Improve Insurance Customer Experience with Application Prefill

Sip and Solve™ 15-Minute Webinar

Sip and Solve™ 15-Minute Webinar

Commercial insurance underwriting has traditionally been a labor-intensive and complex task for insurers. With the rise of automation, ingestion of non-traditional data, and advancements in technology, insurers are adding value to their business while redefining the role of underwriters. In this 15-minute Sip and Solve talk, Heath and Darren from our Insurance team talk about how Experian is helping insurers enhance their underwriting workflows with solutions like Application prefill, scores, predictive models, and nontraditional data.

[Darren]: Hi, everyone. And welcome to another Experian Sip and Solve. If you are new to these sessions, we share some of the insights and learnings we've developed working with our clients around understanding their commercial customers. I'm Darren Dunda, a Data Consultant with Experian Business Information Services. Today I'll be working with Heath Foley, our Insurance lead, talking about digitalization and how it can help improve the commercial insurance customer experience and the application process.

As is traditional with our Sip and Solve, we both have a cup of coffee in front of us that will be sipping throughout the session. Hopefully, you have something good in front of you as well. Since we have about 15 minutes for this coffee break, we'll jump right into it.

Heath, thank you for joining me today and sharing your years of experience of working with commercial insurance customers.

[Heath]: Darren, thanks for having me. I look forward to the discussion.

[Darren]: Digitalization and seeking a better client experience have been a rising trend for many years now. And with the onset of COVID, new technologies, and customers just demanding a better client experience, this has really started to accelerate the movement. How have you seen this trend with your customers in the commercial insurance space?

[Heath]: I've seen it pick up a lot over the last three years, you know? Right around when COVID began, we started to hear a lot more about what we can do by streamlining the process and making it easier to do business with the clients, with the insurers, and with the brokers, wherever they sit within the ecosystem. So digitization has just really exploded. And as we're talking to, you know, executives within our client base, it always seems to be one of the top, if not the top, the second or third top priorities within each organization.

[Darren]: I've seen pretty much the same with my insurance customers as well, and while onboarding new clients will always be multi-channeled also, you'll see phone-based, email-based, and a lot of other access points to getting applications in. I think digital is where I've seen the most lift for most carriers. It's really around automation and a straight-through process that they can use with this kind of digital experience.

I should point out that when we talk at work, as we're talking about this automation and the straight-through processing and a better client experience, it's not just for the clients; the end client who is buying the policy. We're also talking about agents. We're trying to onboard these customers with carriers. Is that pretty much what you've been seeing? Also Heath?

[Heath]: Yes, because we see our carrier clients going, to market in a variety of different ways, whether they're going through a direct channel, whether they're going through independent agents or exclusive agents. We see a lot of other distribution channels. In addition to just working with carriers, we also work with many brokers, MGAs MGU's out there in the market, so we support many different clients. So it depends on where they sit within that ecosystem and how we can help to streamline and digitize the process.

[Darren]: Heath on the screen is an industry quote that mirrors some of what we're seeing. And it points out how critical insurance carriers must have a robust digital customer experience. With all the numerous digital tools like APIs, real-time quotes, and automation. What do you see is gaining the most focus from your clients?

[Heath]: APIs are the key. We see more clients wanting to consume the data via API's. At Experian, we have our our Developer Hub, which is an easy-to-use tool that enables you to go in and take a look at the APIs to easily be able to test those and see how they could work in your environment. I would say that's the number one focus. When we're talking about integrating our data to help clients streamline their processes, it's all API driven at this point.

[Darren]: I agree; for the clients I'm working with, that API real-time connection and the data that they're able to get that paints a clear picture for their customers, and a clear view of the risk involved in those customers is what they're all focusing on right now.

We've talked a little bit about what the carriers are looking for. Let's discuss the why. What are the issues your clients are talking about and what are they trying to overcome to get a better customer or agent experience?

