Search Results for: covid-19

In a world that was already becoming increasingly digital, COVID-19 expedited timelines and turned forecasted projects into immediate needs nearly overnight. I’ve seen this play out in my role at Experian as well as across the financial services industry. Experian was recognized as an innovative company prior to the pandemic and the current environment has only accelerated our ability to innovate. As we surpassed the six month mark adjusting to our new normal, I was invited to join Bloomberg’s Future of Finance: Leveraging Digital Transformation for a Virtual World roundtable discussion with Senior Analyst of Bloomberg Intelligence Julia Chariell and leaders from IBM, Ally Financial, Deutsche Bank and others, to share how we are rising to meet the needs of consumers and lenders during the COVID-19 pandemic. You can find a recap of our conversation here and view the full video discussion here. We know each American is facing unique COVID-19-related circumstances, so there is not a one-size-fits-all solution. This notion has carried us as we are rising to meet the needs of our clients and consumers during the pandemic. We must allow individuals who can still meet their financial obligations to have access to credit and ensure lenders can identify them. Maintaining and improving financial access for these consumers will play an important role in our road to economic recovery. To continue to lend responsibly, the financial services industry must carefully examine all aspects of consumer financial capability in near real-time – consumer control and consumer-permissioned data play a key role in achieving this. By leveraging accurate data, I believe we have a chance to lessen the impact of the current U.S. economic crisis, extend credit responsibly, and support the hardest-hit consumers as we adjust to a new world post COVID-19.

In the midst of COVID-19, we’ve seen the digital transformation accelerate at a rapid pace—and it’s likely to continue in the months and years ahead. According to McKinsey & Company’s COVID-19 Consumer Pulse survey, most business types have seen more than 10 percent growth in their online customer base during the pandemic and many consumers plan to continue shopping online when store locations reopen. While the shift to digital began well before COVID-19, what does the sudden spike mean for marketers? In short, it means digital campaigns have become mission critical—and subsequently, data has become more important than ever. People are more than just their interactions with your brand. They consume information and engage other brands from multiple devices and channels, resulting in hundreds of digital touchpoints. You need to use data to connect these touchpoints to better understand your audiences’ needs, inform your messaging, optimize digital campaigns, and most importantly, build and establish a human connection. Businesses have troves and troves of data, but oftentimes struggle to generate insights. You need to find the right partner to help manage the data and unlock its potential. To help, Forrester recently released its Now Tech: Consumer Data Marketing Services, Q3 2020 report that provides an overview of 22 consumer data marketing providers that can help you leverage your first-party data and create a more comprehensive view of customers and prospects—Experian is proud to be included in the list. Finding the right partner is important; you have to remember data is a privilege and you need a partner that can help you provide value to your customers—otherwise, trust can quickly erode. And without trust, data and your marketing campaigns become obsolete. Identify what matters most to you. Do you need to enrich your current database? Build look-a-like audiences? Do you need to connect digital and offline identities? Do you need to activate your data? With a strong foundation in data and identity resolution, Experian is committed to helping you learn more about your customers and help them navigate their unique circumstances. Experian's ConsumerViewSM database includes attributes on more than 300 million consumers and 126 million households, including demographic data, purchasing behavior, and lifestyle information. In addition, our MarketingConnectSM platform eliminates the need for disparate solutions and enables marketers to access and manage offline and online customer identity attributes, such as MAIDs and IPs. Now, more than ever, consumers want to be heard. You need a data-driven strategy to meet that expectation. The right partner can help you expand what you already know about your customers and allow you to communicate with them effectively and address their most pressing needs. Learn more about how Experian can help you maximize the potential of your data.

