Latest Posts

In this blog post, we explore the empowering impact of income and employment verification on financial institutions.

Using alternative data for credit underwriting is a modern and efficent approach to a risk-based credit approval strategy Read more!

A new Experian report highlights the top four digital audience categories for the automotive industry and specific audiences auto marketers can leverage.

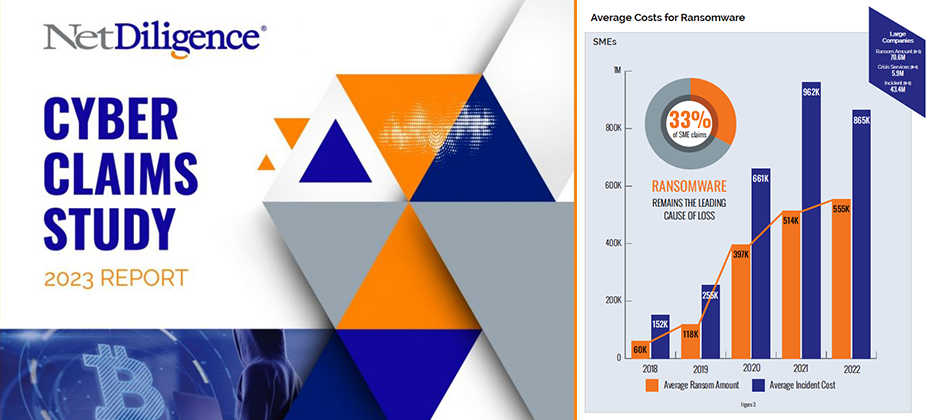

Review of Findings & Front-line Insights Panel Participants: Richard Goldberg (Moderator) – Constangy, Brooks, Smith & Prophete, LLP Michael Bruemmer – Experian Sean Renshw – RSM US, LLP Mark Greisiger – NetDiligence About NetDiligence Cyber Claims Study It is NetDiligence’s 13th year of doing this Cyber Claims Study. A total of 9,028 claims were analyzed during the past five years 2018-2022.An observation from the over 9,000 Cyber Claims (5000 of which are brand new claims this past year in 2023) analyzed is while many of the categories over the last five years have remained the same, the data has changed, sometimes dramatically. About Experian We provide call center coverage, notification coverage, as well as, identity theft protection, and all the consumer resolutions that go along with it for about 5000 data breaches every year, and I was delighted to be on the panel. Key Insights Experian has proudly sponsored the annual NetDiligence Cyber Claims Study for three years. During this time, I’ve witnessed companies adapt and transform their operations to confront the growing tide of cyber threats. The evolution of their infrastructure to anticipate and respond to these challenges has been remarkable and necessary. However, despite my front-row seat in this fast-changing landscape, the results of each study never fail to surprise and intrigue me. The insights from the latest study, conducted in 2023, continue to shape our understanding of the evolving cyber landscape. Ransomware’s Dominance Mark kicked off the discussion by shedding light on the escalating costs associated with cyber incidents. In 2022, the average incident cost for SME organizations remained stable at $169,000 (similar to the combined five-year window from 2018 to 2022 at about 175,000). However, there was a substantial increase for large companies, reaching $20.3 million in 2022 (and if you look at the five-year average, it was about 13 million). This surge raised eyebrows and set the stage for a deep dive into ransomware, a leading cause of concern. Examining Ransomware Trends The conversation swiftly shifted to ransomware, a pervasive threat in the cyber insurance landscape. As I stated, at Experian we see a correlation between the rise in ransomware and third-party breaches. Most of the industry experts on the panel participate in a Ransomware Advisory Group together. Mark brought up a good insight from our advisory group on the brazen tactics employed by threat actors lately, showcasing their intimate knowledge of the cyber insurance world. Business Sectors Under Siege Richard and Sean added to the discussion the top ten business sectors affected by ransomware, with professional services leading the pack. The impact on technology, with a payout of $830,000, stood out as well. Beyond Ransomware The conversation broadened to encompass other types of losses, such as social engineering and business email compromise. The focus on business interruption emerged as a key concern for cyber insurance claims, with the industry grappling with criminal acts versus non-criminal acts. Looking Ahead As the discussion unfolded, industry experts, including myself, expressed eagerness to anticipate the future cyber landscape. Predictions range from the industry mutating to the emergence of new players in the nation-state game. The role of artificial intelligence and innovative solutions from new vendors becomes a focal point of interest. In conclusion, the NetDiligence Cyber Claims Study 2023 Report paints a vivid picture of the challenges and transformations within the cyber insurance domain. The increasing sophistication of threat actors, coupled with evolving business strategies, sets the stage for continuous adaptation and innovation in the fight against cyber threats. As we look ahead, the resilience of businesses and the collaboration between industry stakeholders will play a pivotal role in shaping the cybersecurity landscape. I invite you to access the report and view the discussion replay for a deeper understanding of the challenges and transformations within the cyber insurance claims domain. Get NetDiligece Cyber Claims Study resources on-demand now! Download the report Watch the webinar NetDiligence’s latest Cyber Claims Study and Webinar, sponsored by Experian Data Breach, is available on-demand. This report serves as a resounding call to action, prompting businesses to ready themselves against cyber threats. Dive in to get insights and stay one step ahead of cyber adversaries.

