Tag: financial services trends

Nearly 19 million U.S. households remain unbanked or credit-invisible,1 not due to a lack of financial responsibility but because traditional credit models alone may not include key financial behaviors. These individuals often save, earn and budget wisely, yet conventional scoring systems do not recognize them. We’ve recently partnered with Plaid, the trusted leader in open finance, to change that. Together, we’re putting cash flow underwriting front and center — giving lenders access to real-time, consumer-permissioned financial data that paints a fuller, more accurate picture of creditworthiness. Why cash flow data matters now In the U.S., many consumers with limited credit histories want to build their profiles but don’t know how. Cash flow underwriting bridges this gap. Cash flow insights reveal real-world financial activity — like income patterns, spending habits and account balances — in real time. This empowers lenders to make smarter, faster and more inclusive credit decisions, while helping consumers gain access to the financial services they deserve. What cash flow insights deliver By incorporating cashflow data into your decisioning strategy, you can: See beyond the score with a richer view of a consumer’s financial health. Accelerate approvals with more accurate and timely insights. Expand access to credit while strengthening portfolio diversity and reducing risk. Download our infographic to see how cash flow underwriting is reshaping lending — and how you can lead the change. Download infographic 1Mullen, C. (2024, November 13). Underbanked US population grows to 14.2%, FDIC finds. Banking Dive.

BNPL is a misunderstood form of credit. In fact, many consumers are unaware that it is credit at all and view it simply as a mode of payment. This guide debunks common BNPL myths to explain what BNPL data will mean for lenders and consumers. In the past year, Experian collected more than 130 million buy now, pay later (BNPL) records from four major BNPL fintech lenders and conducted the most comprehensive analysis of BNPL data available today. The results provided valuable insights on: Who are the consumers using BNPL loans? What is the nature of their current mainstream credit relationships? What do their current BNPL behaviors look like? BNPL myth-busting: Who’s using it, how much are they spending and how risky are BNPL loans? Since BNPL launched in the United States in the 2010s, BNPL has exploded into the consciousness of online shoppers, especially during the COVID-19 pandemic. According to Forrester, Millennials are the biggest adopters of BNPL at 18%, followed by their younger counterparts in Gen Z at 11%.1 But looking at statistics like these without additional analysis could be problematic. The dramatic growth of leading BNPL fintechs such as Klarna, Affirm and Afterpay has demonstrated how strongly these services resonate with consumers and retailers. The growth of BNPL has attracted the attention of established lenders interested in capitalizing on the popularity of these services (while also looking to minimize its impact on their existing services, such as credit cards or personal loans). Meanwhile, the Consumer Financial Protection Bureau (CFPB) has urged caution about potential risks, calling for more consistent consumer protections market-wide and transparency into consumer debt accumulation and overextension across lenders. The underlying assumptions debated are that BNPL is used: Predominantly by young people with limited incomes and credit history To pay for frequent, low-value purchases using a cheap and readily available source of credit As a result, it is often seen as a riskier form of lending. But are these assumptions correct? Using data from more than 130 million BNPL transactions from four leading BNPL fintech lenders, we’ve obtained a more detailed and comprehensive understanding of BNPL users and their defining features. Our findings look somewhat different to the popular stereotypes. Myth 1: BNPL is used only for low-value purchases According to our analysis, most BNPL purchases, 95 percent are for items costing $300 or less.2 Some of it is low-value, but not all. In fact, we found that the average purchase using BNPL was similar to that of a credit card, at $132.Average transaction sizes have increased 10 percent year-over-year, and we now see BNPL purchases for goods costing well over $1,000. We also see that consumers take out an average of 5 BNPL loans in a year and 23 percent of them have loans with more than one BNPL provider at a time. Myth 2: BNPL is simply an easier payment method Consumers see BNPL as a simple, quick and convenient way to pay. But, as shoppers receive goods for which payment is deferred, it’s also a form of credit. However, unlike short-term high-interest loans, BNPL credit comes at zero cost to the borrower, with some, but not all BNPL fintech providers charging late payment fees – fueling many borrowers’ sense that it’s an easy way to pay, rather than a loan. Myth 3: Only Gen Z shoppers aged 25 and below are using BNPL Younger shoppers are slightly more represented in the data transactions, but our analysis shows consumers of all ages use BNPL. BNPL is going mainstream, and its appeal is widening. The average age of BNPL consumers is 36 years old, with an average credit history of 9 years.2 The ease of use of these services at the checkout means they have a broad appeal. Over half of U.S. adults have reported using a BNPL service at least once. Despite Millennials and Gen Z having used BNPL financing the most, Gen Xers are not too far behind in usage, with 52% having used it.2 We anticipate that in the use of BNPL will continue to grow as more customers become more familiar with the benefits, and the diversification of products continues. Understanding the opportunities this growth presents to both consumers and lenders is critical to protecting their interests. And helping to facilitate access to credit, enabling responsible spending, while also limiting risks and providing services that consumers can afford is also critical. Download the full guide for additional myths we’re exposing We will take a deep dive into what our early data analysis suggests about the market and the BNPL myths our analysis is exposing. Additionally, we will examine: Why BNPL data matters to providers and lenders How BNPL data can improve visibility of consumers’ creditworthiness Ways in which transparency of BNPL data could benefit consumers 1The Buy Now, Pay Later (BNPL) Opportunity,” Forrester Report, April 29, 2022.2Experian data and analytics derived from 130M+ BNPL transactions