In May 2020, Experian launched Sure Profile and became the first company with an offering to fight synthetic identity fraud that’s integrated into the credit profile with market-leading assurance. In fact, we are so confident in our solution that we’ll share in loan losses on assured profiles if we get it wrong, a first for the industry. Recently, International Data Corporation (IDC) highlighted Sure Profile in the report, IDC, Synthetic Identity Fraud Update: Effects of COVID-19 and a Potential Cure from Experian (doc #US46690220, July 2020) stating “IDC Financial Insights believes that Experian's Sure Profile has the potential to have market disrupting effects in the battle against SIF (synthetic identity fraud).” According to McKinsey, synthetic identity fraud is the fastest growing financial crime in the United States, accounting for 10% to 15% of lender losses each year. Synthetic identity fraud occurs when fraudsters combine real and fake information to create “Frankenstein IDs” which are then used to obtain credit or to add these identities as authorized users to existing credit accounts. Then, financial institutions report the identities to credit reporting agencies. A new record with the false information is created and subsequently, the synthetic identity can be used to generate other fake accounts. It is a significant problem that Juniper Research expects will lead to $48 billion in annual online payment fraud losses by 2023. IDC recommends that financial institutions consider Sure Profile when researching how to fight synthetic identity fraud. For institutions that use an analytical platform to detect synthetic identities, IDC suggests examining Sure Profile to see how it can supplement their models, or even replace them. "Synthetic identity fraud is a massive problem for banks, and I believe that the effects of COVID-19 will exacerbate the problem. However, at the same time, Experian launched a new offering that I believe will be a game changer for how banks attack the synthetic identity problem." — Steven D'Alfonso, research director, IDC Financial Insights Sure Profile validates identities, detects profiles that have an increased risk for synthetic identity fraud and helps cover resulting losses for assured profiles. Leveraging the capabilities of the Experian Ascend Identity Platform™, it uses data to drive advanced analytics, including newly developed machine learning models that predict the likelihood of synthetic identity behavior. Sure Profile provides lenders a simple approach to define and detect synthetic identities early in the originations process. To learn more, check out Experian's Sure Profile.

Experian is a proud member of the Better Identity Coalition, which is committed to working alongside policymakers to improve digital security, identity verification, privacy and convenience for everyone. Together, we’re seeking innovative ways to empower Americans to take control of their identities and conduct online business securely. On September 11, 2020, a bipartisan group of House members led by Congressman Bill Foster, introduced the “Improving Digital Identity Act of 2020” to modernize and digitize our essential government identity infrastructure. Through the Better Identity Coalition, Experian supports this bill and the steps it’s taking to help improve digital identity, security and privacy for Americans. As a result of the impact of the COVID-19 pandemic, consumers and businesses have quickly adapted to doing nearly everything digitally, but most government-issued identity credentials, such as drivers’ licenses and passports, were not created to be verified online. The “Improving Digital Identity Act” creates a comprehensive approach across federal, state and local government to address critical shortcomings in identity tools that today make it easy for fraudsters to prey on Americans. The bill creates a framework of standards that new identity solutions should follow to ensure privacy. The bill also allows for federal grants to be given to states to jumpstart modernization of the systems that provide driver’s licenses or other types of credentials to enable digital identity verification, in accordance with the NIST framework. It’s important that the bill gets passed to bring the United States up to speed on digital identity and help fix government-issued identity problems. In addition to supporting bills like the “Improving Digital Identity Act of 2020,” Experian is working hard to develop new innovations to make digital commerce safer for consumers and businesses. Our most recent innovation, Sure Profile makes us the first company with an offering to fight synthetic identity fraud that’s integrated into the credit profile with market-leading assurance. In fact, we are so confident in our solution that we’ll share in loan losses on assured profiles if we get it wrong. Experian is also proud to be the only credit bureau in the initial rollout of the Social Security Administration’s new electronic Consent Based Social Security Verification service. Our inclusion ensures our clients have the tools to more easily detect online fraud while also better recognizing legitimate consumers.

Download or listen here: Every week, we talk about important data and analytics topics with data science leaders from around the world on Facebook Live. You can subscribe to the DataTalk podcast on iTunes, Google Play, Stitcher, SoundCloud, and Spotify. DataTalk features data science leaders at MIT, Caltech, United Nations, Gartner, Twitter, Google, Salesforce, Amazon, Oracle, IBM, Google, Spotify, Dow Jones and downloaded in over 75 countries. In this week’s #DataTalk, we chat with David Kopec about his academic background, consulting, teaching computer science courses, podcasting about software, and his latest computer science book on Python. Some topics discussed include: Tips for Computer Science Grads Entering Workforce During COVID-19 Dealing with Ethical Dilemmas at Work & Knowing When to Leave Advice for Getting Into Computer Science Grad School Programs Teaching Tips for New College Instructors & Improving Classroom Discussions Strategies for Teaching Complex Computer Science Topics in College Synchronous vs Asynchronous eLearning: Advice for College Instructors Latest Book: Classic Computer Science Problems in Python And check out the full video discussion with David Kopec here. About David Kopec David Kopec is an Assistant Professor of Computer Science & Innovation at Champlain College in Burlington, VT. Prior to joining the faculty at Champlain, David worked in the startup world as a co-founder and consultant to early stage tech companies with a concentration in iOS app development. He is author of the following books: Classic Computer Science Problems in Python Classic Computer Science Problems in Swift Dart for Absolute Beginners Classic Computer Science Problems in Java (Upcoming) Check out all his books here. You can also get a 35% discount on David's books ordered through Manning with this code: poddatatalk20. David holds an A.B. in Economics from Dartmouth College, as well as a M.S. in Computer Science, also from Dartmouth. Follow him on Twitter, LinkedIn, GitHub and his Kopec Explains Software podcast. DataTalk is hosted by Mike Delgado at Experian. Please reach out if you have suggestions for topics or guests.

