Latest Posts

The ongoing COVID-19 pandemic has facilitated an increase in information collection among consumers and organizations, creating a prosperous climate for cybercriminals. As businesses and customers adjust to the “new normal,” hackers are honing in on their targets and finding new, more sophisticated ways to access their sensitive data. As part of our recently launched Q&A perspective series, Michael Bruemmer, Experian’s Vice President of Data Breach Resolution and Consumer Protection, provided insight on emerging fraud schemes related to the COVID-19 vaccines and how increased use of digital home technologies could lead to an upsurge in identity theft and ransomware attacks. Check out what he had to say: Q: How did Experian determine the top data breach trends for 2021? MB: As part of our initiative to help organizations prevent data breaches and protect their information, we release an annual Data Breach Forecast. Prior to the launch of the report, we analyze market and consumer trends. We then come up with a list of potential predictions based off the current climate and opportunities for data breaches that may arise in the coming year. Closer to publication, we pick the top five ‘trends’ and craft our supporting rationale. Q: When it comes to data, what is the most immediate threat to organizations today? MB: Most data breaches that we service have a root cause in employee errors – and working remotely intensifies this issue. Often, it’s through negligence; clicking on a phishing link, reusing a common password for multiple accounts, not using two-factor authentication, etc. Organizations must continue to educate their employees to be more aware of the dangers of an internal breach and the steps they can take to prevent it. Q: How should an organization begin to put together a comprehensive threat and response review? MB: Organizations that excel in cybersecurity often are backed by executives that make comprehensive threats and response reviews a top corporate priority. When the rest of the organization sees higher-ups emphasizing the importance of fraud prevention, it’s easier to invest time and money in threat assessments and data breach preparedness. Q: What fraud schemes should consumers be looking out for? MB: The two top fraud schemes that consumers should be wary of are scams related to the COVID-19 vaccine rollout and home devices being held for ransom. Fraudsters have been leveraging social media to spread harmful false rumors and misinformation about the vaccines, their effectiveness and the distribution process. These mistruths can bring harm to supply chains and delay government response efforts. And while ransomware attacks aren’t new, they are getting smarter and easier with people working, going to school and hosting gatherings entirely on their connected devices. With control over home devices, doors, windows, and security systems, cybercriminals have the potential to hold an entire house hostage in exchange for money or information. For more insight on how to safeguard your organization and consumers from emerging fraud threats, watch our Experian Symposium Series event on-demand and download our 2021 Data Breach Industry Forecast. Watch now Access forecast About Our Expert: Michael Bruemmer, Experian VP of Data Breach Resolution and Consumer Protection, North America Michael manages Experian’s dedicated Data Breach Resolution and Consumer Protection group, which aims to help businesses better prepare for a data breach and mitigate associated consumer risks following breach incidents. With over 25 years in the industry, he has guided organizations of all sizes and sectors through pre-breach response planning and delivery.

Experian's Q4 2020 State of the Automotive Finance Market report gives insight into the current state of the leasing market.

The Q4 2020 State of the Automotive Finance Market report zooms in to get a better picture of the alternative fuel marketplace.

Preventing fraud losses requires an understanding of each individual fraud type—including third-party, first-party, synthetic identity, and account takeover fraud—and how they differ from one another. It’s only with a multi-layered fraud strategy that businesses can adequately detect and treat each type of fraud while maintaining the customer experience. When’s the last time you reviewed your existing fraud strategy? Download infographic Review your fraud strategy

