Latest Posts

Sometimes, the best offense is a good defense. That’s certainly true when it comes to detecting synthetic identities, which by their very nature become harder to find the longer they’ve been around. To launch an offense against synthetic identity fraud, you need to defend yourself from it at the top of your new customer funnel. Once fraudsters embed their fake identity into your portfolio, they become nearly impossible to detect. The Challenge Synthetic identity fraud is the fastest-growing type of financial crime in the United States. The cost to businesses is hard to determine because it’s not always caught or reported, but the amounts are staggering. According to the Aite Group, it was estimated to total at least $820 million in 2017 and grow to $1.2 billion by 2020. This type of theft begins when individual thieves and large-scale crime rings use a combination of compromised personal information—like unused social security numbers—and fabricated data to stitch together increasingly sophisticated personas. These well-crafted synthetic identities are hard to differentiate from the real deal. They often pass Know Your Customer, Customer Identification Program and other onboarding checks both in person and online. This puts the burden on you to develop new defense strategies or pay the price. Additionally, increasing pressure to grow deposits and expand loan portfolios may coincide with the relaxation of new customer criteria, allowing even more fraudsters to slip through the cracks. Because fraudsters nurture their fake identities by making payments on time and don’t exhibit other risk factors as their credit limits increase, detecting synthetic identities becomes nearly impossible, as does defending against them. How This Impacts Your Bottom Line Synthetic identity theft is sometimes viewed as a victimless crime, since no single individual has their entire identity compromised. But it’s not victimless. When undetected fraudsters finally max out their credit lines before vanishing, the financial institution is usually stuck footing the bill. These same fraudsters know that many financial institutions will automatically settle fraud claims below a specific threshold. They capitalize on this by disputing transactions just below it, keeping the goods or services they purchased without paying. Fraudsters can double-dip on a single identity bust-out by claiming identity theft to have charges removed or by using fake checks to pay off balances before maxing out the credit again and defaulting. The cost of not detecting synthetic identities doesn’t stop at the initial loss. It flows outward like ripples, including: Damage to your reputation as a trusted organization Fines for noncompliance with Know Your Customer Account opening and maintenance costs that are not recouped as they would be with a legitimate customer Mistakenly classifying fraudsters as bad debt write offs Monetary loss from fraudsters’ unpaid balances Rising collections costs as you try to track down people who don’t exist Less advantageous rates for customers in the future as your margins grow thinner These losses add up, continuing to impact your bottom line over and over again. Defensive Strategies So what can you do? Tools like eCBSV that will assist with detecting synthetic identities are coming but they’re not here yet. And once they’re in place, they won’t be an instant fix. Implementing an overly cautious fraud detection strategy on your own will cause a high number of false positives, meaning you miss out on revenue from genuine customers. Your best defense requires finding a partner to help you implement a multi-layered fraud detection strategy throughout the customer lifecycle. Detecting synthetic identities entails looking at more than a single factor (like length of credit history). You need to aggregate multiple data sets and connect multiple customer characteristics to effectively defend against synthetic identity fraud. Experian’s synthetic identity prevention tools include Synthetic Identity High Risk Score to incorporate the history and past relationships between individuals to detect anomalies. Additionally, our digital device intelligence tools perform link analyses to connect identities that seem otherwise separate. We help our partners pinpoint false identities not associated with an actual person and decrease charge offs, protecting your bottom line and helping you let good customers in while keeping false personas out. Find out how to get your synthetic identity defense in place today.

