Main St. Report Q1 2019

Your window into small business health

Small businesses brushed off a government shutdown as stock markets recovered and income gains remained steady in the first quarter of 2019. Delinquency rates remained mostly stable, with pockets of weakness spread out among regions and industries, notably agriculture in the Great Lakes and manufacturing in the Southwest. Small firms seem to have simply shrugged off the first-quarter headwinds and continued with business as usual.

| Bucket | 18Q1 | 18Q4 | 19Q1 | |

| Moderately Delinquent | 31-90 | 1.72% | 1.68% | 1.74% |

| Severely Delinquent | 91+ | 3.77% | 3.49% | 3.35% |

| Bankruptcy |

BKC | 0.16% | 0.16% |

0.16% |

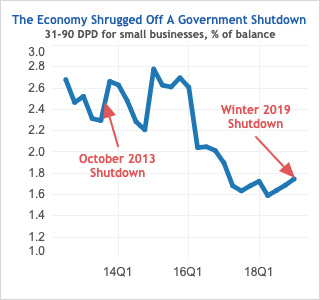

The government shutdown in the first quarter came in with a bang and went out with a whimper as small businesses mostly shrugged off its effects. Previous shutdowns were associated with spikes in delinquency, but the most recent quarter’s data showed a bump of a mere 6 basis points in loans 31–90 days past due (DPD). This might be because it was a partial — as opposed to full — shutdown, but more likely it was the strength of the economy that convinced small businesses to stay the course for the quarter. In the famous words of James Carville, “the economy, stupid.”

Delinquency rates for businesses with fewer than 100 employees moved up in the first quarter, but more slowly than anticipated. The 31–90 DPD rate increased from 1.68 percent to 1.74 percent for the quarter. Using the previous government shutdown in the fourth quarter of 2013 as a guidepost, the recent shutdown could have bumped up delinquencies to over 2 percent. But as with the recent GDP number, which came in above expectations, we can see that the economy is resilient at the moment. Balances also grew at a nice year-over-year rate of 5 percent. This is slower than 2018’s rapid pace, but it’s still solid growth for this stage of the business cycle. All this bodes well for small-business lending for the remainder of the year.

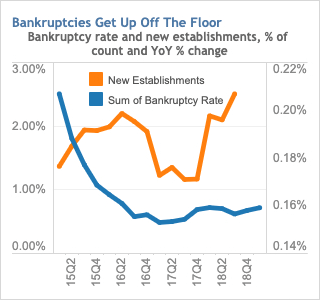

Small-business bankruptcies at small businesses picked up slightly in the first quarter of the year, coming in at just under 16 basis points. Although bankruptcy rates have left behind the floor they reached at 15 basis points, the current rate is a healthy one for the market. The establishment growth rate, which came in at 2.5 percent in the third quarter of 2018, means there are plenty of net new businesses to ensure a healthy market for business borrowing, despite income gains offsetting the need for many businesses to borrow.

The Senior Loan Officer Opinion Survey (SLOOS) rose from its fourth-quarter low in the first quarter, going from -10.8 to -10.1. This number looks at the net response of loan officers and discounts banks reporting steady demand. The trend is more informative than the quarterly value. A two-year moving average shows that the SLOOS trend has been negative since mid-2017. Despite fewer respondents reporting constant or declining demand, the commercial and industrial (C&I) lending trend shows that small firms are still not seeking to increase their financing. Small firms are working in a late-cycle expansion environment, but they need to make sure they don’t miss out on opportunities for a lack of capital. As the current expansion is long in the tooth, it will take more than old age to push the economy into the next stage of the business cycle.

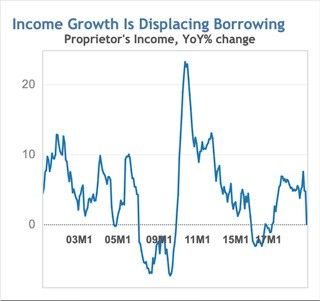

Small businesses are holding off on borrowing as slow but steady gains in proprietor income displaces the need for borrowing. Income gains for small-business owners have been steady since 2017, which has offset the need for greater borrowing. As the downward trend in income continues, businesses will seek alternative sources of capital and set the stage for small and medium-sized enterprise (SME) lending to pick up.

