Tag: identity

Now in its tenth year, Experian’s U.S. Identity and Fraud Report continues to uncover the shifting tides of fraud threats and how consumers and businesses are adapting. Our latest edition sheds light on a decade of change and unveils what remains consistent: trust is still the cornerstone of digital interactions. This year’s report draws on insights from over 2,000 U.S. consumers and 200 businesses to explore how identity, fraud and trust are evolving in a world increasingly shaped by generative artificial intelligence (GenAI) and other emerging technologies. Highlights: Over a third of companies are using AI, including generative AI, to combat fraud. 72% of business leaders anticipate AI-generated fraud and deepfakes as major challenges by 2026. Nearly 60% of companies report rising fraud losses, with identity theft and payment fraud as top concerns. Digital anxiety persists with 57% of consumers worried about doing things online. Ready to go deeper? Explore the full findings and discover how your organization can lead with confidence in an evolving fraud landscape. Download report Watch on-demand webinar Read press release

As Valentine’s Day approaches, hearts will melt, but some will inevitably be broken by romance scams. This season of love creates an opportune moment for scammers to prey on individuals feeling lonely or seeking connection. Financial institutions should take this time to warn customers about the heightened risks and encourage vigilance against fraud. In a tale as heart-wrenching as it is cautionary, a French woman named Anne was conned out of nearly $855,000 in a romance scam that lasted over a year. Believing she was communicating with Hollywood star Brad Pitt; Anne was manipulated by scammers who leveraged AI technology to impersonate the actor convincingly. Personalized messages, fabricated photos, and elaborate lies about financial needs made the scam seem credible. Anne’s story, though extreme, highlights the alarming prevalence and sophistication of romance scams in today’s digital age. According to the Federal Trade Commission (FTC), nearly 70,000 Americans reported romance scams in 2022, with losses totaling $1.3 billion—an average of $4,400 per victim. These scams, which play on victims’ emotions, are becoming increasingly common and devastating, targeting individuals of all ages and backgrounds. Financial institutions have a crucial role in protecting their customers from these schemes. The lifecycle of a romance scam Romance scams follow a consistent pattern: Feigned connection: Scammers create fake profiles on social media or dating platforms using attractive photos and minimal personal details. Building trust: Through lavish compliments, romantic conversations, and fabricated sob stories, scammers forge emotional bonds with their targets. Initial financial request: Once trust is established, the scammer asks for small financial favors, often citing emergencies. Escalation: Requests grow larger, with claims of dire situations such as medical emergencies or legal troubles. Disappearance: After draining the victim’s funds, the scammer vanishes, leaving emotional and financial devastation in their wake. Lloyds Banking Group reports that men made up 52% of romance scam victims in 2023, though women lost more on average (£9,083 vs. £5,145). Individuals aged 55-64 were the most susceptible, while those aged 65-74 faced the largest losses, averaging £13,123 per person. Techniques scammers use Romance scammers are experts in manipulation. Common tactics include: Fabricated sob stories: Claims of illness, injury, or imprisonment. Investment opportunities: Offers to “teach” victims about investing. Military or overseas scenarios: Excuses for avoiding in-person meetings. Gift and delivery scams: Requests for money to cover fake customs fees. How financial institutions can help Banks and financial institutions are on the frontlines of combating romance scams. By leveraging technology and adopting proactive measures, they can intercept fraud before it causes irreparable harm. 1. Customer education and awareness Conduct awareness campaigns to educate clients about common scam tactics. Provide tips on recognizing fake profiles and unsolicited requests. Share real-life stories, like Anne’s, to highlight the risks. 2. Advanced data capture solutions Implement systems that gather and analyze real-time customer data, such as IP addresses, browsing history, and device usage patterns. Use behavioral analytics to detect anomalies in customer actions, such as hesitation or rushed transactions, which may indicate stress or coercion. 3. AI and machine learning Utilize AI-driven tools to analyze vast datasets and identify suspicious patterns. Deploy daily adaptive models to keep up with emerging fraud trends. 4. Real-time fraud interception Establish rules and alerts to flag unusual transactions. Intervene with personalized messages before transfers occur, asking “Do you know and trust this person?” Block transactions if fraud is suspected, ensuring customers’ funds are secure. Collaborating for greater impact Financial institutions cannot combat romance scams alone. Partnerships with social media platforms, AI companies, and law enforcement are essential. Social media companies must shut down fake profiles proactively, while regulatory frameworks should enable banks to share information about at-risk customers. Conclusion Romance scams exploit the most vulnerable aspects of human nature: the desire for love and connection. Stories like Anne’s underscore the emotional and financial toll these scams take on victims. However, with robust technological solutions and proactive measures, financial institutions can play a pivotal role in protecting their customers. By staying ahead of fraud trends and educating clients, banks can ensure that the pursuit of love remains a source of joy, not heartbreak. Learn more