Experian is proud to announce, for the second year in a row, we have been named to the global Fintech Leaders list, placing in the top 20 for 2021. The list and adjoining report are released annually by international research organization, the Center for Financial Professionals (CeFPro). In addition to placing 19th on the list, Experian also placed in the Credit Risk category. The Center for Financial Professionals’ Fintech Leaders 2021 Report is one of the most rigorous programs that rank fintech industry leaders. The report’s coverage includes evaluating top fintech companies, solution providers, and vendors. The results are usually based on gathered surveys from end-users, practitioners, and subject matter experts. CeFPro’s report comes from the group’s market analysis and original research, which are backed by an advisory board that consists of 60 international industry professionals. Andreas Simou, CeFPro’s Managing Director, shared that the CeFPro board and voting members recognized Experian within the fintech survey as leaders for their data, decisioning and analytical capabilities. Simou said, "Experian cements its place on the Fintech Leaders List, and has once again been very highly regarded, as a leading player within credit risk, most notably for their subject-matter expertise and excelling within the areas of data management and modelling,” he said. “We are honored to once again be recognized as a Fintech Leader by CeFPro and the global Fintech marketplace,” said Jon Bailey, Vice President for Fintech at Experian. “We are committed to supporting the Fintech community and we will continue to invest and innovate to help our clients solve problems, create opportunities, and promote financial inclusion,” Bailey said.

Since 2002, lenders have been aware of the importance of Know Your Customer (KYC) and the associated Customer Identification Program (CIP) requirements. As COVID-19 has changed procedures and priorities for businesses and consumers across the board, it’s more important than ever for institutions to ensure their CIP process includes ongoing monitoring of identity risk. What is CIP? Standard KYC programs include a Customer Identification Program to verify and validate identities along with due diligence to assess the risks associated with each identity. CIP defines the process by which a business collects data to establish a reasonable belief that the identity is valid, and that the individual is eligible to participate in our financial system. While this process works in conjunction with other fraud mitigation tactics, they serve different purposes. A good CIP program emphasizes the customer experience, regulatory compliance, cost control, and smart growth. Fraud mitigation focuses on ensuring that an eligible identity is being presented by its true owner, rather than as part of a scheme to acquire goods and services with intent to default on repayment obligations. Businesses who focus on solely on fraud mitigation rather than complying with KYC and CIP regulations run the risk of potential harm to business reputation, and of course, financial penalties. Fenergo found that as of the end of 2019, global penalties for AML and KYC non-compliance totaled $36 billion. CIP vs. Fraud Mitigation Many financial institutions equate a CIP program with efforts to mitigate fraud. It’s understandable, as both processes include emphasis on the accuracy of an identity as it’s presented by a consumer. It is assumed that only the true owner of the identity would possess the detailed information necessary to meet CIP requirements and therefore would not likely be committing fraud. There was a time—prior to large scale thefts of stored information, personal details shared through social media and other behavior changes that made personal information very public—when this would have been true. Unfortunately, those days have passed and even an amateur criminal with limited experience and resources could find current, accurate identity information for sale online, information good enough to pass the CIP test and be considered a legitimate consumer. The real challenge is that when they go through CIP, many real consumers may inadvertently provide true information that doesn’t meet the verification standard. This is a result of consumer lifestyle changes outpacing the sources of data used to verify the information they’ve provided. It makes sense; in most years roughly 13% of American adults change their address. New homes, job changes and changes in marital status impact a large number of people every day. Adding to the confusion—it’s life’s changes that prompt people to borrow and purchase. The result is that many of the people that are more likely to fail CIP verification are the very people trying to legitimately access financial services. The result is that CIP verification often isn’t a challenge for those intending to commit fraud, but it can be for genuine consumers. The challenges of CIP In a recent internal study, Experian reviewed the ability to pass a standard CIP strategy that assessed the accuracy of the name, current address, date of birth and Social Security number provided by a large sample of consumers. We then compared legitimate consumers to those later confirmed to have been identity thieves impersonating a victim. Consistently, the identity thieves were at least as proficient at passing CIP as their true-consumer counterparts. In a second step, we applied a fraud score that looked for identity theft by assessing the past uses of the identities, their consistency, velocity and many other characteristics unrelated to the accuracy of the data. The difference between CIP verification and a fraud risk assessment was striking. Across the entire range of fraud risk, the percentage of records that passed CIP verification remained the same. That said, CIP still plays a very important role in risk mitigation. In fact, CIP and fraud prevention are inextricable in financial services. Just as a CIP verified identity can still be fraud, a record that may appear to be low fraud risk may not pass CIP. Since both processes have existed side by side for nearly two decades, each presumes that the other is in place and both are necessary to detect and prevent fraud. Striking a balance CIP verification and fraud mitigation strategies are both necessary and important to protecting assets and the broader financial system from fraud. It’s important to leverage a layered approach where both eligibility and risk are assessed, and next steps for verification include resolution of identity discrepancies alongside verification that ensures an identity is not being misused for fraud. Experian can help you confidently verify customer identities, understand and anticipate customer activities, and implement ongoing monitoring. If you’d like to set up a review of your current strategy or learn more about how we can help you with CIP and fraud mitigation to strengthen your ability to know your customer compliantly, let us know. Contact us