How businesses respond to economic uncertainty can determine whether they get ahead or fall behind. To better prepare for the coming months, you must remain up to date on the latest economic developments to better understand and evolve with changing consumer needs. With insight into critical macroeconomic and consumer trends, you can proactively manage your portfolio, enhance your decisioning and seize new opportunities. Grab a cup of coffee and join Experian's Shawn Rife, Client Executive, and Josee Farmer, Economic Analyst, during our fireside chat on February 16 @ 1 P.M. ET/10 A.M. PT. Our expert speakers will provide a view of the latest economic and market trends, their impact on consumers, and how financial institutions can survive and thrive. Highlights include: Macroeconomic and consumer credit trends Economic implications on consumer behavior How financial institutions can adapt Register now

There are many facets to promoting a more equitable society. One major driver is financial inclusion or reducing the racial wealth gap for underserved communities. No other tool has impacted generational wealth more than sustainable homeownership. However, the underserved and underbanked home buyers experience more barriers to entry than any other consumer segment. It is important to recognize the well-documented racial and ethnic homeownership gap; doing so will not only benefit the impacted communities, but also elevate the level of support of those lenders who serve them. What are we doing as an industry to reduce this gap? Many organizations are doing their part in removing barriers to homeownership and systemic inequities. In 2021, the FHFA published their Duty to Serve 2021 plans for Fannie Mae and Freddie Mac to focus on historically underserved markets. A part of this plan includes increasing liquidity of mortgage financing for lower- and moderate-income families. Fannie Mae and Freddie Mac each announced individual refinance offerings for lower-income homeowners – Fannie Mae’s RefiNow™ and Freddie Mac’s Refi PossibleSM. Eligible borrowers meet requirements including income at or below 100% area median income (AMI), a minimum credit score of 620, consideration for loans in forbearance and additional newly expanded flexibilities. As part of the plan, lenders will lower a borrower’s monthly payment by at least a half a percentage point reduction in their interest rate, which can translate into hundreds of dollars of savings per month and sustain their homeownership. Experian has the tools to help mortgage lenders take advantage of this offering As a leader in data, analytics and technology, we have the tools needed to help lenders recognize opportunities to be inclusive and identify borrowers who may be eligible for Fannie Mae’s and Freddie Mac’s lower-income refinance offerings. To illustrate, we performed a data study and identified over 6M eligible mortgages nationwide (impacting over 8M borrowers) for this plan, and some lenders had as much as 30% of mortgages in their portfolio eligible with lower- and moderate-incomes.1 These insights can have a positive impact on the borrowers you serve by promoting more inclusion and benefit lenders through improved customer retention, strengthened customer loyalty and an opportunity to continue to build generational wealth through housing. We are committed to enabling the industry's DEI evolution As the Consumer’s bureau, empowering consumers is at the heart of everything we do. We’re committed to developing products and services that increase credit access, greater inclusion in homeownership and narrowing the racial wealth gap. Below are a few of our recent initiatives, and be sure to check out our financial inclusion resources here: United for Financial Health: Promotes inclusion in underserved communities through partnerships and have committed to investing our time and resources to create a more inclusive tomorrow for our communities. Project REACh (Roundtable for Economic Access and Change): brings together leaders from banking, business, technology, and national civil rights organizations to reduce barriers that prevent equal and fair participation in the nation’s economy, and we are engaged with the Alternative Credit Scoring Utility group as part of this initiative. Operation Hope: Empowers youth and underserved communities to improve their financial health through education, so they can thrive (not just survive) in the credit ecosystem so they can sustain good credit and responsibly use credit. DEI-Centric Solutions: From Experian Boost to our recent launch of Experian Go, we offer a variety of consumer solutions designed to empower consumers to gain access to credit and build a brighter financial future. What does this mean for you? Our passion, knowledge and partnerships in DEI have enabled us to share best practices and can help lenders prescriptively look at their portfolios to create inclusive growth strategies, identify gaps, and track progress towards diversity objectives. The mortgage industry has a unique opportunity to create paths to homeownership for underserved communities. Together, we can drive impact for generations of Americans to come. Let’s drive inclusivity and revive the American dream of homeownership. 1Experian Ascend™ as of November 2021