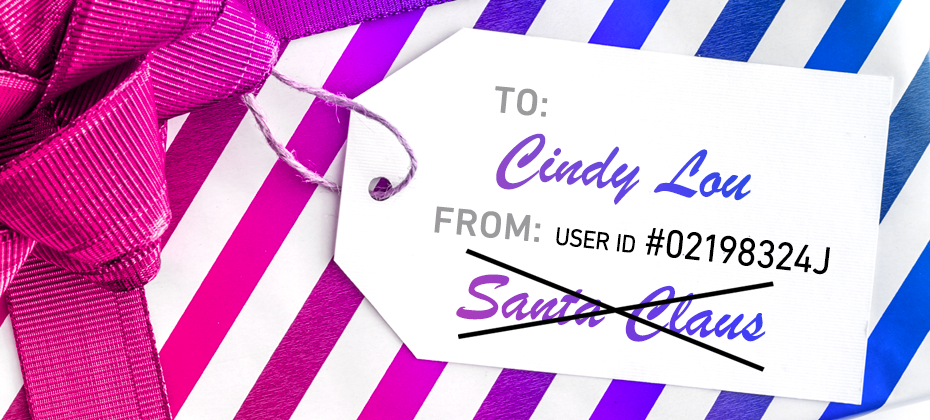

A tale of synthetic ID fraud Synthetic ID fraud is an increasing issue and affects everyone, including high-profile individuals. A notable case from Ohio involved Warren Hayes, who managed to get an official ID card in the name of “Santa Claus” from the Ohio Bureau of Motor Vehicles. He also registered a vehicle, opened a bank account, and secured an AAA membership under this name, listing his address as 1 Noel Drive, North Pole, USA. This elaborate ruse unraveled after Hayes, disguised as Santa, got into a minor car accident. When the police requested identification, Hayes presented his Santa Claus ID. He was subsequently charged under an Ohio law prohibiting the use of fictitious names. However, the court—presided over by Judge Thomas Gysegem—dismissed the charge, arguing that because Hayes had used the ID for over 20 years, "Santa Claus" was effectively a "real person" in the eyes of the law. The judge’s ruling raised eyebrows and left one glaring question unanswered: how could official documents in such a blatantly fictitious name go undetected for two decades? From Santa Claus to synthetic IDs: the modern-day threat The Hayes case might sound like a holiday comedy, but it highlights a significant issue that organizations face today: synthetic identity fraud. Unlike traditional identity theft, synthetic ID fraud does not rely on stealing an existing identity. Instead, fraudsters combine real and fictitious details to create a new “person.” Think of it as an elaborate game of make-believe, where the stakes are millions of dollars. These synthetic identities can remain under the radar for years, building credit profiles, obtaining loans, and committing large-scale fraud before detection. Just as Hayes tricked the Bureau of Motor Vehicles, fraudsters exploit weak verification processes to pass as legitimate individuals. According to KPMG, synthetic identity fraud bears a staggering $6 billion cost to banks.To perpetrate the crime, malicious actors leverage a combination of real and fake information to fabricate a synthetic identity, also known as a “Frankenstein ID.” The financial industry classifies various types of synthetic identity fraud. Manipulated Synthetics – A real person’s data is modified to create variations of that identity. Frankenstein Synthetics – The data represents a combination of multiple real people. Manufactured Synthetics – The identity is completely synthetic. How organizations can combat synthetic ID fraud A multifaceted approach to detecting synthetic identities that integrates advanced technologies can form the foundation of a sound fraud prevention strategy: Advanced identity verification tools: Use AI-powered tools that cross-check identity attributes across multiple data points to flag inconsistencies. Behavioral analytics: Monitor user behaviors to detect anomalies that may indicate synthetic identities. For instance, a newly created account applying for a large loan with perfect credit is a red flag. Digital identity verification: Implement digital onboarding processes that include online identity verification with real-time document verification. Users can upload government-issued IDs and take selfies to confirm their identity. Collaboration and data sharing: Organizations can share insights about suspected synthetic identities to prevent fraudsters from exploiting gaps between industries. Ongoing employee training: Ensure frontline staff can identify suspicious applications and escalate potential fraud cases. Regulatory support: Governments and regulators can help by standardizing ID issuance processes and requiring more stringent checks. Closing thoughts The tale of Santa Claus’ stolen identity may be entertaining, but it underscores the need for vigilance against synthetic ID fraud. As we move into an increasingly digital age, organizations must stay ahead of fraudsters by leveraging technology, training, and collaboration. Because while the idea of Spiderman or Catwoman walking into your branch may seem amusing, the financial and reputational cost of synthetic ID fraud is no laughing matter. Learn more

The risk of identity theft continues to grow yearly for consumers and businesses alike. Identity theft and fraud cases have nearly tripled over the past ten years, with cybercrime losses totaling more than $10 billion this year alone.[1] An effective way for organizations to combat these threats is to implement a policy of identity risk management. Identity risk management Identity risk management refers to the methods used by organizations to anticipate potential fraud threats, protect themselves and their consumers from those vulnerabilities, resolve any fraud incidents that may occur, and prevent future fraud events from happening again. Businesses can implement these methods through a variety of tools and technologies designed to detect fraud risks and mitigate them as quickly and efficiently as possible. By recognizing the risks of identity theft, helping consumers who fall victim to fraud, and preventing identity theft in the future, financial institutions can take an effective approach to identity risk management and ensure that their business is protected and their consumers stay safe. Recognizing risks of identity theft Identifying high-risk situations Inform consumers about high-risk situations that could lead to identity theft. Emphasize the dangers of data breaches, cyber-attacks, phishing scams, and social engineering tactics. Advise them to be cautious with personal documents and to avoid using public Wi-Fi for sensitive transactions. By raising awareness, financial institutions can help consumers stay vigilant. Risk-based authentication solutions can also help minimize risk with adaptive authentication methods. With sophisticated risk assessment and a combination of front- and back-end authentication methods, organizations can optimize the consumer experience and their identity risk management simultaneously. Protecting vulnerable information Guide consumers on safeguarding their most vulnerable information. Explain the importance of protecting Social Security numbers, credit card and bank account details, PINs, passwords, and medical records. Offer tips on securing this information and the potential consequences of it falling into the wrong hands. Providing practical advice, such as using password managers, enabling multifactor authentication, and regularly updating passwords, can significantly enhance your consumers’ security. Additionally, offering secure storage solutions for sensitive documents can further protect their information. Helping consumers who fall victim to fraud Providing immediate support If a consumer falls victim to identity theft, financial institutions should be ready to provide immediate support. Establish a clear protocol for reporting fraud and ensure that consumer service representatives are trained to handle such situations. Assist consumers in contacting their banks and credit card companies to report fraud and prevent further unauthorized transactions. Having a dedicated fraud response team can streamline this process and provide consumers with the reassurance that their issue is being handled by experts. This team can also offer personalized advice and support, making the recovery process less daunting for the victim. Helping restore identity To support consumers in the process of restoring their identity, financial institutions can offer identity restoration services as part of their consumer support. These services can include helping consumers navigate the complexities of repairing their credit, disputing fraudulent charges, and securing their accounts against future threats. Preventing identity theft in the future Enhancing personal security measures Encourage consumers to strengthen their personal security measures. Promote the use of strong, unique passwords and two-factor authentication (2FA) for all accounts. Advise them to regularly update and patch their software and devices. Offer services like secure document shredding to prevent thieves from accessing sensitive information. Financial institutions can also strengthen their identity risk management efforts by implementing robust security measures within their own systems. Demonstrating a commitment to security can build trust and encourage consumers to adopt similar practices. Implementing monitoring and alerts Financial institutions can offer identity theft protection services that include regular monitoring of credit reports and account alerts for suspicious activities. Educate consumers on the importance of closely monitoring their financial statements and bills to detect any unauthorized transactions early. Providing tools such as mobile apps that offer real-time alerts for suspicious activities can empower consumers to take immediate action if something seems amiss. Additionally, offering complimentary credit monitoring services can add an extra layer of protection. Leveraging data Data and analytics are among the most powerful tools at a financial institution’s disposal. By leveraging advanced analytics, institutions can identify patterns and anomalies that may indicate fraudulent activity. Machine learning algorithms can analyze vast amounts of transaction data in real- time, flagging suspicious behavior before it escalates into fraud. This proactive approach not only helps in early detection but also minimizes the impact on the consumer. Moreover, data analytics can streamline and improve the consumer experience by reducing false positives and ensuring that legitimate transactions are not unnecessarily flagged. This balance between security and convenience is crucial in maintaining consumer trust and satisfaction. Financial institutions can use these insights to tailor their fraud prevention strategies, using digital identity management solutions to provide more value to consumers. Behavioral analytics Fraud detection technology, such as behavioral analytics, is continually evolving as hacking methods become increasingly sophisticated. Insights from behavioral analytics can help mitigate fraud in real time and prevent identity theft, account takeover, and bot attacks — empowering businesses to provide a seamless consumer experience. Experian’s recent acquisition of NeuroID, an industry leader in behavioral analytics, means we now offer even more modern and frictionless capabilities, enhancing our fraud risk suite by providing a new layer of insight into digital behavioral signals and analytics throughout the consumer lifecycle. This additional level of defense against fraud can empower businesses to ensure that their consumers are safe and secure online. Identity management solutions Consumers are more at risk of identity theft than ever before, and it’s the responsibility of financial institutions to provide protection and support to the people they do business with. Offering identity management solutions can help organizations feel safe and secure about their consumer and business data without adding friction or functioning outside of their risk tolerance. Experian’s identity management tools allow financial institutions to confirm the identities of businesses and consumers with minimal friction, balancing end-user experience with enhanced security. This allows organizations to easily manage authentication events with confidence. Next steps Financial institutions have a vital role in helping consumers manage their risk of identity theft. By recognizing vulnerabilities, providing support to victims, and implementing preventive measures, financial institutions can protect their consumers’ personal information and financial well-being. Proactive identity risk management not only benefits consumers but also builds trust and loyalty with your brand. Protect your business from identity fraud today. Discover how Experian’s cutting-edge identity risk management solutions can safeguard your consumers and streamline your operations. Learn more about our identity management solutions This article includes content created by an AI language model and is intended to provide general information. [1] IdentityTheft.org. 2024 Identity Theft Facts and Statistics.