With rapid growth comes an increased risk of fraud, making "Buy Now, Pay Never" a crucial fraud threat to watch out for in 2024.

Companies depend on quality information to make decisions that move their business objectives forward while minimizing risk exposure. And in today’s modern, tech-driven, innovation-led world, there’s more information available than ever before. Expansive datasets from sources, both internal and external, allow decision-makers to leverage a wide range of intelligence to fuel how they plan, forecast and set priorities. But how can business leaders be sure that their data is as robust, up-to-date and thorough as they need — and, most importantly, that they’re able to use it to its fullest potential? That’s where the power of advanced analytics comes in. By making use of cutting-edge datasets and analytics insights, businesses can stay on the vanguard of business intelligence and ahead of their competitors. What is advanced analytics? Advanced analytics is a form of business intelligence that takes full advantage of the most modern data sources and analytics tools to create forward-thinking analysis that can help businesses make well-informed, data-driven decisions that are tailored to their needs. Simply put, advanced analytics is an essential component of any proactive business strategy that aims to maximize the future potential of both customers and campaigns. These advanced business intelligence and analytics solutions help leaders make profitable decisions no matter the state of the current economic climate. They use both traditional and non-traditional data sources to provide businesses with actionable insights in the formats best suited to their needs and goals. One key aspect of advanced analytics is the use of AI analytics solutions. These efficient and effective tools help businesses save time and money by harnessing the power of cutting-edge technologies and deploying them in optimal use-case scenarios. These AI and machine-learning solutions use a wide range of tools, such as neural network methodologies, to help organizations optimize their allocation of resources, expediting and automating some processes while creating valuable insights to help human decision-makers navigate others. Benefits of advanced analytics Traditional business intelligence tends to be limited by the scope and quality of available data and ability of analysts to make use of it in an effective, comprehensive way. Modern business intelligence analytics, on the other hand, integrates machine learning and analytics to maximize the potential of data sets that, in today's technology-driven world, are often overwhelmingly large and complex: think not just databases of customer decisions and actions but behavioral data points tied to online and offline activity and the internet of things. What's more, advanced analytics does this in a way that's accessible to an entire organization — not just those who know their way around data, like IT departments and trained analysts. With the right advanced analytics solution, decision-makers can access convenient cloud-based dashboards designed to give them the information they want and need — with no clutter, noise or confusing terminology. Another key advantage of advanced analytics solutions is that they don't just analyze data — they optimize it, too. Advanced analytics offers the ability to clean up and integrate multiple data sets to remove duplicates, correct errors and inaccuracies and standardize formats, leading to high-quality data that creates clarity, not confusion. The result? By analyzing and identifying relationships across data, businesses can uncover hidden insights and issues. Advanced analytics also automate some aspects of the decision-making process to make workflows quicker and nimbler. For example, a business might choose to automate credit scoring, product recommendations for existing customers or the identification of potential fraud. Reducing manual interventions translates to increased agility and operational efficiency and, ultimately, a better competitive advantage. Use cases in the financial services industry Advanced analytics gives businesses in the financial world the power to go deeper into their data — and to integrate alternative data sources as well. With predictive analytics models, this data can be transformed into highly usable, next-level insights that help decision-makers optimize their business strategies. Credit risk, for instance, is a major concern for financial organizations that want to offer customers the best possible options while ensuring their credit products remain profitable. By utilizing advanced analytics solutions combined with a broad range of datasets, lenders can create highly accurate credit risk scores that forecast future customer behavior and identify and mitigate risk, leading to better lending decisions across the credit lifecycle. Advanced analytics solutions can also help businesses problem-solve. Let's say, for instance, that uptake of a new loan product has been slower than desired. By using business intelligence analytics, companies can determine what factors might be causing the issue and predict the tweaks and changes they can make to improve results. Advanced analytics means better, more detailed segmentation, which allows for more predictive insights. Businesses taking advantage of advanced analytics services are simply better informed: not only do they have access to more and better data, but they're able to convert it into actionable insights that help them lower risk, better predict outcomes, and boost the performance of their business. How we can help Experian offers a wide range of advanced analytics tools aimed at helping businesses in all kinds of industries succeed through better use of data. From custom machine learning models that help financial institutions assess risk more accurately to self-service dashboards designed to facilitate more agile responses to changes in the market, we have a solution that's right for every business. Plus, our advanced analytics offerings include a vast data repository with insights on 245 million credit-active individuals and 25 million businesses, as well as the industry's largest alternative data set from non-traditional lenders. Ready to explore? Click below to learn about our advanced analytics solutions. Learn more