With the growing need for authentication and security, fintechs must manage risk with minimal impact to customer experience. When implementing tactical approaches for fraud risk strategy operations, keeping up with the pace of fraud is another critical consideration. How can fintechs be proactive about future-proofing fraud strategies to stay ahead of savvy fraudsters while maintaining customer expectations? I sat down with Chris Ryan, Senior Fraud Solutions Business Consultant with Experian Decision Analytics, to tap into some of his insights. Here’s what he had to say: How have changes in technology added to increased fraud risk for businesses operating in the online space? Technology introduces many risks in the online space. As it pertains to the fintech world, two stand out. First, the explosion in mobile technology. The same capabilities that make fintech products broadly accessible makes them vulnerable. Anyone with a mobile device can attempt to access a fintech and try their hand at committing fraud with very little risk of being caught or punished. Second, the evolution of an interconnected, digital ‘marketplace’ for stolen data. There’s an entire underground economy that’s focused on connecting the once-disparate pieces of information about a specific individual stolen from multiple, unrelated data breaches. Criminal misrepresentations are more complete and more convincing than ever before. What are the major market drivers and trends that have attributed to the increased risk of fraud? Ultimately, the major market drivers and trends that drive fraud risk for fintechs are customer convenience and growth. In terms of customer convenience, it’s a race to meet customer needs in real time, in a single online interaction, with a minimally invasive request for information. But, serving the demands of good customers opens opportunities for identity misuse. In terms of growth, the pressure to find new pockets of potential customers may lead fintechs into markets where consumer information is more limited, so naturally, there are some risks baked in. Are fintechs really more at risk for fraud? If so, how are fintechs responding to this dynamic threat? The challenge for many fintechs has been the prioritization of fraud as a risk that needs to be addressed. It’s understandable that fintech’s initial emphasis had to be the establishment of viable products that meet the needs of their customers. Obviously, without customers using a product, nothing else matters. Now that fintechs are hitting their stride in terms of attracting customers, they’re allocating more of their attention and innovative spirit to other areas, like fraud. With the right partner, it’s not hard for fintechs to protect themselves from fraud. They simply need to acquire reliable data that provides identity assurance without negatively impacting the customer experience. For example, fintechs can utilize data points that can be extracted from the communications channel, like device intelligence for example, or non-PII unique identifiers like phone and email account data. These are valuable risk indicators that can be collected and evaluated in real time without adding friction to the customer experience. What are the major fraud risks to fintechs and what are some of the strategies that Risk Managers can implement to protect their business? The trends we’ve talked about so far today have focused more on identity theft and other third-party fraud risks, but it’s equally important for fintechs to be mindful of first party fraud types where the owner of the identity is the culprit. There is no single solution, so the best strategy recommendation is to plan to be flexible. Fintechs demonstrate an incredible willingness to innovate, and they need to make sure the fraud platforms they pick are flexible enough to keep pace with their needs. From your perspective, what is the future of fraud and what should fintechs consider as they evolve their products? Fraud will continue to be a challenge whenever something of value is made available, particularly when the transaction is remote and the risk of any sort of prosecution is very low. Criminals will continue to revise their tactics to outwit the tools that fintechs are using, so the best long-term defense is flexibility. Being able to layer defenses, explore new data and analytics, and deploy flexible and dynamic strategies that allow highly tailored decisions is the best way for fintechs to protect themselves. Digital commerce and the online lending landscape will continue to grow at an increasing pace – hand-in-hand with the opportunities for fraud. To stay ahead of fraudsters, fintechs must be proactive about future-proofing their fraud strategies and toolkits. Experian can help. Our Fintech Digital Onboarding Bundle provides a solid baseline of cutting-edge fraud tools that protect fintechs against fraud in the digital space, via a seamless, low-friction customer experience. More importantly, the Fintech Digital Onboarding Bundle is delivered through Experian’s CrossCore platform—the premier platform in the industry recognized specifically for enabling the expansion of fraud tools across a wide range of Experian and third-party partner solutions. Click here to learn more or to speak with an Experian representative. Learn More About Chris Ryan: Christopher Ryan is a Senior Fraud Solutions Business Consultant. He delivers expertise that helps clients make the most from data, technology and investigative resources to combat and mitigate fraud risks across the industries that Experian serves. Ryan provides clients with strategies that reduce losses attributable to fraudulent activity. He has an impressive track record of stopping fraud in retail banking, auto lending, deposits, consumer and student lending sectors, and government identity proofing. Ryan is a subject matter expert in consumer identity verification, fraud scoring and knowledge-based authentication. His expertise is his ability to understand fraud issues and how they impact customer acquisition, customer management and collections. He routinely helps clients review workflow processes, analyze redundancies and identify opportunities for process improvements. Ryan recognizes the importance of products and services that limit fraud losses, balancing expense and the customer impact that can result from trying to prevent fraud.

As the holiday shopping season kicks off, it’s prime time for fraudsters to prey on consumers who are racking up rewards points as they spend. Find out how fraud trends in loyalty and rewards programs can impact your business: Are you ready to prevent fraud this holiday season? Get started today

In today’s ever-changing and hypercompetitive environment, the customer experience has taken center-stage – highlighting new expectations in the ways businesses interact with their customers. But studies show financial institutions are falling short. In fact, a recent study revealed that 94% of banking firms can’t deliver on the “personalization promise.” It’s not difficult to see why. Consumer preferences have changed, with many now preferring digital interactions. This has made it difficult for financial institutions to engage with consumers on a personal level. Nevertheless, customers expect seamless, consistent, and personalized experiences – that’s where the power of advanced analytics comes into play. It’s no secret that using advanced analytics can enable businesses to turn rich data into insights that lead to confident business decisions and strategy development. But these business tools can actually help financial institutions deliver on that promise of personalization. According to an Experian study, 90% of organizations say that embracing advanced analytics is critical to their ability to provide an excellent customer experience. By using data and analytics to anticipate and respond to customer behavior, companies can develop new and creative ways to cater to their audiences – revolutionizing the customer experience as a whole. It All Starts With Data Data is the foundation for a successful digital transformation – the lack of clean and cohesive datasets can hinder the ability to implement advanced analytic capabilities. However, 89% of organizations face challenges on how to effectively manage and consolidate their data, according to Experian’s Global Data Management Research Benchmark Report of 2019. Because consumers prefer digital interactions, companies have been able to gather a vast amount of customer data. Technology that uses advanced analytic capabilities (like machine learning and artificial intelligence) are capable of uncovering patterns in this data that may not otherwise be apparent, therefore opening doors to new avenues for companies to generate revenue. To start, companies need a strategy to access all customer data from all channels in a cohesive ecosystem – including data from their own data warehouses and a variety of different data sources. Depending on their needs, the data elements can come from a third party data provider such as: a credit bureau, alternative data, marketing data, data gathered during each customer contact, survey data and more. Once compiled, companies can achieve a more holistic and single view of their customer. With this single view, companies will be able to deliver more relevant and tailored experiences that are in-line with rising customer expectations. From Personalized Experiences to Predicting the Future The most progressive financial institutions have found that using analytics and machine learning to conquer the wide variety of customer data has made it easier to master the customer experience. With advanced analytics, these companies gain deeper insights into their customers and deliver highly relevant and beneficial offers based on the holistic views of their customers. When data is provided, technology with advanced analytic capabilities can transform this information into intelligent outputs, allowing companies to optimize and automate business processes with the customer in mind. Data, analytics and automation are the keys to delivering better customer experiences. Analytics is the process of converting data into actionable information so firms can understand their customers and take decisive action. By leveraging this business intelligence, companies can quickly adapt to consumer demand. Predictive models and forecasts, increasingly powered by machine learning, help lenders and other businesses understand risks and predict future trends and consumer responses. Prescriptive analytics help offer the right products to the right customer at the right time and price. By mastering all of these, businesses can be wherever their customers are. The Experian Advantage With insights into over 270 million customers and a wealth of traditional credit and alternative data, we’re able to drive prescriptive solutions to solve your most complex market and portfolio problems across the customer lifecycle – while reinventing and maintaining an excellent customer experience. If your company is ready for an advanced analytical transformation, Experian can help get you there. Learn More