Nearly 28 million American consumers are credit invisible, and another 21 million are unscorable.1 Without a credit report, lenders can’t verify their identity, making it hard for them to obtain mortgages, credit cards and other financial products and services. To top it off, these consumers are sometimes caught in cycles of predatory lending; they have trouble covering emergency expenses, are stuck with higher interest rates and must put down larger deposits. To further our mission of helping consumers gain access to fair and affordable credit, Experian recently launched Experian GOTM, a first-of-its-kind program aimed at helping credit invisibles take charge of their financial health. Supporting the underserved Experian Go makes it easy for credit invisibles and those with limited credit histories to establish, use and grow credit responsibly. After authenticating their identity, users will have their Experian credit report created and will receive educational guidance on improving their financial health, including adding bill payments (phone, utilities and streaming services) through Experian BoostTM. As of January 2022, U.S. consumers have raised their scores by over 87M total points with Boost.2 From there, they’ll receive personalized recommendations and can accept instant card offers. By leveraging Experian Go, disadvantaged consumers can quickly build credit and become scorable. Expanding your lending portfolio So, what does this mean for lenders? With the ability to increase their credit score (and access to financial literacy resources), thin-file consumers can more easily meet lending eligibility requirements. Applicants on the cusp of approval can move to higher score bands and qualify for better loan terms and conditions. The addition of expanded data can help you make a more accurate assessment of marginal consumers whose ability and willingness to pay aren’t wholly recognized by traditional data and scores. With a more holistic customer view, you can gain greater visibility and transparency around inquiry and payment behaviors to mitigate risk and improve profitability. Learn more Download white paper 1Data based on Oliver Wyman analysis using a random sample of consumers with Experian credit bureau records as of September 2020. Consumers are considered ‘credit invisible’ when they have no mainstream credit file at the credit bureaus and ‘unscorable’ when they have partial information in their mainstream credit file, but not enough to generate a conventional credit score. 2https://www.experian.com/consumer-products/score-boost.html

Experian recently announced the new members named to its Fintech Advisory Board. The board and its members provide Experian with valuable insights and key perspectives into the unique and quickly evolving needs of the fintech industry. “For years Experian has been committed to partnering with innovators in the fintech industry to bring better opportunities to businesses and consumers alike,” said Experian North American CEO Craig Boundy. “We appreciate the thought leadership we get from our Fintech Advisory Board members and the challenge and the push that comes along with it,” he said. The board met virtually last month, welcoming representatives from across the fintech ecosystem representing payments, personal and secured loan lenders, credit card issuers, investors and others. “This was my first board meeting with Experian, and I’m very pleased to see the investment Experian has put into being the best of the three major bureaus in having the best technology to enable us to turnaround our models more quickly, and better data and alternative data sources like Boost,” said one of the new executives appointed to the board. “We are delighted to gather this group of innovators together to ensure we are consistently meeting the needs of our fintech partners,” said Experian Vice President Jon Bailey, who oversees the fintech vertical. “Now more than ever it’s important that we work alongside them in shaping the industry and helping them meet their goals for the future,” he said. Experian’s fintech vertical provides leading-edge solutions and data across the credit lifecycle specifically designed to impact Fintech and marketplace lending companies and their customers. For more information on Experian’s fintech services or the advisory board, click here.