Are you ready to talk football? And read some Taylor Swift puns? And hear about a big automotive ad measurement success story? 'Don’t Blame Me’, I warned you…. As we are all aware, Travis Kelce will be playing for the Chiefs on Superbowl Sunday. Whether you are cheering for the Chiefs, the 49er’s, or you’re just there to watch the commercials and half-time show, ‘You Need to Calm Down’ and just expect to hear a couple references during the game about Taylor and Travis’ ‘Love Story’. Ad Measurement at the Top of Its Game Before the final match-up of this season though, let’s go ‘Back to December’ and talk about a “Red” hot advertising success story from Thursday Night Football. An automotive advertiser wanted to better understand the impact of advertising frequency on vehicle purchase activity. To do this, the advertiser initiated an Amazon Prime streaming advertising campaign to reach Thursday Night Football (TNF) audience viewers. They reached these viewers by leveraging in-game media to raise awareness with new and TNF-engaged audience viewers. In addition, the advertiser used remarketing techniques and other Amazon ads to re-engage the previously exposed TNF viewers. Campaign Results—More Than Just Karma! After the campaign was over, the automotive advertiser wanted to learn whether the results were more than just ‘Karma’. They used Experian’s Vehicle Purchase Insights data within Amazon Marketing Cloud (AMC) to fill in the ‘Blank Space’ and attribute vehicle sales to the exposed TNF audience. Customers exposed 2-3 times to their ads were 1.3X more likely to purchase a vehicle than viewers who were exposed to the advertising only once Customers exposed to their ads 4 times were 1.6X more likely to purchase a vehicle than viewers who were exposed to the advertising only once The advertiser understood ‘All Too Well’ the results, the campaign was a success! Even if you’re over all the pop culture references and the Swift romance, ‘Shake it Off’, there’s no reason for any ‘Bad Blood.” The ‘Fearless’ leader of the scoreboard will have their ‘Wildest Dreams’ come true and be named the Super Bowl LVIII champion. To read more about this case study, (without the Taylor Swift song title puns), click here.