Article written by Melanie Smith, Senior Copywriter, Experian Clarity Services, Inc. It’s been almost a decade since the Great Recession in the United States ended, but consumers continue to feel its effects. During the recession, millions of Americans lost their jobs, retirement savings decreased, real estate reduced in value and credit scores plummeted. Consumers that found themselves impacted by the financial crisis often turned to alternative financial services (AFS). Since the end of the recession, customer loyalty and retention has been a focus for lenders, given that there are more options than ever before for AFS borrowers. To determine what this looks like in the current climate, we examined today’s non-prime consumers, what their traditional scores look like and if they are migrating to traditional lending. What are alternative financial services (AFS)? Alternative financial services (AFS) is a term often used to describe the array of financial services offered by providers that operate outside of traditional financial institutions. In contrast to traditional banks and credit unions, alternative service providers often make it easier for consumers to apply and qualify for lines of credit but may charge higher interest rates and fees. More than 50% of new online AFS borrowers were first seen in 2018 To determine customer loyalty and fluidity, we looked extensively at the borrowing behavior of AFS consumers in the online marketplace. We found half of all online borrowers were new to the space as of 2018, which could be happening for a few different reasons. Over the last five years, there has been a growing preference to the online space over storefront. For example, in our trends report from 2018, we found that 17% of new online customers migrated from the storefront single pay channel in 2017, with more than one-third of these borrowers from 2013 and 2014 moving to online overall. There was also an increase in AFS utilization by all generations in 2018. Additionally, customers who used AFS in previous years are now moving towards traditional credit sources. 2017 AFS borrowers are migrating to traditional credit As we examined the borrowing behavior of AFS consumers in relation to customer loyalty, we found less than half of consumers who used AFS in 2017 borrowed from an AFS lender again in 2018. Looking into this further, about 35% applied for a loan but did not move forward with securing the loan and nearly 24% had no AFS activity in 2018. We furthered our research to determine why these consumers dropped off. After analyzing the national credit database to see if any of these consumers were borrowing in the traditional credit space, we found that 34% of 2017 borrowers who had no AFS activity in 2018 used traditional credit services, meaning 7% of 2017 borrowers migrated to traditional lending in 2018. Traditional credit scores of non-prime borrowers are growing After discovering that 7% of 2017 online borrowers used traditional credit services in 2018 instead of AFS, we wanted to find out if there had also been an improvement in their credit scores. Historically, if someone is considered non-prime, they don’t have the same access to traditional credit services as their prime counterparts. A traditional credit score for non-prime consumers is less than 600. Using the VantageScore® credit score, we examined the credit scores of consumers who used and did not use AFS in 2018. We found about 23% of consumers who switched to traditional lending had a near-prime credit score, while only 8% of those who continued in the AFS space were classified as near-prime. Close to 10% of consumers who switched to traditional lending in 2018 were classified in the prime category. Considering it takes much longer to improve a traditional credit rating, it’s likely that some of these borrowers may have been directly impacted by the recession and improved their scores enough to utilize traditional credit sources again. Key takeaways AFS remains a viable option for consumers who do not use traditional credit or have a credit score that doesn’t allow them to utilize traditional credit services. New AFS borrowers continue to appear even though some borrowers from previous years have improved their credit scores enough to migrate to traditional credit services. Customers who are considered non-prime still use AFS, as well as some near-prime and prime customers, which indicates customer loyalty and retention in this space. For more information about customer loyalty and other recently identified trends, download our recent reports. State of Alternative Data 2019 Lending Report

Time – it’s the only resource we can’t get more of, which is why we tend to obsess over saving it. Despite this obsession, it can be hard for us to identify time-wasting activities. From morning habits to credit decisioning, processes and routines that seem, well, routine, can get in the way of maximizing how we use our time. Identifying the Problem Every morning, I used to turn on my coffee maker, walk to the bathroom to take my multivitamin, then walk back into the kitchen to finish making my coffee. This required maybe twenty steps to the bathroom and twenty steps back, and while this isn’t a huge amount of time—half a minute at best—it’s not insignificant, especially in the morning when time feels particularly precious. One day, I realized I could eliminate the waste by moving my multivitamin to the cabinet above my coffeemaker. What if we could all make minor changes to enhance our efficiency both at home and at work? Imagine how much time we could save by cutting out unnecessary steps. And how saving that time could help drive significant revenue increases. Time Equals Money When businesses waste time with unnecessary steps, that’s money from their bottom line, and out of the pockets of people who are connected to them. Over the last several years, a new time saver has emerged – Application Programming Interface (API). APIs allow application programs to communicate with other operating systems or control programs through a series of server requests or API calls, enabling seamless interaction, data sharing and decisioning. Experian’s partners utilize our ever-growing suite of APIs to quickly access better data, making existing processes more effective and routines more efficient. In the past, banks and other partners had to send files back and forth to Experian when they needed decisioning on a customer’s credit-worthiness prior to approving a new loan or extending a credit limit increase. Now, partners can have their origination system call an Experian API and send their data through that. Our system processes it and sends it back in milliseconds, giving the lenders real-time decisioning rather than shuttling information back and forth unnecessarily. Instead of effectively walking away from one process (assisting the customer/making coffee) to start another (retrieving credit info/walking down the hall to take the multivitamin), our partners are able to link these processes up and save time, allowing them to capitalize on the presence and interest of their customer. The Proof When Washington State Employees Credit Union, the second-largest credit union in the state, realized they needed to make a change to keep pace with increasing competition, they turned to Experian. With our solution, the credit union is now able to provide its members with instant credit decisioning through their online banking platform. This real-time decisioning at the point of member-initiated contact increased the credit union’s loan and credit applications by 25%. Additionally, member satisfaction increased, with 90% of members finding the simplified prequalification process to be more efficient. By accessing Experian’s decisioning services through your existing connection, lenders can to save time and match consumers with the products that match their credit profile before they apply – increasing approval rates once the application is submitted. Best of all, the entire process with the consumers is completed within seconds. Find out how Experian’s solutions can help you improve your existing processes and cut out unnecessary steps. Get started

