Financial Access

Experian is unlocking the power of data to facilitate access to fair and affordable credit for both consumers and businesses. With our products, services and partnerships, we are working to improve financial inclusion for all. Read about our latest financial access news below:

Early in my career, I gained a lot of knowledge about credit. But when I moved to the United States from Brazil, establishing credit was a challenge. I worked part-time in a credit card company call center during college. I come from a humble family, and through helping customers, I learned the ins and outs about credit and money management. But all the solid credit history I built up in my home country didn’t transfer to the U.S. When I immigrated, I had to pay upfront for everything from utilities to a cellphone and it made me feel at a disadvantage. Thanks to Experian Boost®i, our feature that allows you to build credit without debt, and responsible management of debt, my FICO® Scoreii quickly rose to reflect my true creditworthiness. But I’ll never forget how it felt to be invisible when it came to the credit system. Being seen is the first step to equitable access to financial tools. Now that Experian conveniently offers Experian credit reports in Spanish onlineiii, consumers who prefer to access information in Spanish will be able to directly comprehend their credit profile so they can feel empowered. Understanding your credit report is a critical component for your ability to make informed decisions about your finances. As the executive sponsor of our Juntos Employee Resource Group (ERG) and someone who was new to credit in the U.S., I know first-hand that being seen is the first step in a journey towards financial wellness. To help you be informed, Experian also has a Spanish-language credit e-book and articles at the Ask Experian blog. Learn more about my financial health journey and my colleague's through #ExperianStories. i Results will vary. Not all payments are boost-eligible. Some users may not receive an improved score or approval odds. Not all lenders use Experian credit files, and not all lenders use scores impacted by Experian Boost®. Learn more. ii Credit score calculated based on FICO® Score 8 model. Your lender or insurer may use a different FICO® Score than FICO® Score 8, or another type of credit score altogether. Learn more. iii Only Experian credit reports are available in Spanish. All other services associated with an Experian membership are available in English only. English fluency is required for full access to Experian’s products.