According to Experian’s latest Global Insights Report, 38% of consumers expect to increase their online activity in the next 12 months. The report also found that consumers continue to have high expectations for their online experience, and businesses are re-imagining the customer journey to reflect that need. This January, Experian surveyed 3,000 consumers and 900 businesses to explore the changes in consumer behavior and business strategy pre- and post-COVID-19. As consumers have embraced life online, they’ve continued to emphasize their feelings regarding the importance of protecting their information. More than half of consumers still consider security to be the most important factor in their digital experience – the same experience they have such high expectations of. Business are acting in turn, with more than half investing in fraud detection methods or software to reduce friction in the customer experience. Digital transformation is also highlighting the need to: Manage regulatory compliance Integrate security measures Ensure access to AI models Attract and manage customers Integrate automation solutions Download the report to get all the latest insights into consumer desires and business behaviors, and keep visiting the Insights blog for a deeper dive into US-specific findings. Download report

When I worked as a junior analyst for one of the largest credit card issuers in the United States, the chief credit risk officer required the development of a “light switch report” and strongly encouraged everyone in her organization to read the report every day. She called it the light switch report because every morning when she walks into her office and the lights switch on, she would read the report and understand what’s going on with the business. I took her advice and developed the habit of reading the light switch report every morning — for more than a decade while I was with the organization. I knew the volume of applications, the approval rate and the average line of credit of approvals. I developed an informed idea of how delinquency rates would look six months into the future based on the average credit score of approvals today. Her advice was valuable, and the discipline she shared helped me develop my skill sets as a junior analyst, a people manager and head of a retail business line. Performance reports are foundational and are one of the key elements of a sound and prudent risk management framework. Regulators require effective monitoring reports and provide guidance on report generation as part of its examination process. (Office of the Comptroller of the Currency. Comptroller’s Handbook, Retail Lending Safety and Soundness. April 2017. Page 15.) While supporting lender clients on strategy designs and development, I have an opportunity to review various performance reports. I’d like to take this time to reiterate some of the basic components of a good performance report. Knowledge of audience is primary. Good performance reports are tailored for specific audiences who can make decisions that will affect specific outcomes. Performance reports for day-to-day monitoring would be different from reports designed for executive leadership. Transparency and accuracy are required and when reports are designed in support of areas of responsibility, those reports become meaningful and transformative. Relevant metrics matter. Once you identify the report’s audience, the metrics you choose to appear in the report become the next important exercise. Metrics should be relevant and consistent with the audience who’s expected, upon reviewing the report, to make statements such as the business is doing well and stable, or corrective action is needed. For example, a report on the predictive power of credit risk scores intended for model developers will likely contain metrics such Kolmogorov-Smirnov (KS), Gini index or worst scoring capture rate. Such reports won’t include the average handling time of an application, which will be more appropriate for an operations team. Metrics become even more powerful for decision-makers when calculated at a segment level. I’m a big fan of vintage reports. They tell the story of current lending practices (e.g., approval rates, average loan amount, average booked credit risk score), and more significantly they often foretell future performance (e.g., delinquency rates, charge-off rates). These foresights allow analysts and managers to plan and develop strategies today to manage the future state. If approve or decline decisions use a dual score matrix, generate a report showing the volume of applications on the dual score matrix. It’s quicker to spot unusual distributions compared to expectations when data is presented at this sublevel. The benefit is swifter modification or new actions when needed. If statistical designs are utilized, such as test or control segments and champion or challenger segments, metrics calculated at these levels become insightful. They allow validation of a randomized process and support statistical analysis and statements. Timeliness of reports is critical. Some reports for operational or technology purposes require constant and continuous reporting. Daily reports are important especially when new strategies are implemented. Sometimes daily reports are far more relevant within the first two or three weeks of a new strategy implementation. When daily reports show stabilization and alignment to expectations, switching to weekly or monthly reports is acceptable. Most retail products are designed for review on a cycle or monthly basis. Monthly and quarterly reports are milestones and provide good health checks of the business. Don’t forget formats. If a picture is worth a thousand words, then use charts and graphs to display data and capture audience attention. We’re all used to seeing data presented in tables, but there are far more applications today that allow us to read reports with compelling graphics, trendlines and patterns that grab our curiosity and draw us into the story. I like narratives even if they appear as headlines on a report. Succinct comments show discipline and convey understanding of a report’s contents. Effective performance reports evolve as the business changes. Audience, metrics and segments will change, but the basic components provide general guidelines on developing consistent and relevant reports.