AI, machine learning, and Big Data – these are no longer just buzzwords. The advanced analytics techniques and analytics-based tools that are available to financial institutions today are powerful but underutilized. And the 30% of banks, credit unions and fintechs successfully deploying them are driving better data-driven decisions, more positive customer experiences and stronger profitability. As the opportunities surrounding advanced analytics continue to grow, more lenders are eager to adopt these capabilities to make the most of their datasets. And it’s understandable that financial institution are excited at the possibilities and insights that advanced analytics can bring to their business. However, there are some key considerations to keep in mind as you begin this important digital transformation. Here are three things you should do as your financial institution begins its advanced analytics journey. Ensure consistent and clean data quality Companies have a plethora of data and information on their customers. The main hurdles that many organizations face is being able to turn this information into a clean and cohesive dataset and formulating an effective and long-term data management strategy. Trying to implement advanced analytic capabilities while lacking an effective data governance strategy is like building a house on a poor foundation – likely to fail. Data quality issues, such as inconsistent data, data gaps, and incomplete and duplicated data, also haunt many organizations, making it difficult to complete their analytics objectives. Ensuring that issues in data quality are managed is the key to gaining the correct insights for your business. Establish and maintain a single view of customers The power of advanced analytics can only be as strong as the data provided. Unfortunately, many companies don’t realize that advanced analytics is much more powerful when companies are able to establish a single view of their customers. Companies need to establish and maintain a single view of customers in order to begin implementing advanced analytic capabilities. According to Experian research, a single customer view is a consistent, accurate and holistic view of your organization’s customers, prospects, and their data. Having full visibility and a 360 view into your customers paves the way for companies to make personalized, relevant, timely and precise decisions. But as many companies have begun to realize, getting this single view of customers is easier said than done. Organizations need to make sure that data should always be up-to-date, unique and available in order to begin a complete digital transformation. Ensure the right resources and commitment for your advanced analytics initiative It’s important to have the top-down commitment within your organization for advanced analytics. From the C-suite down, everyone should be on the same page as to the value analytics will bring and the investment the project might require. Organizations that want to move forward with implementing advanced analytic capabilities need to make sure to set aside the right financial and human resources that will be needed for the journey. This may seem daunting, but it doesn’t have to be. A common myth is that the costs of new hardware, new hires and the costs required to maintain, configure, and set up new technology will make advanced analytics implementation far too expensive and difficult to maintain. However, many organizations don’t realize that it’s not necessary to allocate large capital expenses to implement advanced analytics. All it takes is finding the right-sized solution with configurations to fit the team size and skill level in your organization. Moreover, finding the right partner and team (whether internal or external) can be an efficient way to fill temporary skills gaps on your team. No digital transformation initiative is without its challenges. However, beginning your advanced analytics journey on the right footing can deliver unparalleled growth, profitability and opportunities. Still not sure where to begin? At Experian, we offer a wide range of solutions to help you harness the full power and potential of data and analytics. Our consultants and development teams have been a game-changer for financial institutions, helping them get more value, insight and profitability out of their data and modeling than ever before. Learn More

Fintech is quickly changing. The word itself is synonymous with constant innovation, agile technology structures and being on the cusp of the future of finance. The rapid rate at which fintech challengers are becoming established, is in turn, allowing for greater consumer awareness and adoption of fintech platforms. It would be easy to assume that fintech adoption is predominately driven by millennials. However, according to a recent market trend analysis by Experian, adoption is happening across multiple generational segments. That said, it’s important to note the generational segments that represent the largest adoption rates and growth opportunities for fintechs. Here are a few key stats: Members of Gen Y (between 24-37 years old) account for 34.9% of all fintech personal loans, compared to just 24.9% for traditional financial institutions. A similar trend is seen for Gen Z (between 18-23 years old). This group accounts for 5% of all fintech personal loans as compared to 3.1% for traditional Let’s take a closer look at these generational segments… Gen Y represents approximately 19% of the U.S. population. These consumers, often referred to as “millennials,” can be described as digital-centric, raised on the web and luxury shoppers. In total, millennials spend about $600 billion a year. This group has shown a strong desire to improve their credit standing and are continuously increasing their credit utilization. Gen Z represents approximately 26% of the U.S. population. These consumers can be described as digital centric, raised on the social web and frugal. The Gen Z credit universe is growing, presenting a large opportunity to lenders, as the youngest Gen Zers become credit eligible and the oldest start to enter homeownership. What about the underbanked as a fintech opportunity? The CFPB estimates that up to 45 million people, or 24.2 million households, are “thin-filed” or underbanked, meaning they manage their finances through cash transactions and not through financial services such as checking and savings accounts, credit cards or loans. According to Angela Strange, a general partner at Andreessen Horowitz, traditional financial institutions have done a poor job at serving underbanked consumers affordable products. This has, in turn, created a trillion-dollar market opportunity for fintechs offering low-cost, high-tech financial services. Why does all this matter? Fintechs have a unique opportunity to engage, nurture and grow these market segments early on. As the fintech marketplace heats up and the overall economy begins to soften, diversifying revenue streams, building loyalty and tapping into new markets is a strategic move. But what are the best practices for fintechs looking to build trust, engage and retain these unique consumer groups? Join us for a live webinar on November 12 at 10:00 a.m. PST to hear Experian experts discuss financial inclusion trends shaping the fintech industry and tactical tips to create, convert and extend the value of your ideal customers. Register now