Financial institutions are constantly searching for ways to engage their consumers while providing valuable services that keep them financially sound and satisfied. At the same time, consumers are looking for ways to limit their risk and grow their financial power while improving and protecting their financial health. Both can be accomplished through personalized financial experiences.

In the ever-expanding financial crime landscape, envision the most recent perpetrator targeting your organization. Did you catch them? Could you recover the stolen funds? Now, picture that same individual attempting to replicate their scheme at another establishment, only to be thwarted by an advanced system flagging their activity. The reason? Both companies are part of an anti-fraud data consortium, safeguarding financial institutions (FIs) from recurring fraud. In the relentless battle against fraud and financial crime, FIs find themselves at a significant disadvantage due to stringent regulations governing their operations. Criminals, however, operate without boundaries, collaborating across jurisdictions and international borders. Recognizing the need to level the playing field, FIs are increasingly turning to collaborative solutions, such as participation in fraud consortiums, to enhance their anti-fraud and Anti-Money Laundering (AML) efforts. Understanding consortium data for fraud prevention A fraud consortium is a strategic alliance of financial institutions and service providers united in the common goal of comprehensively understanding and combatting fraud. As online transactions surge, so does the risk of fraudulent activities. However, according to Experian’s 2023 U.S. Identity and Fraud Report, 55% of U.S. consumers reported setting up a new account in the last six months despite concerns around fraud and online security. The highest account openings were reported for streaming services (43%), social media sites and applications (40%), and payment system providers (39%). Organizations grappling with fraud turn to consortium data as a robust defense mechanism against evolving fraud strategies. Consortium data for fraud prevention involves sharing transaction data and information among a coalition of similar businesses. This collaborative approach empowers companies with enhanced data analytics and insights, bolstering their ability to combat fraudulent activities effectively. The logic is simple: the more transaction data available for analysis by artificial-intelligence-powered systems, the more adept they become at detecting and preventing fraud by identifying patterns and anomalies. Advantages of data consortiums for fraud and AML teams Participation in an anti-fraud data consortium provides numerous advantages for a financial institution's risk management team. Key benefits include: Case management resolution: Members can exchange detailed case studies, sharing insights on how they responded to specific suspicious activities and financial crime incidents. This collaborative approach facilitates the development of best practices for incident handling. Perpetrator IDs: Identifying repeat offenders becomes more efficient as consortium members share data on suspicious activities. Recognizing patterns in names, addresses, device fingerprints, and other identifiers enables proactive prevention of financial crimes. Fraud trends: Consortium members can collectively analyze and share data on the frequency of various fraud attempts, allowing for the calibration of anti-fraud systems to effectively combat prevalent types of fraud. Regulatory changes: Staying ahead of evolving financial regulations is critical. Consortiums enable FIs to promptly share updates on regulatory changes, ensuring quick modifications to anti-fraud/AML systems for ongoing compliance. Who should join a fraud consortium? A fraud consortium can benefit any organization that faces fraud risks and challenges, especially in the financial industry. However, some organizations may benefit more, depending on their size, type, and fraud exposure. Some of the organizations that should consider joining a fraud consortium are: Financial institutions: Banks, credit unions, and other financial institutions are prime targets for fraudsters, who use various methods such as identity theft, account takeover, card fraud, wire fraud, and loan fraud to steal money and information from them. Fintech companies: Fintech companies are innovative and disruptive players in the financial industry, who offer new and alternative products and services such as digital payments, peer-to-peer lending, crowdfunding, and robot-advisors. Online merchants: Online merchants are vulnerable to fraudsters, who use various methods such as card-not-present fraud, friendly fraud, and chargeback fraud to exploit their online transactions and payment systems. Why partner with Experian? What companies need is a consortium that allows FIs to collaboratively research anti-fraud and AML information, eliminating the need for redundant individual efforts. This approach promotes tighter standardization of anti-crime procedures, expedited deployment of effective anti-fraud/AML solutions, and a proactive focus on preventing financial crime rather than reacting to its aftermath. Experian Hunter is a sophisticated global application fraud and risk management solution. It leverages detection rules to screen incoming application data for identifying and preventing fraudulent activities. It matches incoming application data against multiple internal and external data sources, shared fraud databases and dedicated watch lists. It uses client-flexible matching rules to crossmatch data sources for highlighting data anomalies and velocity attempts. In addition, it looks for connections to previous suspected and known fraudulent applications. Hunter generates a fraud score to indicate a fraud risk level used to prioritize referrals. Suspicious applications are moved into the case management tool for further investigation. Overall, Hunter prevents application fraud by highlighting suspicious applications, allowing you to investigate and prevent fraud without inconveniencing genuine customers. To learn more about our fraud management solutions, visit us online or request a call. Learn more This article includes content created by an AI language model and is intended to provide general information.