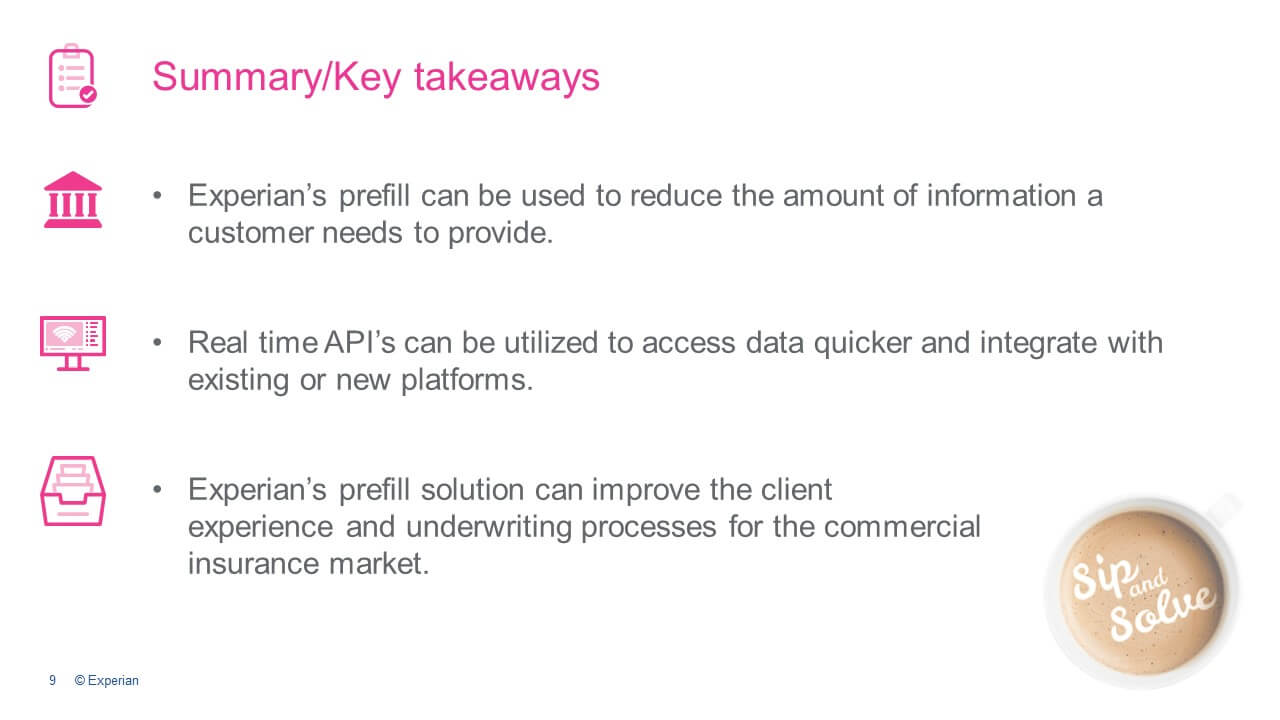

[Heath]: A lot of it's about speed. It's about being able to turn a quote in a timely fashion, making it easy for the insured or the broker to fill in information when they're looking at things such as a prefill. So not having to ask for 40 pieces of information, what can we do to eliminate some of that? So they can type in the name of the business, the address, city, state, and zip, and be able to populate as much information as possible.

And then also when you're utilizing a third-party data provider, you're able to look at and reduce errors in typing because you don't have to fill out as many of the fields in an application, for example. Anything that can be done from a speed and turning the process around in a much timelier fashion makes the overall customer experience so much smoother. It also helps to eliminate any friction within that process, and I know carriers are trying to focus on eliminating, friction moving forward.

[Darren]: I also hear about that challenge of buying a quote time with brokers going to the fastest carrier to provide a policy. Heath, as you said, it's about error reduction, data verification, premium leakage, avoidance, and then quick responses, and prefill addresses all of these issues, correct?

[Heath]: Correct. You know, prefill has been something that has been talked about and leveraged a lot over the past few years, but we continue to see more and more in this area.

Clients ask us what we can do to reduce the number of keystrokes. Because often, if it's an individual business going into a direct carrier, they start typing in information and are asked for all of this information. They could get distracted and leave. So to avoid abandonment from an application, for example, anything we can do from a data company perspective to help our carriers provide a more straightforward, easier way to do business. It enables that process and ensures just a more streamlined process for the carriers.