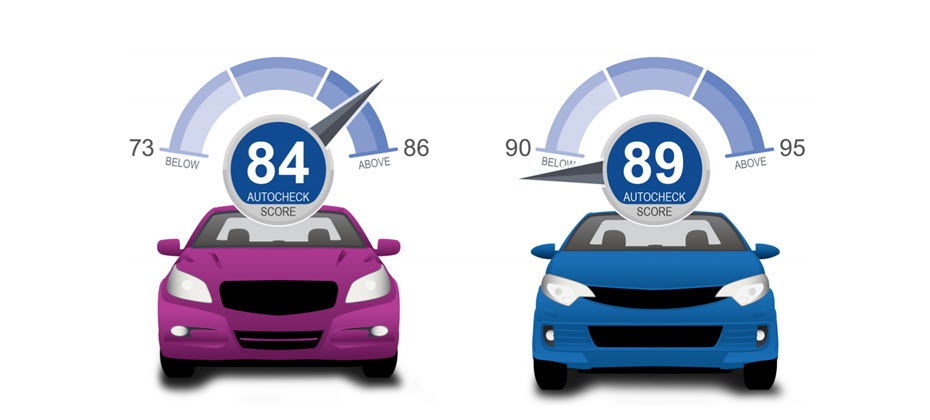

Do you know what the patented AutoCheck Score represents? The AutoCheck Score predicts the likelihood an individual vehicle will be on the road in five years.

Over the last several weeks, I’ve shared articles about the problems surrounding third-party, first-party and synthetic identity fraud. To wrap up this series, I’d like to talk about account takeover fraud and how digital transformation has impacted it over the last year. What is account takeover fraud? Account takeover fraud is a form of identity theft that involves unauthorized access to a user’s online accounts to enable financial crimes. Criminals can obtain information in a number of ways, including the dark web, spyware and malware, and phishing to allow them to make unauthorized transactions with the user’s account. Fraudsters have made efforts to also gain control of mobile or email accounts so they can intercept one-time passwords or password change instructions to retain control of the account. Once fraudsters have control of one account, they can use it to access other personal information to breach additional accounts and graduate to full-scale identity theft. How does account takeover fraud impact me? Account takeover fraud is damaging to businesses and consumers. It leads to losses and well as resources invested to confirm fraud. The potential losses from account takeover fraud have spiked over the last year, in large part due to the opportunities created by the rapid increase of digital interactions and the influx of users interacting with merchants and financial institutions online for the first time. Aite research shows that 64% of financial institutions are seeing higher rates of ATO fraud attacks now than prior to the pandemic. – Trace Fooshee, Senior Analyst, Aite Group1 Account takeover can also be difficult to detect. Unlike credit card fraud where the true owner might quickly notice suspicious charges, an account takeover attack can go undetected for long periods of time. That’s because the criminal can change login and contact information, ensuring that the real accountholder doesn’t realize they’ve been compromised immediately. Solving the account takeover fraud problem A good account takeover fraud prevention strategy requires two things: frictionless customer experience and robust risk management. It’s clear that customers expect seamless interactions with merchants and lenders. At the same time, businesses need to be able to spot risky or suspicious behavior before a bad transaction occurs. That’s where a layered fraud management solution comes into play. With the right tools—including risk-based identity and device authentication and targeted step-up authentication—businesses can provide a good customer experience and only pull in staff for deeper investigations where necessary. With this strategy in place, businesses can easily recognize good customers and provide a more personalized experience, while at the same time combatting fraud – boosting growth and minimizing losses in the long run. I hope this series has helped provide insights into the different types of fraud and why each of them requires different treatment. To learn more about the risks of account takeover and how a layered fraud management solution can help protect your business and your customers, feel free to contact us. 1Key Trends Driving Fraud Transformation in 2021 and Beyond, Aite Group, December 2020