This article was updated on January 26, 2024. Marketers are facing new challenges as third-party cookies crumble, and people use more devices throughout the day. Someone might comparison shop on their laptop in the morning, do more research on a tablet in the afternoon and finally decide to make a purchase on their phone before falling asleep at night. Being able to track these movements and insert yourself where appropriate can be difficult, but it's not impossible. One solution that's becoming increasingly attractive is creating a unified identity for each customer — and matching every piece of data and touchpoint to the single profile. For this to work, you need identity resolution. What is identity resolution? Identity resolution is the ongoing process of linking various identifying elements to create and expand a unique identity. The multi-step process can include: Securely onboarding data into a system Hashing or tokenizing personal information to improve security and privacy Setting aside information that can't be matched to an identity yet Matching or linking identifiers to a known unique identity Verifying that the identities and identifiers are accurate An identity graph (ID graph) is an essential part of identity resolution. It's the proprietary database that can pull in and store data from different sources and link them to a unique identifier — also known as a persistent identification number. Depending on the system and purpose, identity resolution may focus on creating a single identity for a person, household, or business. The information can come from internal sources, including a customer relationship management (CRM) tool, email marketing platforms, event management platforms, social media accounts, point-of-sales systems, and other digital and offline touchpoints. Additionally, third-party data sources, such as credit or demographic data, can contribute to building a more complete identity. And second-party data — information that's shared between brands or companies — can also be helpful. As new digital and offline information is created or found, it's linked to the existing persistent identification number in the ID graph. The process can happen in different ways. The resolution system could accurately match an engagement to a person with deterministic data, such as a hashed email address, assuming they logged in. If the person didn't log in, a probabilistic model may be able to accurately attribute the session to the person's identity based on indicators that it's likely the same person, such as a device ID or behavioral data. A hybrid approach combines deterministic and probabilistic approaches, which could be important for scaling. The goal and end result is often called a holistic, single-unified, or 360-degree view of a customer. READ MORE: Making identities personal Why does identity resolution matter? Identity resolution lets you know with whom you're connecting, which can be important throughout a customer's lifecycle. From marketing to collections, you want to be able to engage the right person on the right channel with the right offer. And that's only possible when you can accurately identify people. Consistent and accurate identity resolution is difficult, though. Experian's 2023 Identity and Fraud Report found that 92% of businesses have a strategy in place for identifying consumers online. But 63% of consumers are either "somewhat confident" or "not very confident" that businesses can accurately recognize them online. What are the benefits of identity resolution? It's a worthy goal to push toward, because you can use identity resolution solutions to: Consolidate your view of customers Companies may have multiple profiles of the same customer — one from an email list, another from their loyalty program and a third from an outdated system. Your customers are also interacting with you in different ways, perhaps logging into an account from their laptop in the morning while visiting your site from a phone at night. Identity resolution lets you connect all these elements to create a single profile. Build targeted and measurable marketing campaigns Once you have a single and consistent view of your customers, you can more accurately segment and target your marketing campaigns. Personalizing messages can increase engagement and effectiveness. And, equally important, knowing to who you don't want to send messages can help you avoid wasting marketing spending. Some identity resolution services can also help you track anonymous visitors and customize your marketing with look-alike models, which can identify people who are likely part of your target audience. You'll also be able to more accurately measure the effectiveness of a campaign. With a single customer view, it's easier to know if and how a targeted social media ad, television spot and emailed coupon worked together to create a sale. Increase customer experiences across brands When implemented throughout an organization, you can also use the single view of a customer to create a consistent experience across brands and business units. Each can benefit from a more holistic understanding of the customer and can contribute to building out customers' profiles. Seamlessly confirm identities Identity resolution can also create a more frictionless experience for customers who want to create or log into your site, and it can help with detecting fraud and high-risk consumers. But keep data security top of mind. Consumers rank privacy (79%) and security (78%) much higher than login convenience (38%) when considering their online experience. What does an identity resolution solution look like? The need for and type of identity resolution can vary depending on a business' challenges and goals. For instance, large retailers often have a lot of first-party data — so much that it may be overwhelming. For them, an identity resolution solution that can organize internal data while enhancing it with external data points could be a priority. In contrast, a business with infrequent touchpoints might not have as much first-party data and could benefit from a solution that offers as much external information as possible. Some organizations are building their own internal identity resolution services to address these challenges, but many are looking to outside partners for identity resolution. When comparing partners, consider: Flexibility and scalability: Understand which data the solution can onboard and how quickly it can onboard data. Consider whether you'll want to be able to use real-time APIs or batch processing, and the limitations on how much data the provider can process at a time. Additionally, consider whether the ID graph will use persistent IDs that can change as you scale. Matching and analysis: Ask about the solution's approach and success with matching online and offline data and the options to integrate or append second and third-party data. If you want to be able to securely and privately share anonymized identities internally or with partners, make sure that's an option as well. Integration: Research whether the provider can easily integrate your existing services and vendors. Privacy: 73% of consumers say it's a business's responsibility to protect them online. Ask about the provider's experience and approach to storing and anonymizing data. Some solutions also have built-in activation tools. These let you build and launch omni-channel campaigns. They also analyze and report on how well your campaigns are performing. Get started today To learn more about the importance of digital identity and Experian's identity solutions, visit us today. Learn more

Online activity is a routine part of people’s days. Americans spend an average of 4 hours and 25 minutes on their phones every day,[1] and many regularly use multiple devices to access the internet. However, with more time spent in the digital space, the risk of identity theft and fraud also continues to grow. The growing threat of identity fraud This year, the FTC has already received 5.7 million total fraud and identity theft reports, 1.4 million of which were identity theft cases.[2] More consumers are becoming vulnerable to the threat of identity fraud, but many are unsure of how to protect themselves. To avoid monetary loss and significant lifestyle disruption, consumers are looking to their financial institutions to provide resources to help them prevent identity theft and protect their personal information online. Consumers want identity protection from their financial institutions Consumers also expect their banks to carry the responsibility of protecting their private data from the risk of theft. While most of them trust in the security provided by their banks, about 50% of consumers want their banks to offer additional protective measures.[3] This creates an opportunity for financial institutions to fulfill the role of “data protector” for the customers that depend on them. The convenience of a full suite of financial services all in one place is also important to consumers, as 45% would prefer to get all their banking products from the same financial institution.[4] While consumers need identity protection, businesses need new ways to engage their customers and drive more revenue. Fortunately, offering identity protection is an effective way to maintain a sticky relationship with your customers while delivering an enhanced, engaging experience. Protect your customers from fraud with Identity Protection Services With identity protection, your customers can: Check for exposed personal information and lower their risk of identity theft Reduce their exposure and decide who can track their activity and access their personal information online Keep control of their digital identity by reclaiming exposed personal information, increasing their privacy, and avoiding future risk An identity protection solution provides a comprehensive strategy to avoid the risk of identity theft, while delivering exceptional results that your customers need to feel safe and secure. Providing frequent updates and recommendations about their digital identity and credit score allows you to maintain an engaging communication channel with your customers and boost your brand interaction. For example, the average Experian® user had a 60% alert open rate and 12% post-alert login rate.[5] As they continue to receive useful suggestions for strengthening their online security, your customers may interact with your app or website more regularly and consistently. This can create valuable opportunities for you to encourage them to open new accounts, start new credit lines, or borrow more money. In addition, giving your customers an added layer of assurance can drive them to remain loyal, long-standing customers to your business. 96% of active Experian subscribers with a free bundle were still subscribed after 12 months[6] 90% of active Experian subscribers with a paid bundle were still subscribed after 12 months[6] Less than 1% churn rate with fewer than 100 service calls[7] Consumers want protection from thieves who might steal their personal information, and they expect it from a trusted source. By offering an identity protection solution, you can foster stronger relationships with your customers while reducing their vulnerability to fraud. Visit our website to see how Identity Protection Services can help you deliver best-in-class protection for your customers. [1] PC Magazine. Americans Check Their Phones an Alarming Number of Times Per Day. May 2023. [2] IdentityTheft.org. 2023 Identity Theft Facts and Statistics. [3] PYMTS. Half of Consumers Want More Security Measures From Banks, January 2023. [4] PYMTS. 45% of US Consumers Want Banking Bundles. August 2022. [5] Experian Data, average user experience with Digital Identity Manager, May 2023. [6] Experian data, August 2023. [7] Experian Data, average user experience with Digital Identity Manager, May 2023.