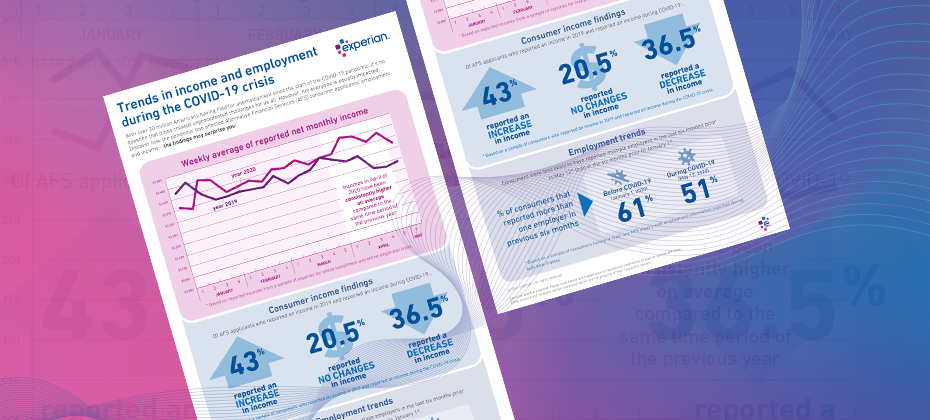

With many individuals finding themselves in increasingly vulnerable positions due to COVID-19, lenders must refine their policies based on their consumers’ current financial situations. Alternative Financial Services (AFS) data helps you gain a more comprehensive view of today's consumer. The COVID-19 pandemic has had far-reaching economic consequences, leading to drastic changes in consumers’ financial habits and behavior. When it comes to your consumers, are you seeing the full picture? See if you qualify for a complimentary hit rate analysis Download AFS Trends Report

With new legislation, including the Coronavirus Aid, Relief, and Economic Security (CARES) Act impacting how data furnishers will report accounts, and government relief programs offering payment flexibility, data reporting under the coronavirus (COVID-19) outbreak can be complicated. Especially when it comes to small businesses, many of which are facing sharp declines in consumer demand and an increased need for capital. As part of our recently launched Q&A perspective series, Greg Carmean, Experian’s Director of Product Management and Matt Shubert, Director of Data Science and Modelling, provided insight on how data furnishers can help support small businesses amidst the pandemic while complying with recent regulations. Check out what they had to say: Q: How can data reporters best respond to the COVID-19 global pandemic? GC: Data reporters should make every effort to continue reporting their trade experiences, as losing visibility into account performance could lead to unintended consequences. For small businesses that have been negatively affected by the pandemic, we advise that when providing forbearance, deferrals be reported as “current”, meaning they should not adversely impact the credit scores of those small business accounts. We also recommend that our data reporters stay in close contact with their legal counsel to ensure they follow CARES Act guidelines. Q: How can financial institutions help small businesses during this time? GC: The most critical thing financial institutions can do is ensure that small businesses continue to have access to the capital they need. Financial institutions can help small businesses through deferral of payments on existing loans for businesses that have been most heavily impacted by the COVID-19 crisis. Small Business Administration (SBA) lenders can also help small businesses take advantage of government relief programs, like the Payment Protection Program (PPP), available through the CARES Act that provides forgiveness on up to 75% of payroll expenses and 25% of other qualifying expenses. Q: How do financial institutions maintain data accuracy while also protecting consumers and small businesses who may be undergoing financial stress at this time? GC: Following bureau recommendations regarding data reporting will be critical to ensure that businesses are being treated fairly and that the tools lenders depend on continue to provide value. The COVID-19 crisis also provides a great opportunity for lenders to educate their small business customers on their business credit. Experian has made free business credit reports available to every business across the country to help small business owners ensure the information lenders are using in their credit decisioning is up-to-date and accurate. Q: What is the smartest next play for financial institutions? GC: Experian has several resources that lenders can leverage, including Experian’s COVID-19 Business Risk Index which identifies the industries and geographies that have been most impacted by the COVID crisis. We also have scores and alerts that can help financial institutions gain greater insights into how the pandemic may impact their portfolios, especially for accounts with the greatest immediate exposure and need. MS: To help small businesses weather the storm, financial institutions should make it simple and efficient for them to access the loans and credit they need to survive. With cash flow to help bridge the gap or resume normal operations, small businesses can be more effective in their recovery processes and more easily comply with new legislation. Finances offer the support needed to augment currently reduced cash flows and provide the stability needed to be successful when a return to a more normal business environment occurs. At Experian, we’re closely monitoring the updates around the coronavirus outbreak and its widespread impact on both consumers and businesses. We will continue to share industry-leading insights to help data furnishers navigate and successfully respond to the current environment. Learn more About Our Experts Greg Carmean, Director of Product Management, Experian Business Information Services, North America Greg has over 20 years of experience in the information industry specializing in commercial risk management services. In his current role, he is responsible for managing multiple product initiatives including Experian’s Small Business Financial Exchange (SBFE), domestic and international commercial reports and Corporate Linkage. Recently, he managed the development and launch of Experian’s Global Data Network product line, a commercial data environment that provides a single source of up to date international credit and firmographic information from Experian commercial bureaus and Tier 1 partners across the globe. Matt Shubert, Director of Data Science and Modelling, Experian Data Analytics, North America Matt leads Experian’s Commercial Data Sciences Team which consists of a combination of data scientists, data engineers and statistical model developers. The Commercial Data Science Team is responsible for the development of attributes and models in support of Experian’s BIS business unit. Matt’s 15+ years of experience leading data science and model development efforts within some of the largest global financial institutions gives our clients access to a wealth of knowledge to discover the hidden ROI within their own data.