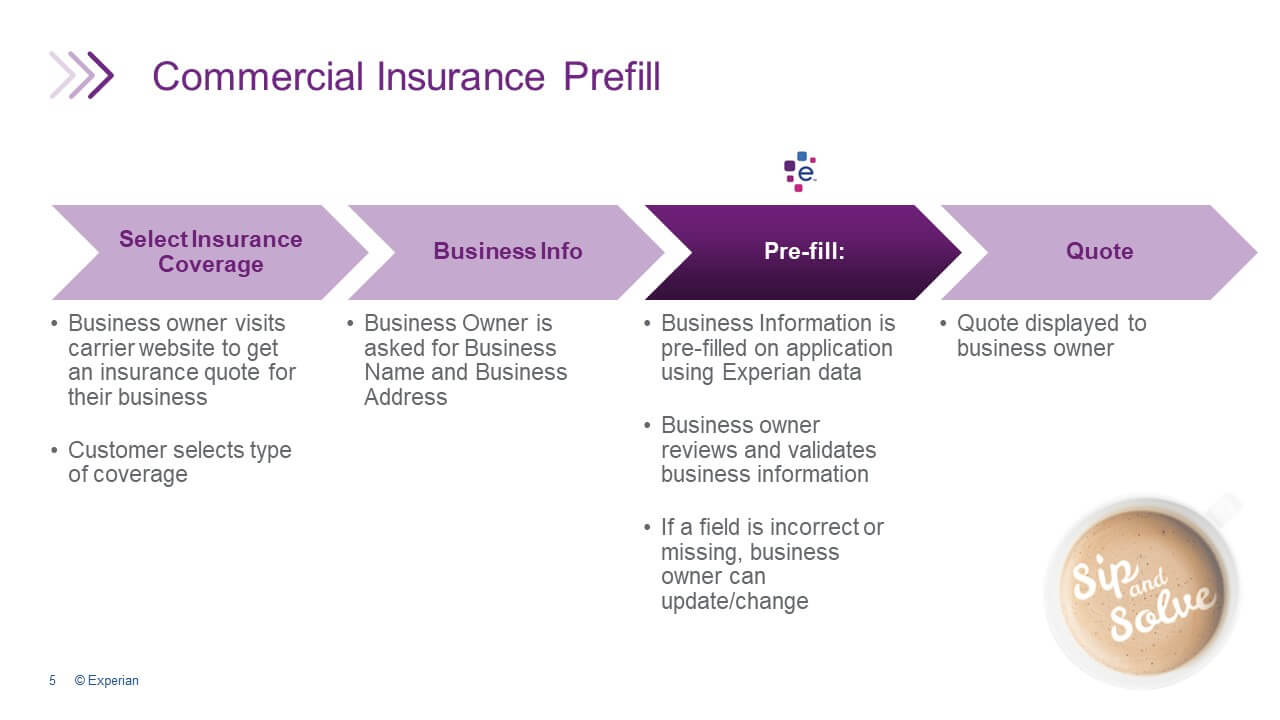

[Darren]: And prefill is a simple process. It starts with the agent or the customer coming to a website or an onboarding portal, filling in and picking a kind of coverage they want, and then filling in five pieces of data. For example, the name of the company, address city, state, and zip, and from there, Experian can return a match for that company that the owner or agent can confirm. "Yes", that's the company that I am. And once that confirmation goes through, the actual quote process can start. It alleviates the need for the client or agent to keep a lot of information already known and in the Experian database.

[Heath]: You're exactly right. It works; it's that simple. And, you know, especially with the API's and the platforms and tools out there that are mostly API enabled, it allows a straightforward process to do that.

[Darren]: Since we're talking about the data, can you address the standard data elements you would get for a prefill and the data that the underwriters can get on the backside to help them make their decision?

[Heath]: Absolutely. Here are a few examples. We start to look at prefilling a lot of information on the business. So being able to prefill things such as website URL, tax ID, the industry they're in, the number of employees, and annual sales. Various kinds of information can be prefilled as we look at some corporate registration details and business contact information.

There are several different ways that we can prefill this data. From an Experian perspective, we've got 700 to 800 other variables when we call from our core data. We've got a lot of alternative data that's outside of that. So there's just a variety of different types of data and types of variables that, that we can help prefill. What's great about that is the API hub that I talked about earlier; it shows and displays all of the different opportunities you can look at in prefilling data.

