Financial Access

Experian is unlocking the power of data to facilitate access to fair and affordable credit for both consumers and businesses. With our products, services and partnerships, we are working to improve financial inclusion for all. Read about our latest financial access news below:

For the past several years, Experian has been on a journey to help drive financial inclusion for millions of people around the world. This has required significant changes in how we operate, who we partner with, and the products and solutions we offer —and with those changes comes a renewed sense of purpose. What we do and the actions we take have the potential to improve lives. We are actively seeking out unresolved problems and creating products and technologies that will help transform the way businesses operate and consumers thrive in today’s society. But we know we can’t do it alone. That’s why over the last year, we have built out an entire team of account executives and other support staff that are fully dedicated to developing and supporting partnerships with leading fintech companies. We’ve made significant strides that will help us pave the way for the next generation of lending, while improving the financial health of more people around the world. Earlier this week, I attended the FinovateSpring conference in San Francisco to speak with fintechs and financial institutions about ways to put financial health at the center of an organization’s plans to build trust, reach new customers and ultimately grow business. We are developing platforms that are designed to play to the strengths of fintechs and disrupt the industry. In the past, we have looked at unresolved problems and asked ‘why?’ Today, with our fintech partners, we look at potential solutions to these unresolved challenges and say, ‘why not.’ As part of our concentration on fintech, Experian has made significant investments in alternative data, such as the game-changing Experian Boost platform, which was launched just two months ago and is already reshaping the way consumers gain access to credit. Since we launched Experian Boost, consumers across America have instantly increased their credit score by sharing their bill payment history for things like utilities, mobile phones and cable TV payments – payments which had never been factored into a credit score before. And, yes, this platform came to fruition as a result of a fintech partnership. We have partnered with fintechs in other powerful ways, too. Our new Ascend Analytical Sandbox – a first-of-its-kind data and analytics platform - gives companies instant access to more than 17 years of depersonalized credit data on more than 220 million U.S. consumers. This creates better opportunities for consumers by allowing our clients to provide more tailored solutions. It’s a great example of the power of analytics and we’re very proud of it. During our time at Finovate, we were able to engage in meaningful conversations with fintech leaders who were united in our goal of helping more consumers access the financial services they need. We’re more inspired than ever before to continue to build and explore strategic partnerships that will ultimately improve the lives of American consumers.

