Tag: synthetic identity

Experian is excited to have been chosen as one of the first data and analytics companies that will enable access to Social Security Administration (SSA) data for the purposes of verifying identity against the Federal Agency’s records. The agency’s involvement in the wake of Congressional interest and successful legislation will create a seismic shift in the landscape of identity verification. Ultimately, the ability to leverage SSA data will reduce the impact of identity fraud and synthetic identity and put real dollars back into the pockets of people and businesses that absorb the costs of fraud today. As this era of government and private sector collaboration begins, many of our clients and partners are breathing a sigh of relief. We see this in a common question our customers ask every day, “Do I still need an analytical solution for synthetic ID now that eCBSV is on the horizon?” The common assumption is that help is on the way and this long tempest of rising losses and identity uncertainty is about to leave us. Or is it? We don’t believe it’s the end of the synthetic ID storm. This is the eye. Rather than basking in the calm light of this moment, we should be thinking ahead and assessing our vulnerabilities because the second half of this storm will be worse than the first. Consider this: The people who develop and exploit synthetic IDs are playing a long game. It takes time, research, planning and careful execution to create an identity that facilitates fraud. The bigger the investment, the bigger the spoils will be. Synthetic ID are being used to purchase luxury automobiles. They’re passing lender marketing criteria and being offered credit. The criminals have made their investment, and it’s unlikely they will walk away from it. So, what does SSA’s pending involvement mean to them? How will they prepare? These aren’t hard questions. They’ll do what you would do in the eye of a storm — maximize the value of the preparations that are in place. Gather what you can quickly and brace yourself for the uncertainty that’s coming. In short, there’s a rush to monetize synthetic IDs on the horizon, and this is no time to declare ourselves safe. It’s doubtful that the eCBSV process will be the silver bullet that ends synthetic ID fraud — and certainly not on day one. It’s more likely that the physical demands of the data exchange, volume constraints, response times and the actionability of the results will take time to optimize. In the meantime, the criminals aren’t going to sit by and watch as their schemes unravel and lose value. We should take some comfort that we’ve made it through the first half of the storm, but recognize and prepare for what still needs to be faced.

Experian has been named one of the 10 participants, and only credit bureau, in the initial rollout of the SSA's new eCBSV service.

Synthetic identities come from accounts held not by actual individuals, but by fabricated identities created to perpetrate fraud. It often starts with stealing a child’s Social Security number (SSN) and then blending fictitious and factual data, such as a name, a mailing address and a telephone number. What’s interesting is the increase in consumer awareness about synthetic identities. Previously, synthetic identity was a lender concern, often showing itself in delinquent accounts since the individual was fabricated. Consumers are becoming aware of synthetic ID fraud because of who the victims are — children. Based on findings from a recent Experian survey, the average age of child victims is only 12 years old. Children are attractive victims since fraud that uses their personal identifying information can go for years before being detected. I recently was interviewed by Forbes about the increase of synthetic identities being used to open auto loans and how your child’s SSN could be used to get a phony auto loan. The article provides a good overview of this growing concern for parents and lenders. A recent Javelin study found that more than 1 million children were victims of fraud. Most upsetting is that children are often betrayed by people close to them -- while only 7 percent of adults are victimized by someone they know, 60 percent of victims under 18 know the fraudster. Unfortunately, when families are in a tight spot financially they often resort to using their child’s SSN to create a clean credit record. Fraud is an issue we all must deal with — lenders, consumers and even minors — and the best course of action is to protect ourselves and our organizations.