Moderate delinquency rates — defined as 31–90 DPD — came in mixed in the fourth quarter. Most regions saw a drop in performance, which is attributable to businesses in the construction industry. We use Bureau of Economic Analysis (BEA) regions in this report to reduce some of the noise that would be observed at the state level from quarter to quarter. This allows us to identify trends that are real and developing, rather than one-off events that may turn out to be false signals. The BEA regions we use are Far West, Great Lakes, Mideast, New England, Plains, Rocky Mountain, Southeast and Southwest.

Far West:

Moderate delinquencies in the Far West region held steady at 1.86 percent in the first quarter. Performance was mixed among industries in the region, but it’s notable that agriculture climbed down from the highs it hit in the fourth quarter, and construction performance continued a rise that has gone on for the better part of a year and a half.

Great Lakes:

Credit performance in the Great Lakes region continued to deteriorate in the first quarter, with 31–90 DPD delinquencies rising to 1.82 percent from 1.63 percent in the fourth quarter. Agriculture firms were hard hit as moderate delinquency (31–90 DPD) jumped from 55 to 65 basis points. This was a large move for agriculture delinquencies. Trade negotiations matter for farms in this region. Tensions high but the first quarter helped to ease conditions somewhat.

Mideast:

The Mideast had a mild first-quarter improvement with moderate delinquencies falling 1 basis point to 1.76 percent across all industries. More important was the decline in severe delinquencies, which fell 7 basis points to 3.44 percent. Digging into the details, the results aren’t as good. Most industries in the Mideast had rising delinquencies, but this was offset by corrections in mining and financial services, both of which were correcting from a fourth-quarter bounce.

New England:

New England’s small-business credit performance for the first quarter was up from the fourth quarter of last year, but down on a year-over-year basis. The moderate delinquency rate was a mild 1.48 percent. There was surprising consistency across industries — most held steady or had small declines in delinquent balances. Construction was the notable exception, with moderate delinquencies jumping from 2.99 percent to 3.54 percent. This was evenly split between the 31–60 and 61–90 DPD buckets, so construction firms in the region are moving into later stages of delinquency sooner than in other regions. This rate is still at a tolerable level for the construction industry, but the increasing shift into later-stage delinquencies bears watching going forward.

Plains:

The Plains region had a 31–90 DPD rate of 2.17 percent in the first quarter. Construction continues to suffer as the region is hit by storms and commodity prices. The saving grace here is that most construction delinquencies have been contained in the 31–60 DPD bucket and haven’t yet moved into the 61–90 or 91+ buckets. Most other industries saw increasing moderate delinquencies. Only transportation and retail saw mild pullbacks in delinquency rates.

Rocky Mountain:

Moderate delinquencies in the Rocky Mountain region rose in the first quarter, moving from 2.05 percent to 2.14 percent. This is roughly in line with year-ago levels and therefore isn’t concerning. Most industries experienced rising delinquencies, but the region was helped by growing balances, which muted the effects somewhat. If this continues, as the trend in proprietor’s incomes suggest is possible, the region will be able to carry on with expansion and reasonable performance.

Southeast:

The Southeast saw a slight increase in moderate delinquencies for the quarter, rising from 1.33 percent to 1.37 percent. This is in line with the year ago number and doesn’t tell us much about what’s happening on the ground. Construction bucked the national trend with a mild decrease. Combined with wholesale and retail, delinquent balances remained highly consistent from the quarter and year-ago periods. The Southeast continues to be the top-performing region, but as with all regions, it has pockets of weakness, which are becoming more difficult to tamp down as the business cycle progresses.

Southwest:

Delinquencies in the Southwest resumed their rise in the first quarter, reaching 2.2 percent. Manufacturing was a point of particular weakness, as moderate delinquencies rose from 2.63 percent to 3.11 percent. At 70 basis points above the year-ago level, manufacturing is a weak spot for the region. The trouble for manufacturing is in the 31–60 DPD bucket, which accounted for 40 basis points of the rise and could pose trouble again in the second quarter.