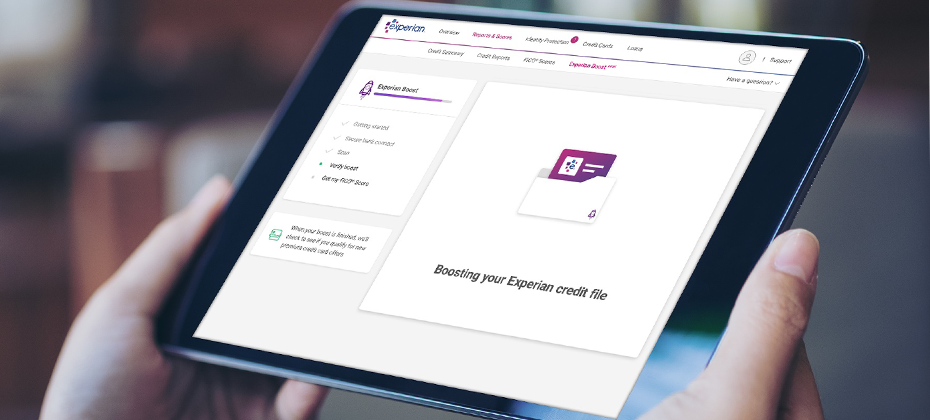

Many of us have turned to streaming services to help us cope during this time of COVID-19. Being able to escape with some good entertainment while still maintaining our social distance is invaluable right now. Television streaming has skyrocketed 85% since March; I’ve certainly contributed to that increase. Now, subscribing to that streaming service can do more than entertain, it can improve a consumer’s financial health. Starting today, Netflix® customers can possibly improve their FICO® Score by adding their positive payment history through Experian Boost. Experian Boost™† is the innovation we launched in 2019 that can help consumers improve their credit score instantly. So far, approximately four million consumers have connected their utility and telecom bills to Experian Boost, leading to more than 29 million points added to FICO® Scores nationwide. This addition makes sense. Experian Boost already allows consumers to receive credit for paying their cable bills, so paying for a video streaming service on time should also help prove creditworthiness. It’s critical that we meet consumers where they are and adapt to help them in their current position, especially during a pandemic. Anticipating and prioritizing consumer needs is our focus and drives our innovation. After all, we’re consumers too. I’m proud of how our team uses their personal experience and their roles at Experian to create opportunity for millions of people to improve their financial health, especially during these uncertain times. Our job is to help consumers, and that doesn’t stop with their credit score. That’s why we’re also launching new free features available to everyone within the CreditWorks Basic and Premium products. The free tools provide personal insights and resources that can help consumers better save money and manage their financial profile. For more information about Experian Boost go to: www.experian.com/Boost. Experian and the Experian trademarks used herein are trademarks or registered trademarks of Experian and its affiliates. The use of any other trade name, copyright, or trademark is for identification and reference purposes only and does not imply any association with the copyright or trademark holder of their product or brand. Other product and company names mentioned herein are the property of their respective owners. †Results may vary. Some may not see improved scores or approval odds. Not all lenders use Experian credit files, and not all lenders use scores impacted by Experian Boost. Credit score calculated based on FICO® Score 8 model. Your lender or insurer may use a different FICO® Score than FICO® Score 8, or another type of credit score altogether. Learn more.

