Tag: alternative data

Since 1996, The Internal Revenue Service (IRS) has issued more than 27 million individual taxpayer identification numbers (ITINs) – a 9-digit number used by individuals who are required to file or report taxes in the United States but are not eligible to obtain a Social Security number (SSN). Across the country, ITIN holders are actively contributing to their communities and the U.S. financial system. They pay bills, build businesses, contribute billions in taxes and manage their finances responsibly. Yet despite their clear engagement, many remain underrepresented within traditional lending models. Lenders have a meaningful opportunity to bridge the gap between intention and impact. By rethinking how ITIN consumers are evaluated and supported, financial institutions can: Reduce barriers that have historically held capable borrowers back Build products that reflect real borrower needs Foster trust and strengthen community relationships Drive sustainable, responsible growth Our latest white paper takes a more holistic look at ITIN consumers, highlighting their credit behaviors, performance patterns and long-term growth potential. The findings reveal a population that is not only financially engaged, but also demonstrating signs of ongoing stability and mobility. A few takeaways include: ITIN holders maintain a lower debt-to-income ratio than SSN consumers. ITIN holders exhibit fewer derogatory accounts (180–400 days past due). After 12 months, 76.9% of ITIN holders remained current on trades, a rate 15% higher than SSN consumers. With deeper insight into this segment, lenders can make more informed, inclusive decisions. Read the full white paper to uncover the trends and opportunities shaping the future of ITIN lending. Download white paper

In our latest Experian fireside chat, Unlocking Alternative Data for Smarter Fintech Decisions, two powerhouse voices in the industry, Ashley Knight, SVP of Product Management at Experian, and Haiyan Huang, Chief Credit Officer at Prosper Marketplace, came together for an exclusive discussion on how alternative data is transforming risk, marketing and growth strategies across the fintech space. Now available to watch on demand, the conversation reveals the data-driven innovations that are empowering fintechs to reach new markets, improve decision-making, and build more inclusive financial experiences. What you'll learn During the session, Ashley and Haiyan explored how fintech leaders are utilizing alternative data to address real-world challenges with smarter, more scalable solutions. Topics include: Identity matching redefined: Discover how Individual Taxpayer Identification Numbers (ITINs), Clarity insights, and device intelligence empower fintechs to gain a competitive edge in verifying and validating identities for thin-file or underserved applicants. Precision credit marketing: Learn how email and phone intelligence help fintechs more accurately connect with qualified consumers, driving better engagement and higher conversion rates. Enhanced risk management with real-time data: Discover how Buy Now, Pay Later (BNPL) data and open banking insights are providing fintechs with a more comprehensive view of consumer financial behavior, beyond what traditional credit scores can reveal. To understand how fintech professionals are approaching alternative data, we asked attendees to weigh in throughout the webinar. Here's what we learned: What the audience had to say Which alternative asset is most important for the underwriting of the insurance? 50% chose open banking. 38% selected behavioral/device intelligence. 12% pointed to asset ownership. Takeaway: Open banking is leading the way, but fintechs are clearly embracing a multi-dimensional data approach. 2. Are you currently using ITINs or planning to in the future? 53% said yes. 47% said no. Takeaway: The adoption of ITINs is gaining momentum, supporting efforts to expand access to underrepresented segments. 3. What’s the most compelling reason to use open banking data? 70% said to better assess risk. 10% said to say yes to more consumers. 10% said to price more effectively. 10% said to improve marketing and personalization. Takeaway: Risk assessment remains the top use case, but marketers and pricing teams are starting to take notice. Why it matters Alternative data isn’t just a trend; it’s a response to the urgent need for smarter, more inclusive lending models. As fintechs continue to grow, the ability to reach new audiences, personalize offers, and manage risk with greater accuracy is no longer a competitive advantage; it’s a requirement. Whether you're already integrating cash flow, open banking, and behavioral insights, or just beginning to explore the possibilities, this webinar offers valuable frameworks and firsthand examples from industry leaders who are putting alternative data into action. Don’t miss this opportunity to catch up on the conversation that's helping define the future of fintech innovation. Watch on-demand webinar