The risk outlook this quarter is weighted toward the positive, given recent moves by the Federal Reserve , and the beginning of a shift in construction patterns, but trade remains a source of consternation.

Following the stock market moves in the fourth quarter of last year and inflation data continuing to come in under target, the Federal Reserve shifted its stance this quarter to return to a wait-and-see posture for rate moves. This sent mortgage rates lower and stock prices higher and helped boost confidence. This has led Moody’s Analytics to lower projected rate hikes in 2019 to zero and look for hikes to resume in 2020. The economy is now all but assured to set a record this summer for the longest expansion in U.S. history, and small businesses should continue to see income gains and continue solid performance on their borrowings.

With trade tensions facing fresh escalation this remains a source of disruption and uncertainty for businesses. Chinese purchases of U.S. agriculture goods in the first quarter, helped alleviate some worry by helping to push up exports but this looks to have been a brief break in tensions. If an agreement is reached, it will go a long way toward helping farmers who were hurt by commodity prices following last year’s trade rhetoric escalation. Cautious optimism is warranted for now, but an agreement must come soon to avoid rising agriculture delinquencies in the Plains and Great Lakes regions.

The average price of new homes continued to trend down in the quarter. But this masks a positive underlying trend, since it’s the result of builders starting to move to more affordable starter homes. This will give more people access to the housing market. Although this will cause some pain for construction firms as margins are squeezed, downstream businesses like retailers and wholesalers stand to gain as the market for home goods increases. Still, housing is slowing as mortgages and homeownership remain out of reach for many people, which takes the wind out of the sails for construction firms.

Small businesses powered through the first obstacle of the year as they brushed off the government shutdown and forged ahead into the new year. In spite of the shutdown, performance came in at a reasonable level for the quarter, and balances rose. Overall, the year is starting off well, with positive news coming from the areas presenting risks to the outlook. The Federal Reserve announced a shift to a dovish stance, trade negotiations are progressing, and housing — though facing obstacles — has room to grow in the first-time buyer market. All told, 2019 looks set to be a decent year, characterized by slowing growth and modest performance fluctuations.

Developed by Experian, the leading global information services company, and Moody’s Analytics, the Experian/Moody’s Analytics Main Street Report brings deep insight into the overall financial well-being of the small-business landscape, as well as providing commentary around what certain trends mean for credit grantors and the small-business community as a whole. Key factors comprised by the Main Street Report include a combination of business credit data (credit balances, delinquency rates, utilization rates, etc.) and macroeconomic information (employment rates, income, retail sales, investments, etc.).

Experian’s Business Information Services is a leader in providing data and predictive insights to organizations, helping them mitigate risk and improve profitability. The company’s business database provides comprehensive, third-party-verified information on 99.9 percent of all U.S. companies. Experian provides market-leading tools that assist clients of all sizes in making real-time decisions, processing new applications, managing customer relationships and collecting on delinquent accounts. For more information about Experian’s advanced business-to-business products and services, visit www.experian.com/b2b.

Visit nowMoody’s Analytics helps capital markets and risk management professionals worldwide respond to an evolving marketplace with confidence. The company offers unique tools and best practices for measuring and managing risk through expertise and experience in credit analysis, economic research and financial risk management. By providing leading-edge software, advisory services, and research, including the proprietary analysis of Moody’s Investors Service, Moody’s Analytics integrates and customizes its offerings to address specific business challenges. Moody’s Analytics is a subsidiary of Moody’s Corporation (NYSE: MCO), which reported revenue of $3.5 billion in 2015, employs approximately 10,900 people worldwide and maintains a presence in 36 countries. Further information is available at www.moodysanalytics.com.

Visit nowExperian and the Experian marks used herein are service marks or registered trademarks of Experian Information Solutions, Inc. Other product and company names mentioned herein are the property of their respective owners.

© 2019 Moody’s Analytics, Inc. and Experian Information Solutions, Inc. and/or their respective licensors and affiliates (collectively, the “Providers”). All rights reserved.