Managing digital identities is a necessity, responsibility and privilege. When done right, digital identity management solutions can help consumers feel recognized and safe. In turn, companies can build strong and personalized relationships with their customers while complying with regulatory requirements and combating hydra-like fraud attacks. What is digital identity? The concept and definition of a digital identity have expanded as everyday interactions increasingly happen in digital realms. Today, a digital identity is more than an online account. Identities can be created and depend on all the digital information associated with a unique entity, which may be a person, business or device. A person's digital identity often includes online and offline attributes that fall into one of three categories: Something a user knows, such as a username, password or PIN. Something a user has, such as a mobile phone or security token. Something that's part of the user, such as a fingerprint, iris, voice pattern, behavior or preferences. People are increasingly open to sharing this type of personal information if it serves a purpose. Our Global Identity and Fraud Report found that 57 percent of consumers are willing to share data if it ensures greater security or prevents fraud, and 63 percent of consumers think sharing data is beneficial (up from 51 percent in 2021).1 People can also use these identifiers to verify their identity at a later point. But digital identity verification tools should rely on more than user-provided verification alone. A person may have hundreds or thousands of digital interactions every day, and these can leave digital footprints that you can use to create or expand digital identities. These types of identifiers — such as search queries, geotags, behaviors and device information — can also help you authenticate a user and offer a more customized and seamless experience. However, when focusing on consumers' digital identities, it's important to remember that their identity is more than the sum of data points. A person's digital identity is unique and personal, and it should be managed accordingly. The business side's challenges A discussion of what makes up an identity can quickly turn philosophical. For instance, you can't authenticate identical twins based on a face scan or DNA test, so what is it that makes them unique? In some ways, the example gets to the heart of businesses' challenges today. To create a safe and enjoyable online identity verification experience, you need to be able to distinguish between a real person and an imitator, even when the two look nearly identical. Access to more information can make this easier, but you then need to ensure that you can keep this information secure. It can be a tricky balance, but if you get it right, your efforts will be rewarded. People want to be recognized as they move across channels and devices, and organizations want to be able to quickly and accurately identify users with a friction-right experience that also helps prevent fraud. However, while 84 percent of businesses say recognizing customers is "very" or "extremely" important, only about 33 percent of consumers are confident that they'll be repeatedly recognized online.1 There's a clear gap — and an opportunity to better meet customers' desires. Organizations across industries know they need a customer recognition strategy and 82% already have one in place.2 Some businesses address this challenge with identity platforms that are standardized and interoperable. Standardization allows the platform to gather and store the growing influx of data that it can use as part of a digital identity strategy. Interoperability allows the platform to match different types of data, including physical data, with a person to verify their digital identity and avoid the creation of duplicate identities. In short, the platforms can make sense of increasingly large amounts of internal and external data and easily incorporate new data sources as they become available. Regulatory compliance and digital identity Navigating the regulatory landscape is a significant challenge for organizations dealing with digital identities. Compliance is not only necessary for legal reasons but also critical to maintaining customer trust and safeguarding institutional reputation. Organizations must stay informed about the regulatory frameworks that affect digital identity, such as the General Data Protection Regulation (GDPR) in the European Union, the California Consumer Privacy Act (CCPA), and other pertinent laws in jurisdictions they operate. These regulations dictate how personal data can be collected, stored, used and shared. Staying ahead of regulatory changes: Regulatory landscapes are dynamic, particularly concerning digital data. Organizations should engage with policymakers and participate in industry forums to stay ahead of changes. By proactively managing compliance, organizations can avoid costly penalties, operational disruptions and reputational damage. The consumer's perspective Some organizations are adopting a consumer-centric approach to digital identity that puts consumers' needs and desires first. These can broadly be broken into four categories: Security: While people want a seamless and personalized experience, security and privacy are listed as top concerns year after year.1 That might not be surprising given that data breaches continually make headlines and there are growing concerns over identity theft. Privacy: Security is related to privacy, but privacy means more than keeping consumers' information safe from hackers. Our April 2022 Global Insight Report found that 90 percent of consumers want some or complete control over how their personal data is used. 3 Recognition: People want to be continually recognized once they share and verify their identity, even if they move between devices or channels. And nearly 70 percent of consumers say it's important for businesses to recognize them across multiple visits.1 Inclusion: Consumers may have varying levels of access to technology, comfort with technology and access to physical identifiers. Creating digital identity solutions for these potential barriers can also increase financial inclusion. While these are all areas of focus, organizations also need to find the right fit for each person and interaction. For instance, consumers may expect and even appreciate a robust verification process when they're opening a new financial account. But they could quickly be turned off by a similar process if they're making a small purchase or trying to play a new online game. What to look for in a digital identity partner Digital identity solutions and services have grown increasingly sophisticated to meet today's challenges. Identity hubs and data orchestration engines can connect with multiple services to help create, resolve, verify and authenticate identities. By moving away from a siloed approach, businesses can offer customers a better experience while minimizing their risk throughout the customer journey. When comparing potential partners, look for a company that: Has a customer-first approach: If your business is customer-first, then you need a partner who has a similar view. Uses multidimensional data: The partner should be able to offer and use offline and digital data sources to resolve, verify and authenticate digital identities. Its capabilities may become increasingly important as new data sources emerge. Isn't afraid to innovate: Look into how the partner is testing and using the latest advancements, such as artificial intelligence, in its digital identity solutions. Protects your brand: Understand how the partner helps detect and prevent fraud while creating a seamless experience for your customers and protecting their data. The right partner can increase your bottom line, help you build trust and improve your brand's reputation. Learn more about Experian Identity, an integrated approach to digital identity that builds on Experian's decades of experience managing and securing identifying information. Learn more 1“2022 Global Identity and Fraud Report: Building digital consumer trust amidst rising fraud activity and concerns," Experian, June 2022 2“2021 Global Identity and Fraud Report: Protecting and enabling customer engagements in the new digital era," Experian, April 2021. https://www.experian.com/content/dam/marketing/na/global-da/pdfs/GIDFR_2022.pdf https://www.experian.co.th/wp-content/uploads/2021/04/Experian-Global-Identity-Fraud-Report-2021.pdf 3"Global Insights Report: April 2022," Experian, April 2022. https://www.experian.com/blogs/global-insights/wp-content/uploads/2022/04/WaveReportApril2022.pdf *This article includes content created by an AI language model and is intended to provide general information.