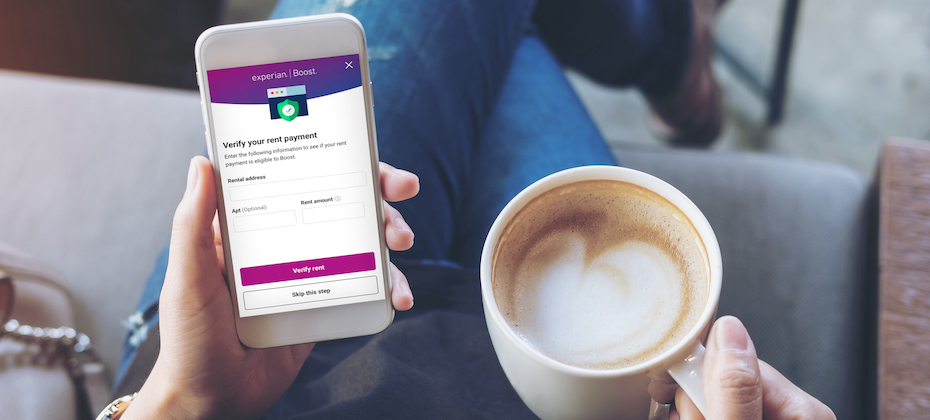

You may have recently read that Experian®, alongside the other two credit bureaus, permanently extended free weekly access to consumer credit reports through AnnualCreditReport.com. While I believe the move helps consumers more regularly review their credit reports, it only begins to scratch the surface of how we empower consumers to take control of their financial lives. People come to Experian looking for ways to improve their financial health. We have direct relationships with millions of consumers and listen to their wants and needs. That’s why we’ve transformed ourselves into the one stop shop for our members to address many facets of their financial journey. Whether it’s accessing credit education materials, monitoring their credit files, finding ways to save money or improving their credit history, consumers can come to Experian to find the tools and resources they need. Building creditFor instance, in 2019, we launched Experian Boost® --a first-of-its-kind feature that allows consumers to contribute positive payment information for eligible bills including utilities, telecom and even video streaming services, directly into their Experian credit file. Consumers can now also add positive residential rent payments through Experian Boost®1. More recently, we debuted Experian Go™—another first-of-its-kind feature designed to help “credit invisibles,” or people with no credit history, begin building credit. Credit invisibles who utilize the feature together with Experian Boost can establish an authenticated Experian credit report, tradelines and a credit history and, as a result, get access to financial offers. Staying on top of your informationBeyond our credit building offerings, we’ve long provided consumers the opportunity to access their Experian credit report and FICO® Score2, free-of-charge. By providing consumers access to their credit report and FICO® Score, we’re enabling them to better understand how they may look to lenders, identify potential fraud, determine the specific factors that are affecting their credit and how to improve it. In addition, our credit and dark web monitoring services help consumers detect whether their personal information is potentially available to fraudsters and protect against identity theft. Putting money back into your walletWe also recognize the value of saving money. As part of an Experian membership, we offer resources that can potentially help consumers save on the cost of their auto insurance and find the best credit card for their financial needs. We empower consumers to: Compare auto insurance policies. Consumers can comparison shop to potentially find a better rate on their current policy and save. The free Experian service delivers multiple, tailored rates from up to 40 leading and well-established auto insurance carriers, allowing consumers to quickly find and purchase an auto insurance coverage plan that meets their needs. Find the right credit card. Our free Marketplace makes it easy for consumers to compare different credit card options. We match consumers’ financial information against lender’s requirements to match them with the tailored offers. Every consumer deserves the opportunity to live their best financial life. Providing free resources to help consumers effectively navigate their financial journey is the best way to help them realize financial independence. While I’m proud of how we’ve helped consumers thus far, we will continue to innovate and offer consumers the tools to improve their financial wellbeing. [1] Results will vary. Not all payments are boost-eligible. Some users may not receive an improved score or approval odds. Not all lenders use Experian credit files, and not all lenders use scores impacted by Experian Boost®. Learn more. [2] Credit score calculated based on FICO® Score 8 model. Your lender or insurer may use a different FICO® Score than FICO® Score 8, or another type of credit score altogether. Learn more. [3] Results may vary and some may not see savings.

Our latest State of the Automotive Finance Report: Q1 2023 showed the average new vehicle loan amount reached $40,851, and today’s average used vehicle loan amount is $26,420. While the growth of average loan amounts is slowing, and in some cases, decreasing from previous years, rising interest rates are pushing monthly payments higher for many consumers. This news comes at a time when many consumers are looking for ways to save money and are holding onto their vehicles longer. In fact, as of Q1 2023, the average length of ownership for new vehicles purchased as far back as 2010 is 4.19 years. At the same time, the cost of vehicle repairs has many consumers feeling financially stressed. Whether to eliminate the burden of rising costs of goods and services, or to plan for big ticket items like vehicle purchases or repairs, our research shows saving money is top of mind for many consumers. Two-thirds tell us they are actively looking for ways to trim expenses from their monthly budget. If you’re shopping for a new set of wheels, or trying to keep your old ones on the road longer, here are four steps you can take to save money: Use credit as a financial tool A good credit score could help you qualify for better interest rates and better terms for loans. Whether you’re looking to purchase a new vehicle or finance repairs, a positive credit history can be a powerful financial tool. Your credit score can also impact the rates you may pay for insurance. Work to keep your credit card balances low and make your payments on time. Using tools like Experian Boost[1] allows you to add your positive payments for telecom and utility bills as well as video streaming services - and now rent payments – to your Experian credit file to potentially increase your FICO®[2] Score instantly. Cut costs where you can We are committed to helping consumers save money in multiple ways and auto insurance is one area consumers may be overpaying. To combat this, we now offer an auto insurance shopping service that delivers tailored rates based on your current policy and vehicle directly from our mobile app. Consumers can potentially save on average more than $900 per year through our service, which is significant. Plan ahead to save on interest rates Interest rates are a key consideration if you’re shopping for a new or used vehicle. Our latest State of the Automotive Finance Market Report showed the average interest rate for a new vehicle is 6.58%. Oftentimes when shopping for a vehicle the main priority is securing a low monthly payment, but it’s also important to assess the total cost of the loan, particularly amid rising interest rates and vehicle prices. With this in mind, some new vehicle shoppers who were in search of lower interest rates opted for shorter loan terms in Q1 2023. Determine how much you can afford to spend each month and opt for shorter loan terms to save on interest. Don’t get a lemon With prices increasing, we know many people are opting for used vehicles. While this can help with costs, it’s important to know what you’re buying before you sign on the dotted line. Request a vehicle history report, like an Experian AutoCheck report, before committing to the purchase. These reports include how many previous owners the vehicle had, or if there were any reported accidents. This can help you avoid surprises down the road and give you a better idea of the value of the car. In addition to a vehicle history report, we recommend having the vehicle inspected by a licensed mechanic. We rely on our vehicles every day. By leveraging the right tools, and with proper planning, you may view them less as a financial burden and more as a means to enjoy the freedom of the open road. [1] [Results will vary. Not all payments are boost-eligible. Some users may not receive an improved score or approval odds. Not all lenders use Experian credit files, and not all lenders use scores impacted by Experian Boost. Learn more. [2] FICO is a registered trademark of Fair Isaac Corporation