Why data analytics matters more to fintech lenders Unlike traditional financial institutions, fintechs grow through rapid experimentation. They build, iterate and deploy at a pace that rewards agility but often exposes gaps in visibility. That’s why unified, trusted data has become essential infrastructure. Many fintech leaders note that building technology is rarely the barrier; the real challenge is ensuring their data can move as quickly as their decisions. Analytics plays a central role in closing that gap by providing real-time insight that supports speed, accuracy and confidence. Fintech analytics goes far beyond reporting. It’s about connecting credit, cash flow and behavioral data to reveal intent, detect risk early and personalize offers. The leaders in this space aren’t those with the most data, but those who can turn it into confident, compliant action. How fintechs are using analytics to stay ahead 1. Managing risk in real timeFintech lenders are increasingly recognizing that the boundary between fraud and credit risk is disappearing. Rather than treating them as separate disciplines, leading firms are developing unified approaches that detect early behavioral signals that indicate financial stress or potential fraud well before losses occur. By fusing transactional and credit data, they are creating adaptive risk models that evolve in real time and deliver faster, more confident decisions. 2. Unlocking value from cash flow and alternative dataFintechs are finding that cash flow tells a richer story than credit alone. By layering bank transaction data on top of bureau insights, many have improved model accuracy and expanded their reach to consumers who might otherwise be overlooked. Analysis of BNPL activity, primary account behavior and income patterns is also helping lenders tailor offers with greater precision and fairness. 3. Accelerating innovation with governed AIAI is driving model development and decisioning speed, but governance remains a universal concern. Fintech leaders acknowledge the challenge of balancing innovation with regulatory transparency, emphasizing the need for faster validation, clearer audit trails and explainable outputs. The next frontier isn’t just building smarter models but ensuring those models are trusted by compliance teams, investors and consumers alike. Persistent pain points in fintech data integration For many fintechs, they are challenged by knowing, that the data exists, but the stitching between sources slows everything down. Even the most advanced fintechs face familiar challenges: Fragmented data ecosystems: Transactional, credit, and behavioral data often live across disconnected systems, creating blind spots and latency. Data quality and recency: Incomplete or outdated information weakens the accuracy of AI models. Scalability and governance: Rapid growth amplifies infrastructure strain and regulatory complexity. Where Experian gives fintechs an edge Fintechs have a need for control, speed and trust — a balance that’s difficult to achieve with point solutions or legacy integrations. That’s where Experian differentiates. The Experian Ascend Platform™ brings data, analytics and decisioning together in a single, secure environment so fintechs can: Access unified, model-ready data that combines credit, cash flow and alternative sources. Build, test, and deploy predictive models through sandbox capabilities that mirror real-world conditions. Enhance transparency and compliance with built-in AI governance and audit tools. Integrate seamlessly through flexible APIs designed for engineering-led teams. Several fintech leaders have stated that Experian’s Ascend platform’s performance and transparency help them move faster without compromising oversight, giving them the speed of an in-house build with the reliability of a proven data partner. The takeaway: from data collection to confident decisioning For fintech lenders, analytics is no longer a back-end function. It is a strategic capability that drives every decision. Those who unify their data, operationalize insights responsibly and automate decisions with transparency will set the pace for the next wave of credit innovation. Experian continues to partner with leading fintechs to transform fragmented data into real-time intelligence, powering smarter lending, sharper risk controls and stronger customer experiences built on trusted data. Discover how Experian’s fintech solutions are helping fintechs harness analytics to accelerate growth and innovation. Learn more

Buy now, pay later (BNPL) has rapidly matured into a $175 billion market in the U.S. alone, according to PYMNTS, reshaping how consumers approach short-term financing. While early BNPL adoption was often associated with younger, higher-risk borrowers, recent data paints a far more nuanced and encouraging picture. Today’s BNPL consumers are showing signs of financial responsibility, planning, and discipline — offering lenders new opportunities to empower financial futures. BNPL adoption is widening Though Millennials and Gen Z remain the largest user base, usage among Gen X and Baby Boomers continues to grow steadily. Between 2021 and 2025, BNPL adoption among Gen X is projected to rise by 13.7%, and by 8.6% for Baby Boomers. According to a Morgan Stanley report, much of this growth is being fueled by the perceived ease and predictability of BNPL terms. In fact, Experian research1 shows 41% of U.S. adults have used BNPL, with nearly half of those users tapping into the service once a month or more. This increased use of BNPL appears to reflect that BNPL has moved from a niche payment option to a mainstream financial tool. The rise of intentional and responsible spending Contrary to outdated perceptions, most BNPL users are not overleveraged impulse spenders. Instead, Experian data shows: 73% of BNPL users report making payments on time and as agreed.2 75% cite convenience and flexible payments as their primary motivations.3 The desire for control and flexibility is a consistent behavioral theme. Investopedia notes that leading BNPL platforms are leaning into this demand by offering budgeting tools and automatic payment reminders. Why this shift matters for lenders When BNPL data becomes available to lenders, the data it generates will offer a powerful lens into consumer behavior. Beyond challenging old assumptions, these insights can be leveraged to strengthen risk assessment, identify new growth opportunities, and serve consumers who may otherwise be overlooked: Enriched credit risk models BNPL payment data can add an additional layer of insight into consumers’ financial health and behaviors. By integrating this information into their underwriting process, lenders can more accurately assess risk. Serving thin-file consumers Thin-file consumers, such as young adults, may often be overlooked by traditional credit models. BNPL data can provide greater visibility into their financial habits, helping lenders expand credit access more equitably and support greater financial inclusion. Evolving with the BNPL consumer Today’s BNPL users are not who they were five years ago. They are increasingly financially literate, focused on credit health and integrating BNPL into everyday budgeting. When BNPL data becomes available, lenders will have a chance to: Sharpen risk models with alternative data Personalize offers with greater precision Expand financial access to underserved groups BNPL users are changing — and lenders who understand this shift will be ready to serve a broader, more responsible borrower base when the data becomes actionable. We continue to work closely with BNPL providers to support expanded data furnishing and bring greater visibility to both consumers and the industry. Visit our webpage to discover the latest insights and developments on BNPL data. Learn more 1-3Experian commissioned Atomik Research to conduct an online survey of 2,005 adults throughout the United States. The margin of error is +/- 2 percentage points with a confidence level of 95 percent. Fieldwork took place between May 15 and May 20, 2025.