It seems like artificial intelligence (AI) has been scaring the general public for years – think Terminator and SkyNet. It’s been a topic that’s all the more confounding and downright worrisome to financial institutions. But for the 30% of financial institutions that have successfully deployed AI into their operations, according to Deloitte, the results have been anything but intimidating. Not only are they seeing improved performance but also a more enhanced, positive customer experience and ultimately strong financial returns. For the 70% of financial institutions who haven’t started, are just beginning their journey or are in the middle of implementing AI into their operations, the task can be daunting. AI, machine learning, deep learning, neural networks—what do they all mean? How do they apply to you and how can they be useful to your business? It’s important to demystify the technology and explain how it can present opportunities to the financial industry as a whole. While AI seems to have only crept into mainstream culture and business vernacular in the last decade, it was first coined by John McCarthy in 1956. A researcher at Dartmouth, McCarthy thought that any aspect of learning or intelligence could be taught to a machine. Broadly, AI can be defined as a machine’s ability to perform cognitive functions we associate with humans, i.e. interacting with an environment, perceiving, learning and solving problems. Machine learning vs. AI Machine learning is not the same thing as AI. Machine learning is the application of systems or algorithms to AI to complete various tasks or solve problems. Machine learning algorithms can process data inputs and new experiences to detect patterns and learn how to make the best predictions and recommendations based on that learning, without explicit programming or directives. Moreover, the algorithms can take that learning and adapt and evolve responses and recommendations based on new inputs to improve performance over time. These algorithms provide organizations with a more efficient path to leveraging advanced analytics. Descriptive, predictive, and prescriptive analytics vary in complexity, sophistication, and their resulting capability. In simplistic terms, descriptive algorithms describe what happened, predictive algorithms anticipate what will happen, and prescriptive algorithms can provide recommendations on what to do based on set goals. The last two are the focus of machine learning initiatives used today. Machine learning components - supervised, unsupervised and reinforcement learning Machine learning can be broken down further into three main categories, in order of complexity: supervised, unsupervised and reinforcement learning. As the name might suggest, supervised learning involves human interaction, where data is loaded and defined and the relationship to inputs and outputs is defined. The algorithm is trained to find the relationship of the input data to the output variable. Once it delivers accurately, training is complete, and the algorithm is then applied to new data. In financial services, supervised learning algorithms have a litany of uses, from predicting likelihood of loan repayment to detecting customer churn. With unsupervised learning, there is no human engagement or defined output variable. The algorithm takes the input data and structures it by grouping it based on similar characteristics or behaviors, without a defined output variable. Unsupervised learning models (like K-means and hierarchical clustering) can be used to better segment or group customers by common characteristics, i.e. age, annual income or card loyalty program. Reinforcement learning allows the algorithm more autonomy in the environment. The algorithm learns to perform a task, i.e. optimizing a credit portfolio strategy, by trying to maximize available rewards. It makes decisions and receives a reward if those actions bring the machine closer to achieving the total available rewards, i.e. the highest acquisition rate in a customer category. Over time, the algorithm optimizes itself by correcting actions for the best outcomes. Even more sophisticated, deep learning is a category of machine learning that involves much more complex architecture where software-based calculators (called neurons) are layered together in a network, called a neural network. This framework allows for much broader, complex data ingestion where each layer of the neural network can learn progressively more complex elements of the data. Object classification is a classic example, where the machine ‘learns’ what a duck looks like and then is able to automatically identify and group images of ducks. As you might imagine, deep learning models have proved to be much more efficient and accurate at facial and voice recognition than traditional machine learning methods. Whether your financial institution is already seeing the returns for its AI transformation or is one of the 61% of companies investing in this data initiative in 2019, having a clear picture of what is available and how it can impact your business is imperative. How do you see AI and machine learning impacting your customer acquisition, underwriting and overall customer experience?