The future of credit underwriting will depend on advanced analytics that can draw conclusions from vast amounts of data.

Ryan Coyne recently participated in a panel with industry experts, delving into third-party cyber risks and mitigation strategies.

Enterprise identity management helps companies manage their customers' digital identities and information.

Auto dealerships may sell dreams of open roads and freedom, but unfortunately, they also attract a different kind of customer: the identity thief. With high-value transactions and access to sensitive personal information, auto dealerships are prime targets for various fraudulent schemes. So, buckle up as we explore the most common types of identity fraud impacting dealerships and how to keep your wheels safe. Four common fraud schemes dealers need to be aware of 1. Third-Party Identity Fraud (Stolen Identities): Hijacking the Identity Highway This method doesn't involve creating new identities; it steals existing ones. Thieves steal personal information, often through data breaches or phishing scams, and use it to apply for auto loans under the victim's name. The dealership unwittingly approves the loan, leaving the real person saddled with the debt and a ruined credit score. 2. Synthetic Identity (Fabricated Credentials): Frankenstein Fraud on the Fast Lane Think of synthetic identity fraud as identity theft with a twist. Criminals combine real and fake information, like stolen Social Security numbers and fabricated addresses, to create entirely new personas. These fabricated identities then build clean credit histories, allowing them to qualify for high-value loans like car financing. By the time the dealership realizes the fraud, the car, and the fake persona have vanished. 3. First Party: No Way Will I Pay This method doesn't involve creating new identities; rather it is when a person knowingly misrepresents their identity or gives false information for financial or material gain. Fraudsters often have no plans to pay for their vehicle. 4. Document Fraud: Paper Trails of Deception Fraudsters can also manufacture fake or altered documents like driver's licenses, proof of income and employment verification. These forged documents create a veneer of legitimacy, allowing them to bypass dealership verification checks and secure loans based on fabricated information. Four ways dealerships can keep their brakes on fraud 1. Robust verification: Implementing multi-factor authentication, cross-referencing information with reliable sources, and verifying documents with advanced technology can significantly reduce the risk of deception. Fraud Protect™ from Experian Automotive leverages license scanning and selfie capture to verify identity. Dealers can find the true person and verify the activity through device, behavior, and step-up services. 2. Employee vigilance: Training staff to identify suspicious behavior and report potential fraud attempts can create a strong internal defense system. Fraud Protect fits within your current systems and processes. The software integrates with your CRM and does not require heavy software training or any additional hardware simplifying employee usage. 3. Secure data: Investing in data security measures like encryption and access controls can significantly deter hackers and minimize the damage from data breaches. Fraud Protect leverages Experian’s world-class data to handle the customer relationship carefully and detect errors and discrepancies. 4. Partnerships: Collaborating with credit bureaus, law enforcement agencies and fraud prevention systems can provide valuable insights and resources for fighting fraud. Experian is the world’s leading information services company. Fraud Protect from Experian Automotive offers a unique partnership for dealers through seamless CRM integration. This simple process makes multiple levels of risk identification quick and efficient for busy buyers. By acknowledging the various forms of identity fraud and implementing proactive measures, dealerships can protect themselves and their consumers from the impact of identity fraud. Fraud Protect empowers dealers with our leading fraud, identity and verification capabilities, integrated within your unique workflows. Whether on your website, leveraged before test drives, initiating out-of-state & and remote closings, or before contracting, Fraud Protect quickly uncovers potential fraud. The entire process is a quick and painless way to address risk while establishing customer trust. Take the first step in protecting profits and preventing fraud by visiting our auto fraud prevention solutions webpage.

Learn how third-party collections can benefit from modern technology to improve recovery rates and compliance.

With automated income verification, lenders can approve more applicants quickly and provide exceptional digital experiences. Learn more!

We've released our 11th annual Experian 2024 Data Breach Industry Forecast to embark on a journey into the future of data breaches.

This report provides a snapshot of the top monthly economic and credit data, including student loans, consumer spending, and delinquencies.