Artificial intelligence (AI) is transforming industries worldwide, and financial services are no exception. One of the most impactful applications is AI credit scoring, a modern approach that uses advanced algorithms to assess consumer creditworthiness with precision, fairness and efficiency.AI credit scoring addresses traditional limitations by introducing more advanced, data-driven techniques. Instead of relying solely on static, historical data points, AI models can process vast amounts of diverse information in real time, spotting patterns and predicting behaviors more accurately. How AI is being used in credit scoring Traditional credit scoring has long relied on structured data such as payment history, credit utilization, and length of credit history. While effective, these models can be limited in capturing a holistic view of an individual’s financial behavior. AI credit scoring expands this view by: Leveraging alternative data: AI models can analyze non-traditional data sources such as rental payments, utility bills, and even digital transaction histories, providing a broader perspective for those with limited credit history. Real-time analysis: Machine learning enables lenders to evaluate applicants faster by instantly processing large amounts of data. Pattern recognition: AI systems identify subtle behavioral and financial patterns that may indicate creditworthiness beyond what traditional models can detect. Continuous learning: Unlike static scoring systems, AI-based models may improve over time as they ingest more data and refine their predictions. Using these methods, AI credit score systems create a richer, more nuanced picture of a borrower’s financial health, making lending more inclusive and predictive. The benefits of AI credit scoring The adoption of AI in credit scoring has created significant benefits for lenders, regulators, and consumers alike: Improved accuracy: AI models draw on a broader range of data, reducing reliance on limited or outdated metrics. Financial inclusion: Millions of consumers globally remain outside the traditional credit system. AI credit scoring allows lenders to evaluate previously overlooked applicants, such as young adults, recent immigrants, or gig economy workers. By factoring in alternative data, lenders can serve historically underserved individuals. Faster and more efficient processes: AI can automate large portions of the decision-making workflow, significantly reducing the time it takes to approve applications. This means faster access to credit for consumers and reduced operational costs for lenders. Fraud detection and risk mitigation: Advanced machine learning models can detect anomalies in borrower behavior that may indicate fraud or identity theft. By flagging these risks earlier, lenders protect both themselves and their customers. Enhanced customer experience: AI-driven insights help lenders design more personalized products and repayment plans. Institutions can better understand customer needs and financial behaviors by offering tailored solutions that improve loyalty and trust. Challenges of AI in credit scoring While the promise of AI is transformative, it also brings new challenges that financial institutions must navigate carefully. Bias and fairness: AI models may inadvertently replicate biases in training data, raising concerns about fairness and equity. Transparency: Complex algorithms can be challenging to explain to regulators, lenders, and consumers, creating a "black box" perception. Data privacy: Using alternative data for credit scoring requires strict compliance with privacy regulations and consumer consent. Regulatory alignment: As AI evolves, credit scoring must comply with evolving financial and consumer protection laws. Why partner with us At Experian®, we understand that trust, accuracy, and transparency are essential in the financial ecosystem. By combining decades of expertise in credit data with AI solutions, we deliver AI credit score solutions that empower lenders to make smarter, fairer, and faster decisions. With us as your trusted partner, you can embrace AI-powered credit solutions confidently and responsibly. Global data expertise: We leverage one of the world’s most comprehensive credit databases, ensuring high-quality insights. Responsible AI: Our solutions are built with fairness, transparency, and regulatory compliance at the forefront. Proven results: We partner with financial institutions worldwide to unlock opportunities for lenders and consumers through AI-driven insights. Commitment to inclusion: Our AI credit scoring tools are designed to expand financial access for underserved communities. The rise of AI credit scoring marks a new era in financial services, where accuracy, speed, and inclusivity converge to benefit lenders and consumers alike. While challenges remain, responsible use of AI ensures that credit scoring becomes more transparent, fair, and effective. Learn more

Nearly 19 million U.S. households remain unbanked or credit-invisible,1 not due to a lack of financial responsibility but because traditional credit models alone may not include key financial behaviors. These individuals often save, earn and budget wisely, yet conventional scoring systems do not recognize them. We’ve recently partnered with Plaid, the trusted leader in open finance, to change that. Together, we’re putting cash flow underwriting front and center — giving lenders access to real-time, consumer-permissioned financial data that paints a fuller, more accurate picture of creditworthiness. Why cash flow data matters now In the U.S., many consumers with limited credit histories want to build their profiles but don’t know how. Cash flow underwriting bridges this gap. Cash flow insights reveal real-world financial activity — like income patterns, spending habits and account balances — in real time. This empowers lenders to make smarter, faster and more inclusive credit decisions, while helping consumers gain access to the financial services they deserve. What cash flow insights deliver By incorporating cashflow data into your decisioning strategy, you can: See beyond the score with a richer view of a consumer’s financial health. Accelerate approvals with more accurate and timely insights. Expand access to credit while strengthening portfolio diversity and reducing risk. Download our infographic to see how cash flow underwriting is reshaping lending — and how you can lead the change. Download infographic 1Mullen, C. (2024, November 13). Underbanked US population grows to 14.2%, FDIC finds. Banking Dive.

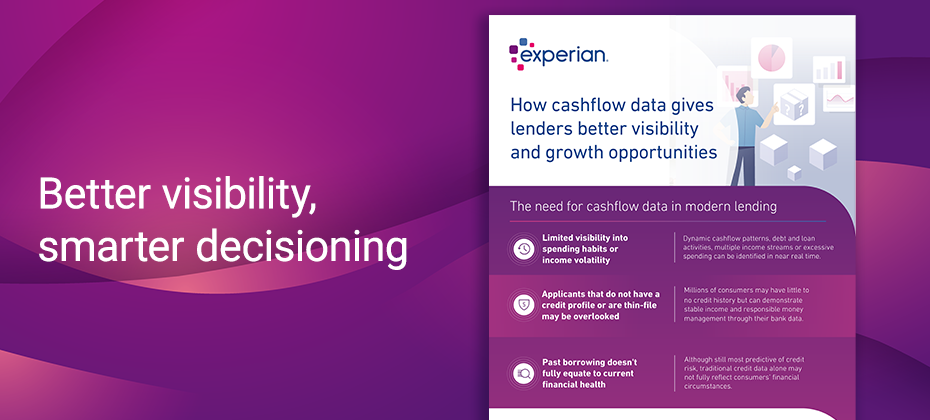

In today’s evolving economic climate, lenders face a growing challenge: how to accurately assess creditworthiness — especially for consumers with limited credit histories. That’s where cash flow insights come into play. Our latest infographic illustrates how cashflow data helps lenders achieve a more comprehensive understanding of borrowers' financial health. What you'll learn: Why cashflow data is essential for modern, inclusive lending The key financial behaviors that cash flow insights can uncover How these insights help lenders expand market reach and make more precise decisions Read the infographic to learn more. View infographic