To provide consumers with clear-cut protections against disturbance by debt collectors, the Consumer Financial Protection Bureau (CFPB) issued a Notice of Proposed Rulemaking (NPRM) to implement the Fair Debt Collection Practices Act (FDCPA) earlier this year. Among many other things, the proposal would set strict limits on the number of calls debt collectors may place to reach consumers weekly and clarify requirements for consumer-facing debt collection disclosures. A bigger discussion Deliberation of the debt collection proposal was originally scheduled to begin on August 18, 2019. However, to allow commenters to further consider the issues raised in the NPRM and gather data, the comment period was extended by 20 days to September 18, 2019. It is currently still being debated, as many argue that the proposed rule does not account for modern consumer preferences and hinders the free flow of information used to help consumers access credit and services. The Association of Credit and Collection Professionals (ACA International) and US House lawmakers continue to challenge the proposal, stating that it doesn’t ensure that debt collectors’ calls to consumers are warranted, nor does it do enough to protect consumers’ privacy. Many consumer advocates have expressed doubts about how effective the proposed measures will be in protecting debtors from debt collector harassment and see the seven-calls-a-week limit on phone contact as being too high. In fact, it’s difficult to find a group of people in full support of the proposal, despite the CFPB stating that it will help clarify the FDCPA, protect lenders from litigation and bring consumer protection regulation into the 21st century. What does this mean? Although we don’t know when, or if, the proposed rule will go into effect, it’s important to prepare. According to the Federal Register, there are key ways that the new regulation would affect debt collection through the use of newer technologies, required disclosures and limited consumer contact. Not only will the proposed rules apply to debt collectors, but its provisions will also impact creditors and servicers, making it imperative for everyone in the financial services space to keep watch on the regulation’s status and carefully analyze its proposed rules. At Experian, our debt collection solutions automate and moderate dialogues and negotiations between consumers and collectors, making it easier for collection agencies to connect with consumers while staying compliant. Our best-in-class data and analytics will play a key role in helping you reach the right consumer, in the right place, at the right time. Learn more

The future is, factually speaking, uncertain. We don't know if we'll find a cure for cancer, the economic outlook, if we'll be living in an algorithmic world or if our work cubical mate will soon be replaced by a robot. While futurists can dish out some exciting and downright scary visions for the future of technology and science, there are no future facts. However, the uncertainty presents opportunity. Technology in today's world From the moment you wake up, to the moment you go back to sleep, technology is everywhere. The highly digital life we live and the development of our technological world have become the new normal. According to The International Telecommunication Union (ITU), almost 50% of the world's population uses the internet, leading to over 3.5 billion daily searches on Google and more than 570 new websites being launched each minute. And even more mind-boggling? Over 90% of the world's data has been created in just the last couple of years. With data growing faster than ever before, the future of technology is even more interesting than what is happening now. We're just at the beginning of a revolution that will touch every business and every life on this planet. By 2020, at least a third of all data will pass through the cloud, and within five years, there will be over 50 billion smart connected devices in the world. Keeping pace with digital transformation At the rate at which data and our ability to analyze it are growing, businesses of all sizes will be forced to modify how they operate. Businesses that digitally transform, will be able to offer customers a seamless and frictionless experience, and as a result, claim a greater share of profit in their sectors. Take, for example, the financial services industry - specifically banking. Whereas most banking used to be done at a local branch, recent reports show that 40% of Americans have not stepped through the door of a bank or credit union within the last six months, largely due to the rise of online and mobile banking. According to Citi's 2018 Mobile Banking Study, mobile banking is one of the top three most-used apps by Americans. Similarly, the Federal Reserve reported that more than half of U.S. adults with bank accounts have used a mobile app to access their accounts in the last year, presenting forward-looking banks with an incredible opportunity to increase the number of relationship touchpoints they have with their customers by introducing a wider array of banking products via mobile. Be part of the movement Rather than viewing digital disruption as worrisome and challenging, embrace the uncertainty and potential that advances in new technologies, data analytics and artificial intelligence will bring. The pressure to innovate amid technological progress poses an opportunity for us all to rethink the work we do and the way we do it. Are you ready? Learn more about powering your digital transformation in our latest eBook. Download eBook Are you an innovation junkie? Join us at Vision 2020 for future-facing sessions like: - Cloud and beyond - transforming technologies - ML and AI - real-world expandability and compliance