Are you looking for ways to make your financial institution more secure without adding unnecessary friction to the customer experience? Automated identity verification is an essential part of this process, safeguarding sensitive consumer information and helping to prevent fraud. This blog post will serve as the ultimate guide to automated identity verification so that you can understand why it's important and how it works. We'll cover all the details, like what automated ID verification is, how authentication software works with identifying documents, why automated identification technology is preferred over manual processes, and tips on implementing automation identity verification solutions into your business practices. What is automated identity verification? Automated identity verification is a secure, efficient process for verifying the identity of individuals or entities. This process is integral in various industries, especially the financial sector, to curb identity theft and fraudulent activities. It operates by using advanced analytics and authentication software that cross-references the provided data with a set of stored information. This technology eliminates manual ID verification, saving time and improving accuracy. ID verification automation uses artificial intelligence and machine learning to compare identifying credentials against various authenticating sources. Automated identity verification also comes into play for employment and income verification. Experian VerifyTM enables businesses through precise, real-time employment and income verification, ultimately helping businesses reduce risk, accelerate conversion and remove friction. For a more comprehensive understanding of automated identity verification, you can visit Experian's Identity Verification Solutions webpage, which provides a deep dive into the intricacies of identity verification, including insights on its importance in modern business operations and how it keeps your business secure. Benefits of automated identity verification for businesses and consumers Automated ID verification has revolutionized the way businesses conduct their operations and interact with customers. For businesses, AIV offers a range of benefits such as: Improved efficiency – businesses can automate the time-consuming process of identity verification, freeing up resources (staff) to focus on other critical tasks. Enhanced security – the technology ensures that customer data is secure and accurate, minimizing fraud risks and/or data breaches. Reduced costs – with the process being faster and more secure, costs are reduced as a byproduct. On the other hand, consumers enjoy a hassle-free experience as they can verify their identity within seconds, without physical documentation. This is essential for today’s consumers who expect frictionless experiences that keep them and their information safe. Data from Experian’s annual U.S. Identity and Fraud Report reflects these sentiments: 37% of consumers moved a new account opening process to another organization because of a poor experience; 95% of consumers say it's important to be repeatedly recognized online by businesses; and 60% of consumers are concerned about their online privacy. With automated identity verification, businesses can build trust, streamline their processes, and ultimately improve their bottom line. Furthermore, automated identity verification is a necessary component for businesses to minimize fraud risks in our evolving digital landscape. Living in an era where cybercrime is rampant, AIV safeguards businesses from potential fraudulent attempts and data breaches that could cause significant financial and reputational damage. From a compliance standpoint, automated identity verification ensures regulatory compliance, which is critical, considering the stringent regulations regarding customer data protection. Non-compliance can lead to severe legal repercussions and financial penalties. For financial institutions, Know Your Customer (KYC) policies must include Customer Identification Programs. Experian can help across the entire customer journey, from onboarding through portfolio management, while reducing risk of non-compliance and providing seamless authentication. Common challenges of automated identity verification As more companies turn to artificial intelligence and automation to deliver superior customer service experiences, the challenges businesses face have multiplied. One of the most common issues is ensuring identity proofing and accurate information protection within their networks. Although account takeover prevention has become more advanced, fraudsters still use increasingly sophisticated methods to circumvent it. As such, businesses must continuously develop new strategies to overcome these challenges, ensuring that their AI-powered solutions continue to provide reliable and secure user experiences. Types of identity verification solutions As the digital world continues to evolve, automated identity verification solutions have become a crucial part of online interactions. These solutions not only enhance security measures, but also provide faster and more efficient ways of identifying individuals. For instance, facial recognition is one example. Experian’s CrossCore® Doc Capture enables confident identity verification via facial recognition, which scans a person's face and compares it to their identification documents. Another type is voice recognition, which uses speech patterns to verify an identity. Additionally, document verification scans and validates various identification documents, such as driver's licenses and passports. It's essential to choose the most suitable AIV solution for your organization to ensure robust and reliable security measures. How to implement an automated ID verification solution It’s not new news that identity theft and fraud continue to be major concerns, particularly in an increasingly digital-only world. Implementing automated identity verification solutions to safeguard against such threats can seem daunting, particularly for businesses with limited IT resources. However, the benefits of automated ID verification, such as increased accuracy and efficiency, make it a worthwhile investment. When choosing a solution, consider factors such as the level of security provided, ease of implementation and integration with existing systems, and the ability to customize rules and settings. With careful planning and the right solution, , organizations can take a significant step towards improving their security posture and protecting their customers. Best Practices for automated identity verification Automated identity verification presents one way that financial institutions can increase automation. In doing so, organizations can improve accuracy, speed, and security in the verification process. One technique that has proven effective is the use of biometric technology, such as facial recognition and fingerprint scanning, to verify a person's identity. Additionally, utilizing various data sources, such as credit bureaus like Experian and government agencies, can increase the accuracy of verification. Implementing these best practices can not only save time and resources but also enhance customer experience by providing a seamless and secure verification process. In summary, automated identity verification is a vital tool for businesses and consumers to enhance their safety and security when engaging with customers. Automated identity verification streamlines customer processes across the lifecycle by eliminating manual checks and lengthy delays. As technology continues to evolve, it’s important for organizations to remain mindful that the methodologies used within automated identity verification will rapidly change as well. The key is to stay ahead. Automated identity verification solutions offer many advantages for businesses who want to maintain their trustworthiness while staying competitive in an ever-changing market. To learn more about Experian’s automated identity verification solutions, visit our website. Learn More *This article includes content created by an AI language model and is intended to provide general information.