Retailers are already starting to display their Christmas decorations in stores and it’s only early November. Some might think they are putting the cart ahead of the horse, but as I see this happening, I’m reminded of the quote by the New York Yankee’s Yogi Berra who famously said, “It gets late early out there.” It may never be too early to get ready for the next big thing, especially when what’s coming might set the course for years to come. As 2019 comes to an end and we prepare for the excitement and challenges of a new decade, the same can be true for all of us working in the lending and credit space, especially when it comes to how we will approach the use of alternative data in the next decade. Over the last year, alternative data has been a hot topic of discussion. If you typed “alternative data and credit” into a Google search today, you would get more than 200 million results. That’s a lot of conversations, but while nearly everyone seems to be talking about alternative data, we may not have a clear view of how alternative data will be used in the credit economy. How we approach the use of alternative data in the coming decade is going to be one of the most important decisions the lending industry makes. Inaction is not an option, and the time for testing new approaches is starting to run out – as Yogi said, it’s getting late early. And here’s why: millennials. We already know that millennials tend to make up a significant percentage of consumers with so-called “thin-file” credit reports. They “grew up” during the Great Recession and that has had a profound impact on their financial behavior. Unlike their parents, they tend to have only one or two credit cards, they keep a majority of their savings in cash and, in general, they distrust financial institutions. However, they currently account for more than 21 percent of discretionary spend in the U.S. economy, and that percentage is going to expand exponentially in the coming decade. The recession fundamentally changed how lending happens, resulting in more regulation and a snowball effect of other economic challenges. As a result, millennials must work harder to catch up financially and are putting off major life milestones that past generations have historically done earlier in life, such as homeownership. They more often choose to rent and, while they pay their bills, rent and other factors such as utility and phone bill payments are traditionally not calculated in credit scores, ultimately leaving this generation thin-filed or worse, credit invisible. This is not a sustainable scenario as we enter the next decade. One of the biggest market dynamics we can expect to see over the next decade is consumer control. Consumers, especially millennials, want to be in the driver’s seat of their “credit journey” and play an active role in improving their financial situations. We are seeing a greater openness to providing data, which in turn enables lenders to make more informed decisions. This change is disrupting the status quo and bringing new, innovative solutions to the table. At Experian, we have been testing how advanced analytics and machine learning can help accelerate the use of alternative data in credit and lending decisions. And we continue to work to make the process of analyzing this data as simple as possible, making it available to all lenders in all verticals. To help credit invisible and thin-file consumers gain access to fair and affordable credit, we’ve recently announced Experian Lift, a new suite of credit score products that combines exclusive traditional credit, alternative credit and trended data assets to create a more holistic picture of consumer creditworthiness that will be available to lenders in early 2020. This new Experian credit score may improve access to credit for more than 40 million credit invisibles. There are more than 100 million consumers who are restricted by the traditional scoring methods used today. Experian Lift is another step in our commitment to helping improve financial health of consumers everywhere and empowers lenders to identify consumers who may otherwise be excluded from the traditional credit ecosystem. This isn’t just a trend in the United States. Brazil is using positive data to help drive financial inclusion, as are others around the world. As I said, it’s getting late early. Things are moving fast. Already we are seeing technology companies playing a bigger role in the push for alternative data – often powered by fintech startups. At the same time, there also has been a strong uptick in tech companies entering the banking space. Have you signed up for your Apple credit card yet? It will take all of 15 seconds to apply, and that’s expected to continue over the next decade. All of this is changing how the lending and credit industry must approach decision making, while also creating real-time frictionless experiences that empower the consumer. We saw this with the launch of Experian Boost earlier this year. The results speak for themselves: hundreds of thousands of previously thin-file consumers have seen their credit scores instantly increase. We have also empowered millions of consumers to get more control of their credit by using Experian Boost to contribute new, positive phone, cable and utility payment histories. Through Experian Boost, we’re empowering consumers to play an active role in building their credit histories. And, with Experian Lift, we’re empowering lenders to identify consumers who may otherwise be excluded from the traditional credit ecosystem. That’s game-changing. Disruptions like Experian Boost and newly announced Experian Lift are going to define the coming decade in credit and lending. Our industry needs to be ready because while it may seem early, it’s getting late.

