Small business owners may have a small business credit card or even use their personal credit card when they’re just getting started. However, as a business grows, new types of financing that don’t depend on the owner’s personal finances—such as corporate credit cards—may become available.

The Difference Between Corporate and Small Business Cards

Corporate and small business credit cards can offer a variety of benefits. One of the main reasons companies sign up for a credit card is to empower employees to make purchases on the company’s behalf by using the company card.

Using these cards, employees won’t have to pay out of pocket and wait to be reimbursed later. And employers may be able to limit where employees can use the card and how much they can spend, giving them greater control over their business finances.

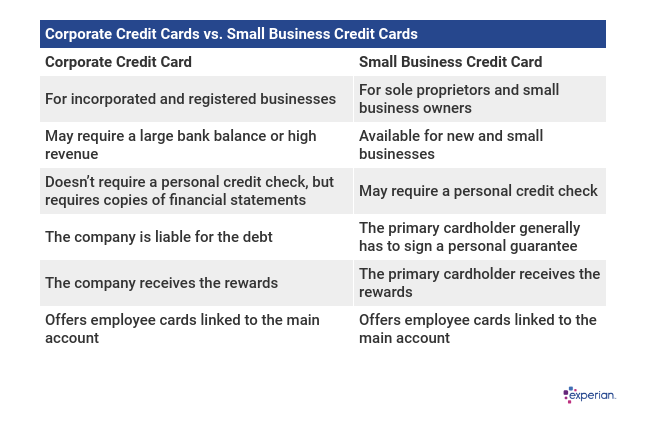

There are some similarities between corporate and small business cards, but they’re not created for the same types of companies. While small business credit cards may be available to any business, corporate cards are primarily intended for large and established businesses.

What Is a Corporate Credit Card?

Corporate credit cards—also known as commercial credit cards—are credit cards for medium- and large-sized businesses, although there are also some corporate card programs for startups. To qualify, a company must be either registered or incorporated—for example, as a limited liability company (LLC) or an S or C corporation.

Card issuers may look at different factors when reviewing a card application, such as the business’s revenue, number of employees, history with the issuer and investors. In some cases, a business may need several hundred thousand (or several million) dollars in revenue to qualify.

You may be subject to a credit check before getting a company card, but it won’t be reported to the credit bureaus under your name or impact your personal credit. Instead, the card’s usage and payment history is added to the company’s business credit report. Corporate cards also often don’t require a personal guarantee, meaning cardholders aren’t personally responsible for the debt.

Unlike many small business cards, corporate cards are often charge cards rather than credit cards—meaning the company must pay the full balance at the end of each billing period. But similarly to personal and small business cards, some corporate cards offer rewards and have annual fees.

Rewards aren’t the only—or even the most important—benefit, however. Companies can request employee cards to easily authorize and track employees’ expenses, eliminating the need for reimbursement requests. Corporate cards may also offer in-depth analytics and integrate with accounting platforms, which can help businesses save time, money and paperwork.

What Is a Small Business Credit Card?

Small business credit cards are typically more similar to consumer credit cards than corporate credit cards. Some consumer and small business cards even have similar names, fees and rewards programs. And, as with consumer cards, small business credit cards may let you revolve a balance and charge you interest on the unpaid amount.

Unlike a corporate credit card, getting approved for a small business credit card can partially depend on the owner’s creditworthiness. If you apply for a small business card, the application might lead to a hard inquiry on your personal credit report. A card issuer may even report the card to the credit bureaus under your name, meaning it can impact your credit—although some only do this if the business misses payments.

Small business cards also generally require a personal guarantee. As a result, if the business can’t afford the payments, you could be personally liable for the card’s unpaid balance.

However, a small business card can help you keep your personal and business finances separate. The cards may also offer business-specific perks, such as free employee cards and bonus rewards on common business purchases. And, as the primary cardholder, you may be able to set limits on employee cards and determine how you want to use the rewards.

Which Credit Card Is Best for Your Business?

Most small business owners, entrepreneurs, solopreneurs and contractors will only be eligible for small business credit cards. However, if you work for or run a medium- to large-sized business or a venture-backed startup, a corporate credit card may be a better option.

While you could open a small business credit card, a corporate card might give you a higher spending limit, more control over employees’ cards and better analytics and reporting. The ability to finance your business’s operations without being personally liable for the debt can also be a major benefit.

Be Sure to Monitor Your Company’s Credit

If you run a business and want to open a business or corporate credit card, your business credit score could be an important factor. Additionally, some small business lenders require a personal credit check before they’ll offer you a business loan, line of credit, invoice factoring or other types of financing. You can check and monitor your Experian business credit report, and get insights into how you can improve your company’s credit scores.

About the author

Louis DeNicola is freelance personal finance and credit writer who works with Fortune 500 financial services firms, FinTech startups, and non-profits to teach people about money and credit. His clients include BlueVine, Discover, LendingTree, Money Management International, U.S News and Wirecutter. Louis lives in beautiful Oakland, California, where he enjoys indoor rock climbing, yoga, and volunteers as a tax preparer.

Louis DeNicola is freelance personal finance and credit writer who works with Fortune 500 financial services firms, FinTech startups, and non-profits to teach people about money and credit. His clients include BlueVine, Discover, LendingTree, Money Management International, U.S News and Wirecutter. Louis lives in beautiful Oakland, California, where he enjoys indoor rock climbing, yoga, and volunteers as a tax preparer.