insights

The economic expansion just passed the eight-year mark, and consumer credit defaults across mortgages, bankcards and auto loans are at pre–financial crisis levels. More specifically: The first-mortgage default rate dropped 4 basis points from May to 0.60%. The bankcard default rate experienced its first drop in 9 months, with a decrease of 4 basis points bringing it to 3.49%. Auto loan defaults decreased 3 basis points from the previous month to 0.82%. With inflation at 1% to 2%, debt service levels close to record lows, and disposable income increasing and supporting spending growth, consumers are in good financial shape nationally. Lenders should take this opportunity to review and adjust their acquisition strategies accordingly. Can your originations platform capitalize on this?

1 in 10 Americans are living paycheck to paycheck Financial health means more than just having a great credit score or money in a savings account. It includes being able to manage daily finances, save for the future and weather a financial shock. Here are some facts about Americans’ financial health: 46% of Americans are struggling financially. Roughly 31% of nonretired adults have no retirement savings or pension. Approximately 50% are unprepared for a financial emergency, and about 1 in 5 have no savings set aside to cover unexpected emergencies. It’s never too late for people to achieve financial health. By providing education on money management, you can drive new opportunities for increased engagement, loyalty and long-term revenue streams. Why financial health matters >

School’s out, and graduation brings excitement, anticipation and bills. Oh, boy, here come the student loans. Are graduates ready for the bills? Even before they have a job lined up? With lots of attention from the media, I was interested in analyzing student loan debt to see if this is a true issue or just a headline grab. There’s no shortage of headlines alluding to a student loan crisis: “How student loans are crushing millennial entrepreneurialism” “Student loan debt in 2017: A $1.3 trillion crisis” “Why the student loan crisis is even worse than people think” Certainly sounds like a crisis. However, I’m a data guy, so let’s look at the data. Pulling from our data, I analyzed student loan trades for the last four years starting with outstanding debt — which grew 21 percent since 2013 to reach a high of $1.49 trillion in the fourth quarter of 2016. I then drilled down and looked at just student loan trades. Created with Highstock 5.0.7Total Number of Student Loans TradesStudent Loan Total TradesNumber of trades in millions174,961,380174,961,380182,125,450182,125,450184,229,650184,229,650181,228,130181,228,130Q4 2013Q4 2014Q4 2015Q4 2016025M50M75M100M125M150M175M200MSource: Experian (function(){ function include(script, next) {var sc=document.createElement("script");sc.src = script;sc.type="text/javascript";sc.onload=function() {if (++next < incl.length) include(incl[next], next);};document.head.appendChild(sc);}function each(a, fn){if (typeof a.forEach !== "undefined"){a.forEach(fn);}else{for (var i = 0; i < a.length; i++){if (fn) {fn(a[i]);}}}}var inc = {},incl=[]; each(document.querySelectorAll("script"), function(t) {inc[t.src.substr(0, t.src.indexOf("?"))] = 1;});each(Object.keys({"https://code.highcharts.com/stock/highstock.js":1,"https://code.highcharts.com/adapters/standalone-framework.js":1,"https://code.highcharts.com/highcharts-more.js":1,"https://code.highcharts.com/highcharts-3d.js":1,"https://code.highcharts.com/modules/data.js":1,"https://code.highcharts.com/modules/exporting.js":1,"http://code.highcharts.com/modules/funnel.js":1,"http://code.highcharts.com/modules/solid-gauge.js":1}),function (k){if (!inc[k]) {incl.push(k)}});if (incl.length > 0) { include(incl[0], 0); } function cl() {if(typeof window["Highcharts"] !