We sit in a pivotal position in the societies where we work. For us at Experian, using our data and expertise to create a better tomorrow is more than an opportunity. It’s a responsibility. We are pleased to announce we have published our annual Sustainable Business Report 2020, which outlines Experian’s dedication to social and environmental issues and details our corporate responsibility performance. In the report, we also highlight Experian’s target to reach 100 million additional people globally by 2025 with social innovation products and services. Additionally, the Sustainable Business Report focuses on our ambition to become carbon neutral by 2030. By utilizing renewable energy, reducing the carbon impact of business travel, and investing in high-quality carbon offsets, we reduced our carbon footprint by 8% last year and cut the carbon intensity of our business by 14% per $1,000 of revenue compared with the previous year. Additionally, 29% of Experian’s worldwide energy was also renewable. We are excited to share a few key takeaways from this year’s Sustainable Business Report: Experian employees volunteered 54,500 hours in and outside of work time to support their communities. This included over 3,500 hours in March 2020 to support communities as the COVID-19 crisis took hold. In Brazil, we have supported the introduction of new legislation enabling millions of consumers to benefit from the use of ‘positive’ data about the credit and other bills they pay on time. Experian Boost helped over 1.5 million Americans improve their credit scores, collectively boosting their FICO® scores by more than 17 million points. Prove ID-Link helped 7.5 million people in India prove their identity. As a result, more people are able to open a bank account and access credit for the first time. Learn more by viewing or downloading our full Sustainable Business Report here.

The panel included Rod Griffin: Senior Director, Consumer Education and Advocacy, Experian; Forbes Advisor; Sara Rathner: Credit Card and Travel Expert, NerdWallet; Beverly Harzog: Credit Card Expert and Consumer Finance Analyst for U.S. News; Alicia R. Hudnett Reiss: CERTIFIED FINANCIAL PLANNER™; Alexandria White: Credit Cards Reporter at CNBC Select; Molly Ford-Coates: Founder, Ford Financial Management; and Take Charge America. Questions We Discussed: Q1: How can your health affect your finances and vice versa? Q2: How do you eat healthy on a budget and busy schedule? Q3: What are some grocery store hacks that can save you money on food? Q4: What are some apps to help you save money on groceries? Q5: What are some budget-friendly meal prep tricks to help you save money? Q6: Where can you get free exercise resources such as workout plans and videos? Q7: What are some free outdoor activities for staying in shape? Q8: What are some creative and inexpensive home workout hacks for those with no equipment or space? Q9: Where can you buy inexpensive fitness apparel without sacrificing comfort and style? Q10: Any last-minute tips on eating healthy and exercising on a budget? Retweet these insights from our community: A1. Staying healthy allows you to continue working, earning and enjoying life. Sudden illness or long-term unhealthy habits can be costly from a financial standpoint, but also compromises quality of life. #creditchat — Take Charge America (@TCAsolutions) July 15, 2020 A2: With more and more people cooking at home and altering their shopping habits during the COVID-19, now is an ideal time to reevaluate your grocery purchasing habits. Planning can save you time, grocery apps (potentially) save you $$. #CreditChat https://t.co/5XWYI716Fv — Forbes Advisor (@ForbesAdvisor) July 15, 2020 A3: Ways to save at the grocery store: go in with a list, buy the store brand versions of products, see if you can save money buying in bulk, figure out which store in your area has the best cost of certain items you always buy. #CreditChat — Christina Roman (@Teena_LaRo) July 15, 2020 A3: Ways to save at the grocery store: go in with a list, buy the store brand versions of products, see if you can save money buying in bulk, figure out which store in your area has the best cost of certain items you always buy. #CreditChat — Christina Roman (@Teena_LaRo) July 15, 2020 A4. I make sure to download my local grocery app so that I can clip the e-coupons which automatically load to my store savings card #CreditChat — Alicia 💖 (@leebee653) July 15, 2020 A5: Crock-pot meals are budget-friendly & you usually get plenty of leftovers to meal plan for the rest of the week. #creditchat — Apprisen (@Apprisen) July 15, 2020 A6: YouTube and Pinterest are great places to look for free exercise videos and ideas for workout plans. Many fitness YouTubers have no equipment videos, so you don’t have to buy expensive equipment to follow along. #CreditChat — American Consumer Credit Counseling (@ACCC_TalkCents) July 15, 2020 A7: Walking in your neighborhood or at nearby parks. Playing basketball, tennis, yard work and gardening. #creditchat — Beverly Harzog (@BeverlyHarzog) July 15, 2020 A8. I love this article from Wisebread on cheap home workout hacks: https://t.co/hgz9wlJNWJ #CreditChat — Jennifer White (@Jennifer_Wwhite) July 15, 2020 A9: I love Old Navy, but you can get great buys in these stores, too, from @healthmagzine. #CreditChat https://t.co/XPZVfYHNHn — Beverly Harzog (@BeverlyHarzog) July 15, 2020 A10. Strive for progress, not perfection. Make small changes and good choices you know you can stick with. And stay hydrated — especially this time of year. #creditchat — Take Charge America (@TCAsolutions) July 15, 2020