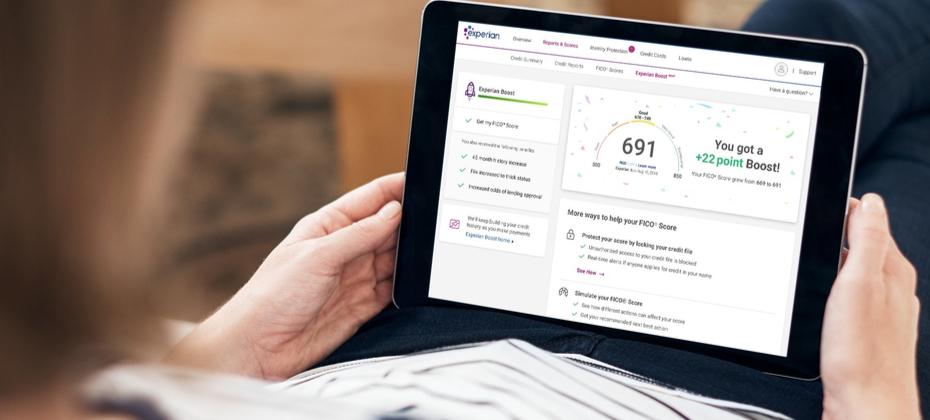

Today marks a notable milestone in our company’s history and for consumers. Today we officially launched Experian Boost, a free tool that, for the first time, will allow millions of consumers to add positive payment history directly into their credit file for an opportunity to instantly increase their credit score. For the past several years, we have been working to develop new products and innovations that will disrupt the credit industry and help improve the financial lives of consumers. This commitment to financial inclusion has defined us and created a real sense of purpose for everyone who works here – and that purpose is realized with the launch of Experian Boost today. There are more than 100 million Americans who don't have access to credit today. A low credit score, due to a thin file or incomplete information, may force these consumers to rely on high interest credit cards and loans. The fact that many of these consumers consistently and responsibly pay cell phone and utility bills on time every month hasn’t seemed to matter. At Experian, we know that’s not right. A good credit score is a gatekeeper to better financial opportunities. We need to develop products and services that make achieving and maintaining a good score easier, not harder. As the consumer’s bureau, we want to ensure that as many people as possible can access and participate in the financial system, and we believe everyone deserves a fair shot at achieving their financial dreams. We have a fundamental mission that is shared by our colleagues around the world: to strive to be a champion for the consumer. With Experian Boost, we're bringing that mission to life and I couldn’t be prouder. Many of our colleagues at Experian worked tirelessly over the last few years to make this day a reality. To everyone who’s played a part, I offer my very heartfelt thanks. It’s truly a great day to be a part of Experian, and we know there will be a lot of great days ahead for all the consumers who will benefit from having their credit score truly reflect who they are. To find out more about the Experian Boost, please visit experian.com/boost.

Financial exclusion is a global issue with an estimated 1.7 billion adults currently ‘unbanked’ . Experian’s core mission is to help bring financial inclusion to every adult in the world. There are currently millions of ‘thin file’ consumers and SMEs in sub-Saharan Africa. These are consumers with limited information on a traditional credit bureau or have no information at all, so-called ‘invisibles’, who find themselves excluded from mainstream finance. They often face more difficulty – or higher costs - when applying for financial products or services. That’s why we are proud to announce today the launch of a ground-breaking new smartphone app, GeleZAR, in South Africa, which aims to bring more micro-entrepreneurs into the mainstream economy and ensure they get the credit score they deserve.. Using the expertise of our global innovation hubs, we have developed a unique financial education and credit scoring mobile app. GeleZAR is designed to educate entrepreneurs and individuals on how to manage their finances, budget and credit score in a fun, entertaining and digestible way. It can also advise individuals on how to maintain a good credit health and recommends remedial actions where needed. In partnership with a local South African consumer and fintech developer, Experian designed the app specifically for entry-level smartphones. We are also working with one of the largest low-cost mobile phone retailers in Africa to trial the app which has been pre-installed on a range of its entry-level smartphones.. The intention is to extend the rollout and make the app accessible for free on more than six million devices annually. Working with alternative data that an individual user consents to share on the app, GeleZAR will be able to assess an individual’s stability, build a credit profile and potentially improve their credit score. This in turn could enable them to access a broader range of financial products at more affordable interest rates. This is a great example of how Experian is innovating to find new ways to empower our customers while uplifting societies. It also fulfils our passion for financial inclusion and the accurate assessment of affordability. Experian’s cutting edge technological capabilities enable us to use the power of data to transform lives, businesses and economies for the better. Through our pioneering work in this space we hope to help consumers around the world on their credit journey. GeleZAR is just one of the ways we are delivering on our mission to build and improve the credit files of millions of people in South Africa and beyond.

Elio Vitucci, CEO of Experian MicroAnalytics, authored the op-ed Financial Empowerment for the Emerging Market Consumer in U.S. News & World Report. To date, Experian MicroAnalytics has extended over 4.9 billion credit offers to the world’s unbanked people, and nearly half of those offers were in the past year. The new emerging market consumer is becoming empowered with tools and services needed for a better quality of life and economic vitality. Experian MicroAnalytics contributes to global progress by helping those with no credit history gain access to credit and financial products for their businesses and personal needs. In regions where financial history doesn't exist, understanding creditworthiness is a challenge. While only a small minority of people in emerging markets have access to credit services, the vast majority have access to mobile services — most of them on a prepaid plan. As such, an alternate credit identity can now be established. Financial services in the emerging world are drastically underserving the potential banked population. Long-term economic growth in the emerging world hinges on access to financial services. Unlocking the new consumer's credit capability is the new financial frontier. Learn more about how Experian is empowering emerging market consumers with financial products and services to improve quality of life and increase prosperity around the world.