== "undefined"){new Highcharts.Chart("highcharts-79eb8e0a-4aa9-404c-bc5f-7da876c38b0f", {"chart":{"type":"column","inverted":true,"polar":false,"style":{"fontFamily":"Arial","color":"#333","fontSize":"12px","fontWeight":"normal","fontStyle":"normal"}},"plotOptions":{"series":{"dataLabels":{"enabled":true},"animation":true}},"title":{"text":"Student Loan Total Trades","style":{"fontFamily":"Arial","color":"#333333","fontSize":"18px","fontWeight":"bold","fontStyle":"normal","fill":"#333333","width":"792px"}},"subtitle":{"text":"","style":{"fontFamily":"Arial","color":"#666666","fontSize":"16px","fontWeight":"normal","fontStyle":"normal","fill":"#666666","width":"792px"}},"exporting":{},"yAxis":[{"title":{"text":"Number of trades in millions","style":{"fontFamily":"Arial","color":"#666666","fontSize":"16px","fontWeight":"normal","fontStyle":"normal"}},"labels":{"format":""},"type":"linear"}],"xAxis":[{"title":{"style":{"fontFamily":"Arial","color":"#666666","fontSize":"16px","fontWeight":"normal","fontStyle":"normal"},"text":""},"reversed":true,"labels":{"format":"{value:}"},"type":"linear"}],"series":[{"data":[["Total Student Loans",174961380]],"name":"Q4 2013","turboThreshold":0,"_colorIndex":0,"_symbolIndex":0},{"data":[["Total Student Loans",182125450]],"name":"Q4 2014","turboThreshold":0,"_colorIndex":1,"_symbolIndex":1},{"data":[["Total Student Loans",184229650]],"name":"Q4 2015","turboThreshold":0,"_colorIndex":2,"_symbolIndex":2},{"data":[["Total Student Loans",181228130]],"name":"Q4 2016","turboThreshold":0,"_colorIndex":3,"_symbolIndex":3}],"colors":["#26478d","#406eb3","#632678","#982881"],"legend":{"itemStyle":{"fontFamily":"Arial","color":"#333333","fontSize":"12px","fontWeight":"normal","fontStyle":"normal","cursor":"pointer"},"itemHiddenStyle":{"fontFamily":"Arial","color":"#cccccc","fontSize":"18px","fontWeight":"normal","fontStyle":"normal"},"layout":"horizontal","floating":false,"verticalAlign":"bottom","x":0,"align":"center","y":0},"credits":{"text":"Source: Experian"}});}else window.setTimeout(cl, 20);}cl();})(); Over the past four years, student loan trades grew 4 percent, but saw a slight decline between 2015 and 2016. The number of trades isn’t growing as fast as the amount of money that people need. The average balance per trade grew 17 percent to $8,210. Either people are not saving enough for college or the price of school is outpacing the amount people are saving. I shifted the data and looked at the individual consumer rather than the trade level. Created with Highstock 5.0.7Student Loan Average Balance per Trade4.044.043.933.933.893.893.853.85Q4 2013Q4 2014Q4 2015Q4 201600.511.522.533.544.5Source: Experian (function(){ function include(script, next) {var sc=document.createElement("script");sc.src = script;sc.type="text/javascript";sc.onload=function() {if (++next < incl.length) include(incl[next], next);};document.head.appendChild(sc);}function each(a, fn){if (typeof a.forEach !== "undefined"){a.forEach(fn);}else{for (var i = 0; i < a.length; i++){if (fn) {fn(a[i]);}}}}var inc = {},incl=[]; each(document.querySelectorAll("script"), function(t) {inc[t.src.substr(0, t.src.indexOf("?"))] = 1;});each(Object.keys({"https://code.highcharts.com/stock/highstock.js":1,"https://code.highcharts.com/adapters/standalone-framework.js":1,"https://code.highcharts.com/highcharts-more.js":1,"https://code.highcharts.com/highcharts-3d.js":1,"https://code.highcharts.com/modules/data.js":1,"https://code.highcharts.com/modules/exporting.js":1,"http://code.highcharts.com/modules/funnel.js":1,"http://code.highcharts.com/modules/solid-gauge.js":1}),function (k){if (!inc[k]) {incl.push(k)}});if (incl.length > 0) { include(incl[0], 0); } function cl() {if(typeof window["Highcharts"] !