“What does a credit bureau do?” is one of the most common questions I’ve answered throughout the years – both at conferences and cookouts. Admittedly, it can be difficult understanding the different roles of credit bureaus, credit score companies, and lenders. Amid COVID-19, it’s important for us to define our purpose and help guide you toward the right resources for financial help. As the consumers’ bureau, Experian is committed to examining financial questions and helping consumers, businesses, and lenders navigate this transitional fiscal landscape. It’s important for you to know your financial options and how to separate fact from fiction, especially during times of crisis. Here are answers to some of the most common questions about credit. Do credit bureaus make lending decisions? This is one of the rare instances in credit reporting for which there is a simple answer. No, credit bureaus do not make lending decisions. Lenders – such as banks, mortgage companies, credit unions, and credit card issuers – help consumers borrow money and they make the lending decisions. The credit bureaus are responsible for working closely with lenders to provide information that helps them make informed and responsible lending decisions. At Experian, we equip lenders with accurate and complete data about consumers’ and small businesses’ credit activity and payment history, which enables lenders to develop a full picture of a borrower’s financial health. During COVID-19, it is important for there to be open lines of communication between consumers and lenders about upcoming payments and payment plans. Some lenders are offering deferments and other workable accommodations to ensure consumers do not fall behind on their payments. It is important for consumers to contact their lenders to understand what options are available to them. Do credit bureaus control my credit score (and whether it goes up or down)? Credit bureaus, like Experian, do not determine your credit score. Credit scores are calculated based on third-party credit-scoring models, like those developed by FICO or VantageScore Solutions. These models use information from your credit reports, including credit activity sourced from credit bureaus, to calculate a credit score. The scoring models are proprietary to the companies that develop them. In the most fundamental terms, the credit bureaus are responsible for compiling the credit reports. The scoring companies create algorithms that calculate the score. Credit scores reflect the information in your credit report at the moment the credit score is calculated. The scores will change to reflect changes in your credit report. You control how you use credit, so you play an important role in determining whether your scores trend upward or slip downward. If you consistently make good credit decisions, your scores will trend upward over time. Reviewing your credit report helps you manage your credit and gives you a full picture of what lenders see. Monitoring your credit report is as important as reviewing bills and bank statements, as your credit is an integral part of your overall financial health. Additionally, with an increase in phishing and cyberscams as a result of COVID-19, it’s especially important to stay informed about your credit report, so that you can dispute anything you believe may be inaccurate and ensure that there is no evidence of fraud that could impact your score. Are lending decisions based solely on my credit score? No, credit scores are just one factor in lenders’ decision-making process. Lenders consider additional information when making a decision, such as employment status, income and information about a consumer’s assets and liabilities. In the wake of COVID-19, lenders may start to tighten their credit standards – meaning consumers may need a higher score to receive a loan. Because of this, it is important to be proactive and take action to mitigate any potential negative impact on your credit score. If you’re worried you may miss a payment, contact your lender to discuss your options. Through April 2021, Experian has partnered with our peer credit bureaus to offer a weekly free credit score at https://www.annualcreditreport.com/. This additional measure will allow consumers to access their credit reports frequently and talk to their lenders with the most updated information possible. How are credit bureaus working with the government during COVID-19? At Experian, we fully supported the signing of the Coronavirus Aid, Relief, and Economic Security Act (CARES Act), which provides relief to Americans through expanded unemployment coverage and by providing grants and loans to small businesses. The CARES Act also provided important guidance to lenders about how to work with consumers affected by COVID-19. Experian is working with lenders to ensure appropriate accommodations are made to protect consumers. Additionally, the credit reporting industry has developed reporting standards for lenders to use during emergency periods, such as COVID-19. These reporting standards allow lenders flexibility when reporting accommodations made to consumers who are experiencing hardships due to the pandemic. For additional questions regarding COVID-19 debt and credit relief options, view Experian’s full list of financial and non-financial institutions’ websites where you can find information on relief measures: COVID-19 (Coronavirus) Credit Card and Debt Relief.