Understanding how credit works is key to protecting your financial health in any environment – and this is especially true today. What’s new: To see how America’s youngest consumers are faring, we recently deployed a national survey looking at: Gen Z and millennial’s understanding of credit and personal financeHow recent economic news is impacting their financial health What would make them feel more optimistic about their situation Why it matters: As we look ahead, millennials and Gen Z consumers will be the biggest drivers of spending and our economy. Ensuring they have access to trusted financial education and resources is key. Survey highlights include: Building a strong credit history is key to unlocking many things we want in life, yet many younger people do not understand its importance until they get older. The bottom line: Our research revealed many Gen Z and millennial consumers are simply unsure how to successfully build credit and are hungry for trusted resources of personal finance information. “We believe in financial power for all and ensuring America’s youngest consumers are empowered to be financially independent adults is key to achieving this,” said Christina Roman, consumer education advocate at Experian. “Personal finance and credit education are central to our mission. We are committed to being a trusted resource for consumers looking to improve their financial health during our current economic environment and beyond.” How Experian Can HelpThere are free and easy steps consumers can take to help improve their financial health with Experian, including: Getting a free copy of your Experian credit report and FICO[1] Score®[2] at www.experian.com or via Experian’s mobile app. Our app also has free personal finance and credit building tools Add positive telecom, utility, video streaming service and qualifying rent payments to your Experian credit report through Experian Boost[3] for an opportunity to improve your credit scores by visiting www.experian.com/boost. Young consumers without an established credit history can download Experian’s mobile app and enroll in a free Experian membership to establish, use and grow credit responsibly with Experian Go™ Joining Experian’s #CreditChat hosted by @Experian on Twitter with financial experts every Wednesday at 3 p.m. Eastern timeVisiting the Ask Experian blog for answers to common questions, advice and education about creditLearn how to build and protect your credit with Experian’s Credit Essentials for Everyone flipbook and find additional credit education resources at resources at http://www.experian.com/consumereducation. Find additional money-saving resources from Experian by visiting experian.com/savings Survey MethodologyExperian commissioned Atomik Research to conduct an online survey of 2,008 adults between the ages of 18-42 years old throughout the United States, with even distribution between Generation Z (N=1,005) and millennials (N=1,003) participants. The margin of error is +/- 2 percentage points with a confidence level of 95 percent. Fieldwork took place between March 31, 2023, and April 4, 2023. Atomik Research is an independent, creative market research agency. [1] FICO is a registered trademark of Fair Isaac Corporation [2] Credit score calculated based on FICO Score 8 model. Your lender or insurer may use a different FICO® Score than FICO® Score 8, or another type of credit score altogether. Learn more. [3] Results will vary. Not all payments are boost-eligible. Some users may not receive an improved score or approval odds. Not all lenders use Experian credit files, and not all lenders use scores impacted by Experian Boost. Learn more.

