Latest Posts

The Q4 2020 State of the Automotive Finance Market report zooms in to get a better picture of the alternative fuel marketplace.

Preventing fraud losses requires an understanding of the individual fraud types, how they differ from one another, and how this impacts potential solutions.

The Center for Financial Professionals (CeFPro) has named Experian in its global Fintech Leaders List for the second year in a row.

Since 2002, lenders have been aware of the importance of Know Your Customer (KYC) and the associated Customer Identification Program (CIP) requirements.

Global Insights Report: The Impact of COVID-19 on Consumer Behaviors and Business Strategies

Apply DA TagAccording to Experian’s latest Global Insights Report, 38% of consumers expect to increase their online activity in the next 12 months.

Performance reports are foundational and are one of the key elements of a sound and prudent risk management framework. Learn how effective reports evolve.

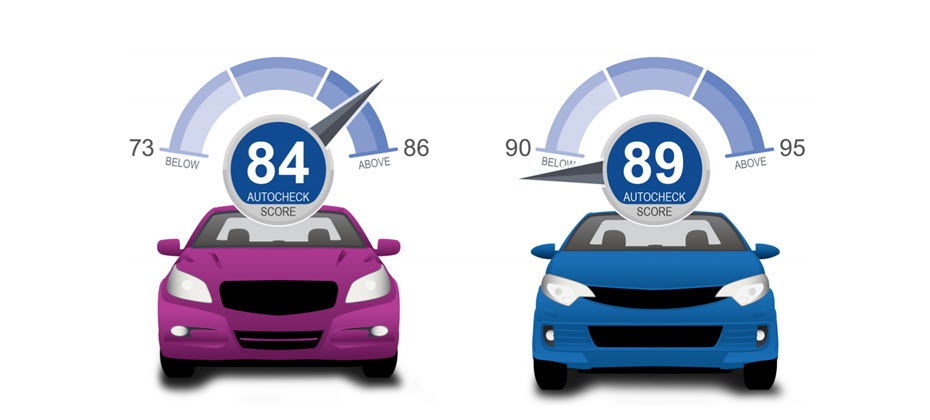

Do you know what the patented AutoCheck Score represents? The AutoCheck Score predicts the likelihood an individual vehicle will be on the road in five years.

Digital transformation has impacted account takeover fraud over the last year, requiring businesses to update their prevention and detection strategies.

Utilities Q&A Perspective Series: Maintaining Quality Contact Data Throughout the Customer Lifecycle

UncategorizedBy ensuring your organization’s data quality, you can allocate resources more effectively, minimize costs and safely serve your customers. Read more!

Inactive credit card accounts pose challenges to lenders. Discover potential reasons for inactivity and learn how to manage these accounts.

Last year is a testament to how quickly trends can shift, and entire industries can be turned upside down.

Millennials and Gen Z consumers have proven to be future trend shapers for the auto industry.

Experian Automotive Market Insights includes an in-depth analysis of auction volume across the United States.

Here are the four steps fintechs should take to reenter the lending market intelligently, while mitigating as much risk as possible.

Experian Automotive Market Insights helps dealers efficiently identify potential conquest opportunities in their region and beyond.