Experian and Plaid are teaming up to power smarter, faster, and more inclusive lending — fueled by real-time cash flow insights. The financial landscape is becoming more dynamic and digitally connected. Consumers are increasingly turning to digital platforms not only to pay bills and track spending, but to better understand their financial health, monitor their credit standing, and plan confidently for the future. This evolution presents a timely opportunity for innovation in underwriting — one that empowers consumers to take control of their financial futures and enables lenders to make faster, smarter, and more inclusive decisions. What happens when the leading global data and technology company joins forces with the largest open banking network in the world? Experian and Plaid are coming together to solve some of the most pressing challenges lenders face, bringing cash flow insights into credit decisions, seamlessly. Smarter lending: Elevating the credit decision process For lenders seeking a holistic view of borrowers to make faster, more informed decisions, this new collaboration is a game-changer. Experian and Plaid are combining real-time, unmatched cash flow data and analytics to help lenders improve decisioning, pinpoint risk precisely, and drive financial inclusion. This marks a pivotal shift in how credit is assessed, moving us toward faster, and fundamentally smarter lending decisions. This strategic collaboration delivers real-time cash flow insights in a comprehensive solution, built on core principles designed to directly enhance your lending capabilities: Speed and simplicity: Driving efficiency with seamless integration In today’s fast-paced financial landscape, efficiency in underwriting isn’t just an advantage; it’s a necessity. Our combined solution prioritizes speed and simplicity by offering easy integration through APIs. This ensures fast access to meaningful risk insights, streamlining your workflows. Imagine easily leveraging real-time cashflow risk insights directly into your existing processes for faster and smarter lending decisions. This is about delivering modern infrastructure that allows you to move at the speed of today's market, empowering your business to expand with confidence. Broader visibility: Unveiling a holistic consumer view Traditional credit scores are a reliable, crucial tool for measuring a borrower’s creditworthiness. When coupled with real-time cashflow data and risk insights, lenders are empowered with broader visibility, bringing to light a more holistic view of a borrower’s current financial reality and opportunities that may have been missed. You gain a comprehensive consumer financial picture, allowing for more precise identification of both strong financial capacity and potential risks, ultimately helping you target and acquire customers who align with your growth objectives. Smarter decisions: Enhancing models with combined intelligence The power to make truly informed decisions hinges on the quality and depth of your data. Without robust insights, risk models can be limited, impacting precision and speed. With Experian's advanced cash flow analytic capabilities and Plaid's streamlined access to real-time cash flow data via Consumer Report, you can enhance your risk assessment for smarter decisions. This synergy empowers financial institutions to expand credit access and uncover hidden risks, leading to more precise underwriting. It’s about leveraging advanced analytics in real-time to drive improved decision-making and build stronger portfolios. More inclusive lending: Expanding access, responsibly A significant challenge in lending is ensuring access for all creditworthy individuals, including those with limited traditional credit histories who may be overlooked. This represents an untapped market and a vital opportunity for responsible growth. Our solution champions more inclusive lending, enabling you to reach underserved communities and empower consumers who demonstrate strong financial capacity. This not only fosters stronger portfolios but critically helps your business grow by efficiently acquiring customers across a broader spectrum. Proven trust: Lending with confidence In the financial industry, the bedrock of any solution is trust – in the data, security, and partners. Lenders require unwavering confidence in the tools they adopt. This collaboration is built on proven trust, leveraging the reach, reliability, and security of two of the most trusted names in financial services. Experian’s expertise in credit data and consumer protection, combined with Plaid’s modern infrastructure and trusted open banking network, offers unparalleled assurance. You can securely integrate these powerful insights, knowing you are backed by industry leaders committed to best-in-class security and compliance, enabling your business to grow with confidence without compromise. Smarter lending starts now The evolution of underwriting demands a more dynamic, inclusive, and precise approach. With Experian and Plaid, you're not just adapting to change; you're leading it. Empower your organization to approve more borrowers, reduce risk more effectively, and make smarter, faster decisions for sustainable success. Ready to transform your lending strategy? Learn more about how to bring cash flow insights into your credit decisions seamlessly. Learn more

Customer retention is crucial for lenders to maximize lifetime value, especially during economic uncertainty. Increasing customer retention rates by just 5% can boost profits by 25% to 95%. However, many lenders struggle with loyalty, as seen in Q2 2024 when mortgage servicers’ retention rates for refinances dropped to 20%, the second lowest in 17 years. Nonbanks and banks also saw significant declines. This is due to increased competition, changing economic conditions, and a lack of personalization. Key strategies for improving customer retention Lenders can improve retention by leveraging data for personalization, maintaining consistent communication, offering loyalty rewards, and utilizing retention triggers. Leverage data for personalization. Use customer data to offer tailored products and refinancing options based on financial behaviors. Using credit attributes, trended data and alternative credit data (alternative financial services data, cashflow attributes, etc.) can help provide deeper insights of your customers. Maintain consistent communication. Keep customers informed with regular updates about interest rate changes or new loan products. Use a variety of communication channels, including email and in-app messaging, to ensure customers are kept in the loop. Ensure your customer service team is always available and responsive, offering clear answers to any financial concerns. Offer loyalty rewards. Develop programs that reward repeat business and referrals. Offer special rates or discounts for returning customers or for those who refer friends and family to your services. Increase customer lifetime value (LTV) by offering additional services like financial planning or credit score monitoring. Utilize retention triggers. Identify key events for engagement with automated retention triggers. For example, a borrower who has a mortgage with a fixed rate may be less likely to consider refinancing unless prompted. Experian’s Retention TriggersSM can notify lenders when refinancing might be beneficial to their customer, offering them personalized incentives or new product options at the right time. Why Experian’s Retention Triggers? By integrating Experian’s Retention Triggers, lenders can keep borrowers engaged, increase retention, and boost profitability even in tough economic times. Advanced data insights: Gain deeper insights into your customers’ behavior to identify those at risk of leaving and take proactive action. Personalized engagement: Automate personalized communications based on customer behaviors, ensuring timely engagement. Increased revenue: By offering personalized, timely and relevant offers, you can increase the likelihood of retaining your customers and growing your revenue. Make customer retention a priority In today’s challenging economic climate, lenders who focus on personalized experiences, consistent communication, and relevant offers will stand out and retain borrowers. Leverage tools like Experian’s Retention Triggers to proactively engage customers, reduce churn, and foster long-term relationships for increased profitability and success. Learn more