Although it’s hard to imagine, some synthetic identities are being used for purposes other than fraud. Here are 3 types of common synthetic identities and why they’re created: Bad — To circumvent lag times and delays in establishing a legitimate identity and data footprint. Worse — To “repair” credit, hoping to start again with a higher credit rating under a new, assumed identity. Worst — To commit fraud by opening various accounts with no intention of paying those debts or service fees. While all these synthetic identity types are detrimental to the ecosystem shared by consumers, institutions and service providers, they should be separated by type — guiding appropriate treatment. Learn more in our new white paper produced with Whitepages Pro, Fighting synthetic identity theft: getting beyond Social Security numbers. Download now>

Experian on the State of Identity podcast In today’s environment, any conversation on the identity management industry needs to include some mention of synthetic identity risk. The fact is, it’s top of mind for almost everyone. Institutions are trying to scope their risk level and identify losses, while service providers are innovating ways to solve the problem. Even consumers are starting to understand the term, albeit via a local newscast designed to scare the heck out of them. With all this in mind, I was very happy to be invited to speak with Cameron D’Ambrosi at One World Identity (OWI) on the State of Identity podcast, focusing on synthetic identity fraud. Our discussion focused on some of the unique findings and recommended best practices highlighted in our recently published white paper on the subject, Synthetic identities: getting real with customers. Additionally, we discussed how a lack of agreement on the definition and size of the synthetic identity problem further complicates the issue. This all stems from inconsistent loss reporting, a lack of confirmable victims and an absence of an exact definition of a synthetic identity to begin with. Discussions must continue to better align us all. I certainly appreciate that OWI dedicated the podcast to this subject. And I hope listeners take away a few helpful points that can assist them in their organization’s efforts to better identify synthetic identities, reduce financial losses and minimize reputation risks.

Sophisticated criminals work hard to create convincing, verifiable personas they can use to commit fraud. Here are the 3 main ways fraudsters manufacture synthetic IDs: Credit applications and inquiries that build a synthetic credit profile over time. Exploitation of authorized user processes to take over or piggyback on legitimate profiles. Data furnishing schemes to falsify regular credit reporting agency updates. Fraudsters are highly motivated to innovate their approaches rapidly. You need to implement a solution that addresses the continuing rise of synthetic IDs from multiple engagement points. Learn more

The data to create synthetic identities is available. And the marketplace to exchange and monetize that data is expanding rapidly. The fact that hundreds of millions of names, addresses, dates of birth, and Social Security numbers (SSNs) have been breached in the last year alone, provides an easy path for criminals to surgically target new combinations of data. Armed with an understanding of the actual associations of these personally identifiable information (PII) elements, fraudsters can better navigate the path to perpetrate identity theft, identity manipulation, or synthetic identity fraud schemes on a grand scale. Using information such as birth dates and addresses in combination with Social Security numbers, criminals can target new combinations of data to yield better results with lower risk of detection. Some examples of this would be: identity theft, existing account takeovers, or the deconstruction and reconstruction of those PII elements to better create effective synthetic identities. Experian has continued to evolve and innovate against fraud risks and attacks with an understanding of attack rates, vectors, and the shifting landscape in data availability and security. In doing so, we’ve historically operated under the assumption that all PII is already compromised in some way or is easily done so. Because of this, we employ a layered approach, providing a more holistic view of an identity and the devices that are used over time by that identity. Relying solely on PII to validate and verify an identity is simply unwise and ineffective in this era of data compromise. We strive to continuously cultivate the broadest and most in-depth set of traditional, innovative and alternative data assets available. To do this, we must enable the integration of diverse identity attributes and intelligence to balance risk, while maintaining a positive customer experience. It’s been quite some time since the use of basic PII verification alone has been predictive of identity risk or confidence. Instead, validation and verification is founded in the ongoing definition and association of identities, the devices commonly used by those individuals, and the historical trends in their behavior. Download our newest White Paper, Synthetic Identities: Getting real with customers, for an in-depth Experian perspective on this increasingly significant fraud risk.

Synthetic identity fraud is on the rise across financial services, ecommerce, public sector, health and utilities markets. The long-term impact of synthetic identity remains to be seen and will hinge largely upon forthcoming efforts across the identity ecosystem made up of service providers, institutions and agencies, data aggregators and consumers themselves. Making measurement more challenging is the fact that much of the assumed and confirmed losses are associated with credit risk and charge offs, and lack of common and consistent definitions and confirmation criteria. Here are some estimates on the scope of the problem: Losses due to synthetic identity fraud are projected to reach more than $800 million in 2017.* Average loss per account is more than $10,000.* U.S. synthetic credit card fraud is estimated to reach $1.257 billion in 2020.* As with most fraud, there is no miracle cure. But there are best practices, and topping that list is addressing both front- and back-end controls within your organization. Synthetic identity fraud webinar> *Aite Research Group