It seems like artificial intelligence (AI) has been scaring the general public for years – think Terminator and SkyNet. It’s been a topic that’s all the more confounding and downright worrisome to financial institutions. But for the 30% of financial institutions that have successfully deployed AI into their operations, according to Deloitte, the results have been anything but intimidating. Not only are they seeing improved performance but also a more enhanced, positive customer experience and ultimately strong financial returns. For the 70% of financial institutions who haven’t started, are just beginning their journey or are in the middle of implementing AI into their operations, the task can be daunting. AI, machine learning, deep learning, neural networks—what do they all mean? How do they apply to you and how can they be useful to your business? It’s important to demystify the technology and explain how it can present opportunities to the financial industry as a whole. While AI seems to have only crept into mainstream culture and business vernacular in the last decade, it was first coined by John McCarthy in 1956. A researcher at Dartmouth, McCarthy thought that any aspect of learning or intelligence could be taught to a machine. Broadly, AI can be defined as a machine’s ability to perform cognitive functions we associate with humans, i.e. interacting with an environment, perceiving, learning and solving problems. Machine learning vs. AI Machine learning is not the same thing as AI. Machine learning is the application of systems or algorithms to AI to complete various tasks or solve problems. Machine learning algorithms can process data inputs and new experiences to detect patterns and learn how to make the best predictions and recommendations based on that learning, without explicit programming or directives. Moreover, the algorithms can take that learning and adapt and evolve responses and recommendations based on new inputs to improve performance over time. These algorithms provide organizations with a more efficient path to leveraging advanced analytics. Descriptive, predictive, and prescriptive analytics vary in complexity, sophistication, and their resulting capability. In simplistic terms, descriptive algorithms describe what happened, predictive algorithms anticipate what will happen, and prescriptive algorithms can provide recommendations on what to do based on set goals. The last two are the focus of machine learning initiatives used today. Machine learning components - supervised, unsupervised and reinforcement learning Machine learning can be broken down further into three main categories, in order of complexity: supervised, unsupervised and reinforcement learning. As the name might suggest, supervised learning involves human interaction, where data is loaded and defined and the relationship to inputs and outputs is defined. The algorithm is trained to find the relationship of the input data to the output variable. Once it delivers accurately, training is complete, and the algorithm is then applied to new data. In financial services, supervised learning algorithms have a litany of uses, from predicting likelihood of loan repayment to detecting customer churn. With unsupervised learning, there is no human engagement or defined output variable. The algorithm takes the input data and structures it by grouping it based on similar characteristics or behaviors, without a defined output variable. Unsupervised learning models (like K-means and hierarchical clustering) can be used to better segment or group customers by common characteristics, i.e. age, annual income or card loyalty program. Reinforcement learning allows the algorithm more autonomy in the environment. The algorithm learns to perform a task, i.e. optimizing a credit portfolio strategy, by trying to maximize available rewards. It makes decisions and receives a reward if those actions bring the machine closer to achieving the total available rewards, i.e. the highest acquisition rate in a customer category. Over time, the algorithm optimizes itself by correcting actions for the best outcomes. Even more sophisticated, deep learning is a category of machine learning that involves much more complex architecture where software-based calculators (called neurons) are layered together in a network, called a neural network. This framework allows for much broader, complex data ingestion where each layer of the neural network can learn progressively more complex elements of the data. Object classification is a classic example, where the machine ‘learns’ what a duck looks like and then is able to automatically identify and group images of ducks. As you might imagine, deep learning models have proved to be much more efficient and accurate at facial and voice recognition than traditional machine learning methods. Whether your financial institution is already seeing the returns for its AI transformation or is one of the 61% of companies investing in this data initiative in 2019, having a clear picture of what is available and how it can impact your business is imperative. How do you see AI and machine learning impacting your customer acquisition, underwriting and overall customer experience?

Last month, Kenneth Blanco, Director of the Financial Crimes Enforcement Network, warned that cybercriminals are stealing data from fintech platforms to create synthetic identities and commit fraud. These actions, in turn, are alleged to be responsible for exploiting fintech platforms’ integration with other financial institutions, putting banks and consumers at risk. According to Blanco, “by using stolen data to create fraudulent accounts on fintech platforms, cybercriminals can exploit the platforms’ integration with various financial services to initiate seemingly legitimate financial activity while creating a degree of separation from traditional fraud detection efforts.” Fintech executives were quick to respond, and while agreeing that synthetic IDs are a problem, they pushed back on the notion that cybercriminals specifically target fintech platforms. Innovation and technology have indeed opened new doors of possibility for financial institutions, however, the question remains as to whether it has also created an opportunity for criminals to implement more sophisticated fraud strategies. Currently, there appears to be little evidence pointing to an acute vulnerability of fintech firms, but one thing can be said for certain: synthetic ID fraud is the fastest-growing financial crime in the United States. Perhaps, in part, because it can be difficult to detect. Synthetic ID is a type of fraud carried out by criminals that have created fictitious identities. Truly savvy fraudsters can make these identities nearly indistinguishable from real ones. According to Kathleen Peters, Experian’s SVP, Head of Fraud and Identity, it typically takes fraudsters 12 to 18 months to create and nurture a synthetic identity before it’s ready to “bust out” – the act of building a credit history with the intent of maxing out all available credit and eventually disappearing. These types of fraud attacks are concerning to any company’s bottom line. Experian’s 2019 Global Fraud and Identity Report further details the financial impact of fraud, noting that 55% of businesses globally reported an increase in fraud-related losses over the past 12 months. Given the significant risk factor, organizations across the board need to make meaningful investments in fraud prevention strategies. In many circumstances, the pace of fraud is so fast that by the time organizations implement solutions, the shelf life may already be old. To stay ahead of fraudsters, companies must be proactive about future-proofing their fraud strategies and toolkits. And the advantage that many fintech companies have is their aptitude for being nimble and propensity for early adoption. Experian can help too. Our Synthetic Fraud Risk Level Indicator helps both fintechs and traditional financial institutions in identifying applicants likely to be associated with a synthetic identity based on a complex set of relationships and account conditions over time. This indicator is now available in our credit report, allowing organizations to reduce exposure to identity fraud through early detection. To learn more about Experian’s Synthetic Fraud Risk Level Indicator click here, or visit experian.com/fintech.