== "undefined"){new Highcharts.Chart("highcharts-66c10c16-1925-40d2-918f-51214e2150cf", {"chart":{"type":"column","polar":false,"style":{"fontFamily":"Arial","color":"#333","fontSize":"12px","fontWeight":"normal","fontStyle":"normal"},"inverted":true},"plotOptions":{"series":{"dataLabels":{"enabled":true},"animation":true}},"title":{"text":"Student Loan Average Number of Trades per Consumer","style":{"fontFamily":"Arial","color":"#333333","fontSize":"18px","fontWeight":"bold","fontStyle":"normal","fill":"#333333","width":"356px"}},"subtitle":{"text":"","style":{"fontFamily":"Arial","color":"#666666","fontSize":"16px","fontWeight":"normal","fontStyle":"normal","fill":"#666666","width":"356px"}},"exporting":{},"yAxis":[{"title":{"text":"","style":{"fontFamily":"Arial","color":"#666666","fontSize":"14px","fontWeight":"normal","fontStyle":"normal"}},"type":"linear","labels":{"format":"{value}"}}],"xAxis":[{"title":{"style":{"fontFamily":"Arial","color":"#666666","fontSize":"14px","fontWeight":"normal","fontStyle":"normal"}},"type":"linear","labels":{"format":"{}"}}],"colors":["#26478d","#406eb3","#632678","#982881","#ba2f7d"],"series":[{"data":[["Average Trades per Consumer",4.04]],"name":"Q4 2013","turboThreshold":0,"_colorIndex":0},{"data":[["Average Trade per Consumer",3.93]],"name":"Q4 2014","turboThreshold":0,"_colorIndex":1},{"data":[["Average Trade per Consumer",3.89]],"name":"Q4 2015","turboThreshold":0,"_colorIndex":2},{"data":[["Average Trades per Consumer",3.85]],"name":"Q4 2016","turboThreshold":0,"_colorIndex":3}],"legend":{"floating":false,"itemStyle":{"fontFamily":"Arial","color":"#333333","fontSize":"12px","fontWeight":"bold","fontStyle":"normal","cursor":"pointer"},"itemHiddenStyle":{"fontFamily":"Arial","color":"#cccccc","fontSize":"18px","fontWeight":"normal","fontStyle":"normal"},"layout":"horizontal"},"credits":{"text":"Source: Experian"}});}else window.setTimeout(cl, 20);}cl();})(); The number of overall student loan trades per consumer is down to 3.85, a decrease of 5 percent over the last four years. This is explained by an increase in loan consolidations as well as the better planning by students so that they don’t have to take more student loans in the same year. Lastly, I looked at the average balance per consumer. This is the amount that consumers, on average, owe for their student loan trades. Created with Highstock 5.0.7Balance in thousands ($)Quarterly $USD Debt per ConsumerQ4 Student Loan TrendsAverage Student Loan Debt Balance per Consumer27,93427,93429,22629,22630,52330,52332,06132,061Q4 2013Q4 2014Q4 2015Q4 201605,00010,00015,00020,00025,00030,00035,000Source: Experian (function(){ function include(script, next) {var sc=document.createElement("script");sc.src = script;sc.type="text/javascript";sc.onload=function() {if (++next < incl.length) include(incl[next], next);};document.head.appendChild(sc);}function each(a, fn){if (typeof a.forEach !== "undefined"){a.forEach(fn);}else{for (var i = 0; i < a.length; i++){if (fn) {fn(a[i]);}}}}var inc = {},incl=[]; each(document.querySelectorAll("script"), function(t) {inc[t.src.substr(0, t.src.indexOf("?"))] = 1;});each(Object.keys({"https://code.highcharts.com/stock/highstock.js":1,"https://code.highcharts.com/adapters/standalone-framework.js":1,"https://code.highcharts.com/highcharts-more.js":1,"https://code.highcharts.com/highcharts-3d.js":1,"https://code.highcharts.com/modules/data.js":1,"https://code.highcharts.com/modules/exporting.js":1,"http://code.highcharts.com/modules/funnel.js":1,"http://code.highcharts.com/modules/solid-gauge.js":1}),function (k){if (!inc[k]) {incl.push(k)}});if (incl.length > 0) { include(incl[0], 0); } function cl() {if(typeof window["Highcharts"] !