How Do You Calculate Net Worth?

Quick Answer

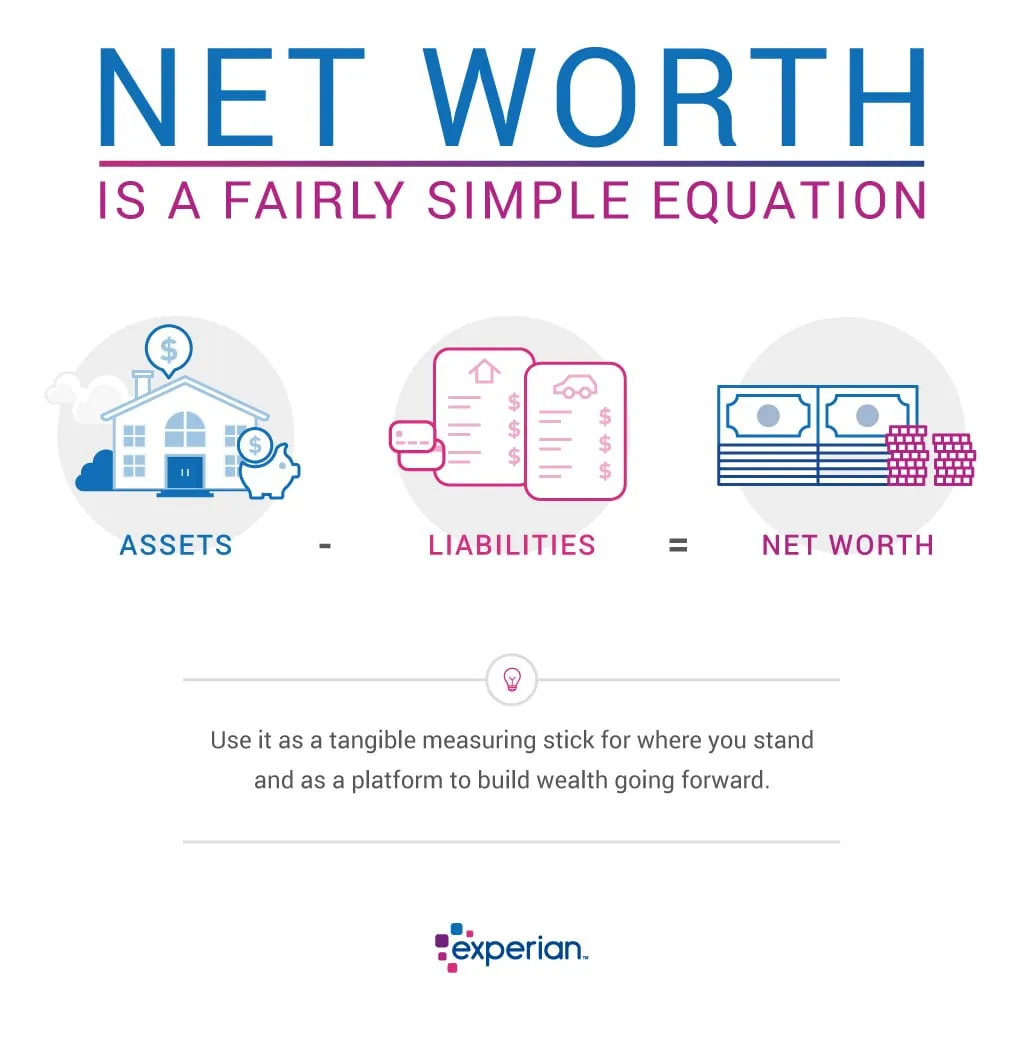

To calculate your net worth, subtract your liabilities from your assets. Liabilities are money you owe: debts, such as your mortgage or credit cards. Assets are any money you have in cash, bank accounts or property such as cars or a home.

Net worth is a snapshot of your full financial picture. To calculate your net worth, you subtract your liabilities from your assets. Knowing your net worth tells you how much wealth you have and can act as a gauge of how financially secure you are.

With a clear view of where you stand now, you may be more equipped to set and reach new financial goals. Here are steps you can take to find your net worth, plus how your net worth compares to the average for your age range.

What Is Net Worth?

Net worth tells you how much money (or valuable assets) you have if you subtract your debts from your assets. You can think of net worth as a measure of your overall financial health.

If your net worth is going up, then you're successfully paying off debts and adding to your savings. On the other hand, if your net worth is trending down, you may need to cut back spending and focus on saving or paying off debt.

Your net worth can also give you a sense of how ready you are to weather a future storm, such as a loss of income or unexpected expense. With more savings and less debt, you're on firmer ground to survive a financial emergency.

How to Calculate Your Net Worth

On a basic level, calculating your net worth just means subtracting your liabilities from your assets. But if you're not sure where to start, follow these steps to get your net worth number.

1. Choose a Date

Your net worth changes over time, so you'll need to decide on a specific date to calculate yours. This is especially important if you plan to calculate your net worth routinely. You should choose a date that gives you a solid reference to work with.

For example, you could choose to calculate your net worth at the start of every month. If you get paid monthly, you could build checking your net worth into your payday routine. This has the added benefit that gauging your financial health before you do your saving and spending for the month can help you make the most informed financial decisions.

