Tag: business credit score

Did you know your small business has its own credit score? Discover how easy it is to check it with Experian. Just visit https://experian.com/smallbusiness, type your business name, and access your credit profile. Choose from a one-time report or a subscription for ongoing updates. Stay prepared and avoid surprises when applying for funding. Check your business credit today! Check Your Business Credit Score

Mike Olson, Owner of Evenflow Sewer and Drain Service in Kings Park, New York shares how his subscription to Experian Business Credit Advantage has helped him gain access to more favorable financing options.

Both businesses and individual consumers have credit scores that reflect how they’ve historically used credit. Lenders and others use these scores to help determine creditworthiness and make decisions based on what they see. Your Business credit score is based on different information than personal credit scores and use a different scoring system. Learn now to check your business credit score. How Do Business Credit Scores Work? Business credit bureaus use information from a wide range of sources to compile business credit reports, which are then used to generate business credit scores. Data in business credit reports may come from your business’s creditors; its vendors and suppliers; public records and court filings; and collection agencies. For instance, Experian business credit reports show data such as location and contact information, time in business, the company’s Standard Industrial Classification (SIC) and North American Industrial Classification System (NAICS) codes, annual sales and number of employees. It will also show any judgments, UCC filings or tax liens against your company and any accounts in collections. Finally, it looks at how you handle commercial credit payments on loans, credit cards, and bank or trade lines of credit. Each business credit reporting agency weighs the information in your credit report differently and uses its own unique method to calculate your credit score. For example, Experian calculates your business credit score based on: Credit: Number of trade accounts, outstanding balances, payment behaviors, credit utilization and trends over time Public records: How recent and how frequent any liens, judgments or bankruptcies are and how much money was involved Demographics: The number of years you’ve been in business, your SIC and NAICS codes and the size of the business Experian Business Credit Scores range from 1 to 100. As with consumer credit scores, higher scores signify better credit. Where Can I Check My Business Credit Score? You can check your Experian business credit score by purchasing a one-time copy of your credit report or signing up for business credit monitoring, including unlimited access to scores. Reasons to Check Your Business Credit Score Prevents fraud: Monitoring your business credit score can reveal potential fraud or identity theft. A new account you don’t recognize, an application for credit you didn't make, or inaccurate information could be a sign of fraudulent activity. Contact the credit bureau if you see anything amiss on your business credit report. Monitors business health: Your business credit score is an indicator of the financial health of your business. A good business credit score can open doors, giving you access to more credit, lower interest rates and better loan terms. Your business credit may be the deciding factor in whether you get approved for a lease or for trade credit. Regularly checking your business credit score gives you a sense of where your business stands and how successful your applications for credit are likely to be. Safeguards your personal assets: Without a good business credit score, you may need to personally guarantee business loans or use your personal credit score to apply for business credit. This could put your personal assets—and personal credit score—at risk if your business suffers a downturn and you can’t pay these bills. A good business credit score can help you get credit in your business’s name, protecting your personal assets. How to Establish and Build Business Credit Start establishing a business credit history by legally registering your business and getting an employer identification number (EIN) from the IRS. Open business bank accounts, leases, utility services and other accounts in your business’s name, rather than your own. You can begin to build business credit by making moves such as getting a business credit card and requesting trade credit from suppliers, then making your payments on time. For these payments to help your business credit score, you’ll need to work with companies that report to business credit bureaus. Not all of them do, but companies are often willing to do so if you ask. As with personal credit, paying your creditors on time is key to improving your business credit score. You should also check your business credit score regularly, making sure the information in your credit report is correct and current. Keep Your Business Credit Score Healthy Regularly monitoring your business credit score helps keep a pulse on the health of your business—but as a business owner, you already have a lot on your plate. For a convenient way to track your credit score, sign up for business credit monitoring services such as Experian’s Business Credit AdvantageSM. It provides alerts whenever your business credit score changes and early warnings of potential fraud to give you peace of mind. Plus you get unlimited access to your business credit report and score all year long. About the author Karen Axelton Drawing on 20-plus years of experience as a journalist, business magazine editor, and marketing copywriter, Karen Axelton specializes in writing about business and entrepreneurship. She has created content for companies including American Express, Bank of America, MetLife, Amazon, Cox Media, Intel, Intuit, Microsoft and Xerox.