Gen Z, or "Zoomers," born from 1997 to 2012, are molded by modern transformations. They have witnessed events from post-9/11 impacts to the rise of the internet and the COVID-19 crisis. As early adopters of technology, their lives are intertwined with smartphones, online shopping, social platforms, cloud services, emerging fintech, and artificial intelligence. They are called “digital natives” as they are the first generation to grow up with internet as part of their daily life. Research generally indicates that this post-millennial generation values practicality, favoring financial stability over entrepreneurial pursuits. They appreciate communication tailored to them and often employ social media to cultivate their personal brands. As a generation growing up immersed in technology, they tend to choose digital interactions, seeking to forge robust, secure, genuine, and unconstrained digital experiences. The challenge of identity verification Identity verification presents a considerable challenge for Generation Z. According to a Fortune survey, close to 50% of this demographic regrets not opening financial accounts earlier, citing a lack of readiness to join the financial ecosystem by the age of 18. Consequently, this has given rise to "digital ghosts"—people with minimal or nonexistent financial histories who face challenges when trying to utilize financial services. The 2009 Credit Card Accountability Responsibility and Disclosure Act mandates that individuals under 21 need a cosigner or show income proof to get a credit card, hindering their early financial involvement. Moreover, conventional identity checks are becoming less reliable due to the surge in identity theft. Innovative solutions for verifying Gen Z Verifying identities and preventing fraud among Gen Z presents unique challenges due to their digital-native status and limited credit histories. Here are some effective strategies and approaches that financial institutions can adopt to address these challenges: Leveraging alternative data sources Academic records leverage information from higher learning institutions such as universities, colleges, and vocational schools. This data can be vital for authenticating the identities of younger individuals who may lack a substantial credit history. Employment verification retrieve data confirming the identity and employment status, especially focusing on Gen Z who are new to the job market. Utility and telecom records leverage payment histories for utilities, phone bills, and other recurring services, which can provide additional layers of identity verification. Alternative financial data includes online small dollar lenders, online installment lenders, single payment, line of credit, storefront small dollar lenders, auto title and rent-to-own. Phone-Centric ID Phone-Centric Identity refers to technology that leverages and analyzes mobile, telecom, and other signals for the purposes of identity verification, identity authentication, and fraud prevention. Phone-Centric Identity relies on billions of signals from authoritative sources pulled in real time, making it a powerful proxy for digital identity and trust. Advance authentication technologies Behavioral biometrics analyze user behaviors such as typing patterns, navigation habits, and device usage. These subtle behaviors can help create a unique profile for each user, making it difficult for fraudsters to impersonate them. Adaptive risk-based authentication that adjusts the level of security based on the user's behavior, location, device, and other factors. For example, a higher level of verification might be required for transactions that are deemed unusual or high-risk. Real-time fraud detection AI and machine learning: Deploy AI and machine learning algorithms to analyze transaction patterns and detect anomalies in real-time. These technologies can identify suspicious activities and flag potential fraud. Fraud analytics: Use predictive analytics to assess the likelihood of fraud based on historical data and current behavior. This approach helps in proactively identifying and mitigating fraudulent activities. Secure digital onboarding Digital identity verification: Implement digital onboarding processes that include online identity verification with real-time document verification. Users can upload government-issued IDs and take selfies to confirm their identity. Video KYC (Know Your Customer): Use video calls to conduct KYC processes, allowing bank representatives to verify identities and documents remotely via automated identity verification. This method is secure and convenient for tech-savvy Gen Z customers. Make identity verification easy To authenticate identities and combat fraud within the Gen Z population, financial organizations need to implement a comprehensive strategy utilizing innovative technologies, non-traditional data, and strong protective protocols. Such actions will enable the creation of a trustworthy and frictionless banking environment that appeals to a generation adept in digital interactions, thereby establishing trust and encouraging enduring connections. To learn more about Experian’s automated identity verification solutions, visit our website. Learn more