2. Add Up Your Assets

Start by finding the value of all of your assets. You'll need to do some digging to ensure you're accounting for all your assets. Here are some things to be sure to include:

- Money you have in savings or investments

- The market value of your car

- The market value of your home

- Cash value of your insurance policy

- Other assets, such as jewelry or art

- Value of a business you own or have interest in

You may have to estimate the value of some of your assets if you're not sure. Also, when in doubt, it's a good idea to lean toward conservative estimates to avoid overestimating your net worth number.

Learn more: What Are Assets?

3. Add Up Your Liabilities

Next, you'll need to gather up all of your balances owed to find your total debt. Be sure to include the following:

- Your mortgage

- Auto loans

- Any credit card or personal loan balances

- Student loans

- Other loans, credit and any other purchases you're financing

- Money you owe to family or friends

Add up all of your liabilities to find your total liability figure.

Learn more: How Can I Find All My Debt?

4. Subtract Your Liabilities From Your Assets

Once you have figures for your assets and liabilities, plug them into this formula to find your net worth:

If calculating your net worth seems like a heavy lift, consider employing an app to do the work for you. Some budgeting apps (such as You Need a Budget) let you connect your financial accounts and then track your net worth for you automatically.

Learn more: How to Increase Your Net Worth

Net Worth Example

Here's an example of how calculating net worth works.

First, you need to find the total amount you have in assets. Let's say you have the following assets:

- Home value: $350,000

- Car's current market value: $20,000

- Money in savings: $15,000

- Money in 401(k): $100,000

Next, add up the value of your individual assets to find your total asset value.

- Total assets = $350,000 + $20,000 + $15,000 + $100,000 = $485,000

Next, find the sum of your liabilities. Say you have the following debts:

- Mortgage: $240,000

- Auto loan: $23,000

- Credit card balance: $7,000

To find your total liabilities, you would add these individual debts up:

- Total liabilities = $240,000 + $23,000 + $7,000 = $270,000

Last, subtract your liabilities from your assets to find your net worth number.

- Net worth number = total assets - total liabilities

- Net worth number = $485,000 - $270,000 = $215,000

Why Knowing Your Net Worth Is Important

Net worth gives you a big-picture view of your financial situation. Here are some reasons it's important.

It Can Provide Clarity

Net worth is one way to gauge your financial stability. With a clear sense of how you're doing now, you can more confidently set goals for what you'd like to change.

For example, you may have a solid emergency fund, which is a sign of financial security. But, on the other hand, you may also have high consumer debt balances. So, while looking at individual factors like your emergency savings, credit score or debt-to-income ratio give you pieces of your financial puzzle, net worth gives you a fuller picture.

It Can Motivate You

If your net worth is lower than you might like, seeing that information laid out clearly in front of you can be a motivating force. You can use the changes you'd like to see as motivation to set new savings goals and stick with them, or to pay off debt faster.

On the other hand, if your net worth is growing, you could let your success motivate you to branch out into investing more of your income to speed up that growth.

Learn more: How to Build Wealth

You Can Track Your Progress Over Time

Calculating your net worth tells you your current financial picture, but net worth fluctuates over time, especially if you pocket a windfall or make a large expenditure. Even small habits, like saving an extra $50 a month, impact the big picture.

So, think of your net worth as always in flux. Consider calculating it every month or so to see how it changes over time. If you notice your net worth decreases in a given month, that could be a sign to reel in overspending and get back on track. On the other hand, if your net worth is increasing, you know to keep it up.

What Is a Good Net Worth?

There's no one answer to what a good net worth is. The net worth number that you might aim for depends on where you are in your own financial journey.

If you're early on in your career, before you've had much time to build up savings, it's not unusual to have a low (or even below zero) net worth. As you approach retirement age, you want your net worth to grow so that you have ample savings to support you in retirement.

To understand what a good net worth might be, consider the most recent Federal Reserve Survey of Consumer Finances (SCF) report, which uses data from 2022.

| Age Range | Median | Average |

|---|---|---|

| All households | $192,900 | $1,063,700 |

| Younger than 35 | $39,000 | $183,500 |

| 35 - 44 | $135,600 | $549,600 |

| 45 - 54 | $247,200 | $975,800 |

| 55 - 64 | $364,500 | $1,566,900 |

| 65 - 74 | $409,900 | $1,794,600 |

| 75 or older | $335,600 | $1,624,100 |

Source: Federal Reserve Survey of Consumer Finances report, 2022 data

When reviewing how your net worth stacks up, keep this in mind: Looking at your range's median figure is likely to give you a more realistic picture than the average (because the median is less skewed by data from the wealthiest households).

Frequently Asked Questions

Looking Beyond Net Worth

Remember that everyone's financial story is personal—and made up of a lot more than just dollars and cents. So, while calculating your net worth provides one important view, there's more to consider.

Instead of focusing solely on your figure, think about what you hope to achieve by increasing your net worth. For instance, are you trying to secure financial freedom in retirement? Feel less burdened by financial stress? Open up the door to buying a home one day? Knowing why your net worth matters to you can help you cut through the noise and start new money habits to support your goals.

What makes a good FICO® Score?

Learn what it takes to achieve a good credit score. Review your FICO® Score for free and see what’s helping and hurting your score.

Get your FICO® ScoreNo credit card required

About the author

Evelyn Waugh

Evelyn Waugh is a personal finance writer covering credit, budgeting, saving and debt at Experian. She has reported on finance, real estate and consumer trends for a range of online and print publications.

Read more from Evelyn