== "undefined"){Highcharts.setOptions({lang:{"thousandsSep":","}});new Highcharts.Chart("highcharts-0b893a55-8019-4f1a-9ae1-70962e668355", {"chart":{"type":"column","inverted":true,"polar":false,"style":{"fontFamily":"Arial","color":"#333","fontSize":"12px","fontWeight":"normal","fontStyle":"normal"}},"plotOptions":{"series":{"dataLabels":{"enabled":true},"animation":true}},"title":{"text":"Average Student Loan Balance per Consumer","style":{"fontFamily":"Arial","color":"#333333","fontSize":"18px","fontWeight":"bold","fontStyle":"normal","fill":"#333333","width":"308px"}},"subtitle":{"text":"","style":{"fontFamily":"Arial","color":"#666666","fontSize":"16px","fontWeight":"normal","fontStyle":"normal","fill":"#666666","width":"792px"}},"exporting":{},"yAxis":[{"title":{"text":"Balance numbers are in thousands ($)","style":{"fontFamily":"Arial","color":"#666666","fontSize":"16px","fontWeight":"normal","fontStyle":"normal"}},"labels":{"format":"{value:,1f}"},"reversed":false}],"xAxis":[{"title":{"style":{"fontFamily":"Arial","color":"#666666","fontSize":"16px","fontWeight":"normal","fontStyle":"normal"},"text":"Balance in thousands ($)"},"labels":{"format":"{value:}"},"type":"linear","reversed":true,"opposite":false}],"series":[{"data":[["Average Balance per Consumer",27934]],"name":"Q4 2013","turboThreshold":0,"_colorIndex":0},{"data":[["Average Balance per Consumer",29226]],"name":"Q4 2014","turboThreshold":0,"_colorIndex":1},{"data":[["Average Balance per Consumer",30523]],"name":"Q4 2015","turboThreshold":0,"_colorIndex":2},{"data":[["Average Balance per Consumer",32061]],"name":"Q4 2016","turboThreshold":0,"_colorIndex":3}],"colors":["#26478d","#406eb3","#632678","#982881"],"legend":{"itemStyle":{"fontFamily":"Arial","color":"#333333","fontSize":"12px","fontWeight":"bold","fontStyle":"normal","cursor":"pointer"},"itemHiddenStyle":{"fontFamily":"Arial","color":"#cccccc","fontSize":"18px","fontWeight":"normal","fontStyle":"normal"}},"lang":{"thousandsSep":","},"credits":{"text":"Source: Experian"}});}else window.setTimeout(cl, 20);}cl();})(); Here we see a growth of 15 percent over the last four years. At the end of 2016, the average person with a student loan balance had just over $32,000 outstanding. While this is a large increase, we should compare it with other purchases: This balance is no more than a person purchasing a brand-new car without a down payment. While we’re seeing an increase in overall outstanding debt and individual loan balances, I’m not yet agreeing that this is the crisis the media portrays. If students are educated about the debt that they’re taking out and making sure that they’re able to repay it, the student loan market is performing as it should. It’s our job to help educate students and their families about making good financial decisions. These discussions need to be had before debt is taken out, so it’s not a shock to the student upon graduation.

There’s a new crew coming of age. Enter Generation Z. Gen Z — those born between the mid-1990s and the early 2000s — makes up one-quarter of the U.S. population. By 2020, they’ll account for 40% of all consumers. The oldest members of this next cohort — 18- to 20-year-olds — are coming of age. Here are some insights on how this initial segment of Gen Z is beginning to use credit. Credit scores averaged 631 in 2016. Debt levels — consisting largely of bankcards and auto and student loans — are low, with an average debt-to-income ratio of just 5.7%. Average income is $33,800. This generation is being raised in an era of instant, always-on access. They expect a quick, seamless and customized mobile experience. You have just 8 seconds to capture their attention. Webinar: A First Look at Gen Z and Credit