In this business credit education post we cover the top factors that impact business credit your business credit score

There are two types of credit inquiry, hard and soft. How do hard and soft credit inquiries impact your business credit score? We explain the difference.

Paying down commercial debt — is paying one account and going delinquent on another a good idea? In this business credit answer, I want to talk with you about paying down commercial debt, and establishing your small business and gaining access to commercial credit. To do this, you need to focus on your commercial credit score. It's just like your personal credit score. You monitor it, you try to get it up, you pay your bills, and you make sure that everything is being reported to the credit bureau. Doing those activities will help your consumer credit score to go up. Same thing for your commercial credit score. It's looking at any type of commercial credit cards that you have, term loans, how you are honoring the debts that are there, and repaying them. This is what a lender uses to establish your repayment behavior and to look at how much additional funding they want to give to your small business. I had a friend that wanted to pay down some of the debt that they had for a small business, and they had two different accounts that had pretty high debt. He was asking me should I just pay down one of those debts, and let the other one go into delinquency for a while and then come back to that one and pay it down? He figured that way he'd have that sense of paying one down quickly and get one out of the way. And then focus on the other one. Well, what I told him was that it's not just a single debt that your credit score looks at. It's over your whole portfolio of debt. And so, missing a payment or pushing a bill to the side can bring your credit score down and sometimes significantly. So, you look at your credit score and you see it go down maybe five or 10 points. With delinquency, it can bring it down up to 30 points. So it's a big drop. As you bring up your credit score, it takes a little while to regain ground you may have lost. So you want to keep that propensity to pay, and that lender view of you in a very positive light. You can check your Experian Business Credit Score by purchasing a one-time copy of your credit report, or by signing up for business credit monitoring, including unlimited access to scores. Read our post on checking your business credit score for more information.