In today’s age of digital transformation, consumers have easy access to a variety of innovative financial products and services. From lending to payments to wealth management and more, there is no shortage in the breadth of financial products gaining popularity with consumers. But one market segment in particular – unsecured personal loans – has grown exceptionally fast. According to a recent Experian study, personal loan originations have increased 97% over the past four years, with fintech share rapidly increasing from 22.4% of total loans originated to 49.4%. Arguably, the rapid acceleration in personal loans is heavily driven by the rise in digital-first lending options, which have grown in popularity due to fintech challengers. Fintechs have earned their position in the market by leveraging data, advanced analytics and technology to disrupt existing financial models. Meanwhile, traditional financial institutions (FIs) have taken notice and are beginning to adopt some of the same methods and alternative credit approaches. With this evolution of technology fused with financial services, how are fintechs faring against traditional FIs? The below infographic uncovers industry trends and key metrics in unsecured personal installment loans: Still curious? Click here to download our latest eBook, which further uncovers emerging trends in personal loans through side-by-side comparisons of fintech and traditional FI market share, portfolio composition, customer profiles and more. Download now

Today is National Fintech Day – a day that recognizes the ever-important role that fintech companies play in revolutionizing the customer experience and altering the financial services landscape. Fintech. The word itself has become synonymous with constant innovation, agile technology structures and being on the cusp of the future of finance. Fintech challengers are disrupting existing financial models by leveraging data, advanced analytics and technology – both inspiring traditional financial institutions in their digital transformation strategies and giving consumers access to a variety of innovative financial products and services. But to us at Experian, National Fintech Day means more than just financial disruption. National Fintech Day represents the partnerships we have carefully fostered with our fintech clients to drive financial inclusion for millions of people around the globe and provide consumers with greater control and more opportunities to access the quality credit they deserve. “We are actively seeking out unresolved problems and creating products and technologies that will help transform the way businesses operate and consumers thrive in our society. But we know we can’t do it alone,” said Experian North American CEO, Craig Boundy in a recent blog article on Experian’s fintech partnerships. “That’s why over the last year, we have built out an entire team of account executives and other support staff that are fully dedicated to developing and supporting partnerships with leading fintech companies. We’ve made significant strides that will help us pave the way for the next generation of lending while improving the financial health of people around the world.” At Experian, we understand the challenges fintechs face – and our real-world solutions help fintech clients stay ahead of constantly changing market conditions and demands. “Experian’s pace of innovation is very impressive – we are helping both lenders and consumers by delivering technological solutions that make the lending ecosystem more efficient,” said Experian Senior Account Executive Warren Linde. “Financial technology is arguably the most important type of tech out there, it is an honor to be a part of Experian’s fintech team and help to create a better tomorrow.” If you’d like to learn more about Experian’s fintech solutions, visit us at Experian.com/Fintech.