I don’t know about you, but the importance of a good credit score wasn’t something talked about around my family’s dining room table growing up. I knew the value of a dollar and the importance of saving and budgeting, but I didn’t realize how many things I’d want in life would depend on having an established credit history. It wasn’t until I went buy my first car that I realized just how important credit can be. I had been using credit, but I wasn’t using it as a tool that could work for me. In fact, in this instance, my credit score was working against me. Thankfully, my boyfriend at the time (and now husband), co-signed on my auto loan so I could get a better interest rate. This experience served as the wakeup call I needed to prioritize improving my credit and overall financial health. I know my story is similar to many others. In fact, our recent research shows 77% of millennials and Gen Z consumers are striving to be more financially literate and nearly 80% are actively trying to increase their credit scores. Just as I was, these consumers are hungry for knowledge and 69% are actively seeking trusted resources for personal finance information. I’m thankful to work for a company that puts consumers at the heart of everything we do. Education is central to our mission and my job is to educate consumers about the tools and resources we have available to help bring financial to all. Talk about coming full circle! So, if you’re looking for ways to improve your financial health, here are a few quick tips: Get engaged: Many people think checking their credit report will hurt their credit scores, but this is not true. This is one of the most common myths about credit reports. You can, and should, check your credit report regularly. This is one of the best ways to understand where you stand from a credit perspective. You can get a free Experian credit report and FICO® Score once a month through our mobile app. You can also get a free credit report from each of the three credit reporting agencies by visiting AnnualCreditReport.com. Usethe tools available to you: There are a lot of helpful tools availabletoday that weren’t even just a few years ago, including Experian Boostand Experian Go. Experian Go makes it easyfor people with a limited or nonexistent credit history to establish, use andgrow credit responsibly. And with Experian Boost, you can self-report your cellphone, utility, telecom, and video streaming service payments directly to yourExperian credit report for an opportunity to instantly improve your creditscore. Seektrusted resources: In this age of information overload andsocial media, it can be hard to find trusted sources of personal finance information,but we’re here to help. You can find answers to common questions by joining ourweekly #CreditChats onTwitter or by visiting our Ask Experian blog.We also have free resources available at www.experian.com/consumerseducation. Avoidmaking mistakes with lasting financial impact: I know, I know. This canbe easier said than done, but it’s an important consideration to protect yourfinancial health. There are many times in life where it’s OK to learn by makingmistakes, but credit and personal finance are not a time you want to do that ifyou can avoid it. If you’re using credit, make sure you have a plan for payingthe debt you owe. Credit can be a financial tool, but debt is a financialproblem. Make sure you understand your needs vs. your wants and try to keep yourbalances as low as possible. As the saying goes, knowledge truly is power. I know this to be true from experience and our research shows a better understanding of personal finance would make 75% of Gen Z and millennials feel more optimistic about their situation. This is good news as there are many easy steps consumers can take today to feel more educated and empowered. Getting engaged with your credit report and finding the right tools and resources are some of the best ways to protect your financial health in our current environment and beyond.

Experian research shows more than a quarter of Black and Hispanic consumers are invisible to the credit market, compared to 16% of Asian and White consumers. This is a significant gap that all of us can improve. At our North American headquarters, a group of young scholars took the lead on finding solutions. Four teams representing Historically Black Colleges and Universities (HBCUs) visited our campus and shared their creativity and personal stories with us in the finale of the inaugural #IYKYK Hackathon. The Hackathon was the culmination of a six-month Center for Financial Advancement® Credit Academy, created in partnership with HomeFree-USA. Through live sessions with Experian credit education experts and self-paced content, more than 250 scholars from 14 HBCUs learned about credit, financial tools, and how to build generational wealth through steps like homeownership. The teams from Alabama State University, Fisk University, Morgan State University and Shaw University made it to the finals and presented their ideas for the next best credit education program for their peers. Left to right, top to bottom: Fisk University, Morgan State University, Shaw University and Alabama State University In addition to their presentations, what was also impressive was the inclusivity in participation. Just at the finals alone, these student leaders represented six countries, eight different languages, the LGBTQ+ community, different faiths, and more. The “Credit Stingers” from Alabama State University took home the prize, a $40,000 scholarship for their idea of a gamified app called “Credit Rush.” In order to overcome obstacles, students watch a video or take a quiz about credit in order to advance to higher levels. Other features of “Credit Rush” include the “Hive,” a library of credit education materials, chat, daily calendar functions and more. The “Credit Stingers” from Alabama State University took home the prize, a $40,000 scholarship for their idea of a gamified app called “Credit Rush.” Many of the student leaders are already putting what they’ve learned into practice. They shared how they’ve been able to rent their own apartments for the first time, help their recently immigrated family members establish their credit identities, and make decisions that will help them eventually buy a home. They showed immense passion. They are committed to being knowledge ambassadors, sharing information about credit with their classmates, families and friends, making their communities the true winners of this program.