It’s Halloween time – time for trick or treating, costume parties and monsters lurking in the background. But this year, the monsters aren’t just in the background. They’re in your portfolio. This year, “Frankenstein” has another meaning. Much more ominous than the neighbor kid in the costume. “Frankenstein IDs” refer to synthetic identities — a type of fraud carried out by criminals that have created fictitious identities. Just as Dr. Frankenstein’s monster was stitched together from parts, synthetic IDs are stitched together pieces of mismatched identities — some fake, some real, some even deceased. It typically takes fraudsters 12 to 18 months to create and nurture a synthetic identity before it’s ready to "bust out" – the act of building a credit history with the intent of maxing out all available credit and eventually disappearing. That means fraudsters are investing money and time to build numerous tradelines, ensure these "fake" identities are in good credit standing, and ultimately steal the largest amount of money possible. “Wait Master, it might be dangerous . . . you go, first.” — Igor Synthetic identities are a notable challenge for many financial institutions and retail organizations. According to the recently released Federal Reserve Board White Paper, synthetic identity fraud accounts for roughly 20% of all credit losses, and cost U.S. businesses roughly $6 billion in 2016 with an estimated 41% growth over 2 years. 85-95% of applicants identified as potential synthetic are not even flagged by traditional fraud models. The Social Security Administration recently announced plans for the electronic Consent Based Social Security Number Verification service – pilot program scheduled for June 2020. This service is designed to bring efficiency to the process for verifying Social Security numbers directly with the government agency. Once available, this verification could be an important tool in the fight against the elusive “Frankenstein” identity monster. But with the Social Security Administration's pilot program not scheduled for launch until the middle of next year, how can financial institutions and other organizations bridge the gap and adequately prepare for a potential uptick in synthetic identity fraud attacks? It comes down to a multilayered approach that relies on advanced data, analytics, and technology — and focuses on identity. Any significant progress in making synthetic identities easier to detect could cost fraudsters significant time and money. Far too many financial institutions and other organizations depend solely on basic demographic information and snapshots in time to confirm the legitimacy of an identity. These organizations need to think beyond those capabilities. The real value of data in many cases lies between the data points. We have seen this with synthetic identity — where a seemingly legitimate identity only shows risk when we can analyze its connections and relationships to other individuals and characteristics. In addition to our High Risk Fraud Score, we now have a Synthetic Fraud Risk Level Indicator available on credit profiles. These advanced detection capabilities are delivered via the simplicity of a straightforward indicator returned on the credit profile which lenders can use to trigger additional identity verification processes. While there are programs and initiatives in the works to help financial institutions and other organizations combat synthetic identity fraud, it's important to keep in mind there's no silver bullet, or stake to the heart, to completely keep these Frankenstein IDs out. Oh, and don’t forget… “It’s pronounced ‘Fronkensteen.’ ” — Dr. Frankenstein

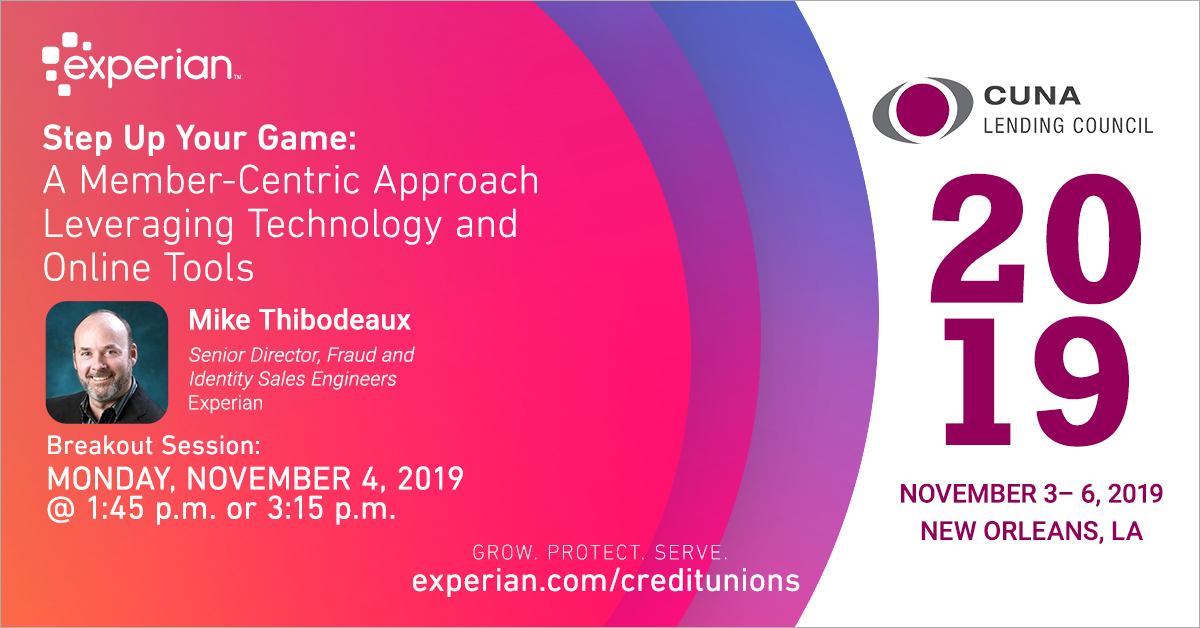

As credit unions look to grow their loan portfolios and acquire new members, improving the member experience is critical to the process and remains a primary focus. In order to compete in the lending universe, financial tools that empower and enable a positive experience are critical to meeting these requirements. That being said, an Experian study reveals that 90% of executives agree that embracing a digital transformation is critical to providing excellent experiences. In this connected, data-driven world, digital transformations are opening the door for better and greater opportunities. With data and analytics, credit unions will be able to gain data-driven insights, to identify key channels of member engagement, create complete member views and further maximize growth and lending strategies. Data-driven organizations that can anticipate their members’ needs and preferences will be able to deepen relationships and maintain relevance – gaining an edge in a highly-competitive environment. The digital revolution is happening now – and it’s time for future-focused credit unions to adapt to changing expectations. However, according to an Experian report, 39% of organizations lack the customer insight and data required to provide these member experiences. That’s where Experian comes in. Join Mike Thibodeaux, Experian’s Senior Director, Fraud and Identity Sales Engineers, for a breakout session at CUNA Lending 2019 on Monday, Nov. 4 at 1:45 p.m. or 3:15 p.m. He will take a closer look at best practices and digital tools that credit unions can use to maximize credit union membership growth, while managing and mitigating fraud. The discussion will revolve around multiple topics, critical to the member experience conversation, including: Increasing profitable loan growth Lending deeper to the underserved Levering digital services and tools for your credit union Minimizing fraud activity (specifically synthetic identity fraud) and credit losses Enhancing and maintaining positive member experiences Experian is excited to once again take part in the 2019 CUNA Lending Council Conference, an event that brings together the credit union movement’s best and brightest in lending. If you’re attending, make sure to engage and connect with our thought leaders at our booth and learn how we’re dedicated to helping credit unions of all sizes advance their decisioning and services. Our team is committed to being a trusted partner – providing solutions that enable you to further grow, protect and serve within your field of membership. Learn More

