Report

Published May 25, 2023

Commercial Commercial InsightsQ1 GDP grew by 1.1% annualized, following a 2.6% gain in Q4 2022. However, recent data's accuracy is affected by weather-induced consumer spending and unusual seasonal adjustments. Notably, Q1 GDP doesn't reflect the impact of tightened lending standards yet. The core of the economy, measured by real final sales to domestic purchasers, rose by a solid 2.9% annualized, driven by strong consumer spending concentrated in early Q1 and aided by significant cost-of-living payments. Inventory reduction subtracted 2.3ppts from Q1 GDP growth, and this trend is expected to persist as businesses draw from existing stockpiles to meet demand. The Oxford Economics US Business Cycle Indicator declined for two consecutive months, indicating weak Q1 performance. The indicator suggests feeble Q2 growth and a possible H2 2023 recession.

Download the report

View now Video

Video

Rising Delinquencies Signal Growing Risk in Transportation & Warehousing

As the U.S. economy continues to recalibrate post-pandemic, the transportation and warehousing segments of the logistics sector are signaling caution. While the broader logistics industry has remained in expansion mode, Experian’s latest Commercial Pulse Report reveals that delinquencies are rising—an early warning of growing risk in two of the economy’s most critical subsectors.

Check out the full report to see how these trends could impact your strategy!

Video

Video

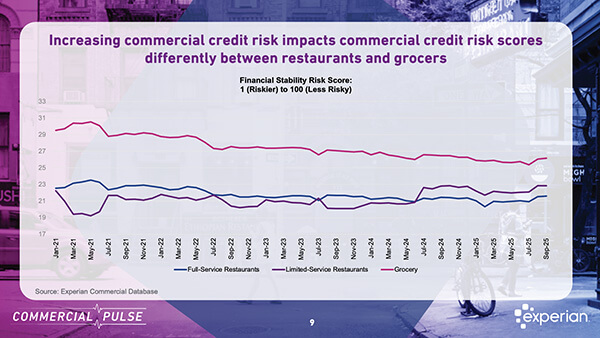

Under Pressure: How Rising Food Costs Are Changing Restaurant Credit Behavior

Experian’s latest Commercial Pulse Report dives into the financial health of the restaurant sector amid rising costs and shifting consumer behavior.

Key insights:

- Menu prices at Full-Service Restaurants rose 4.6% in August — outpacing inflation.

- Limited-Service Restaurants are showing improved credit risk scores, suggesting stronger adaptability.

- Credit access is tightening across the board, with average credit limits falling below $6,000.

- Revolving credit utilization is climbing — an early signal of potential cash flow strain.

What does this mean for lenders and decision makers?

✅ Not all restaurant types face the same risks.

✅ Segmenting credit strategies is more important than ever.

✅ Watch utilization and inquiry trends closely — they may be early indicators of distress.

Check out the full report to see how these trends could impact your strategy!

Video

Video

Credit Signals in Construction: Early Warnings for Lenders and Risk Leaders

The construction industry has experienced significant growth over the last seven years, but fresh data reveals mounting signs of financial stress that commercial lenders and Chief Risk Officers should be closely monitoring.

Check out the full report to see how these trends could impact your strategy!

Video

Video

How Small Businesses Have Changed Since the Pandemic

According to Experian’s latest Commercial Pulse Report, business formation remains strong:

- 471,000 new business applications were filed in July alone

- Between 2018 and 2023, the number of new businesses establishing commercial credit rose by 38%

- New businesses today look more financially stable than those from earlier years

What’s driving this resilience?

👉 Faster tech adoption

👉 Hybrid business models

👉 Stronger financial fundamentals

The pandemic forced small businesses to transform at record speed. Now, they’re leveraging those lessons to build smarter, more adaptable enterprises.

Check out the full report to see how these trends could impact your strategy!