Financial institutions preparing for the launch of the Financial Accounting Standard Board’s (FASB) new current expected credit loss model, or CECL, may have concerns when it comes to preparedness, implications and overall impact. Gavin Harding, Experian’s Senior Business Consultant and Jose Tagunicar, Director of Product Management, tackled some of the tough questions posed by the new accounting standard. Check out what they had to say: Q: How can financial institutions begin the CECL transition process? JT: To prepare for the CECL transition process, companies should conduct an operational readiness review, which includes: Analyzing your data for existing gaps. Determining important milestones and preparing for implementation with a detailed roadmap. Running different loss methods to compare results. Once losses are calculated, you’ll want to select the best methodology based on your portfolio. Q: What is required to comply with CECL? GH: Complying with CECL may require financial institutions to gather, store and calculate more data than before. To satisfy CECL requirements, financial institutions will need to focus on end-to-end management, determine estimation approaches that will produce reasonable and supportable forecasts and automate their technology and platforms. Additionally, well-documented CECL estimations will require integrated workflows and incremental governance. Q: What should organizations look for in a partner that assists in measuring expected credit losses under CECL? GH: It’s expected that many financial institutions will use third-party vendors to help them implement CECL. Third-party solutions can help institutions prepare for the organization and operation implications by developing an effective data strategy plan and quantifying the impact of various forecasted conditions. The right third-party partner will deliver an integrated framework that empowers clients to optimize their data, enhance their modeling expertise and ensure policies and procedures supporting model governance are regulatory compliant. Q: What is CECL’s impact on financial institutions? How does the impact for credit unions/smaller lenders differ (if at all)? GH: CECL will have a significant effect on financial institutions’ accounting, modeling and forecasting. It also heavily impacts their allowance for credit losses and financial statements. Financial institutions must educate their investors and shareholders about how CECL-driven disclosure and reporting changes could potentially alter their bottom line. CECL’s requirements entail data that most credit unions and smaller lenders haven’t been actively storing and saving, leaving them with historical data that may not have been recorded or will be inaccessible when it’s needed for a CECL calculation. Q: How can Experian help with CECL compliance? JT: At Experian, we have one simple goal in mind when it comes to CECL compliance: how can we make it easier for our clients? Our Ascend CECL ForecasterTM, in partnership with Oliver Wyman, allows our clients to create CECL forecasts in a fraction of the time it normally takes, using a simple, configurable application that accurately predicts expected losses. The Ascend CECL Forecaster enables you to: Fulfill data requirements: We don’t ask you to gather, prepare or submit any data. The application is comprised of Experian’s extensive historical data, delivered via the Ascend Technology PlatformTM, economic data from Oxford Economics, as well as the auto and home valuation data needed to generate CECL forecasts for each unsecured and secured lending product in your portfolio. Leverage innovative technology: The application uses advanced machine learning models built on 15 years of industry-leading credit data using high-quality Oliver Wyman loan level models. Simplify processes: One of the biggest challenges our clients face is the amount of time and analytical effort it takes to create one CECL forecast, much less several that can be compared for optimal results. With the Ascend CECL Forecaster, creating a forecast is a simple process that can be delivered quickly and accurately. Q: What are immediate next steps? JT: As mentioned, complying with CECL may require you to gather, store and calculate more data than before. Therefore, it’s important that companies act now to better prepare. Immediate next steps include: Establishing your loss forecast methodology: CECL will require a new methodology, making it essential to take advantage of advanced statistical techniques and third-party solutions. Making additional reserves available: It’s imperative to understand how CECL impacts both revenue and profit. According to some estimates, banks will need to increase their reserves by up to 50% to comply with CECL requirements. Preparing your board and investors: Make sure key stakeholders are aware of the potential costs and profit impacts that these changes will have on your bottom line. Speak with an expert

What is CECL? CECL (Current Expected Credit Loss) is a new credit loss model, to be leveraged by financial institutions, that estimates the expected loss over the life of a loan by using historical information, current conditions and reasonable forecasts. According to AccountingToday, CECL is considered one of the most significant accounting changes in decades to affect entities that borrow and lend money. To comply with CECL by the assigned deadline, financial institutions will need to access much more data than they’re currently using to calculate their reserves under the incurred loss model, Allowance for Loan and Lease Losses (ALLL). How does it impact your business? CECL introduces uncertainty into accounting and growth calculations, as it represents a significant change in the way credit losses are currently estimated. The new standard allows financial institutions to calculate allowances in a variety of ways, including discounted cash flow, loss rates, roll-rates and probability of default analyses. “Large banks with historically good loss performance are projecting increased reserve requirements in the billions of dollars,” says Experian Advisory Services Senior Business Consultant, Gavin Harding. Here are a few changes that you should expect: Larger allowances will be required for most products As allowances will increase, pricing of the products will change to reflect higher capital cost Losses modeling will change, impacting both data collection and modeling methodology There will be a lower return on equity, especially in products with a longer life expectancy How can you prepare? “CECL compliance is a journey, rather than a destination,” says Gavin. “The key is to develop a thoughtful, data-driven approach that is tested and refined over time.” Financial institutions who start preparing for CECL now will ultimately set their organizations up for success. Here are a few ways to begin to assess your readiness: Create a roadmap and initiative prioritization plan Calculate the impact of CECL on your bottom line Run altered scenarios based on new lending policy and credit decision rules Understand the impact CECL will have on your profitability Evaluate current portfolios based on CECL methodology Run different loss methods and compare results Additionally, there is required data to capture, including quarterly or monthly loan-level account performance metrics, multiple year data based on loan product type and historical data for the life of the loan. How much time do you have? Like most accounting standards, CECL has different effective dates based on the type of reporting entity. Public business entities that file financial statements with the Security and Exchange Commission will have to comply by 2020, non-public entity banks must comply by 2022 and non-SEC registered companies have until 2023 to adopt the new standard. How can we help: Complying with CECL may require you to gather, store and calculate more data than before. Experian can help you comply with CECL guidelines including data needs, consulting and loan loss calculation. Experian industry experts will help update your current strategies and establish an appropriate timeline to meet compliance dates. Leveraging our best-in-class industry data, we will help you gain CECL compliance quickly and effectively, understand the impacts to your business and use these findings to improve overall profitability. Learn more