Promoting a better understanding about how the credit economy works and improving financial awareness, so that people can take control of their financial situation with positive, proactive decisions, is absolutely fundamental to our business strategy. This is encapsulated through our financial education programmes. In partnership with Young Enterprise, we have created 28 Centres of Excellence for schools to support children’s financial education. And through Experian’s Values, Money & Me, we have created the UK’s first free online teaching resource to help children develop their financial knowledge and abilities. Credit Awareness Week is, then, a natural place for us to continue that focus. And to take that conversation more widely, to our industry partners, for us all to consider how we might find better ways of working, and drive better outcomes for our customers. There’s no doubt that we are living through a period of significant financial uncertainty. At times like this it is important that consumers are aware of all the options available to them from a financial perspective. And we believe your credit score is one of the first things you should look at. It’s perhaps surprising then that our annual Credit Awareness Week consumer survey found that public awareness of credit and how it can be used to help with day to day challenges still remains relatively low, despite some signs of improvement – potentially driven by the widespread availability of free score services. The percentage of people who said they know their current credit score went up from 22% to 26%, while 47% have ever checked their credit report, up from 45% last year. However, there is still much misunderstanding coming through. 39% of those surveyed wrongly believe their own credit score can be affected by a previous resident of their address having a poor credit score, while 14% think, incorrectly, that checking their own credit report and score has an impact on their credit rating. More than a quarter (26%) are also wrong to believe having a high income can affect their score, while 14% are incorrect to think checking their own score has an impact. The number of people who believe that the system needs to provide clearer explanation about how the decision was made when credit is refused has also increased. What the results of our poll tell me is that more needs to be done in promoting a better understanding about all the options available, like the existence of eligibility and comparison services which are designed to help empower people shop around for better deals and, where credit is concerned, avoid damaging their score while they do so. So there is work to do in building a better understanding about how credit works, which is something we are committed to and that’s why we are supporting this campaign. To help, Experian and Credit Strategy have launched an improved ‘credit refusal pathfinder’ [add hyperlink] tool, to help guide people who apply for credit and get turned down. I’d encourage everyone, even those of us who think we know this business inside out, to take a look at the tool. And, in the spirit of building greater trust and transparency with our customers, let’s take this opportunity to have a think about what we in the industry can do to make things clearer for people. Helping them understand how lending decisions are made and empowering them to take control of their financial situation and make better, sustainable choices through affordable access to finance.

Patients ideally should know what they’re going to owe when they show up for an appointment – the last thing they need is a big financial surprise to add to the stress of their visit. Similarly, doctors, nurses, hospitals and all healthcare providers help people to stay healthy day in and day out. Providers should be able to go to sleep at night knowing that they’ll be fairly compensated for the work that they do. However, making that happen isn’t easy. Behind the scenes, contracts, benefits and eligibility between medical groups, hospitals and insurance payers are fairly nuanced and complex. Clients benefit when it comes to how much a patient owes a hospital or medical group after treatment, rough estimates aren’t ideal – perfection is difficult/ create problems and issues. Billing must have pinpoint accuracy and add nuance based on unique contract terms that all medical groups and hospitals sign with their employers and payers. The details can actually be quite difficult to keep straight, and there is an extensive amount of variation in each contract’s rules. Experian Health works to make payment transparency the norm, so that patients know what to expect and healthcare providers are paid fairly, accurately and in a timely fashion. I began working for Experian in 2004 but my interest in product development and research eventually led me to Experian Health. My team of more than 100 Experian employees painstakingly reviews contracts, patient eligibility, benefits information and historical claims to generate an accurate fee estimate for each patient’s medical visit. Nuance/aiding are helping to work toward this. We utilize up-to-date technology that organizes all the information we find in an extensive database and review the claims on behalf of both our medical group clients and patients. The biggest challenge for me and my team is anticipating both patients’ and hospitals’ future needs and innovation in the field. Any time healthcare policies are changed or reimbursement guidelines shift, it affects our clients and requires nimble thinking on our part. How do we ensure that our technology is as modern as possible and our team members stay current on the latest trends and news? I’m looking forward to seeing how we continue adapting in the future.