[Darren]: And the data for the prefill is the identification information, and on the backside, with that once it's verified, and it goes to the actual quoting process, the agents get the decisioning type data.

[Heath]: Correct, because risk data is core to what we do. So we work with our carriers and provide risk data to help with underwriting, help underwriting and pricing, and being able to help make those decisions in a much faster way. So, in addition to prefilling the data with some of the different variables we were showing. We can also append that to risk data, primarily how clients utilize our data. So they can put that whether they're using our models or their underwriting models, but Experian data can fuel that whole process.

[Darren]: Prefill really provides three critical solutions.

1) It's frictionless to get the five pieces of data to get access to the client information that's already in the Experian database.

2) It provides speed in creating faster and more accessible customer experiences with real-time data through our API's.

3) The data itself, decisioning data, and analytics to make informed underwriting decisions.

Heath, Prefill reduces the unknowns, errors, and application abandonment you mentioned earlier, all of this from the process, and enables the underwriters to do their jobs more efficiently.

[Heath]: Absolutely. Data is such an important piece of the insurance business. And as I'm sure you all know, providing more data to carriers to help with, whether it's the underwriting or pricing process, or just in the front end, reduces the friction in the process. So there are various ways that Experian data can help support your business to help reduce the friction within that overall process. Because again, it gets back to speed. Speed is the key, you know; being able to turn those quotes around, making the best decision on those quotes and the pricing decisions to get that information back promptly maximizes your growth opportunities.

[Darren]: And we should point out that data consultants — integration experts like myself are standing by to help customers get through this process, which is all included in this API setup.

[Heath]: We really go in and look at the entire process. Where is data coming into the organization? How is it coming into the organization? What are the different work streams that come through? Then make recommendations on how our data can support it. It's a real collaborative effort. And the more that we know from our clients or prospects that we're working with about that process, the more we can make the best recommendations. And then once we determine the variables or the information you need, we've got a team on the back end that can help with API deployment and help with some of the technical pieces that go along with that.

[Darren]: Ok, so we discussed the standard Pre-fill in underwriting. You touched a little bit on the alternate data. Can you elaborate on what alternate data is coming through our API's that our insurance carriers are using today?

[Heath]: So we're doing a lot around property data. Experian offers social media data, and that gets leveraged a lot. For example, some of the variables we include with social media data are hours of operation. It is also more accessible to determine if a business falls outside traditional NAICS codes. Also, the ability to understand a business is a bar or a breakfast restaurant. For example, do they have a liquor license?

So there's a variety of different variables that can be leveraged. OSHA data's another area for people doing more with their workers' comp that we see more and more. One thing I'll say is we continue to add new data to our API hub. So our clients can, can review that and be able to see other opportunities out there. And if we don't have the data, we can often go out and create some new data connections.

[Darren]: Well, that's all we have for you today. I want to thank Heath for joining us and sharing his time with us. And, of course, we'd like to thank our audience for spending their coffee break with us. Hopefully, some of the key takeaways from Heath's insights on prefill can help your company and your organization with your customer experience improvement efforts for your commercial lines of business. If you have any questions and want to learn more about what we've discussed today, feel free to use our link to our private Facebook group to join us and chat with us.

Also, if you want to get notified of future Sip and Solve's, make sure you're subscribed by joining the list here, and again, thank you for sharing your coffee breaks with us. And now it's time to go back to work.

Heath Foley works in Experian’s Business Information Services Group, supporting insurance clients. In this role, Heath leads a sales team that enables insurance organizations to manage risk and drive profitable growth more effectively.

Heath has spent the past 25 years working in the Data and Analytics Industry, providing solutions that help organizations manage risk, streamline processes, and grow top-line revenue with insights provided through data.

As a Senior Consultant, Darren empowers Experian Business Information Services clients to address strategic data challenges to reach their business goals. His tenure at Experian has enabled him to develop deep experience in improving processes and providing solutions in credit, marketing, procurement, fraud/KYC/AML, decisioning, and analytics.

To be notified when we schedule more Sip and Solve webinars.

This site is protected by reCAPTCHA and the Google Privacy Policy and Terms of Service apply.