The ongoing COVID-19 crisis and the associated rise in online transactions have made it more important than ever to keep customer information accurate and company databases up to date. By ensuring your organization’s data quality, you can allocate resources more effectively, minimize costs and safely serve your customers. As part of our recently launched Q&A perspective series, Suzanne Pomposello, Experian’s Strategic Account Director for CEM vertical markets, and William Palmer, Senior Sales Engineer, provided insight on how utility providers can manage and maintain accurate client data during system migrations and modernizations, achieve a single customer view and implement an operational data quality program. Check out what they had to say: Q: What are the best practices for effective data quality management that utility providers should follow? SP: To ensure data quality, we advise starting with a detailed understanding of the data your organization is currently maintaining and how new data entering your systems is being utilized. Conducting a baseline assessment and being able to properly validate the accuracy of your data is key to identifying areas that require cleansing and enrichment. Once you know what improvements and corrections need to be made, you can establish a strategy that will empower your organization to unlock the full potential of your data. Q: How does Experian help clients improve their data hygiene? SP: Experian has over 30 years of expertise in data cleansing, which is tapped to help clients deploy tactics and strategies to ensure an acceptable level of data integrity. First, we obtain a complete picture of each organizations objectives and challenges. We then assess the quality of their data and identify sources that require remediation. Armed with insight, we work alongside organizations to develop a phased action plan to standardize and enhance their data. Our data management solutions satisfy a wide range of needs and can be consumed in real-time, bulk and batch form. Q: Are there any protection regulations to be aware of when obtaining updated data? WP: Unlike Experian’s regulated divisions, most Experian Data Quality data elements are not burdened by complex regulations and restrictions. Our focus is on organizations’ main customer data points (e.g., address, email address and phone). We reference this data against unregulated source systems to validate, append and complete customer profiles. Experian’s data quality management tools can serve as a foundation for many regulatory, compliance and governance requirements, including, Metro 2 reporting, TCPA and CCPA. Q: Are demos of Experian’s data management solutions available? If so, where can they be accessed? WP: Yes, you can visit our website to view product functionality clips and recorded demonstrations. Additionally, we welcome the opportunity to explore our comprehensive data quality management tools via tests and live demonstrations using actual client data to gain a better understanding of how our solutions can be used to improve operational efficiency and the customer experience. For more insight on how to cleanse, standardize, and enhance your data to make sure you get the most out of your information, watch our Experian Symposium Series event on-demand. Watch now Learn more About Our Experts: Suzanne Pomposello, Strategic Account Director, Experian Data Quality, North America Suzanne manages the energy vertical for Experian’s Data Quality division, supporting North America. She brings innovative solutions to her clients by leveraging technology to deliver accurate and validated contact data that is fit for purpose. William Palmer, Senior Sales Engineer, Experian Data Quality, North America William is a Senior Sales Engineer for Experian’s Data Quality division, supporting North America. As an expert in the data quality space, he advises utility clients on strategies for immediate and long-term data hygiene practices, migrations and reporting accuracy.