Starting a small business can be very hard. Building strong credit for the business takes discipline and a certain amount of intention. In this post, we are going to start by describing two imaginary business owners working hard down on Main Street. Harry runs “Harry’s Hardware & Mercantile”, a busy hardware store. He has been trading with local do-it-yourselfers and contractors since 1973. Over the course of the business lifecycle, he established trade credit (Tradelines) with dozens of companies. Mildred just opened “Millie’s Fabric” next door to Harry’s on a shoestring after she got laid off from her job. She founded Millie’s by borrowing money from friends and family, charging most of her startup costs to her personal credit card. And that is where the paths of these two somewhat different businesses diverge. Harry discovered the benefits of establishing tradelines with his suppliers in the early stages of his business and now runs a resilient profitable business. Mildred is embarking on the difficult challenge of establishing her business and will need to manage her cash flow wisely. Like Harry, she will discover how beneficial tradelines will be to her success as she starts to form relationships with trading partners. What are tradelines and how can they benefit my business credit report? Tradelines or trade information comprises the financial payment obligations that a business has to its creditors, suppliers, and service providers that involve payment terms like Net 15, Net 30, 60 or 90. It means your business has that much time to pay back the balance of what you borrow. So, for example, if your business buys $300 worth of products at Net 30 terms, you have 30 days to pay it back. A business will start to add tradelines over the course of its lifecycle and establishing tradelines early in the life of the business can be very beneficial. Experian gets a lot of questions about how tradelines impact a business credit score, so in this post, we explain how that all works. Things to consider before applying for tradelines Establish a legal entity. In order for any business to establish trade terms with your company, take the steps to establish the business as a legal entity (ie; forming an LLC, or S Corporation), sole proprietors should make sure the business is registered with your Secretary of State. Establish separate bank accounts. Separate bank accounts will help keep finances separate and help your business track accounts payables. Business email and contact information. Your vendor will look for signs of credibility when assessing whether or not your business is legitimate. Having a business email address in the name of the company helps in that effort. Avoid using free email services like Yahoo or Gmail. Establishing a presence for your business on social media such as Facebook, Twitter, Instagram, LinkedIn or YouTube, depending where your customers spend time online. Bootstrapping a business in start-up is becoming more common, but the mistake that many business owners will make is leveraging their personal credit for company expenses. Doing this can hurt the owner’s personal credit, and it will not help to build strong credit for the business. It is much more beneficial to establish the business and start applying for credit in the name of the company. Trade supplier types When your business orders raw materials for your business, or purchases office supplies, you would sign for the goods and receive an invoice, and be provided a period of weeks to pay the balance. If your vendor is reporting to Experian, your payment history good or bad will be reported and be a contributing factor in your business credit score. Experian classifies these tradelines as trade supplier types and groups them into the following categories. Financial loan, line, lease, credit card Supply raw materials, building supply, office Services accounting, marketing, financial services Utilities telecommunications, gas, water, electricity Transportation ground, air transport If you are familiar with consumer credit reports, you should be familiar with financial trades, as they are on our consumer credit reports too. These tradelines include loans, lines of credit, leases, and credit cards. Commercial credit reports also include trades from other supplier types as well. Basically, any business that has a commercial accounts receivable portfolio can provide their information to Experian and can establish a tradeline for their business accounts. To contribute data to Experian, you must be able to export into TXT, CSV or XLS (Excel - saved as comma delimited) and also adhere to encryption guidelines. Data contributors are also required to submit monthly updates. If you are interested in becoming a business data contributor you can find more information about reporting to Experian here. How tradelines are classified and updated The first time Experian gets a trade from a specific data supplier for business, that is considered a new trade. On the next update of that trade, it is reclassified as a regular trade. If there are no updates to a regular trade within 3 months, it becomes an aged trade. A trade falls off the business credit report without an update in 36 months. It doesn’t end there; however, if an update comes in for an existing trade, even for a trade that fell off the business credit report, it becomes a regular trade again. Tradeline credit attributes Experian provides information on the total balance outstanding, total credit and utilization, payment delinquencies as of today, and payment trends over time. With this type of grouping, it’s easy to quickly identify newly added trades, regularly updated trades, and trades that are becoming stale. The tradeline disparity between male-owned and woman-owned small businesses Experian studied 3.1 million small business credit profiles between 2016 and 2018 and found variances in the number of tradelines in male-owned businesses compared to woman-owned businesses as the chart below describes. When we look at trade count and the amount of commercial debt or outstanding balances, we saw a different picture between the two cohorts. On average woman business owners have less than 1 tradeline ( avg. .6 trades) vs male business owners, who average roughly 1.4 commercial tradelines. When you compare the average balances, male business owners carry about $40,000 in commercial credit while women business owners carry about $25,000, a $15,000 difference. This difference in the number of tradelines puts women-owned businesses at a competitive disadvantage. To be competitive small businesses should strongly consider establishing tradelines and making on-time payments to these lines. How can tradelines help small businesses gain access to capital? Tradelines can help your business develop the credibility that matters to banks and other capital lenders. A business credit report that includes multiple, positive lines of trade credit in your company’s name shows that your business pays its creditors in a timely manner. Commercial Lenders review this business credit history of tradelines to determine whether to fund a loan or capital, as well as the interest rates and repayment terms if capital is extended. Businesses with good trade credit often qualify for loans with lower interest rates and better payment terms than those with poor or limited trade credit history. For more information about establishing business tradelines check out our post Building Strong Tradelines For Your Small Business.