While the principle of “trust but verify” might work for personal relationships, “verifying before trusting” is a more appropriate approach for businesses. According to Experian’s 2024 U.S. Identity and Fraud Report, consumers ranked identity theft as their top online security concern. As consumers conduct more activities online, the use of digital identity verification methods is becoming increasingly important. In this article, we explore how a streamlined initial verification process and continual authentication can help you build consumer trust and loyalty, as well as protect your business. What is identity verification? Online identity verification is the process of digitally confirming the identity of a user. Whether you’re reviewing an account application or approving an online transaction, you need to know that the person you’re dealing with is who they claim to be. Technology can help bring traditional identification verification methods online, such as checking a photo ID. Additionally, people and organizations have more digital “fingerprints” than ever before, which digital identity solutions can use to authenticate users with increased accuracy and less friction. What do online identity verification methods help solve? A well-designed and implemented online identity verification process can help address fraud, compliance and customer demands all at once. Verifying someone’s identity when they first create an account could be an important part of the know your customer (KYC) and customer identification program (CIP) requirements. From that moment on, continuous authentication can help detect and prevent fraud. Balancing the need for identity verification with a smooth online experience can be challenging. Customers may abandon a cart if identification requirements aren’t easy and fast, and may look for new services altogether if they’re repeatedly asked to authenticate themselves. But the challenge also presents an opportunity for companies that can leverage online identity verification services and methods to verify users’ identities accurately and discreetly. Examples of online identity verification methods There are multiple ways to verify someone’s identity, but some of the most popular online identity verification methods include: Personally identifiable information. Including their name, address, email address and phone number that can be checked against existing databases. Mobile network operator data. A service that verifies a person’s mobile phone identity. For instance, this can help verify the name, address, device details and other information associated with a phone number. Document verification. There are services that ask consumers to snap and upload a picture of the required document, like a driver’s license, passport, visa or national ID card. These may be verified with 2D or 3D facial recognition with liveness detection (e.g., verifying the user is human) or validating whether the document is real by verifying things like magnetic ink, the machine-readable zone and the barcode are genuine. One-time passwords. A one-time password is sent to a user’s phone or email during an application process to verify that they can access the account or device. Multifactor authentication. A service for existing users who can verify their identity with a combination of different factors, such as a password or biometrics (a method that measures unique physiological characteristics using fingerprints and face recognition). Knowledge-based association questions. These are questions that users answer to verify their identity. The questions may be based on their previous answers to “secret questions” or information from a credit bureau. Behavioral analysis. A service that verifies identity by comparing how a user interacts with a website or app to their previous behavior or an average user’s behavior. Environmental attributes, such as time and location, may also be considered. This technique requires no effort from the consumer. To keep up with increasing consumer and business demand, online identity verification processes may use artificial intelligence and machine learning techniques to complement the digital and manual processes. Some methods, such as consistency checks on a device and behavioral biometric assessments, can also help offer an “invisible” approach to verification. Even small behavioral traits, such as a user’s scrolling style or finger pressure, could be important data points. These invisible methods may be welcomed as a low-friction approach by consumers, who are increasingly aware of the lack of security that comes from only using passwords as an identity verification method. In Experian’s 2024 U.S. Identity and Fraud Report, 71 percent of consumers said physical biometrics are most important for a better online experience, followed by PIN codes sent to a mobile device (70 percent) and behavioral biometrics (66 percent). How Experian can help Experian is a global leader in identity verification and fraud detection services. We offer a layered approach that draws on different verification methods, including credit, device, non-traditional and user-provided data. Step-up authentication can add additional verification requirements based on how risky a user appears or the action they’re trying to take. The approach gives your trusted users a lower-friction experience while helping you detect multiple types of fraud and address CIP discrepancies. At the same time, your customers are assigned a unique and persistent identity, which can give you a single, consolidated view of your customers based on data from different platforms. Using these insights from identity resolution, you can deliver a personalized experience that surprises and delights. Learn more about Experian’s identity verification solutions and Experian VerifyTM. Learn more

Experian’s eighth annual identity and fraud report found that consumers continue to express concerns with online security, and while businesses are concerned with fraud, only half fully understand its impact – a problem we previously explored in last year’s global fraud report. In our latest report, we explore today’s evolving fraud landscape and influence on identity, the consumer experience, and business strategies. We surveyed more than 2,000 U.S. consumers and 200 U.S. businesses about their concerns, priorities, and investments for our 2023 Identity and Fraud Report. This year’s report dives into: Consumer concerns around identity theft, credit card fraud, online privacy, and scams such as phishing.Business allocation to fraud management solutions across industries.Consumer expectations for both security and their experience.The benefits of a layered solution that leverages identity resolution, identity management, multifactor authentication solutions, and more. To identify and treat each fraud type appropriately, you need a layered approach that keeps up with ever-changing fraud and applies the right friction at the right time using identity verification solutions, real-time fraud risk alerts, and enterprise orchestration. This method can reduce fraud risks and help provide a more streamlined, unified experience for your consumers. To learn more about our findings and how to implement an effective solution, download Experian’s 2023 Identity and Fraud Report. Download the report

What Is Identity Proofing? Identity proofing, authentication and management are becoming increasingly complex and essential aspects of running a successful enterprise. Organizations need to get identity right if they want to comply with regulatory requirements and combat fraud. It's also becoming table stakes for making your customers feel safe and recognized. 63 percent of consumers expect businesses to recognize them online, and 48 percent say they're more trusting of businesses when they demonstrate signs of security. Identify proofing is the process organizations use to collect, validate and verify information about someone. There are two goals — to confirm that the identity is real (i.e., it's not a synthetic identity) and to confirm that the person presenting the identity is its true owner. The identity proofing process also relates to and may overlap with other aspects of identity management. Identity proofing vs identity authentication Identity proofing generally takes place during the acquisition or origination stages of the customer lifecycle — before someone creates an account or signs up for a service. Identity authentication is the ongoing process of re-checking someone's identity or verifying that they have the authorization to make a request, such as when they're logging into an account or trying to make a large transaction. How does identity proofing work? Identity proofing typically involves three steps: resolution, validation, and verification. Resolution: The goal of the first step is to accurately identify the single, unique individual that the identity represents. Resolution is relatively easy when detailed identity information is provided. In the real world, collecting detailed data conflicts with the need to provide a good customer experience. Resolution still has to occur, but organizations have to resolve identities with the minimum amount of information. Validation: The validation step involves verifying that the person's information and documentation are legitimate, accurate and up to date. It potentially involves requesting additional evidence based on the level of assurance you need. Verification: The final step confirms that the claimed identity actually belongs to the person submitting the information. It may involve comparing physical documents or biometric data and liveness tests, such as a comparison of the driver's license to a selfie that the person uploads. Different levels of identity proofing may require various combinations of these steps, with higher-risk scenarios calling for additional checks such as biometric or address verification. Service providers can implement a range of methods based on their specific needs, including document verification, database validation, or knowledge-based authentication. Building an effective identity proofing strategy By requiring identity proofing before account opening, organizations can help detect and deter identity fraud and other crimes. You can use different online identity verification methods to implement an effective digital identity proofing and management system. These may include: Document verification plus biometric data: The consumer uploads a copy of an identification document, such as a driver's license, and takes a selfie or records a live video of their face. Database validations: The proofing solution verifies the shared identifying information, such as a name, date of birth, address and Social Security number against trusted databases, including credit bureau and government agency data. Knowledge-based authentication (KBA): The consumer answers knowledge-based questions, such as account information, to confirm their identity. It can be a helpful additional step, but they offer a low level of assurance, partially because data breaches have exposed many people's personal information. In part, the processes you'll use may depend on business policies, associated risks and industry regulations, such as know your customer (KYC) and anti-money laundering (AML) requirements. But organizations also have to balance security and ease of use. Each additional check or requirement you add to the identity proofing flow can help detect and prevent fraud, but the added friction they bring to your onboarding process can also leave customers frustrated — and even lead to customers abandoning the process altogether. Finding the right amount of friction can require a layered, risk-based approach. And running different checks during identity proofing can help you gauge the risk involved. For example, comparing information about a device, such as its location and IP address, to the information on an application. Or sending a one-time password (OTP) to a mobile device and checking whether the phone number is registered to the applicant's name. With the proper systems in place, you can use high-risk signals to dynamically adjust the proofing flow and require additional identity documents and checks. At the same time, if you already have a high level of assurance about the person's identity, you can allow them to quickly move through a low-friction flow. Experian goes beyond identity proofing Experian builds on its decades of experience with identity management and access to multidimensional data sources to help organizations onboard, authenticate and manage customer identities. Our identity proofing solutions are compliant with National Institute of Standards and Technology (NIST) and enable agencies to confidently verify user identities prior to or during account opening, biometric enrollment or while signing up for services. Learn more This article includes content created by an AI language model and is intended to provide general information.