Inactive credit card accounts are defined as credit cards that were approved, opened and never used by account holders. They also include credit card accounts that were approved, opened, utilized by account holders but don’t have a balance for the last six to 12 months. Inactive credit card accounts pose several challenges and opportunities to lenders. A review of inactivity rates of credit card portfolios of credit unions across the United States as of March 2018 shows that inactive accounts comprise approximately 11 percent of total accounts on the books. The average credit line of inactive accounts is $8,700. (Data were extracted from Experian’s File One™ database using a sample of credit card accounts with credit unions across the United States as of March 2018. Sample size is approximately 600,000 credit card accounts.) Why do credit card accounts become inactive? One potential reason for inactivity is the convenience of securing a credit card during demand deposit account (“DDA”) opening processes. Lenders today may prequalify or preselect a customer quickly and efficiently for a credit card while a customer’s request to open a checking account or deposit account is being processed. Lenders benefit from this choreographed process with no to very minimal additional effort and time requested from the customer. The removal or significant decrease in friction costs — such as requiring additional customer information that previously would have deterred a customer from proceeding with the credit card application — gave lenders the advantage of processing more applications. (Schruder, Kyle. Feb. 26, 2018. The Top 5 Behavioural Economics Principles for Designers — Bridgeable blog. https://uxplanet.org/the-top-5-behavioural-economics-principles-for-designers-ea22a16a4020.) Because of this convenience, some customers say yes to obtaining a credit card even though they had no intention of securing one in the first place. In behavioral economics, this may be identified as the “yeah, whatever” heuristic. People take the option with the least effort or the path of least resistance. (Thaler, Richard H. and Cass R. Sunstein. 2009. Nudge Improving Decisions About Health, Wealth, and Happiness. New York: Penguin Books. Pages 35, 85.) With low commitment to the credit card, customers who are approved will receive the new plastic and forget about it. An active credit card user may become inactive because the features, benefits and rewards are no longer relevant for their current financial needs. For example, a merchandise purchase or balance transfer promotion has expired and was paid off. Rewards are less attractive compared to other credit card offers in the marketplace. Lack of lender engagement activities may also lead to inactivity. For example, there are no marketing campaigns with promotions or special rewards offers. Revolving accounts with very low credit lines aren’t given credit line increases even though credit risk is acceptable, and accounts generate good interest income. The challenges to lenders with a large segment of inactive accounts include the direct cost of contingent liability. A percentage of unused credit lines is classified as contingent liability in the balance sheet. If contingent liability is reduced, then funds may be used to invest in more productive activities. In the absence of analytics and deep understanding of various customer behaviors in the portfolio, it can become costly for a lender when inactive accounts are included in all kinds of marketing campaigns. Marketing budgets are limited and ought to be used wisely to target segments with high expected returns and to achieve specific and well-defined objectives. Inactive accounts may also come with credit risk challenges. Some customers designate certain credit cards as emergency credit cards. That is, these cards will be used only in emergency situations where payment is needed immediately, and no other funds can be easily accessed at such time. Some situations are significantly more serious and may be accompanied by deep financial stress. During these times, inactive accounts are utilized and may result in collections or charge-offs. How can lenders handle the challenges of inactive accounts? An inactive account strategy that uses data and analytics is very helpful and prudent. Determine which accounts are never active or were inactive within the last 12 months. Identify which accounts pose elevated credit risk. There are various interventions that can be designed to improve card activation, which may include marketing campaigns and account management strategies including credit line options. If inactive accounts were included in marketing campaigns or account management strategies, then track the performance. These performance reports will provide the rationale and guidelines for further action, which may include account closure. Evaluate the multiple relationships of the customer with the lender and estimated cardmember value. Survey the inactive accounts and obtain feedback regarding the reasons for lack of card usage. Those insights will help identify areas for improvement and drive new initiatives. We have seen that inactive accounts aren’t a trivial component of a credit card portfolio. There are real costs and risks associated with inactive accounts. They also provide opportunities for improving card features and benefits and ways to continue engaging existing cardmembers.

Last year is a testament to how quickly trends can shift, and entire industries can be turned upside down.

Millennials and Gen Z consumers have proven to be future trend shapers for the auto industry.

Experian Automotive Market Insights includes an in-depth analysis of auction volume across the United States.