Open banking is revolutionizing the financial services industry by encouraging a shift from a closed model to one with greater transparency, competition, and innovation. But what does this mean for financial institutions, and how can you adapt to this new landscape, balancing opportunity against risk? In this article, we will define open banking, illustrate how it operates, and weigh the challenges and benefits for financial institutions. What is open banking? Open banking stands at the forefront of financial innovation, embodying a shift toward a more inclusive, transparent, and consumer-empowered system. At its core, open banking relies on a simple yet powerful premise: it uses consumer-permissioned data to create a networked banking ecosystem that benefits both financial institutions and consumers alike. By having secure, standardized access to consumer financial data — granted willingly by the customers themselves — lenders can gain incredibly accurate insights into consumer behavior, enabling them to personalize services and offers like never before. How does open banking work? Open banking is driven by Application Programming Interfaces (APIs), which are sets of protocols that allow different software components to communicate with each other and share data seamlessly and securely. In the context of open banking, these APIs enable: Account Information Services (AIS): These services allow third-party providers (TPPs) to access account information from financial institutions (with customer consent) to provide budgeting and financial planning services. Payment Initiation Services (PIS): These services permit TPPs to initiate payments on behalf of customers, often offering alternative, faster, or cheaper payment solutions compared to traditional banking methods. Financial institutions must develop and maintain robust and secure APIs that TPPs can integrate with. This requires significant investment in technology and cybersecurity to protect customer data and financial assets. There must also be clear customer consent procedures and data-sharing agreements between financial institutions and TPPs. Benefits of open banking Open banking is poised to create a wave of innovation in the financial sector. One of the most significant benefits is the ability to gain a more comprehensive view of a consumer’s financial situation. With a deeper view of consumer cashflow data and access to actionable insights, you can improve your underwriting strategy, optimize account management and make smarter decisions to safely grow your portfolio. Additionally, open banking promotes financial inclusion by enabling financial institutions to offer more tailored products that suit the needs of previously underserved or unbanked populations. This inclusivity can help bridge the gap in financial services, making them accessible to a broader segment of the population. Furthermore, open banking fosters competition among financial institutions and fintech companies, leading to the development of better products, services, and competitive pricing. This competitive environment not only benefits consumers but also challenges banks to innovate, improve their services, and operate more efficiently. The collaborative nature of open banking encourages an ecosystem where traditional banks and fintech startups co-create innovative open banking solutions. This synergy can accelerate the pace of digital transformation within the banking sector, leading to the development of cutting-edge technologies and platforms that address specific market gaps or consumer demands. Challenges of open banking While open banking presents a plethora of opportunities, its adoption is not without challenges. Financial institutions must grapple with several hurdles to fully leverage the benefits open banking offers. One of the most significant challenges is fraud detection in banking and ensuring data security and privacy. The sharing of financial data through APIs necessitates robust cybersecurity measures to protect sensitive information from breaches and fraud. Banks and TPPs alike must invest in advanced security technologies and protocols to safeguard customer data. Additionally, regulatory compliance poses a considerable challenge. Open banking regulations vary widely across different jurisdictions, requiring banks to adapt their operations to comply with diverse legal frameworks. Staying abreast of evolving regulations and ensuring compliance can be resource-intensive and complex. Furthermore, customer trust and awareness are crucial to the success of open banking. Many consumers are hesitant to share their financial data due to privacy concerns. Educating customers on the benefits of open banking and the measures taken to ensure their data’s security is essential to overcoming this obstacle. Despite these challenges, the strategic implementation of open banking can unlock remarkable opportunities for innovation, efficiency, and service enhancement in the financial sector. Banks that can successfully navigate these hurdles and capitalize on the advantages of open banking are likely to emerge as leaders in the new era of financial services. Our open banking strategy Our newly introduced open banking solution, Cashflow Attributes, powered by Experian’s proprietary data from millions of U.S. consumers, offers unrivaled categorization and valuable consumer insights. The combination of credit and cashflow data empowers lenders with a deeper understanding of consumers. Furthermore, it harnesses our advanced capabilities to categorize 99% of transaction Demand Deposit Account (DDA) and credit card data, guaranteeing dependable inputs for robust risk assessment, targeted marketing and proactive fraud detection. Watch open banking webinar Learn more about Cashflow Attributes

Over the past few decades, the financial industry has gone through significant changes. One of the most notable changes is the use of alternative credit data1 for lending. This type of data is becoming increasingly essential in consumer and small business lending. In this blog post, we’ll explore the importance of alternative credit data and the insights you can gain from our new 2023 State of Alternative Credit Data Report. Benefits and uses of alternative credit data and alternative lending Alternative credit data and alternative financial services offer substantial benefits to lenders, borrowers, and society as a whole. The primary advantage of alternative credit data is that it provides a more comprehensive and accurate credit history of the borrower. Unlike traditional credit data that focuses on a borrower’s financial past, alternative credit data includes information from non-traditional sources like rent payments, full-file public records, utility bills, and income and employment data. This additional data allows you to gain a better understanding of financial behavior and assess creditworthiness more accurately.Alternative credit data can be used throughout the loan lifecycle, from underwriting to servicing. In the underwriting phase, alternative credit data can help lenders expand their pool of potential borrowers, especially those who lack or have limited traditional credit history. Additionally, alternative credit data can help lenders identify risks and minimize fraud. In the servicing phase, alternative credit data can help lenders monitor financial health and provide relevant services and an enhanced customer experience.Alternative lending is critical for driving financial inclusion and profitability. Traditional credit models often exclude individuals who have limited or no access to credit, causing them to turn to high-cost alternatives like payday loans. Alternative credit data can provide a more accurate assessment of their ability to pay, making it easier for them to access affordable credit. This increased accessibility improves the borrower's financial health and creates new opportunities to expand your customer base. “Lenders can access credit data and real-time information about consumers’ incomes, employment statuses, and how they are managing their finances and get a more accurate view of a consumer’s financial situation than previously possible.”— Scott Brown, President of Consumer Information Services, Experian State of alternative credit data Our new 2023 State of Alternative Credit Data Report provides exclusive insight into the alternative lending market, new data sources, inclusive finance opportunities and innovations in credit attributes and scoring that are making credit scoring more accurate, transparent and inclusive. For instance, the use of machine learning algorithms and artificial intelligence is enabling lenders to develop more predictive alternative credit scoring models and enhance risk assessment. Findings from the report include: 54% of Gen Z and 52% of millennials feel more comfortable using alternative financing options rather than traditional forms of credit.2 62% of financial institution firms are using alternative data to improve risk profiling and credit decisioning capabilities.3 Modern credit scoring methods could allow lenders to grow their pool of new customers by almost 20%.4 By understanding the power of alternative credit data and staying on top of the latest industry trends, you can widen your pool of borrowers, drive financial inclusion, and grow sustainably. Download now 1When we refer to “Alternative Credit Data,” this refers to the use of alternative data and its appropriate use in consumer credit lending decisions, as regulated by the Fair Credit Reporting Act. Hence, the term “Expanded FCRA Data” may also apply in this instance and both can be used interchangeably.2Experian commissioned Atomik Research to conduct an online survey of 2,001 adults throughout the United States. Researchers controlled for demographic variables such as gender, age, geographic region, race and ethnicity in order to achieve similar demographic characteristics reported in the U.S. census. The margin of error of the overall sample is +/-2 percentage points with a confidence level of 95 percent. Fieldwork took place between August 22 and August 28, 2023. Atomik Research is a creative market research agency. 3Experian (2022). Reaching New Heights with Financial Inclusion 4Oliver Wyman (2022). Financial Inclusion and Access to Credit