I recently came across a quote that said, “The world you see is created by what you focus on.” As I look back on my last 16 years with Experian, I see a lot of truth in this. While Experian has historically been recognized as a business-to-business organization, over the last several years, we’ve had a transformational shift in focus that’s fundamentally changed our business. This shift has made our world look a lot different than it used to. Today, consumers are at the center of everything we do. They’re the driving force behind our innovation and growth. Every day, millions of consumers come to Experian looking for ways to improve their financial health and we’ve been building one of the largest global member bases. These direct relationships put us in a unique position. We can listen to consumers to hone our focus – and we do. Just like in everyday relationships, listening builds trust and respect. It helps us understand what consumers want and allows us to innovate to meet them where they are on their financial journey. In 2019, we heard consumers’ call for more control of their data and responded with Experian Boost®[1]– a first-of-its-kind feature that allows consumers to contribute information directly to their Experian credit file. To date, we’ve helped 8.6 million consumers instantly improve their FICO® Scores[2] with an average increase of 13 points. Since launch, we’ve continued to listen and enhance the feature to maximize the number of consumers who can benefit. Shortly after we brought Experian Boost to market, we wanted to ensure consumers who paid their monthly telecom and utility bills from their savings or credit cards could benefit alongside those who paid these reoccurring bills through their checking account, and we did. Against the backdrop of the COVID-19 pandemic, at a time when television streaming had skyrocketed, we wanted to ensure consumers who subscribed to video streaming services, including Netflix®, Hulu™, HBO Max™, Disney+™ and others, could use these monthly payments to build their credit histories, and we did. We regularly connect new streaming service partners to Experian Boost. Most recently, consumers who subscribe to Paramount+, Peacock, Showtime® and ESPN+ can also contribute their on-time bill payments directly to their Experian credit file through Experian Boost. Earlier this year we introduced Experian Go™ - a free, first-of-its-kind program to help “credit invisibles,” or people with no credit history, begin building credit. Within minutes, credit invisibles who enroll in the program can have an authenticated Experian credit report, tradelines and a credit history by using Experian Boost and instant access to financial offers through Experian Go. Since launch, more than 84,000 consumers have established an Experian credit report through Experian Go and become visible to potential lenders. As a next step, today we’ve announced a new beta release of Experian Boost that allows consumers to contribute qualifying, “positive” residential rent payments directly to their Experian credit file. This capability makes Experian Boost the only feature that can instantly improve a consumer’s FICO® Score 8through positive rent payments at no cost. This is the next step in our commitment to helping consumers get the credit they deserve. With the beta release, consumers who rent from over 1,500 of some of the largest U.S.-based property management companies, and who pay their rent directly to their property management company or through platforms like AppFolio Property Management, Buildium®, Yardi® Breeze and Zillow® Rental Manager, can add qualifying positive rent payments to their Experian credit file through Experian Boost. Based on preliminary analysis[3] highlighting the potential impact of positive residential rent payment reporting through Experian Boost, we estimate 66% of consumers will see an instant increase to their FICO® Score 8, a FICO® Score 8 improvement of nearly 10 points on average for those who receive a boost and are new to using Experian Boost. And we’re not done yet. To ensure more renters can benefit, we’ll continue to add new property management companies over time. In later phases, we’ll update the feature further to add individual landlords and smaller property management companies over time. I’m proud of what we’ve accomplished so far and, as we look ahead, I’m excited for the ways we can help consumers that are yet to come. With our focus on consumers and our ability to listen and innovate, I believe we’ve just scratched the surface in terms of our capacity to help bring financial power to all. [1] Results will vary. Not all payments are boost-eligible. Some users may not receive an improved score or approval odds. Not all lenders use Experian credit files, and not all lenders use scores impacted by Experian Boost®. Learn more. [2] Credit score calculated based on FICO® Score 8 model. Your lender or insurer may use a different FICO® Score than FICO® Score 8, or another type of credit score altogether. Learn more. [3] Analysis completed using FICO® Score 8 with Experian data. Experian and the Experian trademarks used herein are trademarks or registered trademarks of Experian and its affiliates. The use of any other trade name, copyright, or trademark is for identification and reference purposes only and does not imply any association with the copyright or trademark holder of their product or brand. Other product and company names mentioned herein are the property of their respective owners. Licenses and Disclosures.

As a leading information services company, some of our chief priorities include protecting and ensuring the accuracy of consumer information. The integrity of our data is critical and aligns with our efforts to advocate for financial inclusion for everyone. Data accuracy is particularly relevant for the transgender and non-binary community with regard to name changes. It’s important to note that information about gender/sex, age, race, ethnicity, religion or sexual orientation is not included in credit reports or scores. However, when someone transitions, and changes their name, their credit and financial history may still be tied to their birth name, which is also referred to as their “deadname.” This can unintentionally “out” the consumer or force them to establish a new credit history. At Experian, we have a process through which those who identify as transgender and non-binary can provide legal documentation to prove their identity without the negative emotional and financial impact. You can learn more about this process here. When you affirm your identity and update your name, Experian will also suppress your deadname so it does not appear on your Experian credit report. Taking these steps only changes your name on your Experian credit reports, and you may need to inquire about the process with other credit bureaus. Fair access to credit tools is part of our mission, as is providing these services with dignity and respect. At Experian, this is our purpose, advocating for all communities and people. This is financial inclusion.