Kathleen Peters, Chief Innovation Officer, Decision Analytics for Experian, was recently featured on the Eliances Heroes podcast as part of the new weekly segment, the “Experian Identity Report.” In the introductory show, podcast host David Cogan, spoke with Kathleen about why identity is so important to our society. Listen to the podcast for the full discussion and see the transcript below. Learn more about Experian Identity David Cogan: How critical is it? Well, I’ll tell you. Payment fraud will exceed $206 billion in the next five years and let’s face it. Managing one’s personal identity is very complicated on its own and if the business enterprise managing customer identities in a strategic and secure way and scale across countless interaction is extremely complicated. And it’s only going to get more complex with the future from what I understand and all the technology that’s coming out if not by the day, by the hour. And that’s why we’re bringing this to you. Interviews with the world’s leading experts on the game changing impact of identity and the need to use reliable data to make confident decisions that securely accelerate customer engagement and that’s why we’re honored here today to have with us Kathleen Peters, Chief Innovation Officer, Experian Decision Analytics North America. Kathleen Peters: Thanks so much David, it’s great to be here with you. DC: $206 billion of payment fraud in the next five years? I mean who’s going to want to turn on their computer after this. That is a serious number. What do we do? KP: It’s really important that we get our arms around this both as consumers as well as businesses because we want to engage online. So much of what we’re doing is digital. It especially started in COVID when we were having our groceries delivered and everything else and even our grandparents are having to do their banking transactions online. The world is changing, and fraudsters take notice of that as well. Fraudsters are opportunistic and when they see a bunch of folks doing stuff online that they’ve never done before, they’re seeing that as an opportunity too. DC: You know the days of people horseback riding and overtaking trains are long gone and now it’s all digital. KP: It’s a lot easier these days. DC: Why is identity so important to our daily digital lives and in business? KP: It’s a great question, David. And as a consumer myself, you, and I when we transact online whether that’s to have food delivered, or I’m buying something for my kids or I’m even paying a bill, I want to be able to trust that my information will be safe, that my privacy will be protected and that my experience will be as smooth as possible. I think that’s what we all want. So as consumers and as businesses, how do we enable all the opportunities this new digital world is presenting to us in a way that we are safe and also businesses can transact with us securely and have confidence on who’s engaging with them online. DC: Let’s talk about identity. What really makes identity so challenging to manage at a business enterprise level especially with how complex the business portion is? KP: Absolutely. It really comes down to there are so many elements that comprise our identity. It’s multidimensional. So historically, when we think about identity, we probably think about the things that were on our DL or passport the kind of information that’s pretty static – name, address, SSN, date of birth – those kinds of things. Once we get online, that identity becomes a little more challenging. We’re not necessarily physically in front of the business that we’re engaging with so the business needs to determine if the person is who we say we are. There’s a famous Far Side comic from years ago where a dog is sitting in front of the computer and he says “On the internet, no one knows you’re a dog.” And that still rings true in that you need to be able to ensure that the customer that’s coming to your business online is a real person and not a bot, is a person with good intent and not a fraudster. You need to look no farther than some of the recent controversies around Twitter and Elon Musk’s on-again, off-again, on-again intent to buy the company. A few months ago he had pulled back because he wanted to know definitively how many users on Twitter are humans versus bots and sometimes determining that can be really hard. And that comes down to managing all these new definitions of identity. DC: That’s very important. The thing is businesses and consumers want to know really what to be able to do. So, what kinds of things is Experian able to offer to help with all of that? KP: We’re in a great position as Experian because we have such a depth and breadth of identity data. We have the analytics horsepower and really touchpoints that are really unique when it comes to thinking about identity. So we’ve been talking about these traditional identity elements and digital, online identity. When you think about it, Experian also really understands your financial identity. So when you bring those things together and a consumer is looking to maybe understand what their financial identity means, their credit score or even how to improve their credit score, Experian’s there. We’ve got a robust direct to consumer business, we’ve got offerings like Boost and Go that help people establish and build their credit. We’ve got marketplaces for cards, insurance, etc. And then when consumers want to open a new account at a financial institution, or a fintech, or a retailer, or even maybe buy some crypto or log into a business, Experian can bring that wealth of capability to help our clients, help businesses, separate those good consumers with good intent from the fraudsters and do that very quickly and efficiently so that consumers can have a great experience and build that trust with who they’re engaging with. DC: Kathleen, that’s really amazing. Alright, now with all of that going on, what is Experian doing now with innovating for the identity space? KP: This is a real passion of mine David and this is where I spend a lot of my time. We’re always looking ahead to see what is the new data, new capabilities that can help us improve that consumer experience and engagement, help clients find the right consumers online to engage and target, and really allow our clients to grow their businesses safely. So, we’re building some products in house, where we’re connecting new pieces that might be new to Experian like linking some of that traditional identity data with particular payment instruments. Is this Kathleen’s credit card? Is this my bank account? When I come and try to do transactions online. But we’re also partnering with new companies. There are a number of startups that are being formed that have been in business looking at new ways to stop fraud and new ways to help identify and authenticate users online. So, as we innovate, we’re building some things in house, we’re partnering, we’re investing in young companies, and sometimes we’re even acquiring. So, bringing together that breadth of data, analytics, really trying to think about what will be the next way that we’ll think about identifying ourselves online is some of the ways we’re innovating. DC: Well, we’re very fortunate to have you and your company here to be able to do that because it’s growing by leaps and bounds. I’m amazed by the number $206 billion which is probably going to go higher, so we’re very fortunate that Experian is around and really identifying this issue and trying to do something now. What do you think our audience will learn about these weekly, critical chats about identity with Experian experts? KP: These are going to be great conversations that we’re going to be able to share and talk about how rapidly things are changing and evolving and how this really relates to our daily lives and the things that are going on in this very dynamic economic climate, digital climate, the way things are changing the way we’re engaging. I think people are also going to learn a lot about Experian’s mission around financial inclusion and opportunity creation. We’re a very mission driven company and we’re the consumer’s bureau, so we want to do this journey in partnership with consumers so that you can take an active part in protecting yourself, understanding what’s going on, helping us fight fraud, but also just really be able to take advantage of all of these new opportunities in a safe way.