Alternative credit scoring has become mainstream. Lenders that use alternative credit scores can find opportunities to expand their lending universe without taking on additional risk and more accurately assess the credit risk of traditionally scoreable consumers. Obtaining a more holistic consumer view can help lenders improve automation and efficiency throughout the customer lifecycle. What is alternative credit scoring? Alternative credit scoring models incorporate alternative credit data* that isn't typically found on consumer credit reports. These scores aren't necessarily trying to predict alternative outcomes. The goal is the same — to understand the likelihood that a borrower will miss payments in the future. What's different is the information (and sometimes the analytical techniques) that inform these predictions.Traditional credit scoring models solely consider information found in consumer credit reports. There's a lot of information there — Experian's consumer credit database has data on over 245 million consumers. But although traditional consumer data can be insightful, it doesn't necessarily give lenders a complete picture of consumers' creditworthiness. Alternative credit scores draw from additional data sources, including: Alternative financial services: Credit data from alternative financial services (AFS) can tell you about consumers' experiences with small-dollar installment loans, single-payment loans, point-of-sale financing, auto title loans and rent-to-own agreements. Buy Now Pay Later: Buy Now Pay Later (BNPL) borrowing is popular with consumers across the scoring spectrum, and lenders can use access to open BNPL loans to better assess consumers' current capacity. Rental payments: Landlords, property managers, collection companies, rent payment services and consumer-permissioned data can give lenders access to consumers' rent payment history. Full-file public records: Credit reports generally only include bankruptcy records from the previous seven to ten years. However, lenders with access to full-file public records can also learn about consumers' property deeds, address history, and professional and occupational licenses. READ: Take a deep dive into Experian's State of Alternative Credit Data report to learn more about the different types of alternative credit data and uses across the loan lifecycle. With open banking, consumers can now easily and securely share access to their banking and brokerage account data — and they're increasingly comfortable doing so. In fact, 70% would likely share their banking data for better loan rates, financial tools or personalized spending insights.Tools like Experian Boost allow consumers to add certain types of positive payment information to their Experian credit reports, including rent, utility and select streaming service payments. Some traditional scores consider these additional data points, and users have seen their FICO Score 8 from Experian boosted by an average of 13 points.1 Experian Go also allows credit invisible consumers to establish a credit report with consumer-permissioned alternative data. The benefits of using alternative credit data The primary benefit for lenders is access to new borrowers. Alternative credit scores help lenders accurately score more consumers — identifying creditworthy borrowers who might otherwise be automatically denied because they don't qualify for traditional credit scores. The increased access to credit may also align with lenders' financial inclusion goals.Lenders may additionally benefit from a more precise understanding of consumers who are scoreable. When integrated into a credit decisioning platform, the alternative scores could allow lenders to increase automation (and consumers' experiences) without taking on more credit risk. The future of alternative credit scoring Alternative credit scoring might not be an alternative for much longer, and the future looks bright for lenders who can take advantage of increased access to data, advanced analytics and computing power.Continued investment in alternative data sources and machine learning could help bring more consumers into the credit system — breaking barriers and decreasing the cost of basic lending products for millions. At the same time, lenders can further customize offers and automate their operations throughout the customer lifecycle. Partnering with Experian Small and medium-sized lenders may lack the budget or expertise to unlock the potential of alternative data on their own. Instead, lenders can turn to off-the-shelf alternative models that can offer immediate performance lifts without a heavy IT investment.Experian's Lift PlusTM score draws on industry- leading mainstream credit data and FCRA-regulated alternative credit data to provide additional consumer behavior insights. It can score 49% of mainstream credit-invisible consumers and for thin file consumers with a new trade, a 29% lift in scoreable accounts. Learn more about our alternative credit data scoring solutions. Learn more * When we refer to “Alternative Credit Data," this refers to the use of alternative data and its appropriate use in consumer credit lending decisions as regulated by the Fair Credit Reporting Act (FCRA). Hence, the term “Expanded FCRA Data" may also apply in this instance and both can be used interchangeably.1Experian (2023). Experian Boost