In the United States, many individuals struggle with managing their money. In fact, a recent study by Mintel found that only 19 percent of respondents would rate themselves highly on their financial knowledge. As the Director of Public Education at Experian, this finding, while concerning, is not surprising. Since joining Experian twenty years ago, my team and I have spoken with thousands of consumers across the country about personal finance. From bank presidents to blue-collar workers, the individuals I speak to all want the answer to one question – “how can I plan for my financial future, taking into consideration life’s ups and downs?” The Mintel survey found that 21 percent of Americans today are not at all confident about reaching their financial goals, but my team and I are working every day to change this. We are committed to working with various communities within the U.S. to help them better understand their finances. We provide training for young men and women in the Air Force about how to succeed financially while on active duty and when returning to civilian life as part of a program with the Hero’s at Home organization. In partnership with the Society for Financial Education and Professional Development, we also educate young adults at historically black colleges and universities, answering questions about building credit and managing money. Through the LifeSmarts Competition, we challenge high school students to compete on knowledge of personal finance. And through some of our other programs, we work with low-income women and immigrant populations to promote financial inclusion by helping them establish credit or understand loans. Through these experiences, we’ve met countless inspiring individuals from various backgrounds with compelling success stories. For example, a member of the Air Force once told us that, following one of our sessions, she was able to improve her credit and buy her first home. Stories like this are why I am so proud to be part of the only dedicated financial education team in the industry. I am excited to continue empowering people from all walks of life to reach their financial goals. Learn more about the Mintel research here.

The real-time economy is all around us. With the swipe of a finger, we can order a car, find a babysitter or make a mortgage payment.

About a year ago, my colleague Natalia invited me to join her in a new volunteer opportunity with the Ministry of Housing in Colombia. The Ministry had created a new program called Mi Casa Ya – which means in English “My Own Home Now,” to help people in Colombia own their first homes. Excited and eager to lend a hand, Natalia and I introduced ourselves to Alejandro, the Director of the National Housing Fund at the Ministry of Housing. Alejandro told us how an unexpected roadblock threatened to derail the program. He had created Mi Casa Ya so that even the poorest people in the country could get a government subsidy to purchase a home. To get the subsidy, they just needed to qualify for a mortgage from a local bank. But that was the problem. In order to get the bank loan, applicants needed a strong credit history. Yet most of the people looking to take advantage of the subsidy through Mi Casa Ya, he explained, were considered “credit invisible.” That is, they had no viable credit history, thin or un-scoreable credit files, or they simply had bad credit. So banks had no choice but to reject them. Natalia and I heard the frustration in Alejandro’s voice, and we knew just how we could help. We told Alejandro that if the Ministry could determine which individuals were being rejected by the banks, we could come in and build credit scores for them using Experian’s data. You see, building credit histories is the sort of thing we do every day at Experian. Over the years, Experian has innovated with analyzing traditional and alternative data sources, such as public records and magazine subscriptions, to create the most accurate and realistic picture of someone’s credit. And by unlocking the power of this data, we are able to identify the data sets that can help lenders make better decisions when making loans, especially for people with thin credit files. Working with Natalia and Alejandro for Mi Casa Ya over the past year has been incredibly rewarding – and our work here isn’t done! Since I work in the legal department at Experian, I am now involved in reaching an agreement with the Ministry of Housing to help advance this project. The details are tricky and the process is tedious, but when I think about the people whose lives we have the ability to transform, I just get excited. Because of our work, many more families in Colombia will be able to fulfill their dream of owning their own homes – that’s huge.