Over the years, businesses have gathered a plethora of datasets on their customers. However, there is no value in data alone. The true value comes from the insights gained and actions that can be derived from these datasets. Advanced analytics is the key to understanding the data and extracting the critical information needed to unlock these insights. AI and machine learning in particular, are two emerging technologies with advanced analytics capabilities that can help companies achieve their business goals. According to an IBM survey, 61% of company executives indicated that machine learning and AI are their company’s most significant data initiatives in 2019. These leaders recognize that advanced analytics is transforming the way companies traditionally operate. It is no longer just a want, but a must. With a proper strategy, advanced analytics can be a competitive differentiator for your financial institution. Here are some ways that advanced analytics can empower your organization: Provide Personalized Customer Experiences Business leaders know that their customers want personalized, frictionless and enhanced experiences. That’s why improving the customer experience is the number one priority for 80 percent of executives globally, according to an Experian study. The data is already there – companies have insights into what products their customers like, the channels they use to communicate, and other preferences. By utilizing the capabilities of advanced analytics, companies can extract more value from this data and gain better insights to help create more meaningful, personalized and profitable lending decisions. Reduce Costs Advanced analytics allows companies to deploy new models and strategies more efficiently – reducing expenses associated with managing models for multiple lending products and bureaus. For example, OneMain Financial, was able to successfully drive down risk modeling expenses after implementing a solution with advanced analytics capabilities. Improve Accuracy and Speed to Market To stay ahead of the competition, companies need to maintain fast-moving environments. The speed, accuracy and power of a company’s predictive models and forecasts are crucial for success. Being able to respond to changing market conditions with insights derived from advanced analytics is a key differentiator for future-forward companies. Advanced analytic capabilities empower companies to anticipate new trends and drive rapid development and deployment, creating an agile environment of continual improvement. Drive Growth and Expand Your Customer Base With the rise of AI, machine learning and big data, the opportunities to expand the credit universe is greater than ever. Advanced analytic capabilities allow companies to scale datasets and get a bird’s eye view into a consumer’s true financial position – regardless of whether they have a credit history. The insights derived from advanced analytics opens doors for thin file or credit invisible customers to be seen – effectively allowing lenders to expand their customer base. Meet Compliance Requirements Staying on top of model risk and governance should always remain top of mind for any institution. Analytical processing aggregates and pulls new information from a wide range of data sources, allowing your institution to make more accurate and faster decisions. This enables lenders to lend more fairly, manage models that stand up to regulatory scrutiny, and keep up with changes in reporting practices and regulations. Better, faster and smarter decisions. It all starts with advanced analytics. Businesses must take advantage of the opportunities that come with implementing advanced analytics, or risk losing their customers to more future-forward organizations. At Experian, we believe that using big data can help power opportunities for your company. Learn how we can help you leverage your data faster and more effectively. Learn More

To provide consumers with clear-cut protections against disturbance by debt collectors, the Consumer Financial Protection Bureau (CFPB) issued a Notice of Proposed Rulemaking (NPRM) to implement the Fair Debt Collection Practices Act (FDCPA) earlier this year. Among many other things, the proposal would set strict limits on the number of calls debt collectors may place to reach consumers weekly and clarify requirements for consumer-facing debt collection disclosures. A bigger discussion Deliberation of the debt collection proposal was originally scheduled to begin on August 18, 2019. However, to allow commenters to further consider the issues raised in the NPRM and gather data, the comment period was extended by 20 days to September 18, 2019. It is currently still being debated, as many argue that the proposed rule does not account for modern consumer preferences and hinders the free flow of information used to help consumers access credit and services. The Association of Credit and Collection Professionals (ACA International) and US House lawmakers continue to challenge the proposal, stating that it doesn’t ensure that debt collectors’ calls to consumers are warranted, nor does it do enough to protect consumers’ privacy. Many consumer advocates have expressed doubts about how effective the proposed measures will be in protecting debtors from debt collector harassment and see the seven-calls-a-week limit on phone contact as being too high. In fact, it’s difficult to find a group of people in full support of the proposal, despite the CFPB stating that it will help clarify the FDCPA, protect lenders from litigation and bring consumer protection regulation into the 21st century. What does this mean? Although we don’t know when, or if, the proposed rule will go into effect, it’s important to prepare. According to the Federal Register, there are key ways that the new regulation would affect debt collection through the use of newer technologies, required disclosures and limited consumer contact. Not only will the proposed rules apply to debt collectors, but its provisions will also impact creditors and servicers, making it imperative for everyone in the financial services space to keep watch on the regulation’s status and carefully analyze its proposed rules. At Experian, our debt collection solutions automate and moderate dialogues and negotiations between consumers and collectors, making it easier for collection agencies to connect with consumers while staying compliant. Our best-in-class data and analytics will play a key role in helping you reach the right consumer, in the right place, at the right time. Learn more