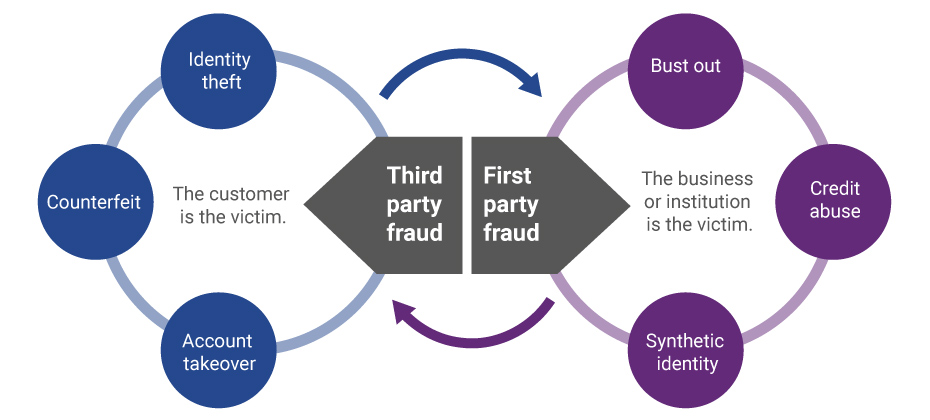

Evolution of first-party fraud to third Third-party and first-party schemes are now interchangeable, and traditional fraud detection practices are less effective in fighting these evolving fraud types. Fighting this shifting problem is a challenge, but it isn’t impossible. To start, incorporate new and more robust data into your identity verification program and provide consistent fraud classification and tagging. Learn more>

Mitigating synthetic identities Synthetic identity fraud is an epidemic that does more than negatively affect portfolio performance. It can hurt your reputation as a trusted organization. Here is our suggested 4-pronged approach that will help you mitigate this type of fraud: Identify how much you could lose or are losing today to synthetic fraud. Review and analyze your identity screening operational processes and procedures. Incorporate data, analytics and cutting-edge tools to enable fraud detection through consumer authentication. Analyze your portfolio data quality as reported to credit reporting agencies. Reduce synthetic identity fraud losses through a multi-layer methodology design that combats both the rise in synthetic identity creation and use in fraud schemes. Mitigating synthetic identity fraud>

The creation of synthetic identities (synthetic id) relies upon an ecosystem of institutions, data aggregators, credit reporting agencies and consumers. All of which are exploited by an online and mobile-driven market, along with an increase in data breaches and dark web sharing. It’s a real and growing problem that’s impacting all markets. With significant focus on new customer acquisition and particular attention being paid to underbanked, emerging, and new-to-country consumers, this poses a large threat to your onboarding and customer management policies, in addition to overall profitability. Synthetic identity fraud is an epidemic that does more than negatively affect portfolio performance. It can hurt your reputation as a trusted organization and expose institutions, like yours, as paths of lesser resistance for fraudsters to use in the creation and farming of synthetic identities. Here is a suggested four-pronged approach to mitigate this type of fraud: The first step is knowing your risk exposure to synthetic identity fraud. Identify how much you could lose or are losing today using a targeted segmentation analysis to examine portfolios or customer populations. Next, review your front- and back-end identity screening operational processes and procedures and analyze that information to ensure you have industry best practices, procedures and verification tools deployed. Then incorporate data, analytics and some of the industry’s cutting edge tools. This enables you to perform targeted consumer authentication and identify opportunities to better capture the majority of fraud and operational waste. Lastly, ensure your organization is part of the solution – not the problem. Analyze your portfolio data quality as reported to credit reporting agencies and then minimize your exposure to negative compliance audit results and reputational risk. Our fraud and identity management consultants can help you reduce synthetic identity fraud losses through a multilayer methodology design that combats the rise in synthetic identity creation and use in fraud schemes.