Experian Business Information Services was delighted to participate in a #CreditChat tweet chat recently. For the chat, we compiled some answers to frequently asked questions about business credit. Why should you separate business credit from personal credit? How do you establish business credit? Is it possible to build business credit with poor credit How do you get a business credit report? How are business credit scores determined How do you correct or dispute information on your business credit report? How do you get higher limits for your business credit? Five tips for establishing, building and monitoring business credit. Why should you separate business credit from personal credit If your business ever becomes at risk your personal credit score becomes at risk as well. And so maintaining separation can protect your personal credit profile should a financial mishap occur in the company or vice versa. Building separation between the two can also help your business develop the credibility that matters the bank's, lenders, suppliers and partners. How do you establish business credit? One of the first things you can do to establish small business credit is to file your business with your State by forming a corporation or LLC to operate your business under and obtain a FIN or EIN number from the IRS. Of course, comply with the business credit market requirements by obtaining proper licenses state and federal requirements for your business. Also, act as a business by establishing accounts (telephone utilities, leases, loans) all under the business name, not your personal name. Even if you operate as a sole proprietor or as a home-based office, prepare financial statements and a professional business plan. Be visible. Find companies willing to grant credit to your business without a personal guarantee. This is typically referred to as Trade Credit. Ensure that your good payment behavior is reported to Experian. Ask suppliers and other businesses that extend your business credit or payment terms to consistently report your payment history to Experian. Also, borrow and then pay on time. Manage your debt, stay current to your terms by making on-time payments and don't rely just on small business credit cards. Secure terms from suppliers or take out a commercial loan. And lastly, monitor your business credit report regularly check and correct outdated information. Be alert to important credit changes in your company's name. Is it possible to build business credit with poor credit? If you have poor credit, you know, it's never too early to enable healthy management behaviors of separating personal from business credit risk and building business credit. But in the early startup stages, you may need to personally guarantee payments. But, the more you act like a business by establishing accounts in your business name, the more likely it is that you'll be able to negotiate and secure good credit terms without personal guarantees. How do you get a business credit report? Experian offers instant online access to business credit reports at the following websites: Experian.com/mybusinesscredit SmartBusiness Reports.com These sites easily help you monitor your own report or access a report on other businesses you can purchase a single report as needed or save with a subscription to a plan. How are business credit scores determined Experian collects business credit data from a wide range of sources such information is used to create a score that illustrates how your businesses historically met its financial obligations. This helps creditors to decide whether to extend credit to your company. Some of those sources include State Filing Offices, Public Records, Credit Card Companies, Collection Agencies, Corporate Financial Information, and Marketing Databases. If you are curious about the behaviors that impact your credit score you can always access our Score Planner Tool. This is a free tool that Experian offers. You can get in there and do what-if scenarios, modeling your current credit behavior and how that impacts your business credit score. It is a very useful tool and helps you build smart business credit. How do you correct or dispute information on your business credit report? First, you must have a copy of your business credit report. You can download that instantly at Experian.com/mybusinesscredit or SmartBusinessReports.com. Of course, review the details circling any incorrect information and you would submit that to BusinessDisputes@experian.com for investigation. That will open a ticket for your case and return to our self-service Web sites for future access and alerts on the case. How do you get higher limits for your business credit? You should monitor your business credit report and manage the factors that drive a good business credit score. And doing so can help you boost your credit score and improve your credit terms. Five tips for establishing, building and monitoring business credit. Act as a business by maintaining a distinctly separate business credit profile from your personal credit. Avoid surprises. Be proactive in monitoring your business credit score. Stay current on payments to creditors. It seems simple but it is great advice that just pay those bills on time. Don't let them go delinquent Ensure that your good payment history is reported to the credit bureau. Establish some good strong trade credit lines and make sure you're doing business with partners who are reporting to the credit bureau. Use business credit reports to limit your risk of doing business with others such as your business customers suppliers and vendors and partners. We hope these business credit answers have been helpful!

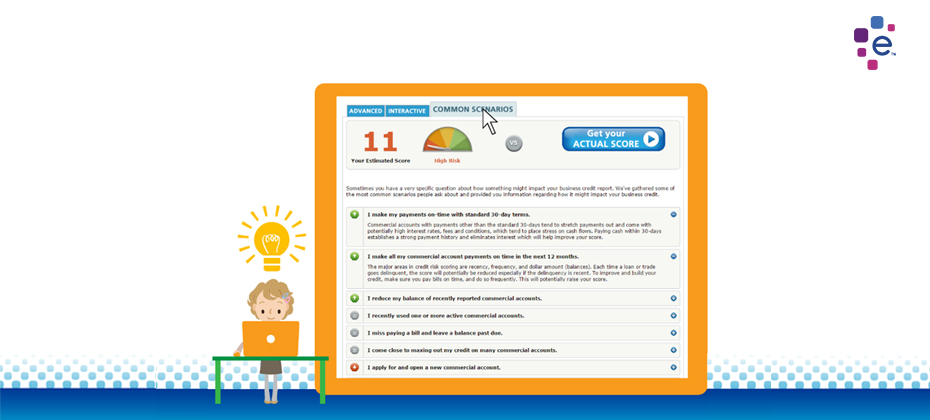

Experian has released a business credit score planner tool to help you run what-if scenarios. It helps you learn behaviors that build strong credit.