With consumers having more credit options than ever before, it’s imperative for lenders to get their message in front of ideal customers at the right time and place. But without clear insights into their interests, credit behaviors or financial capacity, you may risk extending preapproved credit offers to individuals who are unqualified or have already committed to another lender. To increase response rates and reduce wasted marketing spend, you must develop an effective customer targeting strategy. What makes an effective customer targeting strategy? A customer targeting strategy is only as good as the data that informs it. To create a strategy that’s truly effective, you’ll need data that’s relevant, regularly updated, and comprehensive. Alternative data and credit-based attributes allow you to identify financially stressed consumers by providing insight into their ability to pay, whether their debt or spending has increased, and their propensity to transfer balances and consolidate loans. With a more granular view of consumers’ credit behaviors over time, you can avoid high-risk accounts and focus only on targeting individuals that meet your credit criteria. While leveraging additional data sources can help you better identify creditworthy consumers, how can you improve the chances of them converting? At the end of the day, it’s also the consumer that’s making the decision to engage, and if you aren’t sending the right offer at the precise moment of interest, you may lose high-value prospects to competitors who will. To effectively target consumers who are most likely to respond to your credit offers, you must take a customer-centric approach by learning about where they’ve been, what their goals are, and how to best cater to their needs and interests. Some types of data that can help make your targeting strategy more customer-centric include: Demographic data like age, gender, occupation and marital status, give you an idea of who your customers are as individuals, allowing you to enhance your segmentation strategies. Lifestyle and interest data allow you to create more personalized credit offers by providing insight into your consumers’ hobbies and pastimes. Life event data, such as new homeowners or new parents, helps you connect with consumers who have experienced a major life event and may be receptive to event-based marketing campaigns during these milestones. Channel preference data enables you to reach consumers with the right message at the right time on their preferred channel. Target high-potential, high-value prospects By using an effective customer targeting strategy, you can identify and engage creditworthy consumers with the greatest propensity to accept your credit offer. To see if your current strategy has what it takes and what Experian can do to help, view this interactive checklist or visit us today. Review your customer targeting strategy Visit us

Even before the COVID-19 pandemic, many Americans lacked equal access to financial products and services — from tapping into affordable banking services to credit cards to financing a home purchase. The global pandemic likely exacerbated those existing issues and inequalities. That reality makes financial inclusion — a concerted effort to make financial products and services affordable and accessible to all consumers — more crucial than ever. The playing field wasn't level before the pandemic The Federal Reserve reported that in 2019, Black and Hispanic/Latino families had median wealth that was just 13 to 19 percent of that of White families — $24,100 and $36,100, respectively, compared to $188,200 for White families. That inequity is also reflected in credit score disparities. While credit scores, income, and wealth aren't synonymous, the traditional credit scoring system leads marginalized communities to be disproportionately labeled unscoreable or credit invisible, and face challenges in accessing credit. New research from Experian shows that in over 200 cities, there can be more than a 100-point difference in credit scores between neighborhoods — often within just a few miles from each other. Marginalized communities bore the financial brunt Minority communities were also disproportionately impacted by COVID-19 in terms of infections, job losses, and financial hardship. In mid-2020, the Economic Policy Institute (EPI) reported Black and Hispanic/Latino workers were more likely than White workers to have lost their jobs or to be classified as essential workers — leading to economic or health insecurity. Government initiatives — including the Coronavirus Aid, Relief, and Economic Security (CARES) Act, the Paycheck Protection Program (PPP) and the American Rescue Plan — created expanded unemployment benefits, paused loan payments, eviction moratoriums, and direct cash payments. These helped consumers' immediate financial well-being. The National Bureau of Economic Research found that, on average, U.S. households spent approximately 40 percent of their first two stimulus checks, with about 30 percent used for savings and another 30 percent used to pay down debt. In some communities highly affected by COVID-19, consumers were able to pay down nearly 40 percent of their credit card balances and close more than 9 percent of their bank card accounts, according to recent data. Stimulus payments have been credited with reducing childhood poverty and helping families save for financial emergencies. That being said, people on the upper end of the income scale were able to improve their financial situation even more. Their wealth grew at a much faster pace than people at the bottom end of the income distribution scale, according to data from the Federal Reserve. How the pandemic deepened financial exclusion Although hiring has picked up in low-wage industries, research indicates that low-wage jobs have been the slowest to return. According to a survey by the Pew Research Center, among respondents who said their financial situation worsened during the pandemic, 44 percent believe it will take three years or more to get back to where they were a year ago. About 10 percent don't think their finances will ever recover. Recent Experian data shows that consumers in certain communities that were already struggling to pay their debts fell into an even bigger hole. These consumers missed payments on 56 percent more accounts in the period between spring 2019 to spring 2020 compared to the year prior. Credit scores in these neighborhoods fell by an average of over 20 points during the first 18 months of COVID-19. That being said, U.S. consumers overall increased their median credit scores by an average of 21 points from the end of 2019 to the end of 2021. When consumers with deteriorating credit encounter financial stresses, often their only recourse is to pile on additional debt. Even worse, those who can't access traditional credit often turn to alternative credit arrangements, such as short-term loans, which may charge significantly higher interest rates. READ MORE: More Than a Score: The Case for Financial Inclusion What can the financial sector do? Without access to affordable financial services and products, subprime or credit invisible consumers may not get approved for a mortgage or car loan — things that might come much easier for consumers with better scores. This is just one reason why financial inclusion is so important — and why financial services companies have a big role to play in driving it. One place to start is by taking a broader view of what makes a creditworthy consumer. In addition to traditional credit scoring models, new tools can leverage artificial intelligence and machine learning, along with alternative data, to analyze the creditworthiness of consumers. By qualifying for credit, more consumers can access affordable mortgages, car loans, business loans and insurance - freeing up money for other expenses and allowing them to grow their wealth.. READ MORE: What Is Alternative and Non-Traditional Data? Last word Marginalized communities were already struggling economically before the pandemic, and the impact of COVID-19 has made the wealth disparities worse. With the pandemic waning, now is the time for financial institutions to take action on financial inclusion. Not only does it help improve your customers' lives and make them better prepared for the next crisis, but it also fuels your business's growth and bottom line.