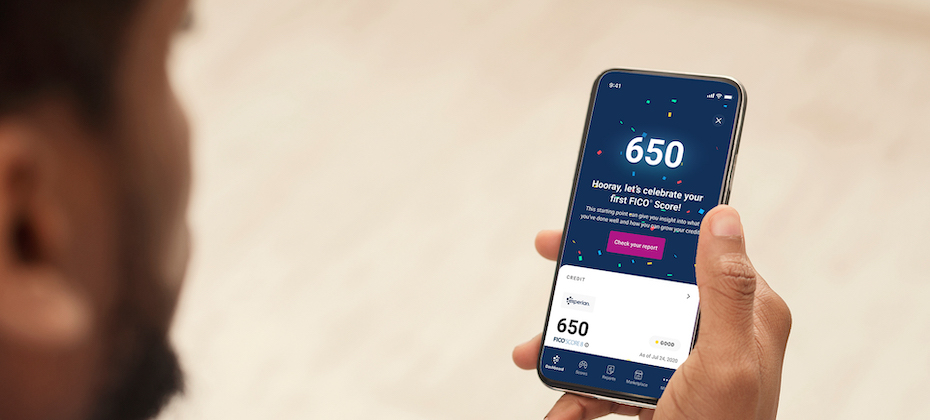

For the past several years, we’ve been on a journey to improve financial access for millions of people around the world. We’ve made it our job to help consumers get the best financial outcomes. This focus on consumers defines us and informs everything we do. In 2019, we reshaped how consumers access credit with Experian Boost™. Since then, nearly 9 million consumers have connected to the product. While we are proud of what we have and continue to accomplish with Experian Boost, we know there is more to be done to ensure more consumers can access fair and affordable credit. Improving outcomes for underserved consumers When credit is used responsibly, it can create new opportunities from getting a college degree, buying a car or home and starting or expanding a business. These are milestones that help people establish careers, build wealth and ultimately achieve greater financial freedom. Yet, there are millions of consumers who are unable to participate in the mainstream financial ecosystem today because they don’t have a financial identity. Without an established credit history, these consumers struggle to qualify for everything from an auto loan to a mortgage and even an apartment or employment. This problem more frequently impacts communities of color with 28 percent of all Black and 26 percent of all Hispanic consumers currently unscoreable or credit invisible. Increasing financial inclusion depends on creating opportunities for underrepresented consumers to succeed. And this starts with ensuring all consumers have a financial identity. Bringing financial power to all with Experian Go The challenge is many consumers who are not in the credit ecosystem today are unsure where to start. Today, we reached a pivotal and exciting milestone in our commitment to consumers with the launch of Experian Go™. This new program opens the front door to the financial ecosystem for millions of consumers by helping them establish their financial identity and move from credit invisible to scoreable. Within minutes, credit invisibles can have an authenticated Experian credit report, tradelines and a credit history by using Experian Boost™[1], and instant access to financial offers through Experian Go. In fact, early analysis shows 91 percent of consumers with no credit history who connect to Experian Boost, a free feature that allows users to contribute their on-time cell phone, video streaming service, internet, and utility payments directly to their Experian credit report, can become scoreable in minutes with an average starting near-prime FICO® Score of 665[2]. Throughout the experience, we’ll provide ongoing credit education and access to tools like Experian Boost™ to make it easy for consumers to learn how to use and responsibly grow their credit histories. Until now, our industry has struggled to verify the identity of credit invisibles. Over the last several years, we’ve introduced new identity verification technologies to our toolbox. With Experian Go, we’re leveraging these technologies to verify a credit invisible’s identity and get them in the front door to start building credit. No other credit bureau or organization is doing this today. During our pilot, we helped more than 15,000 consumers establish their credit history. This is a great start. Now that Experian Go has launched, I look forward to helping millions more consumers get the credit they deserve. To learn more about Experian Go, visit www.experian.com/go. [1] Results may vary. Some may not see improved scores or approval odds. Not all lenders use Experian credit files, and not all lenders use scores impacted by Experian Boost. [2] Experian analysis based on an anonymized and statistically relevant sample of consumer credit reports with only Experian Boost tradelines included and FICO® Scores. December 2021.